Every business in the United States, no matter how small, relies on accounting to function. Without accurate records, timely reports, and clear insights, even the most successful companies can run into trouble. Yet most business owners do not have the time or expertise to manage accounting themselves.

This is where accounting services come in. They allow companies to stay focused on operations and grow your business while professionals handle the numbers. From payroll processing and tax filing to financial reporting and cash flow tracking, outsourced accounting support is essential for healthy operations.

For CPA firms, this demand presents both an opportunity and a challenge. Clients expect more speed, transparency, and insight. At the same time, internal teams face tighter deadlines, complex compliance rules, and high turnover in talent.

Madras Accountancy supports CPA firms across the United States with offshore accounting teams. Our goal is to help firms increase capacity, reduce cost pressure, and deliver consistent quality across every accounting service line.

In this article, we break down the key accounting services offered in the U.S., the operational challenges firms face, and how offshore solutions can create a competitive advantage.

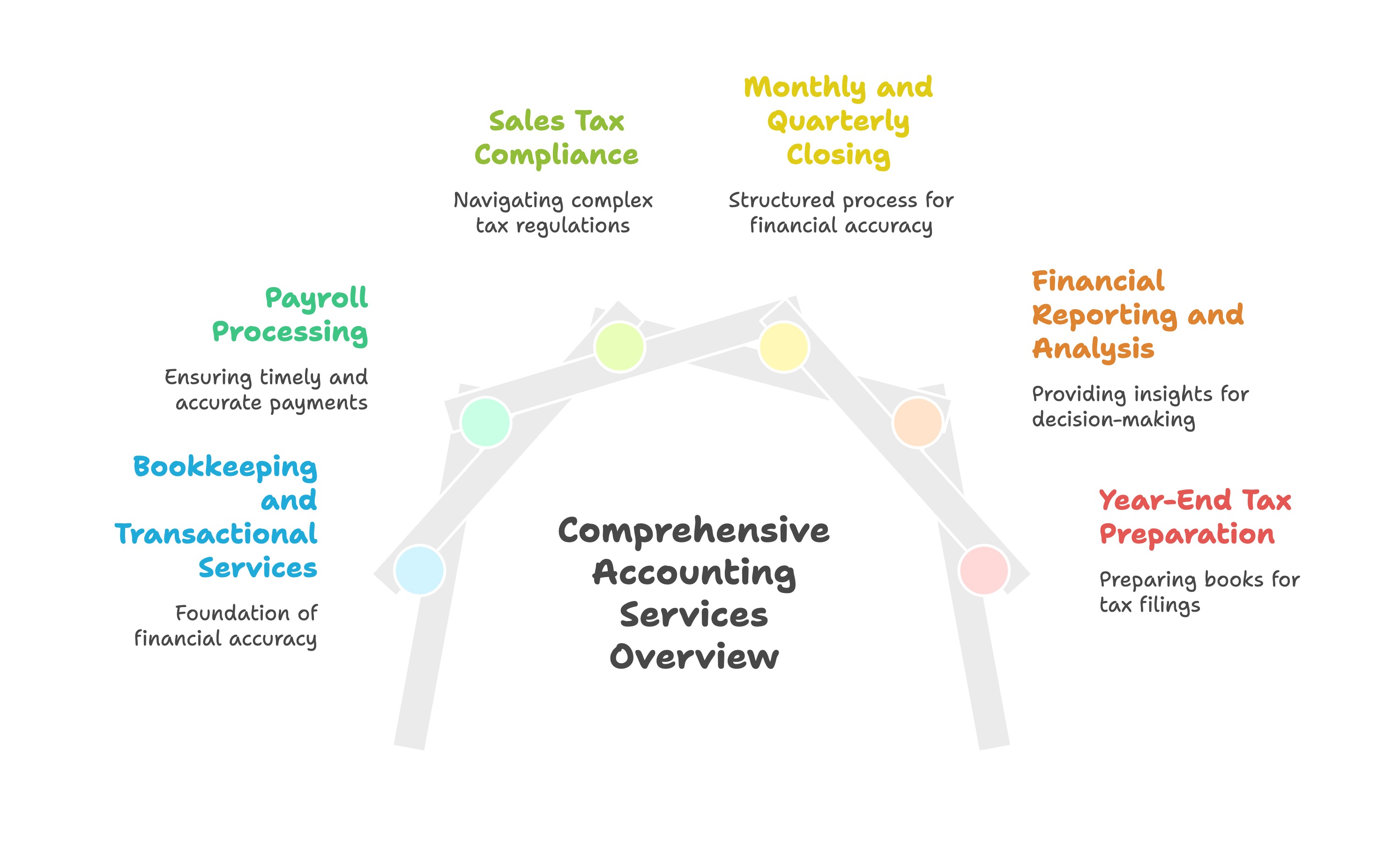

Accounting services in the United States go far beyond bookkeeping. Most CPA firms provide a wide range of offerings that support businesses throughout the year. These services can be grouped into four main categories: transactional, compliance, advisory, and reporting.

This is the foundation of any accounting relationship. It includes:

Bookkeeping service may seem simple, but accuracy here sets the stage for every financial report and compliance obligation. Errors in data entry or missed transactions lead to serious issues later. Many small business owners rely on their accountant to provide this foundational support.

Payroll involves more than just paying employees. It includes:

Because payroll errors can trigger audits or penalties, many businesses choose to outsource this service to trusted accounting providers.

