.png)

C Corps vs. S Corps: Key Differences and How to Choose for Your Business

Meta Desc - Learn the key differences between C Corps and S Corps, including taxes, ownership, and funding. Discover which structure is right for your business.

Slug - /c-corps-vs-s-corps-new-guide

Choosing between C Corps and S Corps isn't just a paperwork decision, it shapes your company's taxes, growth trajectory, and fundraising options.

Many business owners rush incorporation to check a box, only to discover later that the business structure they chose creates unexpected tax bills or limits their ability to raise capital. Understanding the difference between S Corp and C Corp structures helps you align your business with your goals, whether you're aiming for fast VC-backed growth or building a lean, profitable company you control.

Corps and C Corps are both built on the corporation framework, but they differ in how they're taxed, how profits are distributed, and what kinds of investors you can bring on board. These differences can directly impact your take-home income, your company's scalability, and your exit opportunities down the line.

In this guide, you'll learn:

Whether you're incorporating for the first time or rethinking your current structure, this breakdown will help you avoid costly mistakes and align your entity choice with your business's financial future.

An S Corporation (S Corp) is not a separate type of corporation but a tax status election made with the Internal Revenue Service that allows a corporation to pass its income, losses, deductions, and credits directly to shareholders for federal tax purposes.

This "pass-through" structure avoids the double taxation faced by C Corps while retaining the liability protection and formal corporate structure. When you become an S Corporation, you're essentially choosing a different tax treatment under the Internal Revenue Code.

When you form a corporation (or LLC in some cases), you can file Form 2553 with the IRS to elect S Corp status if you meet the requirements. This election by a small business corporation allows you to:

The IRS imposes specific requirements for S Corps:

These restrictions can limit scalability if your business plans to raise venture capital or accept foreign investment.

S Corps pass income and losses to shareholders, who report them on their individual income tax returns. This often results in a lower overall business tax burden compared to C Corps, especially for business owners that distribute most of their profits.

However:

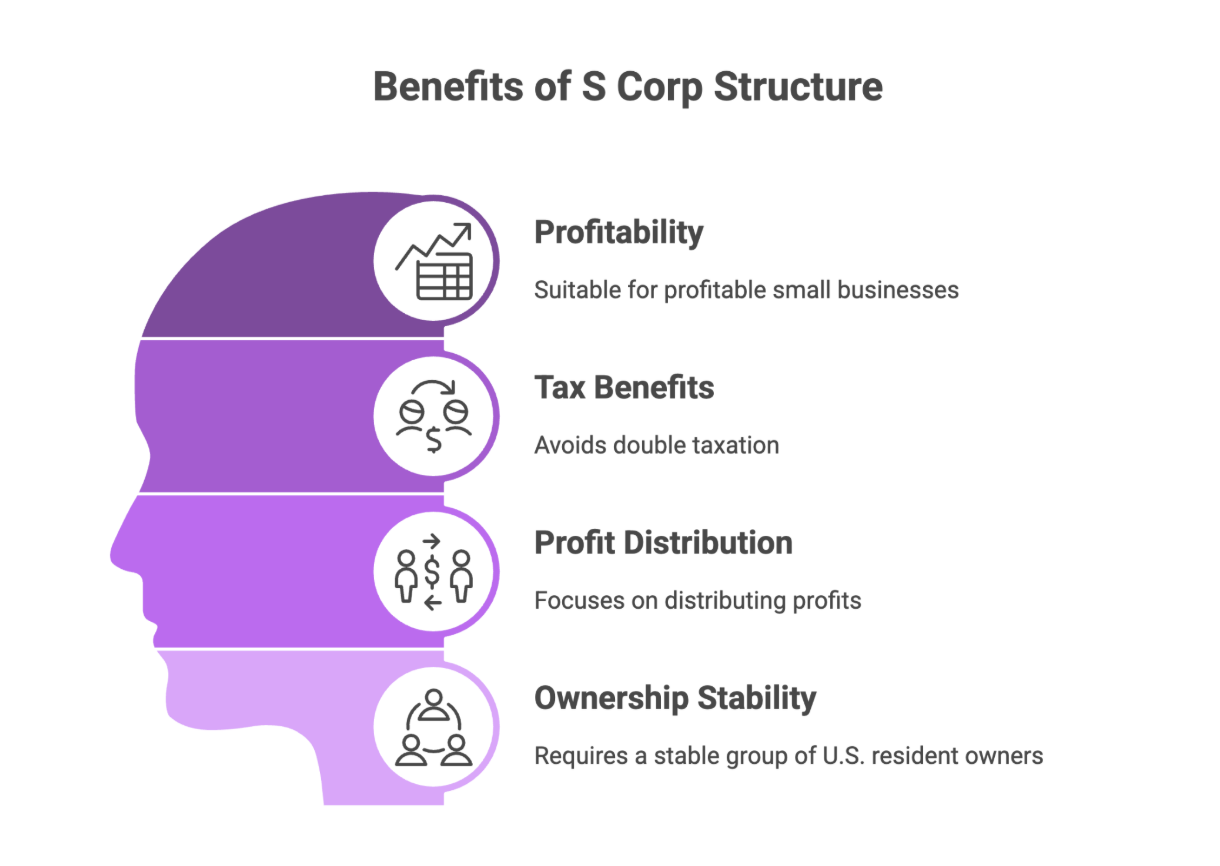

An S Corp structure can be beneficial if:

For example, a consulting agency generating consistent profits can file as an S Corp to save on self-employment taxes while paying owners a reasonable salary, ensuring clean compliance.

Despite the pass-through tax structure, when you're taxed as an S Corp, you must maintain:

Failing to adhere to these requirements can lead to the loss of S Corp status, potentially triggering unexpected tax consequences.

A C Corporation represents the default corporation status under the Internal Revenue Code. When business owners file articles of incorporation to create a corporation, they automatically create what becomes a C Corp unless they later elect different tax treatment. Understanding whether you need a corp or c corp structure depends on your business goals and tax strategy.

When you're deciding between a corporation vs c corporation, it's important to note that a C Corporation is simply the default tax treatment. C Corps are taxed under Subchapter C of the Internal Revenue Code, which means:

When you operate as a C Corp, your business structure includes:

C Corporations have no restrictions on the types of investors they can accept, making them ideal for business owners seeking external funding. The distinction between corporations and c corporations is primarily semantic - they refer to the same entity type with the same default tax treatment.

