As a business owner, you're constantly looking for a competitive edge. You need to optimize your operations, cut costs without sacrificing quality, and free up your team to focus on what they do best: growing your business. For companies in the US, UK, and Australia, a powerful strategic advantage has emerged from an unexpected place: accounting outsourcing to India.

This isn't just about finding cheaper labor. It's about tapping into a deep well of highly skilled, globally-trained financial professionals who can handle everything from day-to-day bookkeeping to complex tax compliance. It’s about building a more efficient, resilient, and scalable financial backbone for your company at a fraction of the cost of an in-house team.

But what does this process actually look like? What tasks can you confidently hand over? And how do you ensure quality and security from halfway across the world? This guide will cut through the noise and answer the most pressing questions about accounting outsourcing to India.

The scope of accounting services you can outsource to India is vast. Indian accounting professionals are trained to handle a full spectrum of financial tasks, ensuring compliance with international standards for businesses in the US, UK, and Australia.

Indian accountants are well-versed in US GAAP and IRS regulations, making them ideal partners for managing your stateside financial operations. Common tasks outsourced include:

With a deep understanding of IFRS, UK GAAP, and HMRC protocols, Indian firms can bridge the skills gap many UK businesses face. Key outsourced functions include:

Indian accountants serving Australian clients are proficient in BAS requirements, GST regulations, and ATO compliance. They can confidently handle:

The most immediate benefit of accounting outsourcing to India is the significant cost reduction. Businesses regularly report saving up to 60% on their overhead costs.

These aren't just salary savings. The costs of an in-house team go far beyond their paycheck. When you outsource, you eliminate expenses related to:

By delegating these tasks, you also gain efficiency. Expert handling reduces the chance of costly errors and compliance-related penalties, saving you from hidden expenses that can cripple a growing business.

Making the move to outsource your accounting is a structured process. Here’s what the journey typically looks like:

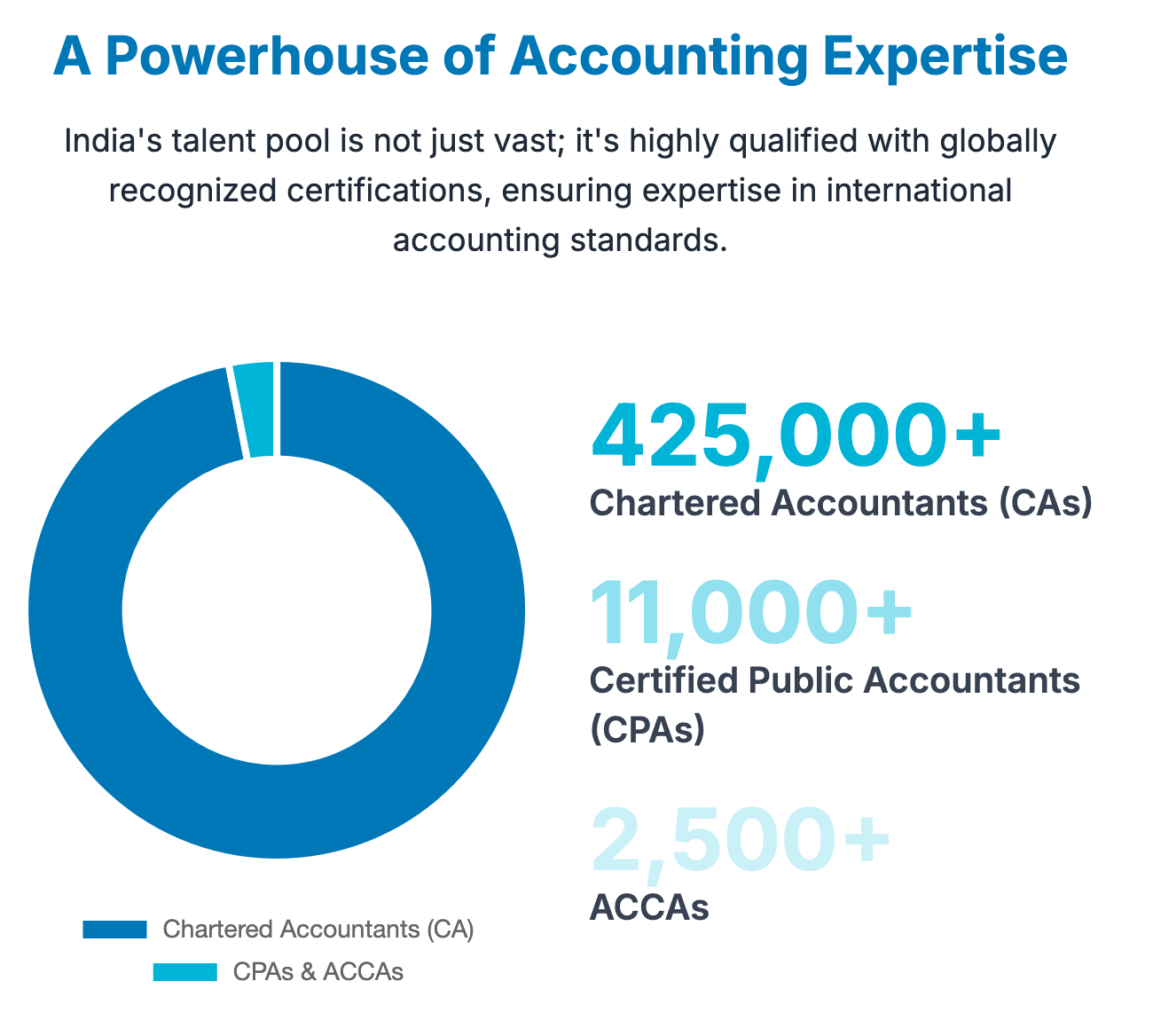

One of the biggest drivers behind the boom in accounting outsourcing to India is the sheer quality of the talent pool. Indian accountants are not just affordable; they are highly qualified and technically proficient.

Indian accountants are rigorously trained. The Chartered Accountant (CA) qualification is the gold standard in India. Many professionals also pursue global certifications like the CPA (Certified Public Accountant) and ACCA (Association of Chartered Certified Accountants) to better serve international clients. This means they are well-versed in global frameworks like US GAAP, IFRS, and UK GAAP. With over 425,000 CAs and thousands of CPAs and ACCAs, India is a powerhouse of accounting expertise.

Your offshore team will be fluent in the language of modern accounting technology. Skilled Indian accountants have a strong command of all major global accounting platforms, including:

Top outsourcing firms prioritize continuous training to ensure their teams can expertly integrate with your existing systems, automating routine tasks and providing real-time financial insights.

It's natural to have questions about working with a team in another country. Let's address the most common concerns.

Partnering with an Indian accounting firm is a strategic decision that offers far more than just cost savings. It provides access to a world-class talent pool, enhances operational efficiency, and gives your business the flexibility and scalability to thrive in a competitive landscape.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.