Businesses that sell goods or services across state lines must comply with sales tax laws. This includes:

Sales tax rules vary by state and change often. That makes this one of the most time-consuming services for accounting firms to manage in-house.

Financial close is a structured process that ensures all accounts are accurate at the end of a period. It includes:

A reliable close process helps businesses spot trends, measure performance, and prepare for audits or tax filings.

Business owners need more than raw data. They need insight. Reporting services may include:

Clear reports allow leadership teams to make better decisions. This service also supports lenders and investors who need visibility into business performance and effective financial management.

Though often handled by a tax specialist, accounting teams play a critical role in preparing the books for year-end filings. This includes:

Strong accounting throughout the year reduces last-minute scrambling when tax season arrives.

Business owners expect more than just clean books. They want a proactive partner who helps them understand their numbers, avoid compliance problems, and plan for growth.

Here is what clients typically look for:

Even one incorrect journal entry can throw off an entire financial report. Clients rely on their accountants for precision. They expect accurate balances, reconciled statements, and error-free reports.

Financial data is only useful when delivered on time. Late reports delay decisions and frustrate leadership. Many clients expect month-end reports within ten days and real-time support during major events.

Clients want to understand what is happening in their books. They expect accountants to explain reports, point out red flags, and answer questions without jargon.

Communication is key to building trust. Clients want quick responses when they send emails, upload files, or face urgent issues. Delays create doubt about service quality.

Growing businesses often face new accounting needs. Clients expect their accounting firm to support them as they expand. This may include more detailed reporting, payroll in new states, or support for fundraising and audits.

