.png)

Colorado's sales tax system can feel like navigating a maze, especially when you consider how many different jurisdictions can add their own local taxes to your final rate. Whether you're starting a new business or expanding into Colorado, understanding the state's unique tax structure is essential for staying compliant and avoiding penalties.

Let's walk through everything you need to know about Colorado sales tax for 2025, from basic rates to filing requirements and exemptions.

Colorado operates what's called a "home-rule" tax system, which means local jurisdictions have significant freedom to set their own sales tax rates and rules. This creates complexity but also explains why tax rates can vary so dramatically across different areas of the state.

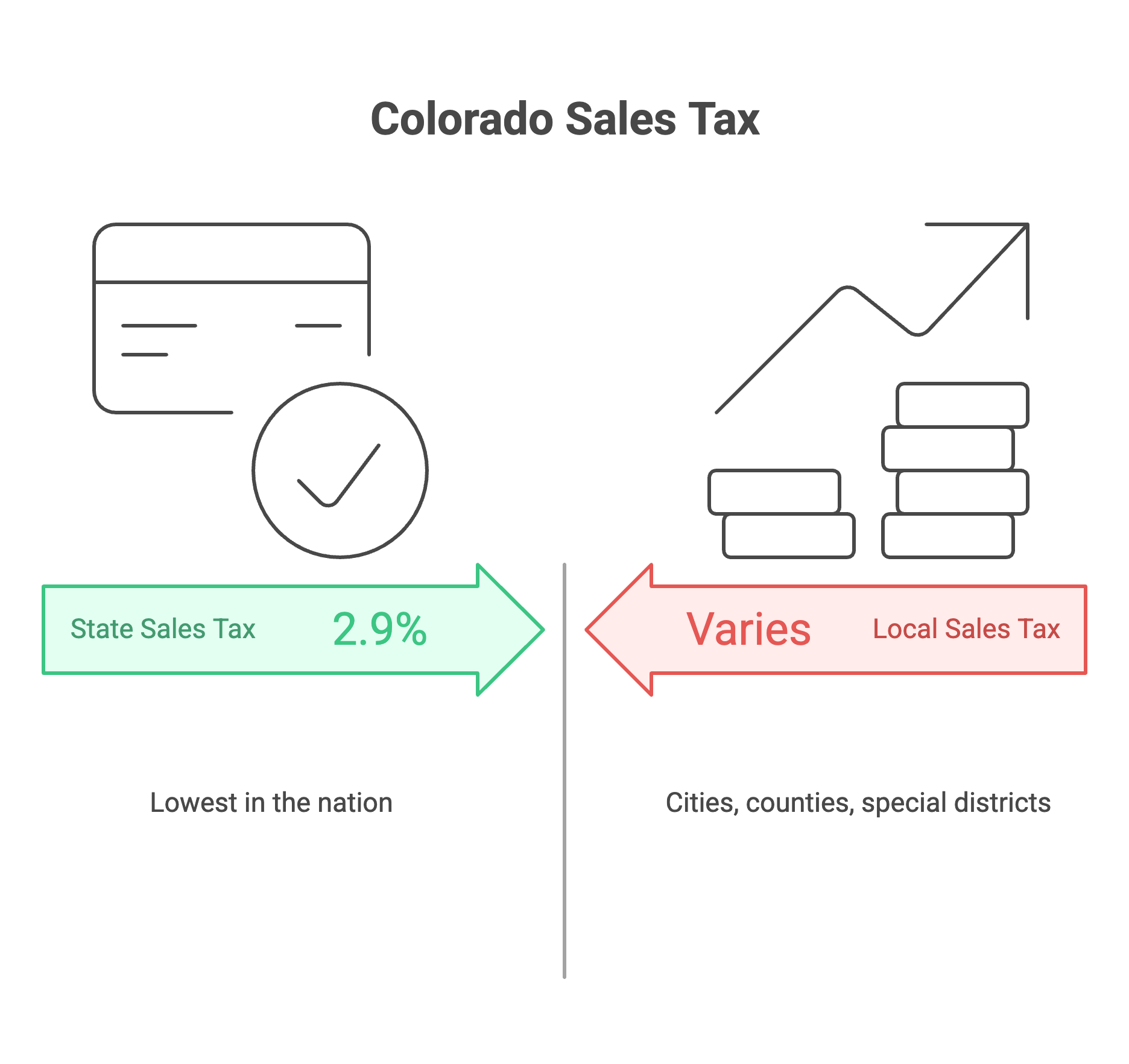

The state sales tax rate sits at 2.9% statewide - one of the lowest in the nation. However, this is just the beginning of your tax calculation. Local sales tax from cities, counties, and special districts can add several percentage points to your total rate.

