You're sitting in your office in January, looking at your bank account with growing concern. December was your best month ever—revenue was through the roof. But now you're staring at a dwindling cash balance, wondering how you'll pay your bills until the busy season starts again in March.

Sound familiar? You're not alone. Over 60% of small businesses experience cash flow problems, and most of them are caught off guard by seasonal fluctuations they didn't plan for.

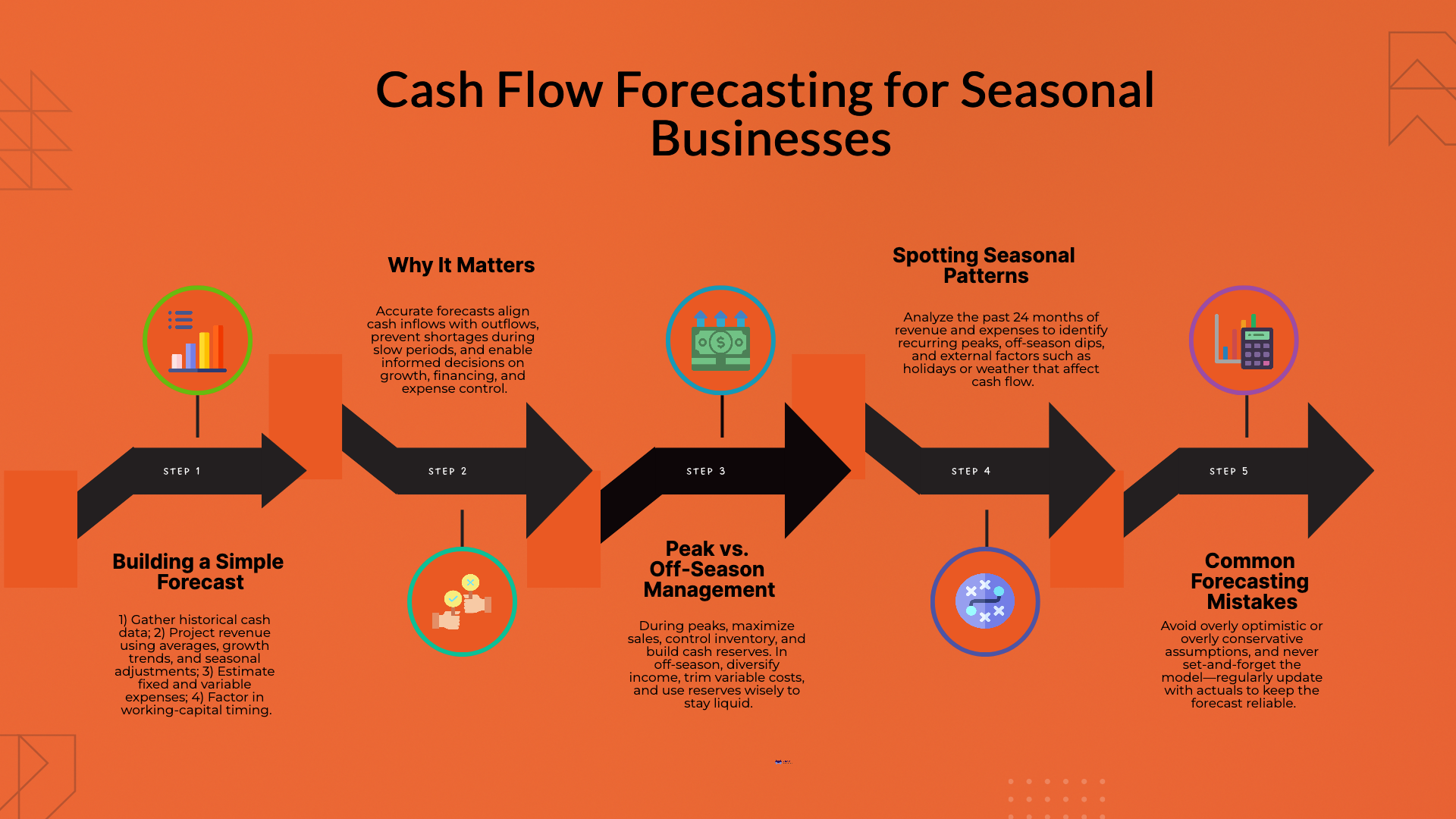

The problem is that revenue and expenses don't always align perfectly. Seasonal businesses face unique challenges, growth requires more working capital, and unexpected expenses can derail even the best plans. The solution is accurate cash flow forecasting, proactive planning and management, better decision-making, and reduced stress and uncertainty.

