.png)

Choosing the right business entity is one of the most critical decisions a company will make. The structure affects taxation, liability, ownership flexibility, funding options, and long-term growth. For CPA firms guiding startups, small businesses, and even restructuring mid-sized companies, understanding the differences among limited liability companies (LLCs), corporations (C or S), and partnerships is essential.

While attorneys typically manage the legal formation, CPAs play a central role in analyzing how each structure affects compliance, reporting, and tax efficiency. The right choice is not one-size-fits-all. It depends on the business model, funding strategy, risk appetite, and ownership goals.

This guide serves as a reference for CPA firms advising clients on entity formation and conversion. We break down the core differences, tax treatments, advantages, drawbacks, and strategic considerations for each business type.

Before comparing entity types, CPA firms must assess client needs using the following dimensions:

Each of these variables plays a role in the ultimate decision. The CPA's job is to balance short-term simplicity with long-term planning.

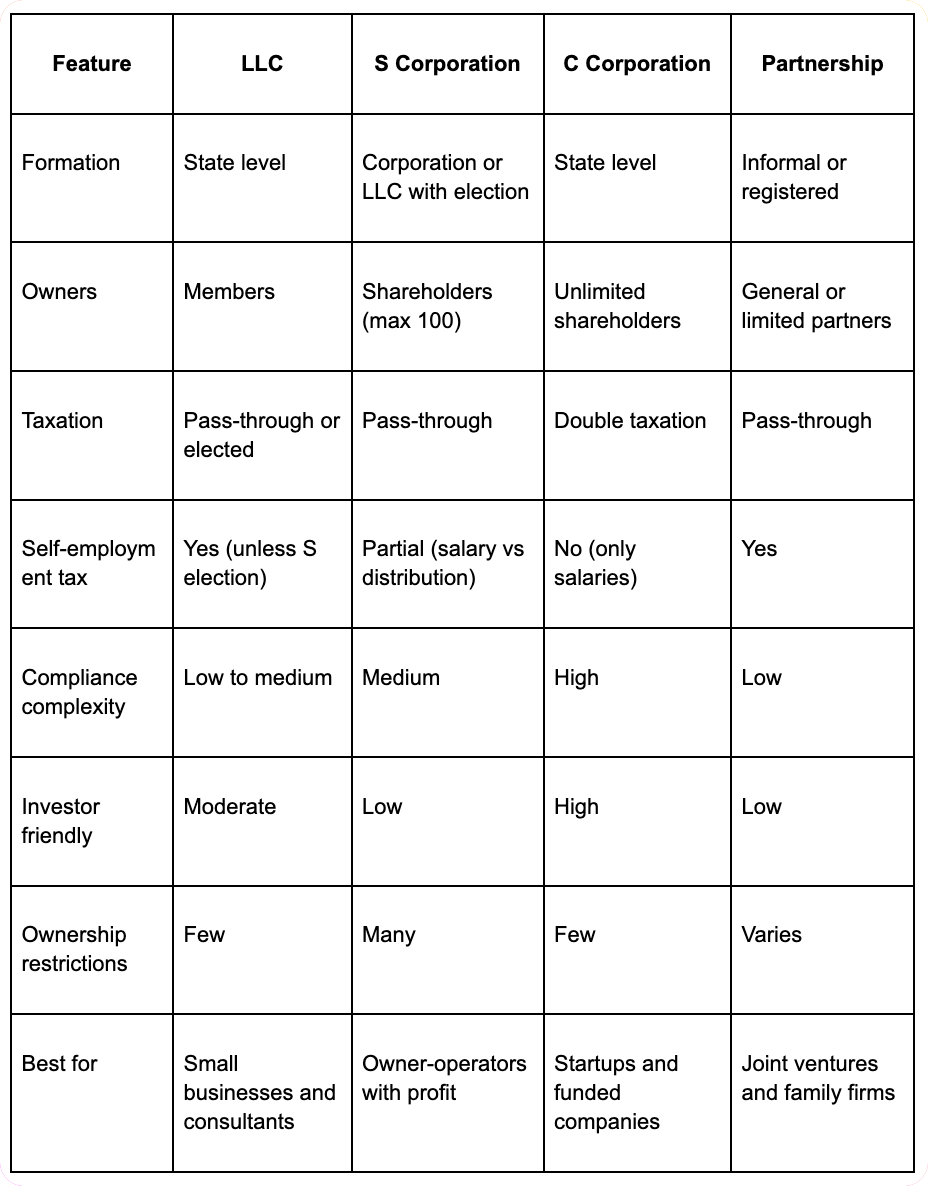

An LLC is a hybrid entity that combines the liability protection of a corporation with the tax simplicity of a partnership or sole proprietorship.

LLCs are flexible from a tax standpoint:

The most common default is pass-through taxation, where profits and losses flow directly to members’ individual returns.

.png)

LLCs are ideal for small to mid-sized businesses that:

However, if the business is planning to raise outside capital or eventually go public, a corporate structure may be more appropriate.

C corporations are separate legal entities from their owners. They are subject to corporate income tax and have the most rigid structure.

.png)

C corporations work well for:

CPA firms should model both short-term and long-term tax liabilities when advising on C corp formation. Pay special attention to Qualified Small Business Stock (QSBS) exclusion rules under IRC Section 1202.

An S corporation is not a type of entity but a tax election available to eligible corporations and LLCs.

S corps are often recommended for:

However, aggressive use of salary-distribution splits can draw IRS scrutiny. CPA firms should maintain payroll documentation and compensation benchmarks.