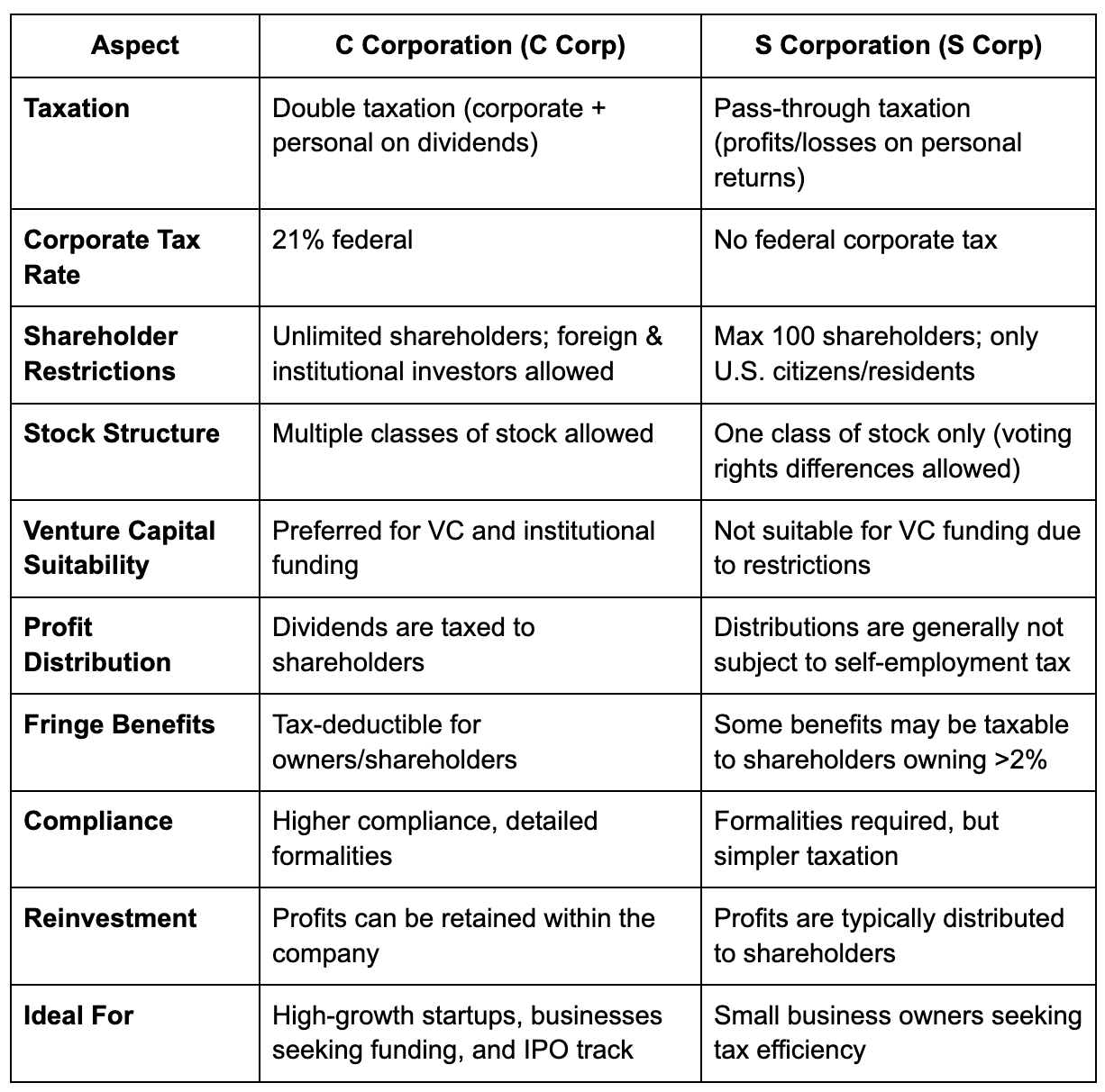

While both C Corps and S Corps provide limited liability protection and a formal corporate structure, they differ significantly in tax treatment, ownership flexibility, compliance requirements, and suitability for growth plans.

Here's a clear side-by-side comparison of these legal entities:

C Corps pay business tax on corporate profits and shareholders pay individual income tax on dividends. While this seems like a disadvantage, it allows profits to be retained in the business for growth, often with a lower effective tax rate if dividends aren't issued immediately. When you're taxed as a c corp, this double taxation structure applies regardless of your business size.

S Corps avoid double taxation by passing income directly to shareholders. However, shareholders must pay themselves a reasonable salary (subject to payroll taxes), with remaining profits distributed as dividends. Many business owners convert from a corp to an s corp specifically to avoid this double taxation.

C Corps:

S Corps:

C Corps require:

S Corps:

C Corps align with business owners planning:

S Corps are well-suited for:

If you're building a high-growth, venture-backed startup, a C Corp is practically non-negotiable.

If you're building a profitable, owner-operated business prioritizing tax efficiency, an S Corp may save you money and administrative hassle.

The difference between an S Corp and C Corp becomes most apparent when you consider your long-term business and tax strategy.

Forming a C Corporation isn't just about ticking an incorporation box, it's a strategic decision shaping how your business raises funds, scales, and handles taxes. Here's a detailed breakdown to help you assess whether a C Corp aligns with your goals:

C Corps can have unlimited shareholders, including foreign and institutional investors. This makes them the preferred structure for startups seeking venture capital, angel investment, or planning for an IPO.

C Corps can issue multiple classes of stock (common, preferred, restricted), allowing you to:

Unlike pass-through entities where profits flow directly to owners for taxation, a C Corp pays corporate taxes but can retain earnings within the company for reinvestment, which is ideal for growth-focused businesses needing to build cash reserves. When evaluating whether a corp or a c corp structure fits your needs, this profit retention capability is often a key deciding factor for growth-oriented companies.

