.png)

You've just sold an investment property for a significant profit. While you're celebrating the sale, you realize that capital gains tax on the sale could claim 15% to 20% of your proceeds, or even more when you factor in state taxes and the 3.8% net investment income tax. For many real estate investors, this tax burden can wipe out a substantial portion of their gains.

A 1031 exchange, also known as a like-kind exchange, allows real estate investors to defer capital gains taxes by reinvesting the proceeds from the sale of an investment property into another like-kind property. Named after Section 1031 of the Internal Revenue Code, this powerful tax strategy enables investors to defer capital gains taxes indefinitely, allowing them to preserve wealth and continue building their real estate portfolio.

In this guide, you'll learn exactly how a 1031 exchange works, the strict timelines you must follow, common pitfalls to avoid, and actionable strategies to maximize your tax savings while staying compliant with IRS rules.

A 1031 exchange is a tax-deferred transaction that allows real estate investors to sell an investment property and reinvest the proceeds into a replacement property of like-kind without immediately paying capital gains taxes. The exchange must be completed within specific timeframes and follow strict IRS guidelines outlined in IRC Section 1031.

The Tax Cuts and Jobs Act of 2017 significantly changed the scope of 1031 exchanges. Previously, the provision applied to both real and personal property. Starting in 2018, Section 1031 exchanges are limited to real property held for investment or business purposes. This means you can no longer exchange personal property like equipment, vehicles, or artwork under Section 1031.

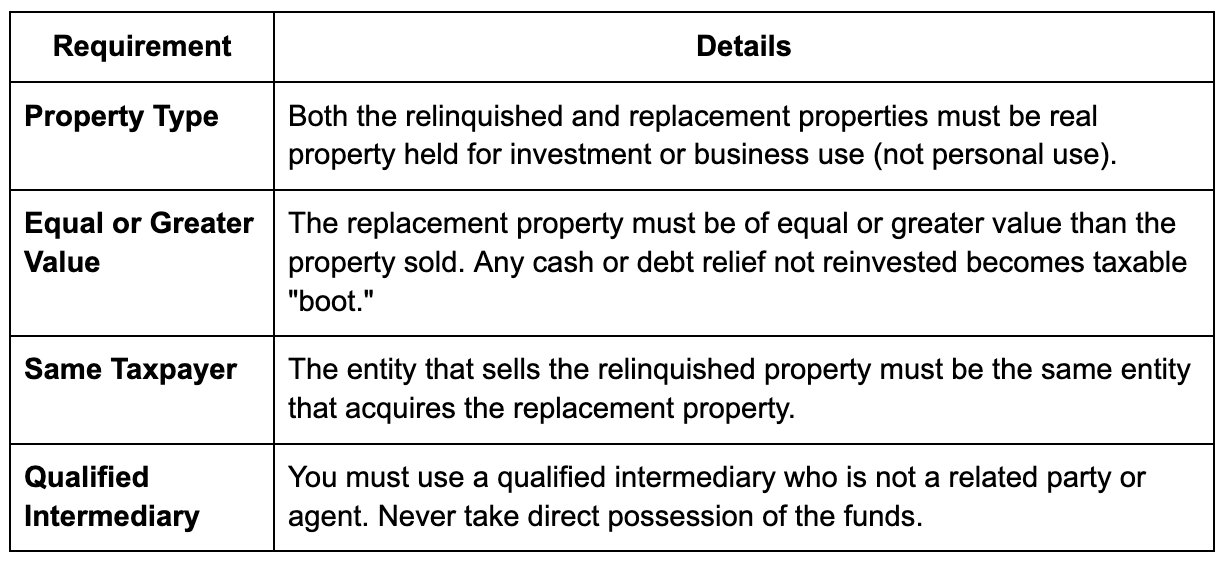

The key phrase here is like-kind properties. According to the Internal Revenue Service, like-kind refers to the nature or character of the property, not its grade or quality. In practical terms, almost any type of real estate held for investment can be exchanged for another type of investment real estate.

However, your primary residence does not qualify for a 1031 exchange, as it must be property held for investment or business use.

A 1031 exchange involves several critical steps and strict deadlines that must be followed precisely to qualify for tax deferral. Here's the complete process:

You cannot simply sell your property, pocket the cash, and then buy another property. The IRS requires that you use a qualified intermediary (also called an exchange accommodator) to facilitate the exchange. The qualified intermediary holds the proceeds from the sale of your relinquished property and uses them to purchase the replacement property on your behalf.

