You file on time, you keep good records, and you still worry about that letter in the mail. That is normal. The IRS relies on data matching and risk flags to decide who gets extra scrutiny. Here are the 10 Common IRS Audit Triggers to Avoid, why they happen, and how to lower your risk. UK readers will find a quick HMRC note under each point to help you spot similar red flags.

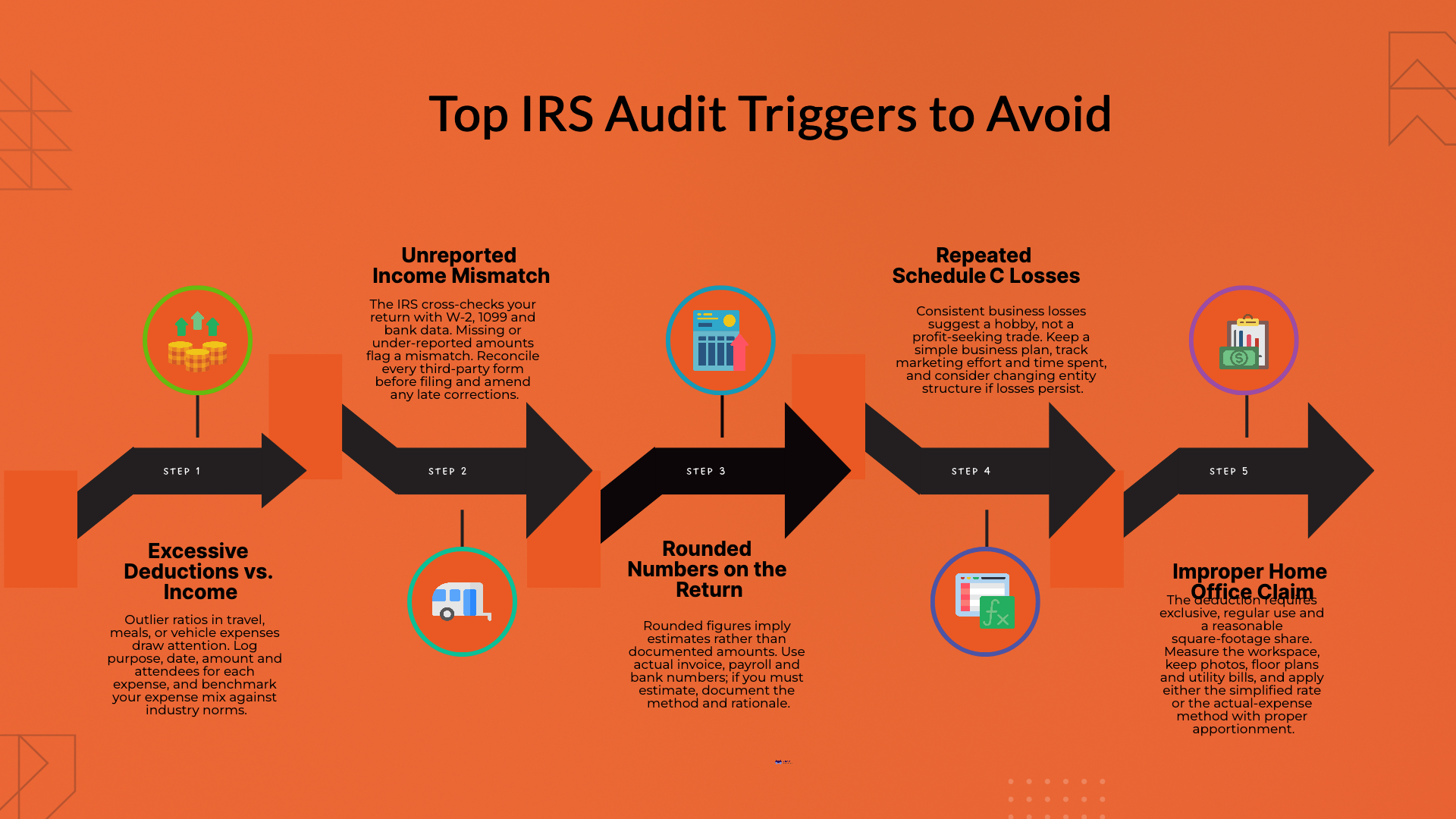

Why it triggers. The IRS matches your return to forms like W-2, 1099-NEC, 1099-K, 1099-INT, and 1099-DIV. Missing or underreported income is a direct mismatch.