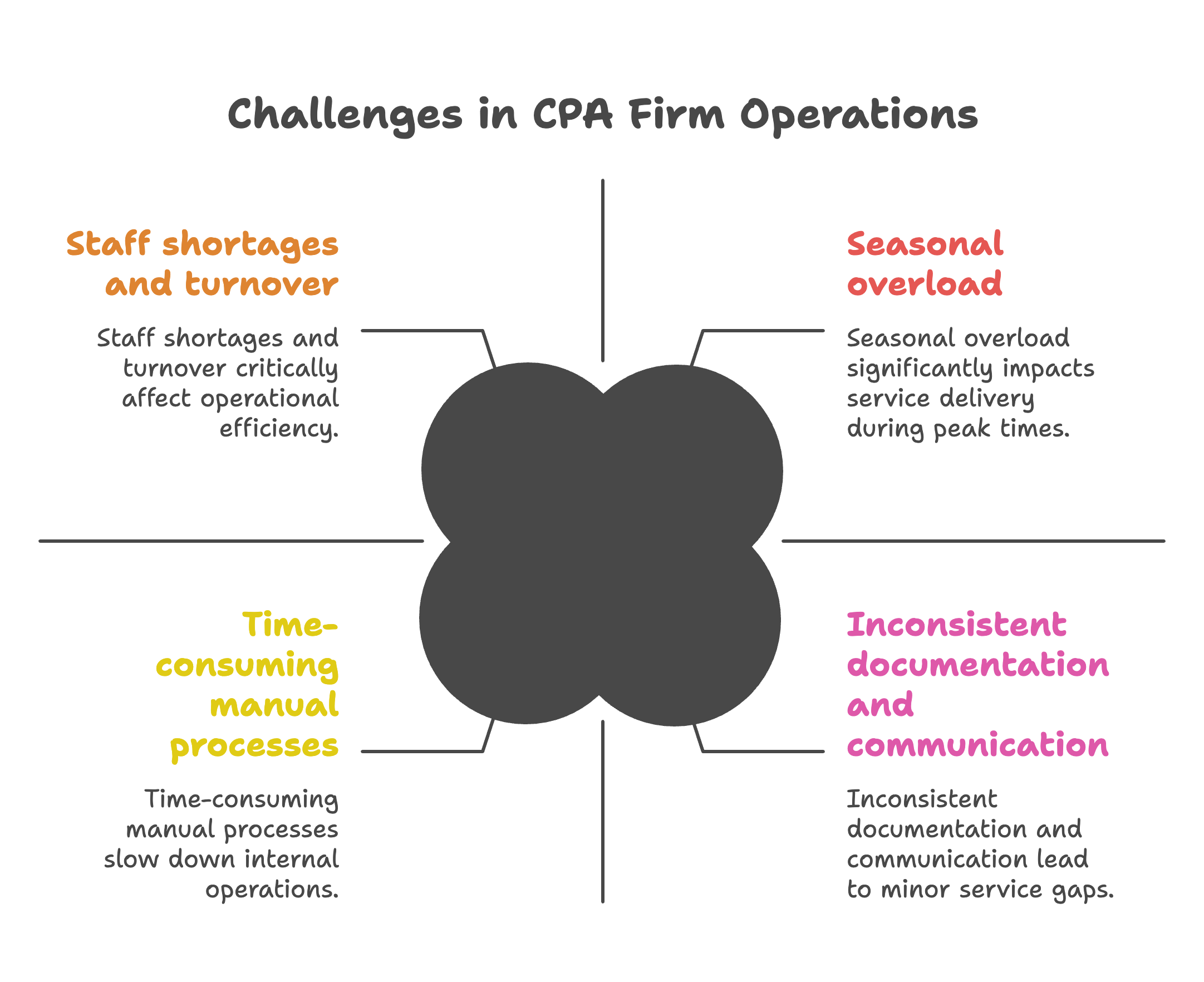

Even experienced firms can fall short of client expectations. That is often not due to a lack of skill but to operational pressure.

Recruiting and retaining accounting talent has become difficult. Long hours, repetitive work, and competition from larger firms lead to burnout and resignations. This creates backlogs and delays in service delivery.

During tax season or year-end close, accounting teams face overwhelming workloads. This affects response times and increases the risk of mistakes.

Many firms still rely on spreadsheets or outdated tools. Without automation or standardized workflows, accounting work takes longer and requires constant rechecking.

When clients upload files at different times or use multiple systems, it becomes difficult for firms to maintain accurate books. Delays in data entry mean reports are often outdated.

In busy teams, knowledge often lives in people's heads. When a team member leaves or takes time off, clients may experience service gaps.

Outsourcing accounting tasks to an offshore partner allows CPA firms to deliver services more efficiently. This approach provides cost-effective capacity without sacrificing quality.

Offshore teams allow firms to add or reduce capacity based on workload. This means more support during busy periods and lower costs during slow months.

Mature offshore firms use templates, checklists, and structured workflows. This reduces rework, improves consistency, and supports knowledge transfer between team members.

With time zone advantages and clear task handoffs, offshore teams can process transactions and prepare reports overnight. This accelerates client delivery without increasing local workload.

Outsourcing does not just apply to data entry. Many offshore partners offer skilled staff for payroll, sales tax, reconciliations, and financial reporting.

Firms can improve margins by reducing the cost per hour of accounting delivery. This allows them to reinvest in technology, training, or client experience.