This is critical: If you take actual or constructive receipt of the sale proceeds at any point during the exchange, the transaction is disqualified, and you'll owe capital gains taxes immediately.

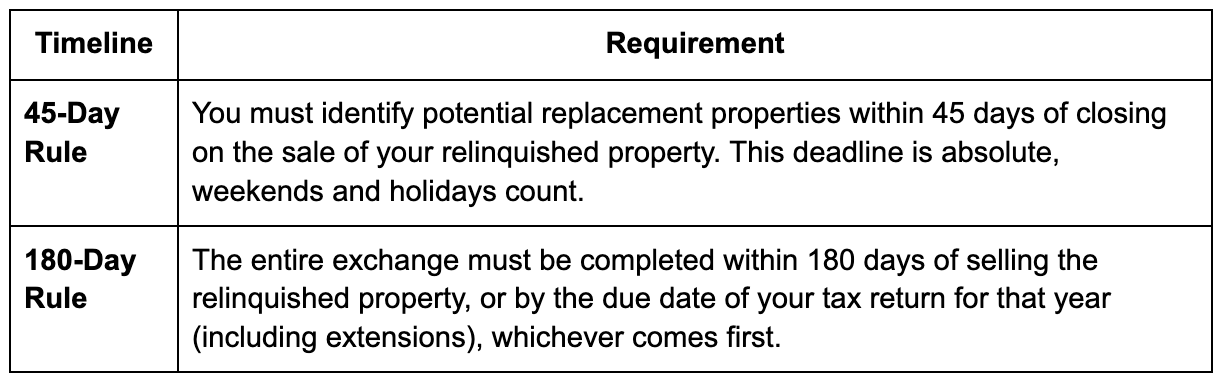

The 1031 exchange operates on two strict, non-negotiable timelines that run concurrently:

Identification Rules

There are three identification rules you can use when identifying replacement properties within 45 days:

Three-Property Rule: Identify up to three properties regardless of their value

200% Rule: Identify any number of properties as long as their combined value doesn't exceed 200% of the relinquished property's value

95% Rule: Identify any number of properties of any value, but you must acquire 95% of the total value identified

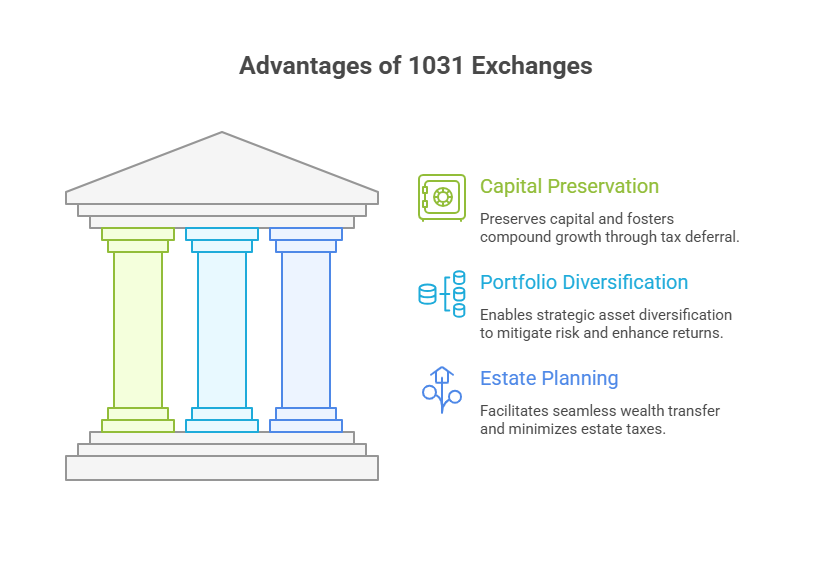

The 1031 exchange offers several powerful advantages for real estate investors looking to build and preserve wealth:

By deferring capital gains taxes, you keep more capital working for you. Consider this example: If you sell a property for a $500,000 gain and face a 20% federal capital gains tax plus a 3.8% net investment income tax, you'd owe approximately $119,000 in taxes. With a 1031 exchange, you can reinvest that entire $500,000 into your next property, giving you significantly more purchasing power.

Over multiple transactions, this tax deferral creates a compounding effect. Many investors use tax planning strategies for small businesses to maximize these benefits across their entire investment portfolio.

A 1031 exchange allows you to shift your real estate portfolio without tax consequences. You might consolidate multiple smaller properties into one larger property for easier management, or diversify a single property into multiple properties across different markets. This flexibility is invaluable for adapting your strategy as markets change.