C Corps can deduct the cost of employee benefits (health insurance, retirement plans, education assistance) provided to employees, including owners, reducing taxable income.

Ownership changes do not impact the corporation's existence, which:

C Corporations are taxed at the corporate level on profits, and shareholders pay taxes again on dividends received, increasing overall tax exposure if profits are distributed rather than reinvested. Understanding how c corps are taxed is crucial when evaluating whether this structure makes sense for your business. Generally, c corps pay corporate income tax at a flat 21% federal rate, plus any applicable state corporate taxes.

C Corps must:

This requires ongoing legal and accounting support.

For owner-operated businesses that intend to distribute profits regularly, the double taxation structure can be less tax-efficient compared to S Corps or limited liability companies.

While federal corporate tax is 21%, some states impose additional corporate income or franchise taxes, adding layers of complexity to your tax planning. A c corp may face varying state tax obligations depending on where it operates, and some states don't distinguish between corp and a c corp for tax purposes since they're the same entity type.

Choosing an S Corporation is often seen as a tax-savvy move for business owners who want liability protection without double taxation. But while the tax benefits can be significant, S Corps also have limitations that may impact your growth plans.

Here's a clear, practical breakdown:

The biggest advantage of an S Corp is avoiding double taxation. Profits and losses pass through to shareholders, who report them on their personal income tax returns at individual tax rates. This structure can reduce your overall tax burden, especially for businesses that distribute profits regularly.

Corp owners working in the business must pay themselves a reasonable salary (subject to payroll taxes), but distributions beyond that are not subject to self-employment tax. This can lead to meaningful savings compared to sole proprietorships or partnerships.

Like C Corps, S Corps provide limited liability protection for shareholders, safeguarding personal assets from business debts and lawsuits.

An S Corp structure can enhance your business's credibility, which may help with client acquisition, vendor relationships, and financing negotiations.

Shares in an S Corp can be transferred without triggering complicated tax consequences, provided transfers remain within the eligibility restrictions.

S Corps:

These restrictions make S Corps unsuitable for business owners seeking VC or institutional investment.

S Corps can only issue one class of stock (though differences in voting rights are allowed). This makes it difficult to structure complex investor agreements or equity-based compensation plans.

Owners actively working in the business must take a reasonable salary, which is subject to payroll taxes, before taking additional distributions. Mismanaging this can trigger IRS audits and penalties.

Not all states recognize S Corp status, and some impose their own taxes on S Corps, reducing the federal tax advantage.

While simpler than a C Corp, an S Corp still requires:

Before deciding between a Corp vs C Corp structure, business owners should also consider other business entities. It's worth noting that there's no meaningful difference between a corporation or c corporation - these terms refer to the same entity type. However, understanding how different corps are taxed can help you make the right choice:

For many small business owners, the decision might not be corp or an S Corp, but whether to form an LLC instead. LLCs offer:

However, LLCs may not be suitable for businesses seeking external investment or planning for an IPO.

Under current tax law, certain business owners may be eligible for a qualified business income deduction that can reduce their individual tax burden. This affects the tax calculation for both S Corp shareholders and LLC members. Note that maintaining c corp status typically means you won't benefit from this deduction since C Corps are separate taxable entities.

Now that you understand what's the difference between these business structures in taxation, ownership, and compliance, the next step is aligning your choice with your business goals, growth plans, and funding strategy.

Below is a practical decision framework to help you choose confidently.

