.png)

You just sold your investment property for $450,000. You purchased it five years ago for $300,000. Now you're facing a $150,000 capital gain and wondering how much the IRS will take. The answer depends on several critical factors: how long you owned the property, your income level, and specific exclusions available for primary residences.

Capital gains tax on real estate is the federal tax you pay on profits from selling property. For 2025, long-term capital gains (property held over one year) are taxed at 0%, 15%, or 20% depending on your income bracket, while short-term gains face ordinary income tax rates of up to 37%. Understanding these rates and available strategies can save you tens of thousands of dollars.

Capital gains tax applies to the profit you make when selling real estate property. The gain is calculated by subtracting your adjusted cost basis (original purchase price plus improvements) from the sale price, minus selling expenses like real estate commissions and closing costs.

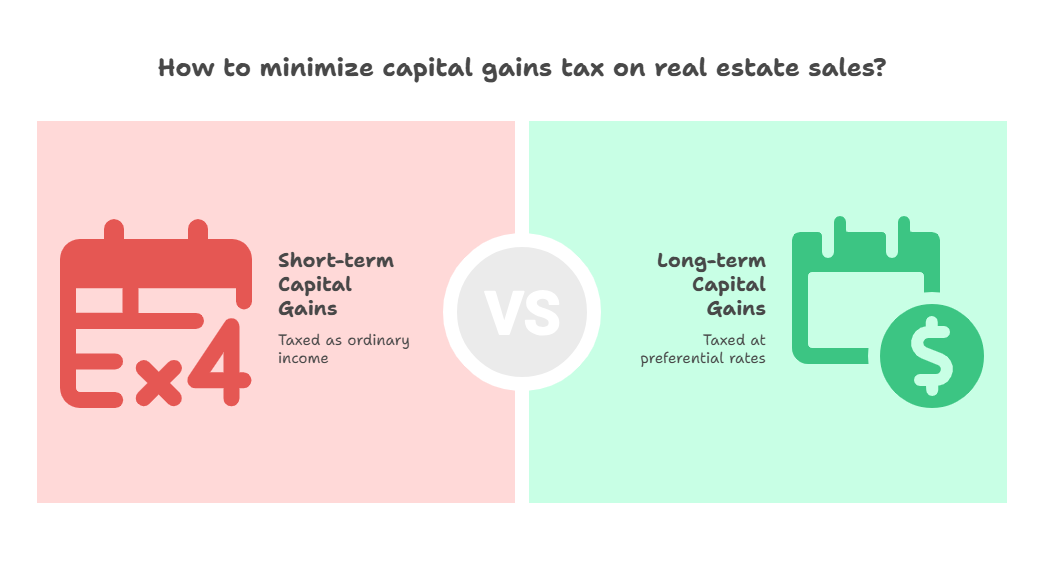

The Internal Revenue Service distinguishes between two types of capital gains:

Short-term capital gains: Properties held for one year or less, taxed as ordinary income at your regular income tax rate (10% to 37% for 2025)

Long-term capital gains: Properties held for more than one year, taxed at preferential rates (0%, 15%, or 20%)

If you bought a rental property for $200,000, spent $50,000 on improvements, and sold it for $350,000 with $20,000 in selling costs, your taxable capital gain would be $80,000 ($350,000 - $200,000 - $50,000 - $20,000).

The capital gains tax rate you pay depends on your taxable income and filing status. For 2025, the IRS has established three long-term capital gains tax brackets that significantly impact your tax liability on real estate sales.

Filing Status

0% Rate

15% Rate

20% Rate

Single

Up to $47,025

$47,026-$518,900

Over $518,900

Married Filing Jointly

Up to $94,050

$94,051-$583,750

Over $583,750

Head of Household

Up to $63,000

$63,001-$551,350

Over $551,350

Important: High-income earners may also face the 3.8% Net Investment Income Tax (NIIT) on capital gains if their modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly), bringing the effective top rate to 23.8%.