When you pass away, your heirs receive a step-up in basis on inherited property. This means the deferred gains from your 1031 exchanges are essentially forgiven. Your heirs inherit the property at its current market value, and all those years of deferred capital gains taxes disappear. Combined with proper fractional CFO services for strategic tax planning, this creates a powerful wealth transfer strategy.

To qualify for a 1031 exchange, you must meet several strict requirements. Here's what the IRS requires:

Even experienced investors make costly errors with 1031 exchanges. Here are the most common pitfalls and how to avoid them:

This is the most common mistake. The 45-day deadline is strict, no extensions are granted, even if the 45th day falls on a weekend or holiday. To avoid this trap, start identifying potential replacement properties before you even close on the sale of your relinquished property.

"Boot" refers to any cash or debt relief that is not reinvested in the replacement property. If you sell a property for $1 million and only reinvest $900,000, that $100,000 difference is taxable boot. Similarly, if you're relieved of more debt than you take on in the replacement property, the difference is taxable.

If you acquire a replacement property intending to convert it to personal use or a primary residence shortly after the exchange, the IRS may disqualify the transaction. The replacement property must be held for investment or business purposes. While there's no specific holding period requirement, most tax professionals recommend holding the property for at least one to two years to demonstrate investment intent.

Your qualified intermediary cannot be someone who has acted as your agent within the past two years. This includes your real estate agent, attorney, accountant, or investment banker. Choose an independent, experienced qualified intermediary with proper bonding and insurance.

When you exchange depreciable real property, you must be aware of depreciation recapture rules. While a 1031 exchange defers capital gains taxes, any depreciation you claimed on the relinquished property carries over to the replacement property. Understanding Section 179 and bonus depreciation strategies can help you maximize tax benefits across your portfolio.

No, a 1031 exchange is only available for investment property or property held for business use. Your primary residence does not qualify. However, you may be able to use the Section 121 primary residence exclusion, which allows you to exclude up to $250,000 ($500,000 for married couples) of gain from the sale of your primary residence if you've lived there for at least two of the last five years.

If you miss either deadline, your exchange is disqualified, and you'll owe capital gains taxes on the sale of your relinquished property. There are no extensions or exceptions to these deadlines. The only way to avoid this is to plan ahead and work with an experienced qualified intermediary who can guide you through the process efficiently.

Yes, you can exchange one property for multiple replacement properties, or multiple properties for one replacement property. As long as the total value of the replacement properties is equal to or greater than the value of the relinquished property, and you follow all 1031 exchange rules, the transaction qualifies for tax deferral.

Yes, using a qualified intermediary is mandatory for a valid 1031 exchange. You cannot take possession of the sale proceeds at any time during the exchange. The qualified intermediary holds the funds and facilitates the transaction to ensure compliance with IRS regulations. Choose an intermediary with experience, proper insurance, and a solid track record.

No, Section 1031 requires that both the relinquished property and the replacement property be located within the United States. Real property in the United States is not like-kind to real property outside the United States. If you're considering international real estate investments, consult a tax professional about alternative strategies.

Almost all types of real estate are considered like-kind to each other for 1031 exchange purposes. You can exchange residential rental properties for commercial buildings, raw land for apartment complexes, or office buildings for industrial warehouses. The key is that both properties must be real property held for investment or business use.

There's no limit to the number of 1031 exchanges you can complete. Many real estate investors use this strategy repeatedly throughout their investing career, continuously deferring capital gains taxes while building wealth. Some investors complete dozens of exchanges over their lifetime.

A reverse 1031 exchange allows you to acquire the replacement property before selling your relinquished property. This is useful in competitive markets where you need to act quickly to secure a desirable property. An exchange accommodation titleholder (EAT) temporarily holds title to either the relinquished or replacement property while you complete the exchange. Reverse exchanges are more complex and expensive than standard exchanges but offer valuable flexibility.

A 1031 exchange is one of the most powerful tax-deferral strategies available to real estate investors. By reinvesting the proceeds from one investment property into another like-kind property, you can defer capital gains taxes indefinitely, preserve more capital for growth, and build a more valuable real estate portfolio over time.

The key to success is careful planning, strict adherence to IRS deadlines, and working with experienced professionals. Start identifying potential replacement properties early, choose a reputable qualified intermediary, and ensure your replacement property is of equal or greater value than your relinquished property to avoid taxable boot.

At Madras Accountancy, we've helped real estate investors navigate complex 1031 exchanges since 2015. Our team provides comprehensive tax planning services to ensure your exchange complies with all IRS regulations while maximizing your tax savings. Contact us to discuss how a 1031 exchange can fit into your overall investment strategy.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.