Madras Accountancy provides dedicated offshore accounting teams that integrate into your workflows. You retain full control while we handle the execution. That means fewer delays, better documentation, and happier clients.

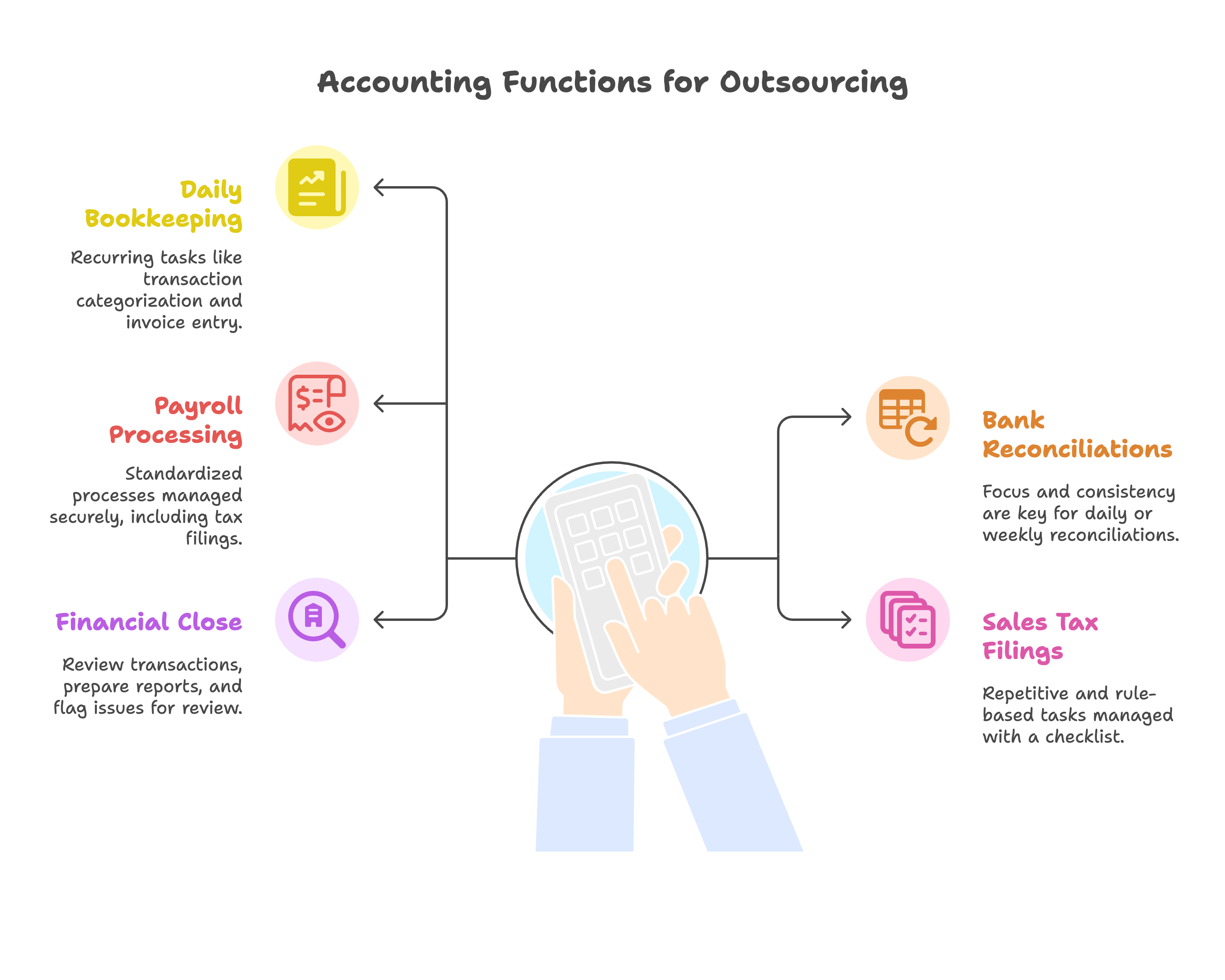

Some accounting functions are especially well-suited for offshore support. These include:

Daily and weekly bookkeeping

Recurring tasks like transaction categorization, receipt matching, and invoice entry can be handled reliably by trained offshore teams. This bookkeeping service is particularly effective when managed remotely.