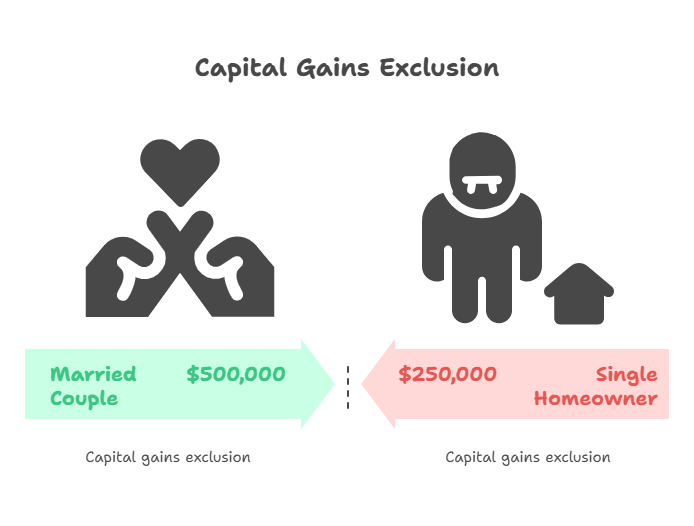

The most powerful tax break for homeowners is the primary residence capital gains exclusion. If you meet specific ownership and use requirements, you can exclude up to $250,000 of capital gains ($500,000 for married couples filing jointly) from your taxable income when selling your home.

Ownership test: You must have owned the home for at least two years during the five-year period ending on the sale date

Use test: You must have lived in the home as your primary residence for at least two years during that same five-year period

Frequency limit: You haven't used this exclusion on another home sale in the past two years

Not acquired through 1031 exchange: The property wasn't acquired through a like-kind exchange in the past five years

A married couple bought their home in 2019 for $400,000 and sold it in 2025 for $850,000. Their capital gain is $450,000, but they can exclude $500,000, resulting in zero capital gains tax. If they were single, they'd exclude $250,000 and pay tax on the remaining $200,000.

The tax treatment differs dramatically between investment properties and primary residences. While primary homes qualify for the generous exclusion described above, rental properties and investment real estate face full capital gains taxation without this benefit.

If you claimed depreciation deductions on a rental property, you'll pay depreciation recapture tax at 25% on the depreciated amount when you sell, even if the property lost value. This applies separately from capital gains tax on the appreciation.

Staying informed about key 2025 tax law changes can help you optimize your real estate investment strategy and timing.

Smart planning can significantly reduce your capital gains tax liability on real estate sales. While you can't avoid taxes entirely on investment property gains, several legitimate strategies can lower your tax bill or defer it to future years.

Hold property over one year: Qualify for lower long-term capital gains rates instead of ordinary income rates. The difference between short-term and long-term rates can save you 10-17% on your tax bill

Time your sale strategically: If you expect lower income in a future year, delaying the sale could push you into a lower tax bracket and reduce your capital gains rate from 15% to 0%

Use a 1031 exchange: Defer all capital gains tax by reinvesting proceeds into a like-kind investment property within strict timelines (45 days to identify, 180 days to close)

Maximize your cost basis: Track all capital improvements (not repairs) to increase your adjusted basis and reduce taxable gain. This includes additions, renovations, and major upgrades like new roofs or HVAC systems

Convert rental to primary residence: Live in your rental property for at least two years to potentially qualify for the primary residence exclusion, though IRS rules limit this for former rentals

Offset gains with losses: Harvest capital losses from other investments in the same tax year to offset real estate gains. Losses can offset gains dollar-for-dollar

Installment sale method: Spread the gain over multiple years by accepting payments over time, potentially keeping you in a lower tax bracket each year

Opportunity Zone investment: Defer and potentially reduce capital gains tax by investing proceeds into Qualified Opportunity Funds within 180 days of the sale

These strategies work best with proper tax planning for your business and real estate portfolio. The right strategy depends on your specific situation, income level, and long-term investment goals.

Federal capital gains tax is only part of the equation. Most states also tax capital gains, though rates and rules vary significantly. Some states have no income tax at all, while others tax capital gains at rates approaching 14%.

Alaska, Florida, Nevada, New Hampshire (limited), South Dakota, Tennessee, Texas, Washington, and Wyoming. Selling property in these states means you only pay federal capital gains tax.

California: Up to 13.3% (top bracket)

New York: Up to 10.9%

New Jersey: Up to 10.75%

Oregon: Up to 9.9%

State tax is based on residency, not property location. If you're a California resident selling property in Texas, you'll still pay California state tax on the gain. However, if you've moved to a no-income-tax state before the sale, you may avoid state capital gains tax entirely.