Cash flow forecasting predicts future cash by showing when you'll have cash, identifying potential shortfalls, planning for seasonal variations, and supporting growth planning. It enables better decisions about when to invest in growth, how to manage expenses, when to seek financing, and how to optimize operations.

Understanding your cash flow cycle is essential for effective forecasting. Cash comes in from customer payments, investment income, loan proceeds, and asset sales. Cash goes out for operating expenses, debt payments, capital expenditures, and owner distributions.

Timing differences create challenges because revenue is earned at different times than it's received, expenses are incurred at different times than they're paid, seasonal variations affect both income and expenses, and growth requirements change your cash needs.

Identifying seasonal patterns requires analyzing historical data, looking for recurring trends, considering external factors, and planning for variations. Common seasonal factors include weather and seasons, holidays and events, industry cycles, and economic conditions.

Understanding these patterns helps you prepare for the ups and downs that every seasonal business faces. This knowledge is crucial for creating accurate forecasts and making informed business decisions.

Start by collecting revenue patterns including monthly revenue for the past 24 months, seasonal variations, growth trends, and customer payment patterns. This historical data provides the foundation for your forecast.

Expense patterns include monthly expenses for the past 24 months, fixed versus variable costs, seasonal variations, and one-time expenses. Understanding these patterns helps you predict future costs more accurately.

Cash flow patterns include monthly cash balances, peak and low periods, working capital needs, and financing requirements. This information helps you understand your business's cash flow characteristics.

Revenue forecasting methods include historical averages, growth trends, seasonal adjustments, and market conditions. The key is to use multiple methods and adjust based on your specific situation.

Payment timing is crucial because revenue is earned at different times than it's received. Consider when revenue is earned, when payments are received, collection periods, and payment terms when creating your forecast.

Seasonal adjustments include peak season increases, off-season decreases, gradual transitions, and external factors. These adjustments help you create a more accurate forecast that reflects your business's seasonal nature.

Fixed expenses include rent and utilities, salaries and benefits, insurance and taxes, and loan payments. These expenses are relatively predictable and easier to forecast.

Variable expenses include materials and supplies, marketing and advertising, travel and entertainment, and miscellaneous costs. These expenses can vary significantly and require more careful estimation.

Seasonal variations include higher costs in busy periods, lower costs in slow periods, inventory adjustments, and staffing changes. Understanding these variations is essential for accurate forecasting.

Accounts receivable management includes tracking outstanding invoices, understanding collection periods, setting appropriate payment terms, and making provisions for bad debt. This helps you predict when you'll actually receive payments.

Inventory management includes monitoring current levels, planning for seasonal requirements, understanding turnover rates, and accounting for storage costs. This helps you manage your inventory investment effectively.

Accounts payable management includes tracking outstanding bills, understanding payment terms, maintaining vendor relationships, and considering the cash flow impact of payment timing.

Your monthly cash flow statement should include cash inflows from customer payments, other income, loan proceeds, and investment returns. These inflows represent money coming into your business.

Cash outflows include operating expenses, debt payments, capital expenditures, and owner distributions. These outflows represent money going out of your business.

Net cash flow is simply inflows minus outflows, showing your monthly change, cumulative balance, and trend analysis. This helps you understand your business's cash flow performance over time.

A 13-week rolling forecast provides weekly detail for more granular planning, better cash management, earlier problem detection, and improved accuracy. This approach gives you a more detailed view of your short-term cash needs.

Key benefits include real-time adjustments, better decision-making, reduced surprises, and improved planning. This approach is particularly useful for businesses with volatile cash flows or those in rapid growth phases.

Revenue management during peak season includes maximizing peak period sales, optimizing pricing, managing capacity, and planning for growth. This helps you make the most of your busy periods.

Expense management includes controlling costs, managing inventory, optimizing staffing, and planning for maintenance. This helps you maintain profitability during busy periods.

Cash management includes building reserves, planning for investments, managing working capital, and preparing for the off-season. This helps you maintain financial stability throughout the year.

Revenue management during off-season includes diversifying income streams, offering off-season services, maintaining customer relationships, and planning for the next peak. This helps you maintain revenue during slow periods.