The Colorado Department of Revenue handles state-level sales and use tax collection, but many local jurisdictions collect their own taxes separately. This means you might need to file returns with multiple agencies depending on where you do business.

Colorado's use tax system complements the sales tax structure. Use tax applies when you purchase items for business use but no sales tax was collected at the time of purchase. Think of it as ensuring the state gets its revenue even when sales tax wasn't originally paid.

Understanding tax rates in Colorado requires looking at both state and local components. The state sales tax rate of 2.9% applies everywhere, but local sales tax rates vary dramatically depending on your specific location.

In Colorado Springs, for example, the total sales tax rate includes the state's 2.9% plus additional local taxes from El Paso County and the city itself. Denver has its own rate structure that differs significantly from surrounding areas.

City and county governments can impose their own sales taxes, and special districts can add even more. These special districts might fund things like transportation improvements, cultural facilities, or economic development projects. The result is that your total sales tax rate depends heavily on your exact location.

Using the Colorado Department of Revenue's geographic information system (GIS) becomes essential for determining exact rates. This online tool helps you find the specific tax rate that applies to any address in Colorado, which is crucial given how much rates can vary even within the same city.

The total sales tax rate in some areas can exceed 8% when you combine state, county, city, and special district taxes. This makes accurate rate lookup critical for proper tax collection and remittance.

Before you can collect sales tax in Colorado, you need to obtain a sales tax license from the Colorado Department of Revenue. This license authorizes you to collect state sales tax and provides your account number for filing returns.

The registration process covers basic business information, what types of goods or services you'll sell, and your expected sales volumes. You'll also need to specify all the locations where you'll be conducting business, as this affects which local taxes apply.

Colorado requires most businesses to file sales tax returns monthly, with returns due by the 20th day of the month following the reporting period. So January sales get reported by February 20th. Some smaller businesses may qualify for quarterly filing.

Local jurisdictions often have their own registration requirements separate from the state. If you're doing business in multiple cities or counties, you may need to register with each one individually and file separate returns.

The state's Revenue Online portal makes registration and filing much easier than paper processes. This system handles both registration and ongoing compliance requirements through a single interface.

Most retail sales of tangible personal property are subject to sales tax in Colorado. This includes typical retail items like clothing, electronics, furniture, and general merchandise sold to end consumers.

Certain services are also taxable, though Colorado taxes fewer services than many other states. Taxable services typically include things like telecommunications, certain repair services, and some recreational activities.

Food for home consumption is generally exempt from state sales tax, though local jurisdictions may still tax it. Prepared foods and restaurant meals are typically taxable. Prescription medications are exempt from sales tax.

Goods purchased for resale are exempt from sales tax when proper exemption certificates are provided. This wholesale exemption prevents double taxation when businesses sell to other businesses rather than end consumers.

Manufacturing equipment and machinery may qualify for exemptions under certain circumstances. These rules can be complex, so businesses involved in manufacturing should review the specific requirements carefully.

Tax exemptions in Colorado require proper documentation through exemption certificates. When a customer claims an exemption, you need a valid certificate on file to support the tax-free sale.

Common exemptions include sales to other businesses for resale, sales to government entities, and sales of certain necessities like prescription drugs and some food items. Each exemption type has specific requirements and documentation needs.

Nonprofit organizations may qualify for sales tax exemptions, but they need to provide proper certificates and meet specific criteria. Not all nonprofit activities qualify for exemption, so it's important to understand the limitations.

Agricultural exemptions apply to certain farm equipment and supplies, but the rules are detailed and specific. Farmers and agricultural businesses should review these provisions carefully to ensure they're claiming exemptions correctly.

Special event sales may have different rules or exemptions depending on the type of event and location. If you're selling at farmers markets, craft fairs, or similar events, check with local jurisdictions about any special requirements.