Partnerships are entities formed by two or more people who share ownership of a business. They come in various forms:

Partnerships are best for:

CPA firms should assist in drafting clear partnership agreements, including capital contribution terms, buy-sell provisions, and dissolution clauses.

Many businesses outgrow their original structure. CPA firms must evaluate:

Advance planning can reduce taxes and preserve business continuity.

Each state has different rules on franchise taxes, formation fees, and reporting requirements. For instance:

CPA firms should factor these into entity recommendations.

If the owner plans to sell the business, take on investors, or go public, the choice of entity matters. C corporations are often favored by acquirers and venture capitalists. LLCs may face complications in asset sales or equity transfer.

Corporations can offer retirement plans, stock options, and health benefits that are deductible. This gives owners more tools for tax-efficient compensation.

Entity selection is more than a legal formality. It sets the foundation for tax planning, risk management, capital raising, and succession. For CPA firms, offering strategic guidance on entity structure deepens client relationships and helps businesses avoid costly mistakes.

Whether a client is starting fresh, expanding operations, or restructuring for growth, understanding the trade-offs between LLCs, S corporations, C corporations, and partnerships is key. With the right insights and modeling tools, CPA firms can lead these decisions with confidence.

Question: What are the main differences between LLC, Corporation, and Partnership structures for CPA firms?

Answer: LLC structures offer operational flexibility, pass-through taxation, and limited liability protection while allowing professional licensing compliance. Corporations provide formal structure, potential tax benefits through S or C election, and clear ownership rights but require more administrative compliance. Partnerships offer simple pass-through taxation and operational flexibility but may limit liability protection. CPA firms must consider professional licensing requirements, liability exposure, tax implications, and state-specific regulations when choosing entity structures for their practices.

Question: How do professional licensing requirements affect entity selection for CPA firms?

Answer: Professional licensing requirements significantly impact CPA firm entity selection as most states require professional service entities to comply with specific ownership, management, and liability rules. Many states allow Professional LLCs (PLLCs) or Professional Corporations (PCs) for CPA practices, requiring all owners to be licensed professionals. Some states restrict certain entity types or require specific professional liability insurance coverage. Review state board of accountancy regulations and consult legal counsel to ensure entity selection complies with professional licensing requirements and maintains practice authorization.

Question: What liability protection considerations apply to different entity structures for CPA firms?

Answer: Entity structures provide varying liability protection levels for CPA firms. LLCs and corporations generally shield personal assets from business debts and certain professional liabilities, but professional malpractice claims may still reach personal assets regardless of entity structure. Professional liability insurance remains essential regardless of entity choice. Partnerships typically offer less liability protection, making partners personally liable for business obligations and potentially other partners' actions. Consider professional risks, client types, and insurance coverage when evaluating liability protection needs for entity selection.

Question: How do tax implications differ between entity structures for CPA firm owners?

Answer: Tax implications vary significantly between entity structures for CPA firms. LLCs and partnerships offer pass-through taxation, avoiding double taxation but subjecting owners to self-employment taxes on all profits. S Corporations provide pass-through taxation with potential self-employment tax savings by allowing reasonable salary payments and tax-free distributions. C Corporations face double taxation but offer benefits like retained earnings flexibility and employee benefit deductions. Consider current income levels, growth projections, and tax planning strategies when evaluating entity tax implications.

Question: What operational and administrative requirements differ between entity structures for CPA firms?

Answer: Operational and administrative requirements increase with entity formality. LLCs require operating agreements, annual state filings, and basic record-keeping but offer management flexibility. Corporations require bylaws, board meetings, shareholder agreements, and formal governance procedures with detailed record-keeping requirements. Partnerships need partnership agreements and basic compliance but have fewer formal requirements. Consider administrative burden, compliance costs, and operational complexity preferences when selecting entity structures for CPA firm operations and management.

Question: How should CPA firms evaluate entity structure changes as their practices grow?

Answer: CPA firms should regularly evaluate entity structures as practices grow by considering changing tax situations, liability exposure, operational needs, and succession planning requirements. Growth may justify more formal structures for tax benefits, operational clarity, or professional appearance. Consider conversion costs, tax implications of changes, and disruption to ongoing operations. Consult tax and legal professionals annually to review entity structure appropriateness and plan potential changes. Document decision rationale and maintain flexibility for future adjustments as business circumstances evolve.

Question: What factors should CPA firms consider when choosing between single-member and multi-member entity structures?

Answer: Single-member entity structures offer simplicity, full control, and straightforward taxation but limit growth potential and succession planning options. Multi-member structures enable partnership growth, shared responsibilities, and succession planning but require partnership agreements, profit-sharing arrangements, and consensus decision-making. Consider current ownership situation, growth plans, succession intentions, and operational preferences. Single-member LLCs can easily convert to multi-member structures when adding partners, providing initial simplicity with future flexibility for practice expansion and development.

Question: How do state-specific regulations impact entity selection for CPA firms?

Answer: State-specific regulations significantly impact CPA firm entity selection through professional licensing requirements, tax obligations, and compliance costs. Some states prohibit certain entity types for professional services, while others have specific professional entity requirements. State income tax rates, franchise taxes, and filing requirements vary considerably. Research state board of accountancy rules, tax implications, and ongoing compliance requirements in your practice location. Consider multi-state practice implications if serving clients across state lines, as entity structure may affect licensing and tax obligations in multiple jurisdictions.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.