Expense management includes reducing variable costs, maintaining essential operations, planning for maintenance, and investing in improvements. This helps you control costs during slow periods.

Cash management includes using reserves wisely, planning for expenses, maintaining liquidity, and preparing for the next peak. This helps you survive the off-season and prepare for the next busy period.

Excel and Google Sheets offer customizable templates that are easy to use, cost-effective, and flexible. These tools are perfect for small businesses just starting with cash flow forecasting.

Key features include monthly and weekly views, seasonal adjustments, scenario planning, and charts and graphs. These features help you create comprehensive forecasts that are easy to understand and update.

Accounting software like QuickBooks, Xero, Sage, and FreshBooks often include basic forecasting capabilities. These tools integrate with your existing accounting data, making forecasting easier and more accurate.

Dedicated forecasting tools like Float, Pulse, PlanGuru, and Adaptive Insights offer advanced features including automated data entry, real-time updates, scenario planning, and integration capabilities. These tools are ideal for businesses with complex forecasting needs.

Being overly optimistic leads to unrealistic revenue projections, underestimated expenses, ignoring seasonality, and poor assumptions. This can result in cash flow crises and poor business decisions.

Being too conservative leads to underestimated revenue potential, overestimated expenses, missed opportunities, and slow growth. This can prevent you from taking advantage of growth opportunities.

Set and forget approaches include not updating regularly, failing to adjust, ignoring variances, and poor follow-through. This makes your forecast useless and can lead to poor business decisions.

Over-complicating includes too much detail, complex processes, time-consuming maintenance, and difficulty keeping up. This can make forecasting a burden rather than a helpful tool.

Best case assumptions include higher revenue than expected, lower expenses than budgeted, better market conditions, and successful growth. Planning for this scenario helps you understand how to handle growth and identify investment opportunities.

Worst case assumptions include lower revenue than expected, higher expenses than budgeted, poor market conditions, and economic downturn. Planning for this scenario helps you develop cost reduction strategies, cash preservation tactics, and survival plans.

Most likely assumptions include realistic projections, balanced assumptions, achievable goals, and regular monitoring. Planning for this scenario helps you maintain normal operations, steady growth, and regular monitoring with adjustments as needed.

Weekly reviews include comparing actual versus forecast, identifying variances, adjusting projections, and taking action. This helps you stay on top of your cash flow and make timely adjustments.

Monthly reviews include comprehensive analysis, major adjustments, strategic planning, and goal setting. This helps you maintain a longer-term perspective and make strategic decisions.

Quarterly reviews include complete forecast overhaul, setting new goals, planning for the next quarter, and learning from experience. This helps you improve your forecasting process over time.

Cash flow metrics include monthly cash flow, cash conversion cycle, working capital ratio, and burn rate. These metrics help you understand your business's cash flow performance.

Operational metrics include revenue growth, expense ratios, profit margins, and customer metrics. These metrics help you understand your business's overall performance.

Consider hiring an accountant for complex situations including multiple revenue streams, complex seasonal patterns, growth planning needs, and tax planning requirements. Professional help can save you time and improve accuracy.

Hire help when you lack expertise, have limited time, need accuracy, or require professional guidance. The cost of professional help is often much lower than the cost of poor forecasting decisions.

Look for experience and expertise including relevant industry experience, forecasting expertise, technology proficiency, and communication skills. These qualifications ensure you get the help you need.

Services offered should include forecast preparation, monthly monitoring, variance analysis, and strategic planning. These services help you maintain accurate forecasts and make informed decisions.

Cash flow forecasting isn't just about predicting the future—it's about taking control of your business's financial destiny. By understanding your cash flow patterns and planning for seasonal variations, you can make better decisions, avoid crises, and position your business for sustainable growth.

The key is to start simple, be realistic, and review regularly. Don't try to create the perfect forecast on your first try. Start with the basics, learn from your mistakes, and improve over time.

Ready to improve your cash flow management? Check out our comprehensive guide on In-House vs. Outsourced Accounting: A Cost-Benefit Analysis to understand your options.

For insights on working with external teams, read our article on Best Practices for Working with an Offshore Accounting Team.

And if you're ready to take the next step, our guide on How to Choose an Accounting Outsourcing Provider: 10 Questions to Ask will help you select the right partner.

Related read: working capital.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.