.png)

Cost segregation is a tax strategy that identifies and reclassifies personal property assets within a building to accelerate depreciation deductions. Instead of depreciating your entire property over 27.5 or 39 years, a cost segregation study separates components like electrical systems, HVAC, flooring, and landscaping that can be depreciated over 5, 7, or 15 years. This front-loads tax deductions, reducing your current tax bill by 20-40% and immediately increasing cash flow you can reinvest.

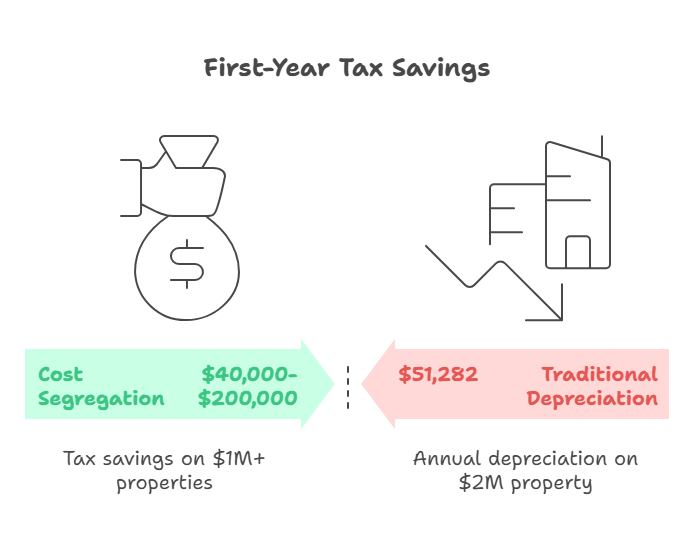

You just closed on a $2 million commercial property. Your CPA tells you to depreciate it over 39 years, that's $51,282 annually. Meanwhile, you're writing checks for $480,000 in taxes over the next decade. There's a better way that the IRS explicitly allows but most property owners never hear about.

Cost segregation studies let you reclassify 20-40% of your building's purchase price into shorter depreciation periods. Real estate investors who use this strategy typically generate $40,000-$200,000 in first-year tax savings on properties worth $1 million or more. Here's exactly how it works, when it makes sense, and what the actual ROI looks like based on real analyses we've completed.

A cost segregation study is a detailed engineering-based analysis that breaks down your building's components and reclassifies assets from 27.5-year or 39-year property into 5-year, 7-year, or 15-year property classes. The IRS recognizes these shorter depreciation schedules for personal property and land improvements separate from the building structure itself.

Here's what gets reclassified: electrical systems dedicated to specific equipment, specialty lighting, carpeting and flooring, built-in cabinets and shelving, security systems, decorative finishes, HVAC components, parking lots, sidewalks, and landscaping. These items depreciate faster than the building as a whole.

The study allocates your property's total cost basis across these asset classifications. If you paid $2 million for a commercial property, the analysis might identify $600,000 in 5-year property, $200,000 in 15-year property, and $1.2 million in 39-year property. This reclassification dramatically accelerates your depreciation deductions in early years of ownership.

The tax benefits of a cost segregation study come from timing. Standard depreciation spreads deductions evenly over 27.5 years for residential properties and 39 years for commercial property. Cost segregation front-loads those deductions, putting more money back in your pocket today rather than decades from now.

Real numbers: A property owner with a $3 million commercial building typically has $900,000-$1.2 million in assets that qualify for accelerated depreciation. In year one, instead of claiming $76,923 in depreciation ($3M ÷ 39 years), you might claim $280,000-$350,000 after reclassification. At a 35% combined tax rate, that's an additional $71,000-$95,000 in cash you keep.

The study results show immediate impact. Most property owners recoup the cost of the study, typically $5,000-$15,000 depending on the property type and complexity, in the first year through tax savings alone. The ROI on cost segregation analyses averages 10:1 to 30:1 for properties over $1 million.

Bonus depreciation amplifies these benefits. Through 2025, you can immediately deduct 60% of the value of 5-year and 15-year property placed into service (declining to 40% in 2026, 20% in 2027, and zero in 2028). This creates enormous first-year deductions that can offset rental income or, if you're a real estate professional, other income types.

The process starts with assembling documentation: closing statements, blueprints, construction invoices, property appraisals, and any improvement records. If original documents aren't available, the engineering team conducts a detailed site inspection, photographing and measuring every component.

Engineers and tax specialists then categorize every asset using IRS guidelines and relevant case law. They separate personal property (equipment, fixtures, movable items) from structural components, identify land improvements (parking, landscaping, exterior lighting), and allocate costs using engineering-based methodologies the IRS accepts.

The deliverable is a comprehensive report documenting the basis allocation, depreciation schedules, and the methodology used. This report includes hundreds of line items showing exactly what was reclassified and why. You file this information with Form 3115 (Application for Change in Accounting Method) to implement the new depreciation schedule on your tax return.