Bank and credit card reconciliations

This work requires focus and consistency, not in-person meetings. Offshore teams can perform reconciliations daily or weekly to keep books current.

Payroll processing and compliance

Standardized processes, especially when using cloud-based accounting software, can be managed securely offshore. This includes calculations, tax filings, and report generation.

Sales tax filings

Multi-state filings are repetitive and rule-based. Offshore teams can manage registrations, returns, and documentation with a clear checklist-driven process.

Financial close and reporting

Offshore support can help with monthly close by reviewing transactions, preparing reports, and flagging issues for review. This speeds up internal workflows and improves accuracy.

Not every provider will be a good fit. Here are key traits to evaluate:

Madras Accountancy meets these standards and provides dedicated teams trained specifically for U.S. accounting workflows.

Our approach focuses on helping CPA firms scale accounting delivery without losing control. We tailor our services to meet each firm's unique needs. Here is how it works.

We understand your current workflow, client volume, tools, and pain points.

We assign a dedicated offshore team trained in your preferred accounting software. We create documentation and process guides to ensure consistency.

You assign tasks through your existing systems. We complete work on your timeline, using agreed templates and quality checks.

Your local team reviews outputs, sends feedback, and approves final reports. Our team tracks any issues and refines processes as needed.

We share monthly productivity reports, raise any red flags, and help you identify opportunities to improve service delivery.

This creates a partnership, not a one-off project. You stay in control. We help you move faster and more efficiently.

When CPA firms outsource certain functions, the benefits extend directly to their small business clients:

By leveraging outsourced accounting services, firms can provide enhanced value while maintaining competitive pricing for small business clients.

Accounting services in the U.S. are foundational to every business, but delivering them consistently is not easy. CPA firms face pressure to move faster, provide more insight, and control costs - all at once.

Offshore support helps bridge that gap. It gives firms access to trained, reliable professionals who can handle routine work with accuracy and speed. That frees up in-house teams to focus on review, planning, and client relationships.

The key is finding a partner who can tailor their approach to your specific needs and integrate seamlessly with your existing processes. Whether you need support with basic bookkeeping or complex multi-entity accounting, the right outsourced accounting partner can help you scale without compromising quality.

Madras Accountancy partners with CPA firms to deliver clean, scalable, and secure accounting support. If you are ready to improve how your firm delivers accounting services, we are ready to support you.

Question: What are the current market demands for accounting services in the US?

Answer: Current US market demands for accounting services include comprehensive bookkeeping and financial reporting, tax compliance and planning, advisory services for business growth, and specialized industry expertise. Growing demands cover cloud accounting implementation, automation consulting, cybersecurity for financial data, and remote service delivery capabilities. Businesses increasingly seek integrated services combining compliance, advisory, and technology solutions rather than standalone offerings. Additional demands include international tax services, succession planning, merger and acquisition support, and outsourced CFO services. The market also shows growing need for real-time financial reporting, business intelligence implementation, and strategic planning support. CPA firms must adapt service offerings to meet evolving client expectations while maintaining traditional compliance excellence.

Question: How can CPA firms identify and target their ideal client segments?

Answer: Identify ideal client segments through market analysis, profitability assessment, service capability evaluation, and geographic considerations. Analyze current client characteristics to identify most profitable relationships, highest growth potential, and best service fit. Consider industry specializations, company size preferences, service complexity capabilities, and competitive advantages. Evaluate factors including fee potential, service scope, growth prospects, and referral likelihood when defining target segments. Geographic analysis helps identify underserved markets and expansion opportunities. Technology capabilities and staff expertise should align with target segment needs and expectations. Market research, competitor analysis, and client feedback help refine targeting strategies while ensuring sustainable growth and profitability. Professional positioning and marketing efforts should align with clearly defined target segments.

Question: What strategies help CPA firms scale their operations efficiently?