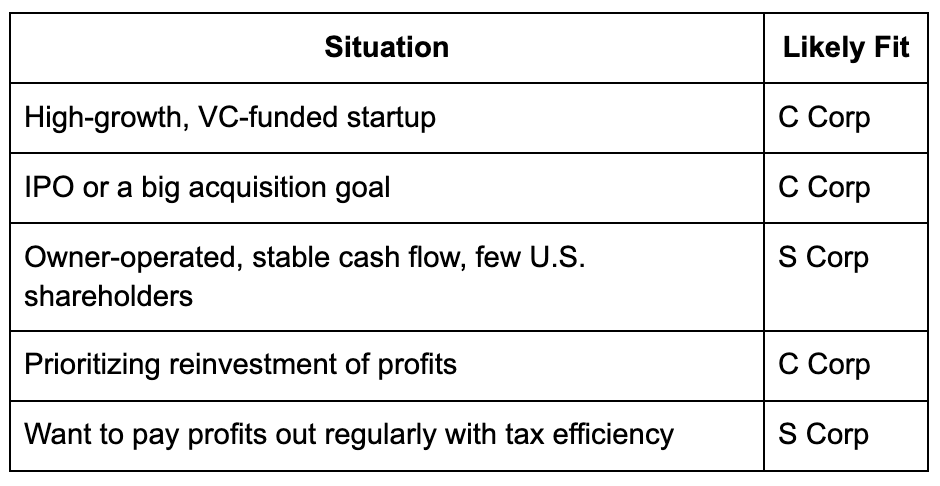

Planning to raise venture capital or institutional funding? Go with a C Corp. VCs and institutional investors require the flexible stock structures only C Corps allow, multiple classes of stock, foreign shareholders, and preferred shares are standard in VC deals.

Owner-funded or privately held business with no VC plans? An S Corp can be more tax-efficient if you want to avoid double taxation and keep your shareholder circle small and domestic.

Will you reinvest most profits to fuel growth? A C Corp can retain earnings within the business at the corporate tax rate (currently 21%), which can sometimes result in a lower effective tax rate if dividends aren't issued right away.

Want to pay yourself and owners regularly? An S Corp makes more sense for tax savings. Profits pass directly to shareholders, avoiding the corporate layer of tax, as long as you pay a reasonable salary first.

Planning for many shareholders, foreign investors, or other corporations on the cap table? An S Corp won't work, you'll need a C Corp to allow unlimited shareholders and foreign or institutional ownership.

Keeping ownership within a small, U.S.-based group? An S Corp is viable and can deliver tax savings.

Both structures require formalities, annual meetings, minutes, and state filings.

To create either a C Corp or become an S Corporation, you must first file articles of incorporation with your state. This process establishes your business as a legal corporate entity.

If you want to be taxed as an S Corp, you must:

Remember, you cannot file as an S Corp directly - you must first create a corporation and then elect the tax treatment.

Different states have varying requirements for business entities. Some states may:

When choosing between these business structures, consider:

The difference between S Corps and C Corps becomes more complex when you factor in state taxes:

Entity choice impacts taxes, compliance, and funding options for years. Many business owners file the wrong structure because it's cheap upfront, then spend much more fixing it later.

Work with a trusted tax or accounting partner to align your entity decision with your business's financial reality and growth vision.

The difference between S Corp and C Corp taxation, along with operational differences, means that what's best for your business depends on your specific situation, growth plans, and tax strategy.

Choosing between C and S Corporations isn't just a tax decision; it's a strategy decision.

If you're building a high-growth, VC-backed startup or planning for an IPO, a C Corp gives you the flexibility and investor alignment you need to scale.

If you're running a profitable, owner-operated business with no plans to raise venture funding, an S Corp can help you save on taxes while maintaining liability protection.

The key is to align your entity choice with your funding goals, growth plans, and how you intend to handle profits. Getting this right early can save you significant time, money, and headaches as your business grows.

Understanding the difference between an S Corp and other business structures helps ensure you make the right choice for your specific situation. Whether you choose to be taxed as a C or elect S Corp status, the decision should align with your long-term business and tax strategy.

At Madras Accountancy, we help business owners like you make the right calls on entity selection, incorporation, and compliance so you can scale with clarity and confidence.

Whether you're switching structures, planning your first round of funding, or simply want to ensure your taxes and compliance align with your business goals, our team can guide you every step of the way.

Explore our services at Madras Accountancy today and set your business up for long-term growth, the right way.

Question: What are the fundamental differences between C Corporation and S Corporation tax treatment?

Answer: C Corporations face double taxation where the corporation pays corporate income tax on profits and shareholders pay personal income tax on dividends received. S Corporations provide pass-through taxation where profits and losses flow directly to shareholders' personal tax returns, avoiding corporate-level taxation. C Corp tax rates range from 21% federally, while S Corp income is taxed at individual rates (up to 37%). C Corps can retain earnings for future use, while S Corps must distribute income to shareholders for tax purposes. This fundamental difference significantly impacts cash flow, tax planning, and business growth strategies.