Most Colorado businesses must file sales tax returns monthly, regardless of whether they owe any tax. Returns are due by the 20th day of the month following the reporting period, and late filing comes with penalties that add up quickly.

Electronic filing through Revenue Online has become the standard method. The system guides you through the process, calculates any penalties automatically, and provides confirmation of successful filing.

When filing, you'll report your gross sales, exempt sales, and total taxable sales for the reporting period. If you operate in multiple jurisdictions, you may need to break down sales by location to ensure proper allocation of local taxes.

Payment can be made electronically along with your return filing. The state encourages electronic payment and offers slightly extended due dates for businesses that file and pay electronically.

Record keeping requirements are strict in Colorado. You need to maintain detailed records of all sales, exemption certificates, and tax collections for at least three years. During audits, the Colorado Department expects thorough documentation.

The Colorado Department of Revenue's geographic information system (GIS) provides the most accurate way to determine tax rates for specific addresses. This online tool is essential for businesses that sell to customers throughout the state.

A Colorado sales tax calculator can help ensure you're applying the correct rates, especially when dealing with multiple jurisdictions. Many businesses integrate these tools with their point-of-sale systems for automatic calculation.

Revenue Online serves as the central portal for most tax-related activities in Colorado. You can register your business, file returns, make payments, and access account information through this single system.

Many modern point-of-sale systems can integrate with Colorado's tax rate databases to ensure automatic application of correct rates. This reduces errors and helps maintain compliance as local rates change.

For businesses selling online or through mobile channels, automated tax calculation becomes even more important. You need systems that can determine the correct rate based on delivery address and apply it automatically.

Home-rule municipalities in Colorado can have significantly different requirements from the state system. Some collect their own taxes separately, while others participate in the state's collection system.

Special districts add another layer of complexity to Colorado's tax system. These districts can levy additional taxes for specific purposes, and the boundaries don't always align with city or county lines.

Seasonal businesses or those with fluctuating sales may qualify for different filing frequencies during different periods. The Colorado Department can adjust requirements based on actual business activity.

Construction and contracting businesses face unique challenges in Colorado due to the varying local rates. Projects that span multiple jurisdictions need careful tracking to ensure proper tax collection and remittance.

Colorado's tax laws and local rates change periodically, making it important to stay current with updates. The Colorado Department of Revenue publishes notices about rate changes and new requirements.

Local jurisdictions can adjust their rates or impose new taxes, which affects your total collection requirements. Regular rate lookup ensures you're always using current information.

Working with tax professionals who understand Colorado's unique system can help ensure ongoing compliance. The complexity of multiple jurisdictions and varying local rules makes professional guidance valuable for many businesses.

What is the current Colorado state sales tax rate for 2025?Colorado's state sales tax rate is 2.9%, one of the lowest in the nation. However, local cities, counties, and special districts add their own taxes, bringing total rates typically between 4% and 8% depending on the specific location.

How do I find the exact sales tax rate for a specific Colorado address?Use the Colorado Department of Revenue's Geographic Information System (GIS) tool on their website. This online lookup tool provides the exact combined rate for any address in Colorado, including all applicable state, county, city, and special district taxes.

Do I need separate licenses for different Colorado cities where I do business?It depends on the jurisdiction. Some cities participate in the state collection system and only require state registration, while home-rule municipalities may require separate registration and filing. Check with each local jurisdiction where you conduct business.

How often do I need to file Colorado sales tax returns?Most businesses file monthly returns due by the 20th of the month following the reporting period. Some smaller businesses may qualify for quarterly filing based on their tax liability. The Colorado Department of Revenue assigns your filing frequency when you register.

Are there any items exempt from Colorado sales tax?Yes, common exemptions include food for home consumption, prescription medications, and goods purchased for resale with proper exemption certificates. Manufacturing equipment may also qualify for exemptions under specific circumstances.

What happens if I file my Colorado sales tax return late?Late filing results in penalties and interest that accumulate quickly. Even if you don't owe any tax, failing to file on time can result in penalties. Colorado has automated penalty calculations, so consistent late filing becomes expensive and may trigger additional scrutiny from the Department of Revenue.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.