For property investors, this creates opportunities for strategic planning. Establishing residency in a no-tax state before a major real estate sale can save six figures on a substantial gain. However, states scrutinize such moves closely, so genuine relocation with supporting documentation is essential.

Properly reporting capital gains from real estate sales is crucial for tax compliance. The IRS receives notification of your property sale through Form 1099-S, which your closing agent typically files. You must report this on your tax return even if you qualify for exclusions.

Form 8949: Reports all capital asset sales and purchases, including real estate

Schedule D: Summarizes capital gains and losses from Form 8949

Form 4797: Required for investment property or business property sales, reports depreciation recapture

Schedule E: For rental property owners, shows rental income history

The IRS can audit real estate transactions up to six years after filing if they suspect substantial underreporting. Understanding how to prepare for a tax audit and maintaining comprehensive documentation protects you if questions arise.

Not necessarily. If the property was your primary residence and you meet the ownership and use tests (owned and lived in it for two of the past five years), you can exclude up to $250,000 of gain ($500,000 for married couples). Any gain above these amounts is subject to capital gains tax. Investment properties don't qualify for this exclusion and face full capital gains taxation.

Short-term capital gains apply to properties held for one year or less and are taxed at your ordinary income tax rate (10-37% for 2025). Long-term capital gains apply to properties held over one year and are taxed at preferential rates of 0%, 15%, or 20% depending on your income. The holding period makes a significant difference—potentially saving 17% or more in taxes.

Inherited property receives a 'step-up in basis' to the fair market value on the date of the decedent's death. This means if you inherit a home worth $500,000 that your parents bought for $100,000, your cost basis becomes $500,000. If you sell it shortly after inheriting for $510,000, you'd only pay capital gains tax on the $10,000 gain, not $410,000.

Yes, but only through a 1031 like-kind exchange for investment properties. This allows you to defer all capital gains tax by reinvesting the proceeds into another investment property. You must identify the replacement property within 45 days and close within 180 days. This strategy doesn't apply to primary residences, which use the exclusion rules instead.

You can deduct selling expenses like real estate commissions, closing costs, legal fees, and transfer taxes. You can also add capital improvements (not repairs) to your cost basis—this includes additions, renovations, new roofing, HVAC systems, and major upgrades. Regular repairs like painting or fixing a leaky faucet don't count. Keep all receipts for improvements made during your ownership.

For your primary residence, you cannot deduct a capital loss on your tax return. However, losses on investment properties can be deducted and used to offset other capital gains. If your capital losses exceed your gains, you can deduct up to $3,000 per year against ordinary income, with remaining losses carried forward to future years.

You can potentially use the primary residence exclusion after meeting the two-year use requirement, but IRS rules limit this for former rentals. Post-2008, the exclusion is prorated based on years of qualified use versus non-qualified use. Additionally, you must pay depreciation recapture tax at 25% on all depreciation claimed during the rental period, even if you later qualify for the exclusion on appreciation.

Madras Accountancy provides comprehensive tax planning services for real estate investors and CPA firms. Our team calculates your exact capital gains liability, identifies opportunities for tax reduction through strategies like 1031 exchanges and strategic timing, ensures proper documentation and reporting compliance, and coordinates with your CPA for seamless tax preparation. We've helped clients save an average of 18-24% on capital gains taxes through proactive planning.

Understanding capital gains tax on real estate empowers you to make informed decisions about when to sell, how to structure transactions, and which strategies can save you thousands of dollars. The difference between short-term and long-term rates, the power of the primary residence exclusion, and strategic planning tools like 1031 exchanges can dramatically impact your after-tax proceeds.

The key is planning ahead. Tax-saving strategies work best when implemented before the sale, not after. Whether you're selling your first investment property or managing a large real estate portfolio, working with experienced tax professionals ensures you take advantage of every available benefit while remaining fully compliant with IRS regulations.

Madras Accountancy specializes in real estate tax planning for investors, CPA firms, and property owners. Our team stays current on the latest IRS guidance and state tax laws to provide strategic advice that reduces your tax burden. We handle everything from calculating your exact liability to coordinating complex transactions like 1031 exchanges, giving you confidence in your tax position and peace of mind.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.