How to mitigate. Track every payor form before filing. Reconcile bank deposits to 1099 totals. If you receive a late or corrected form, file an amended return.

UK note. HMRC uses RTI and bank interest feeds in a similar way. Check P60, P11D, and interest summaries.

Why it triggers. Repeated losses suggest a hobby rather than a trade. The IRS expects a profit motive and reasonable business conduct.

How to mitigate. Keep a simple business plan, track marketing, time spent, and pricing. Capitalize or depreciate assets correctly. If losses continue, consider an entity change.

UK note. HMRC challenges loss relief where there is no commercial basis.

Why it triggers. Outlier ratios in categories like travel, meals, and vehicle expenses stand out in IRS norms for your industry and income level.

How to mitigate. Log purpose, date, amount, and attendees for meals and travel. Use a mileage log. Benchmark your expense mix against prior years and trade peers.

UK note. The “wholly and exclusively” test applies. Keep receipts and a mileage log.

Why it triggers. Many rounded amounts signal estimates rather than records.

How to mitigate. Record actual figures from invoices, payroll reports, and statements. If you must estimate a minor item, document the method.

UK note. Same principle. HMRC expects precise entries supported by evidence.

Why it triggers. The IRS looks for exclusive and regular use, plus a sensible square-footage share.

How to mitigate. Map the workspace, measure square feet, and keep photos and a floor plan. Use either the simplified rate or the actual-expense method with bills and apportionment.

UK note. Use HMRC’s simplified expenses or a reasonable apportionment with bills and meters.

Why it triggers. The IRS checks for control, integration with your business, and financial dependence. Misclassification shifts payroll taxes off the employer.

How to mitigate. Use written contracts, clear scopes, and vendor invoices. Avoid employee-like schedules, tools, and supervision for contractors. Issue 1099-NEC when required.

UK note. Watch IR35 and employment status tests. Contracts and working practices must align.

Why it triggers. Noncash donations and gifts over substantiation thresholds get attention.

How to mitigate. For cash gifts, keep bank proof and receipts. For noncash over the applicable limit, obtain qualified appraisals and complete Forms 8283 as needed. Confirm the charity’s status.

UK note. Keep Gift Aid records and charity confirmations.

Why it triggers. Businesses must report cash receipts of ten thousand dollars or more using Form 8300. Missing reports or patterns around the threshold raise questions.

How to mitigate. Train staff, file Form 8300 on time, and maintain ID records. Separate cash logs from card settlement reports.

UK note. HMRC monitors cash-intensive trades and has similar expectations on AML controls.

Why it triggers. The passive loss rules limit deductions unless you qualify as a real estate professional or meet participation tests.

How to mitigate. Track hours and activities. Keep a participation log. Separate property records and elections. Match depreciation methods to asset classes.

UK note. Relief is limited for UK property losses in several cases. Keep a ledger per property.

Why it triggers. Foreign accounts and interests carry special filings such as FBAR and FATCA forms. Missing forms draw fast attention.

How to mitigate. List all accounts, peak balances, and ownership. File FBAR and Form 8938 if thresholds apply. Coordinate with any UK reporting to avoid double disclosure gaps.

UK note. UK residents must declare worldwide income. Use the appropriate foreign pages and keep bank statements.

Most audits start with mismatches and outliers. If your numbers tie to third-party reports, your deductions are documented, and your positions follow clear rules, your return looks ordinary. Ordinary is good. Build simple habits around reconciliation, logs, and evidence, and you reduce both risk and stress.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.