.png)

Running a C corporation comes with serious responsibilities, and IRS Form 1120 is one of the big ones. But every year, thousands of businesses miss the business tax deadline, triggering late fees, interest charges, and worse, audit risk.

And here's the catch:

The Form 1120 due date isn't the same for everyone. Calendar-year corporations have one deadline. Fiscal-year filers have another. And if you're counting on a 6-month extension of time to file, you still need to act before the original due date, not after.

This article breaks it all down for 2025:

If your business files Form 1120, missing a deadline isn't just a paperwork issue, it's a risk to your cash flow and compliance status. Let's make sure you get it right.

If your business operates as a C corporation, Form 1120 is one of the most important tax forms you'll file each year. Officially titled the U.S. Corporation Income Tax Return, this IRS form is used to report corporate income, claim deductions and credits, and calculate the total federal income tax due to the government.

But not every business needs to file Form 1120, and missing it can result in costly penalties. Here's a clear breakdown of who needs to file, what the form includes, and why it matters.

You're required to file Form 1120 if your business is:

This includes corporations in all industries, from tech startups to holding companies and real estate entities. The corporation must file form 1120 as an information return to the IRS, documenting all business income and activities for tax purposes.

Important: Businesses taxed as S corporations should file Form 1120-S, not Form 1120. Partnerships typically file Form 1065, and sole proprietors file Schedule C with their individual income tax Form 1040.

Form 1120 gives the IRS a full financial snapshot of your corporation for the tax year. It includes:

The form also asks for:

💡 Why it matters: The IRS uses Form 1120 to assess whether your corporation has complied with tax law, underpaid tax, or qualifies for credits. It's also a key document in the event of an audit.

Failing to file Form 1120 on time, or filing an incomplete return, can lead to:

Even if your corporation made zero revenue, you still need to file Form 1120 to stay in compliance. Many businesses find that working with a tax professional during filing season helps ensure they meet the business tax deadline requirements.

Filing deadlines aren't just about avoiding penalties, they also help you plan cash flow, tax strategy, and financial reporting. For the 2025 tax year, here's exactly when Form 1120 is due, how extensions work, and what to watch out for.

For calendar-year C corporations (those whose fiscal year ends December 31, 2024), the Form 1120 due date is Monday, April 15, 2025.

This is the standard federal tax return deadline, and it applies to the vast majority of small and mid-sized C corps during the 2024 tax year.

However, if your corporation follows a fiscal year (not the calendar year), the due date for filing is:

The 15th day of the 4th month after the end of its tax year.

📌 Example: If your corporation's tax year ended on June 30, 2024, your Form 1120 would be due by the 15th day of October 2024.

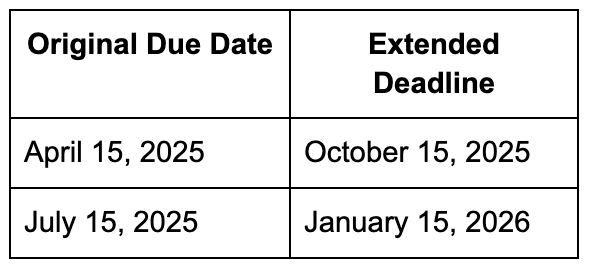

Need more time? The IRS allows corporations to file Form 7004 to request an automatic extension of time to file.

Here's what that looks like:

⚠️ Important: An extension gives you more time to file, not to pay. Any corporate tax owed is still due by the original deadline (April 15, 2025 for calendar-year filers), or you'll face late payment penalties and interest. Even if you file Form 4868 or making an automatic extension of time request, payments are due by the original due date of the return.

Filing a return isn't just another tax chore, it's a legal responsibility that directly impacts your corporate compliance, penalties, and potential audits. Whether you're running a C corporation or a closely held startup, this step-by-step guide will walk you through how to file your 1120 return accurately and confidently.

Before touching the form, ensure your books are closed for the tax year. The IRS expects a clear and accurate snapshot of your business activity.

You'll need:

🧠 Tip: Even if your business didn't generate profit, you're still required to file Form 1120. A tax professional can help with preparing your tax return to ensure all information to the irs is accurate and complete.

Form 1120 is available as a fillable PDF on the IRS website, but many corporations use specialized software or a tax preparer to simplify filing.

Popular options include:

Tax software can auto-fill key calculations and reduce common arithmetic errors, but it still requires you to understand your numbers. Electronic tax filing systems can streamline the process when filing your return.