Question: What are the ownership limitations and restrictions for S Corporation elections?

Answer: S Corporations are limited to 100 shareholders, all of whom must be US citizens or residents, and can only have one class of stock (though voting and non-voting shares are permitted). Shareholders cannot include corporations, partnerships, most LLCs, or nonresident aliens. These restrictions don't apply to C Corporations, which can have unlimited shareholders of any type, multiple stock classes, and foreign ownership. S Corp restrictions often limit growth potential and investor options, while C Corps offer maximum flexibility for raising capital and accommodating diverse investor types.

Question: How do employment tax implications differ between C Corps and S Corps for owner-employees?

Answer: S Corporation owner-employees who materially participate in the business must receive reasonable salaries subject to payroll taxes (15.3% total), while remaining profits can be distributed as tax-free distributions avoiding employment taxes. C Corporation owner-employees pay the same payroll taxes on wages, but all compensation is subject to employment taxes with no distribution alternative. This difference can result in significant employment tax savings for S Corp owners, though the IRS scrutinizes reasonable salary determinations. However, C Corp employees can receive certain tax-free fringe benefits not available to S Corp owner-employees.

Question: What are the advantages and disadvantages of C Corporation double taxation?

Answer: C Corporation double taxation disadvantages include higher overall tax burdens when profits are distributed as dividends and complexity of tax planning for profit distributions. However, advantages include ability to retain earnings in the corporation at lower corporate tax rates (21%), qualified small business stock benefits for original shareholders, and more favorable capital gains treatment for stock sales. C Corps can also time dividend distributions to optimize shareholder tax situations and accumulate earnings for future growth without immediate shareholder tax consequences, providing flexibility unavailable to S Corps.

Question: How do fringe benefits and employee compensation options differ between entity types?

Answer: C Corporations can provide tax-free fringe benefits to all employees including owner-employees, such as health insurance, life insurance, disability insurance, and other welfare benefits. S Corporation owner-employees with 2% or greater ownership cannot receive tax-free fringe benefits - these are treated as taxable compensation. However, both entity types can offer retirement plans, stock option plans, and other compensation arrangements. C Corps have more flexibility with employee benefit programs, while S Corps may require different approaches to achieve similar benefit objectives for owner-employees.

Question: When should businesses choose S Corporation versus C Corporation election?

Answer: Choose S Corporation election when seeking pass-through taxation, planning for near-term profit distributions, wanting to avoid double taxation, and operating with ownership that meets S Corp restrictions. S Corps work well for service businesses, closely-held companies, and businesses expecting significant early losses that benefit shareholders personally. Choose C Corporation when planning significant growth requiring diverse investors, expecting to retain substantial earnings, needing maximum ownership flexibility, or when double taxation is offset by strategic benefits. Consider long-term goals, ownership plans, and tax optimization strategies.

Question: Can businesses change from C Corporation to S Corporation election or vice versa?

Answer: Businesses can elect S Corporation status by filing Form 2553 within specific timeframes, converting from C Corp to S Corp taxation. However, C Corps with accumulated earnings and profits face potential tax complications during S Corp years. Converting from S Corp back to C Corp simply requires revoking the S election, but businesses cannot re-elect S status for five years without IRS consent. Consider tax implications of conversions, including built-in gains tax for C Corps converting to S Corps and the impact on accumulated earnings and profits.

Question: What factors should influence the choice between C Corp and S Corp for new businesses?

Answer: New businesses should consider projected profitability, ownership structure plans, growth and investment objectives, and tax optimization goals when choosing between C Corp and S Corp. Evaluate factors including number and type of planned shareholders, need for profit retention versus distribution, employment tax planning for owners, and long-term exit strategies. Consider professional advice for complex situations, industry-specific factors, and state tax implications. The choice significantly impacts taxes, ownership flexibility, and growth options, making careful analysis essential for optimal business structure selection and long-term success planning.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.