The entire process typically takes 4-8 weeks from start to report delivery, depending on property complexity and documentation availability. Studies can be performed on properties you've owned for years, the IRS allows retroactive studies through a "look-back" analysis that captures missed deductions from prior years without amending returns.

Properties worth $500,000 or more typically justify the cost of a study, though the sweet spot is $1 million and above. The benefits scale with property value, larger properties have more components to reclassify and generate bigger tax savings that far outweigh the cost of the study.

Commercial properties deliver the best results: retail buildings, office complexes, medical facilities, warehouses, hotels, restaurants, and mixed-use developments. These properties have extensive electrical systems, specialized HVAC, custom finishes, and significant land improvements that qualify for accelerated depreciation.

Residential rental properties also benefit, especially apartment buildings with 20+ units, student housing complexes, or upscale residential developments with high-end amenities. The amount of short-life property in these buildings, appliances, flooring, lighting, security systems, creates substantial reclassification opportunities.

Recently purchased or constructed properties offer the largest benefit because you capture the maximum depreciation deductions going forward. However, properties you've held for years still benefit through the look-back provision. You'll pay some depreciation recapture when you eventually sell, but the time value of money and increased cash flow now typically far outweigh that future cost.

Cost segregation studies range from $5,000 to $25,000 depending on property size, complexity, and documentation availability. A straightforward office building runs $7,000-$12,000, while a specialized facility with extensive custom improvements might cost $15,000-$20,000.

The benefits often outweigh the costs even when you factor in eventual depreciation recapture. When you sell the property, the IRS recaptures accelerated depreciation as ordinary income (up to 25% rate) rather than capital gains (20% rate). However, the immediate cash flow increase and the time value of money typically make this worthwhile.

Working with experienced providers matters. Our cost segregation accounting services include both the engineering study and tax implementation, ensuring your depreciation schedules comply with IRS requirements while maximizing your deductions.

The IRS explicitly permits cost segregation studies under tax law. The Hospital Corporation of America v. Commissioner case in 1997 established that taxpayers can use engineering-based cost segregation to identify assets with shorter recovery periods. IRS Audit Technique Guide 3.20 provides detailed guidance on acceptable methodologies.

You must file Form 3115 to change your accounting method when implementing cost segregation on properties placed into service in prior years. For newly purchased or constructed properties, you simply report the accelerated depreciation on your current tax return without needing Form 3115.

Studies must use acceptable methodologies: detailed engineering, residual estimation, sampling, or survey approaches. The IRS favors detailed engineering studies because they provide the most supportable documentation if audited. Your report should include photographs, floor plans, cost estimates, and detailed explanations of the allocation methodology.

Proper documentation is critical. The study must show that reclassified assets are truly personal property or land improvements rather than structural components. For example, general lighting is structural, but specialty retail lighting fixtures are personal property. HVAC serving the entire building is structural, but dedicated HVAC for a server room is equipment.

Understanding these nuances requires expertise, which is why many real estate investors work with specialists. Our comprehensive tax planning strategies incorporate cost segregation as part of a broader approach to minimizing tax liability legally and sustainably.

The main downside is depreciation recapture when you sell. Assets depreciated under shorter schedules get recaptured as ordinary income (up to 25%) rather than capital gains (20%). However, most property owners hold for 5-10+ years, and the present value of immediate tax savings exceeds the future recapture cost.

Poorly executed studies create audit risk. The IRS scrutinizes aggressive reclassifications, especially when the methodology isn't well-documented or when personal property percentages seem unreasonably high. Using qualified professionals who follow IRS guidelines minimizes this risk significantly.

Some taxpayers can't fully utilize the deductions immediately due to passive activity loss limitations. If you're not a real estate professional and your adjusted gross income exceeds $150,000, you can't deduct rental losses against other income. The deductions carry forward, but you lose the time value of money benefit.

The upfront cost might not justify the study for smaller properties. Properties under $500,000 rarely generate enough additional deductions to offset the $5,000-$15,000 study cost. Run the numbers first, our team provides preliminary analyses to determine whether cost segregation makes financial sense for your specific situation.

Timing matters. Perform the study in the year you acquire or complete construction on the property to maximize depreciation deductions going forward. Even if you've owned the property for years, a look-back study captures all the deductions you should have taken, creating a large "catch-up" deduction in the current year.

Combine cost segregation with bonus depreciation while it's still available. The 60% bonus depreciation in 2025 means you can immediately deduct more than half the value of reclassified 5-year and 15-year property. This creates massive first-year deductions that dramatically reduce your tax bill.

Consider selling properties strategically. If you're planning to sell within 1-2 years, cost segregation might not make sense because you'll immediately face recapture. However, if you're holding 5+ years or doing a 1031 exchange, the benefits typically far outweigh the recapture costs.