Here's a breakdown of the major sections you'll need to complete:

Page 1 – Basic Info + Tax Computation

Schedule C – Dividends, Interest, and Royalties

Schedule J – Tax Computation and Payments

Schedule K – Other Info

Schedule L – Balance Sheet

Schedule M-1 – Book vs. Tax Income Reconciliation

Schedule M-2 – Retained Earnings Reconciliation

📌 Mistakes in any of these schedules can delay processing or trigger an IRS review.

You can file your Form 1120:

Electronically (e-file): The IRS prefers this for faster processing. Most tax software handles this seamlessly when the return is filed electronically.

By mail: If filing on paper, send to the correct IRS address for your state and payment status (check the IRS Where to File).

🗓 Deadline: For calendar-year corporations, the form is due April 15, 2025 (for 2026 will update the blog later on).

Even if you request an extension to file, you must pay the tax by April 15 to avoid penalties. If your corporation is required to make estimated tax payments throughout the year, these should be made quarterly.

Payment options include:

For corporations with significant tax liability, you must deposit the tax using electronic methods or making a federal tax deposit as required by law.

💡 Tip: If cash flow is tight, explore IRS installment agreements, but don't ignore your balance due.

The IRS can audit a Form 1120 return up to 3 years after filing, or longer if fraud or gross underreporting is suspected.

You should retain:

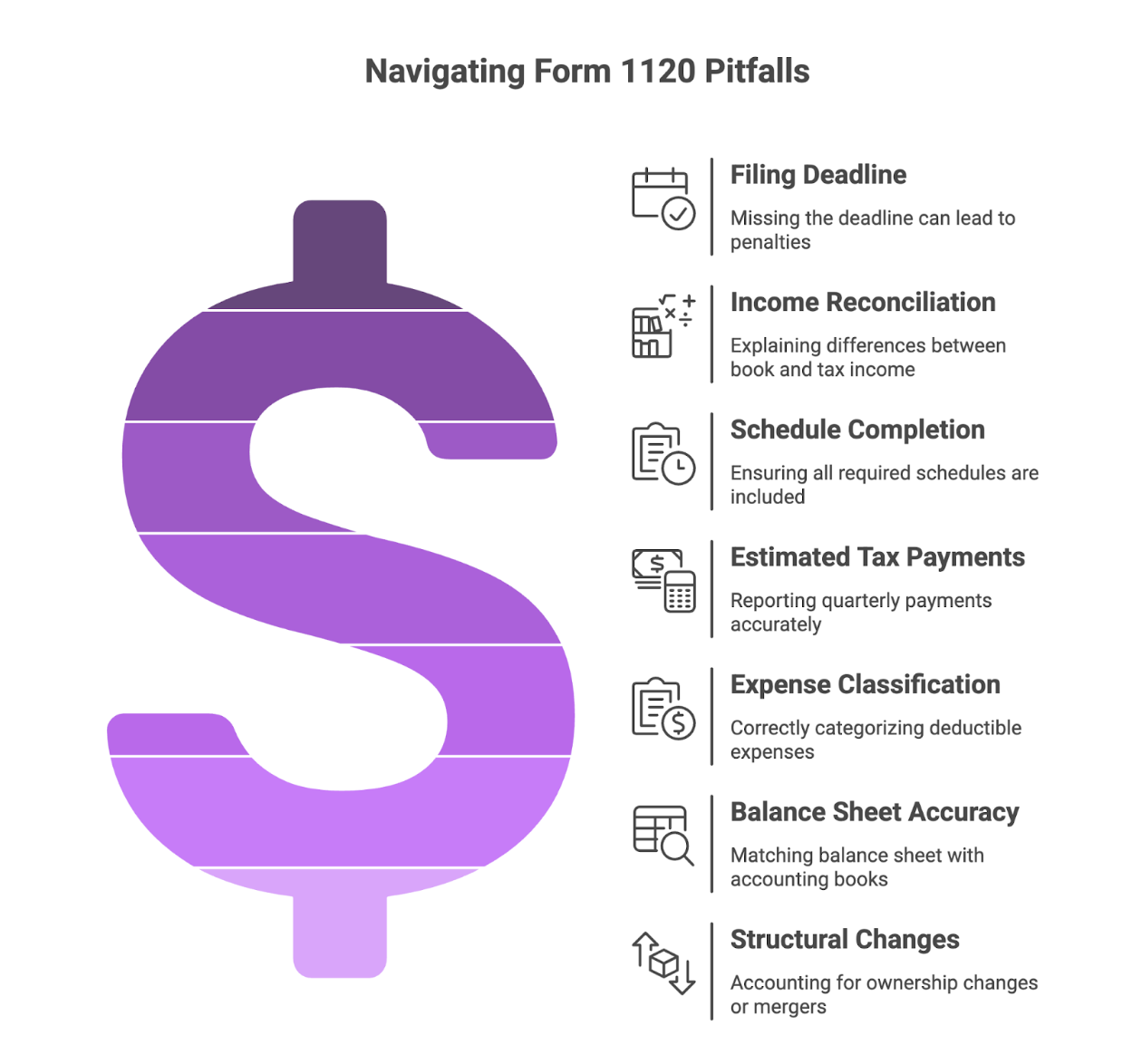

Form 1120 is the cornerstone of C corporation tax filing, but it's also where many businesses slip up. Whether you're filing for the first time or managing annual compliance, these common mistakes can lead to IRS notices, delays, or even penalties.

Let's break them down and offer real solutions, so your corporation stays in good standing.

The IRS expects C corporations to file certain business income tax returns by due by the 15th day of the 4th month after the end of the corporation's tax year (usually April 15 for calendar-year corporations). Missing this business tax deadline can lead to penalties, 5% of the unpaid tax per month, up to 25%.

Why it happens: Many founders confuse the business deadline with personal returns, or assume an extension means more time to pay (it doesn't).

How to avoid it:

Your financial books and your tax return often won't match exactly, but you need to explain why. That's where Schedule M-1 comes in.

Why it matters: If your accounting income differs from what you report on Form 1120, and you don't explain it clearly, you increase your risk of an audit.

Best practice:

Form 1120 is rarely filed alone. Depending on your business, you might also need:

Mistake to avoid: Submitting Form 1120 without required schedules or leaving key sections blank.

Tip: Use the official IRS Form 1120 instructions as a checklist before you file. Remember that the form is used to report all corporate activities, so completeness is essential.

If your C corp made quarterly estimated payments throughout the year, don't forget to report them on Schedule J. The corporation must file form reporting all payments made during the months of the corporation's tax year.

Why this matters: If you skip this, the IRS may assume you owe more than you do, and hit you with a bill for taxes you've already paid.

Best practice: Keep a running log of estimated payments made throughout the year, with dates and amounts, and reconcile them before filing.

Not all business expenses are fully deductible. And some, like entertainment or excessive travel, might not be deductible at all.

Common areas of error:

Solution: Review IRS Pub 535 with your tax professional to ensure all expense categories are treated correctly. This also helps maximize legal deductions while staying compliant.

If your corporation has more than $250,000 in assets or revenue, you're required to complete Schedule L. And your balance sheet must match your books, or the IRS will likely flag it.

Watch out for:

Fix it by: Running a final trial balance from your accounting software and reviewing it with your tax preparer before submission.

If your C corp underwent a structural change like adding shareholders, merging, or shutting down, you may need to attach additional disclosures or file other forms (like Form 966 for dissolution).

Oversight here can lead to:

Solution: Work with a tax professional familiar with corporate structures and transactions. Don't treat Form 1120 as "just another return", it's a legal record of your business activity.

While Form 1120 handles your federal income tax obligations, don't forget about state tax requirements. Many states require separate business tax returns with their own deadlines and requirements. Some states may have different due dates or extension procedures, so it's important to coordinate your federal and state filings.

Work with a tax professional who understands both federal and state requirements to ensure you don't miss any important deadlines or obligations.

If your corporation had a short tax year due to formation, dissolution, or changing accounting periods, special rules may apply for calculating due dates and tax liability. The form 7004 is used for extensions in these situations as well.

Don't forget that corporations must also file other tax forms throughout the year:

These business tax returns and payments have their own deadlines separate from Form 1120.

Corporations may also need to file various information returns throughout the year, such as:

Filing a corporate tax return isn't just another administrative task, it's a key compliance obligation with long-term financial consequences. Whether it's meeting the Form 1120 due date, organizing accurate financials, or navigating complex deductions, every step matters.

Understanding when your income tax filing is due, whether you need an extension of time to file, and how to properly report all required information to the IRS can save your business from costly penalties and compliance issues.

And while the IRS doesn't cut corners, you don't have to go it alone. Working with an experienced tax professional can ensure your tax return is filed correctly and on time.

Madras Accountancy helps U.S.-based businesses file smarter, stay compliant, and plan ahead. With expertise in corporate returns, tax planning, and financial advisory, our team ensures you're not just filing taxes, you're building a stronger financial foundation.

✅ Need help with your 1120 return or tax prep strategy? Explore our services at MadrasAccountancy.com, and let's simplify tax season together.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.