Answer: Efficient CPA firm scaling strategies include technology automation, process standardization, strategic hiring, and service line expansion targeted to client needs. Implement cloud-based systems, automated workflows, and standardized procedures to improve efficiency and capacity. Strategic hiring focuses on specialized expertise, cultural fit, and growth potential rather than just filling immediate needs. Service expansion should leverage existing capabilities while meeting identified client demands. Consider outsourcing routine tasks, offshore staffing for specific functions, and technology solutions for capacity enhancement. Training and development programs ensure staff capabilities grow with firm expansion. Client retention and referral programs support sustainable growth while maintaining service quality. Professional management systems and performance metrics help monitor scaling effectiveness and identify optimization opportunities.

Question: How should CPA firms leverage technology to improve service delivery and scalability?

Answer: Leverage technology for improved service delivery through cloud-based accounting platforms, automated workflow systems, client portal implementations, and data analytics capabilities. Technology enables remote service delivery, real-time collaboration, and enhanced client communication while reducing manual processing time. Implement practice management software, time tracking systems, and automated billing to improve operational efficiency. Use business intelligence tools for client advisory services, automated reporting for enhanced value delivery, and cybersecurity measures for data protection. Mobile capabilities enable flexible service delivery while API integrations connect various software platforms for seamless operations. Technology investments should focus on client value enhancement, operational efficiency, and scalability rather than just cost reduction. Professional technology planning ensures optimal ROI and competitive advantage.

Question: What are the key challenges CPA firms face when scaling their businesses?

Answer: Key scaling challenges for CPA firms include talent acquisition and retention, maintaining service quality during growth, technology integration complexity, and capital requirements for expansion. Staffing challenges cover finding qualified professionals, training new hires, and retaining key employees during periods of change. Quality control becomes more complex with larger teams and diverse client bases requiring systematic procedures and oversight. Technology integration involves significant investments, implementation challenges, and ongoing maintenance requirements. Capital needs include equipment, software, space, and working capital for growth periods. Additional challenges cover client communication during transitions, competitive pressures, and regulatory compliance across multiple jurisdictions. Professional planning and gradual implementation help address scaling challenges while maintaining operational excellence and client satisfaction.

Question: How can CPA firms develop effective pricing strategies for different service offerings?

Answer: Develop effective pricing strategies by conducting market research, analyzing cost structures, evaluating value propositions, and implementing flexible pricing models. Value-based pricing works well for advisory services while competitive pricing may be necessary for compliance work. Consider factors including service complexity, client size, industry specialization, and geographic location when setting prices. Implement tiered pricing structures, retainer arrangements for ongoing services, and project-based pricing for specific engagements. Monitor profitability by service line and client to identify optimization opportunities. Consider alternative fee arrangements including success fees, risk-sharing models, and subscription-based pricing for appropriate services. Regular pricing reviews ensure competitiveness while maintaining profitability. Professional consultation helps evaluate pricing strategies and implement optimal approaches for different market segments.

Question: What role does specialization play in CPA firm growth and competitive positioning?

Answer: Specialization enables CPA firms to command premium pricing, attract ideal clients, develop deeper expertise, and create competitive differentiation in crowded markets. Industry specialization allows firms to understand specific client challenges, regulatory requirements, and business models while building reputation and referral networks. Service specialization in areas like tax planning, business valuation, or forensic accounting creates expertise-based competitive advantages. Geographic specialization helps firms dominate local markets and build community relationships. However, specialization requires careful market analysis to ensure adequate demand and growth potential. Balanced specialization maintains some diversification while building competitive advantages. Professional development and marketing efforts should align with chosen specializations to maximize positioning benefits and growth opportunities.

Question: How should CPA firms plan for long-term growth and succession in changing markets?

Answer: Plan long-term growth and succession through strategic planning, leadership development, cultural preservation, and adaptive business models. Develop next-generation leaders early, create clear advancement paths, and ensure knowledge transfer from senior partners. Business model adaptation should anticipate technology changes, market evolution, and client expectation shifts. Consider factors including partner retirement timing, ownership transition strategies, and firm valuation methods for succession planning. Growth planning should balance organic expansion with potential acquisitions or mergers based on strategic objectives. Financial planning ensures adequate capital for growth investments and succession needs. Regular strategic reviews help adjust plans based on market changes and opportunities. Professional succession planning consultation helps navigate complex transition requirements while maintaining firm value and client relationships.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.