Use the cash flow increase strategically. The $50,000-$150,000 in tax savings can be reinvested into property improvements, used to acquire additional properties, or deployed to pay down high-interest debt. Real estate investors who compound these savings build portfolios faster than those who ignore cost segregation.

Partner with professionals who understand the complete financial picture. The interaction between cost segregation, entity structure, passive activity rules, and long-term holding strategy requires sophisticated tax planning. Our fractional CFO services help real estate investors optimize their entire tax and financial strategy, not just individual tactics.

You should consider a cost segregation study if you own commercial or residential rental property worth $500,000 or more, especially if you purchased or completed construction in the last 1-3 years. The immediate tax savings and cash flow increase typically justify the study cost many times over.

Newly acquired properties offer the best opportunity because you capture maximum deductions going forward. However, properties held for years still benefit, the IRS allows look-back studies that generate large catch-up deductions in the current tax year without amending prior returns.

Real estate professionals who can offset active income with rental losses benefit most, but even passive investors gain from increased cash flow and the ability to carry forward unused losses to future years when they might have more passive income or eventually sell the property.

The break-even calculation is straightforward: if the study costs $10,000 and your combined tax rate is 35%, you need to generate at least $28,571 in additional depreciation to break even in year one ($28,571 × 35% = $10,000). Properties over $1 million typically generate $150,000-$400,000 in additional first-year depreciation, making the ROI 5x to 15x even in year one.

Madras Accountancy provides cost segregation studies backed by licensed engineers and CPAs, ensuring your documentation withstands IRS scrutiny. Since 2015, we've completed analyses for 150+ real estate investors, identifying an average of $180,000 in additional first-year deductions per property. Our offshore partnership model delivers the same quality as big-firm studies at 40% lower cost.

Bottom Line: Cost segregation studies generate 10x to 30x ROI for real estate investors by reclassifying 20-40% of building costs into 5-year, 7-year, or 15-year depreciation schedules. Properties worth $1 million typically see $40,000-$200,000 in first-year tax savings, creating immediate cash flow you can reinvest to accelerate portfolio growth.

Next Steps:

Cost segregation studies range from $5,000 to $25,000 depending on property size, complexity, and available documentation. A standard commercial building runs $7,000-$12,000, while complex properties with extensive custom improvements cost $15,000-$20,000. The study typically pays for itself in the first year through tax savings, with most properties generating 10x to 30x ROI over the holding period.

Yes, the IRS allows look-back studies on properties you've owned for any length of time. You file Form 3115 to change your accounting method, which generates a large "catch-up" deduction in the current tax year for all the depreciation you should have claimed in prior years. You don't need to amend previous returns, all the benefit flows through the current year's return.

The IRS recaptures depreciation when you sell, taxing the accelerated portion as ordinary income at rates up to 25% rather than the lower capital gains rate of 20%. However, the time value of money typically makes cost segregation worthwhile, having $100,000 today is more valuable than paying $25,000 in extra taxes 10 years from now. Plus, if you do a 1031 exchange, you defer recapture indefinitely.

Yes, cost segregation works well for residential rental properties, especially apartment buildings with 20+ units or upscale properties with high-end finishes and amenities. Residential properties have appliances, flooring, specialty lighting, security systems, and landscaping that can be reclassified into 5-year, 7-year, or 15-year property. Properties over $1 million typically see $30,000-$150,000 in first-year tax savings.

Cost segregation typically makes financial sense for properties worth $500,000 or more, though the sweet spot is $1 million and above. Below $500,000, the $5,000-$15,000 study cost might not be justified by the additional deductions. Run a preliminary analysis to determine the ROI for your specific property, if the first-year tax savings exceed 3x the study cost, it's usually worth doing.

No, properly executed cost segregation studies don't increase audit risk. The IRS explicitly permits cost segregation under established tax law and provides detailed guidance in Audit Technique Guide 3.20. However, poorly documented studies or aggressive reclassifications can attract scrutiny. Working with qualified engineers and CPAs who follow IRS methodologies ensures your study withstands audit if selected for review.

Yes, but passive activity loss rules may limit immediate benefits. If your adjusted gross income exceeds $150,000 and you're not a real estate professional, you can't deduct rental losses against other income. However, you still benefit from reduced rental income taxes, and unused losses carry forward to offset future rental income or gains when you sell. The increased cash flow from lower taxes is still valuable.

Madras Accountancy provides complete cost segregation services combining licensed engineering analysis with CPA-level tax implementation. We've completed studies for 150+ investors since 2015, identifying an average of $180,000 in first-year deductions per property. Our offshore partnership model delivers big-firm quality at 40% lower cost, studies that would cost $15,000-$20,000 elsewhere typically run $9,000-$12,000 with our team. We handle everything from initial analysis through IRS compliance documentation.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.