.png)

Credit unions operate in a tightly regulated environment that emphasizes member trust, fiduciary responsibility, and regulatory compliance. As member-owned financial cooperatives, they are held to high standards when it comes to transparency, asset quality, and internal controls.

Audits are a central part of ensuring that credit unions remain compliant, secure, and financially sound. Whether federally or state-chartered, every credit union must conduct annual supervisory committee audits, maintain sound internal audit procedures, and comply with National Credit Union Administration (NCUA) requirements.

For CPA firms that specialize in auditing financial institutions, credit unions present a unique blend of complexity and mission-driven accountability. Audit procedures must not only validate the accuracy of financial statements but also ensure that the organization follows operational and regulatory expectations.

This guide outlines the mandatory audit requirements, compliance standards, best practices, and common pitfalls encountered in credit union audits. It is designed for both internal audit teams and external CPA firms looking to enhance their audit approach.

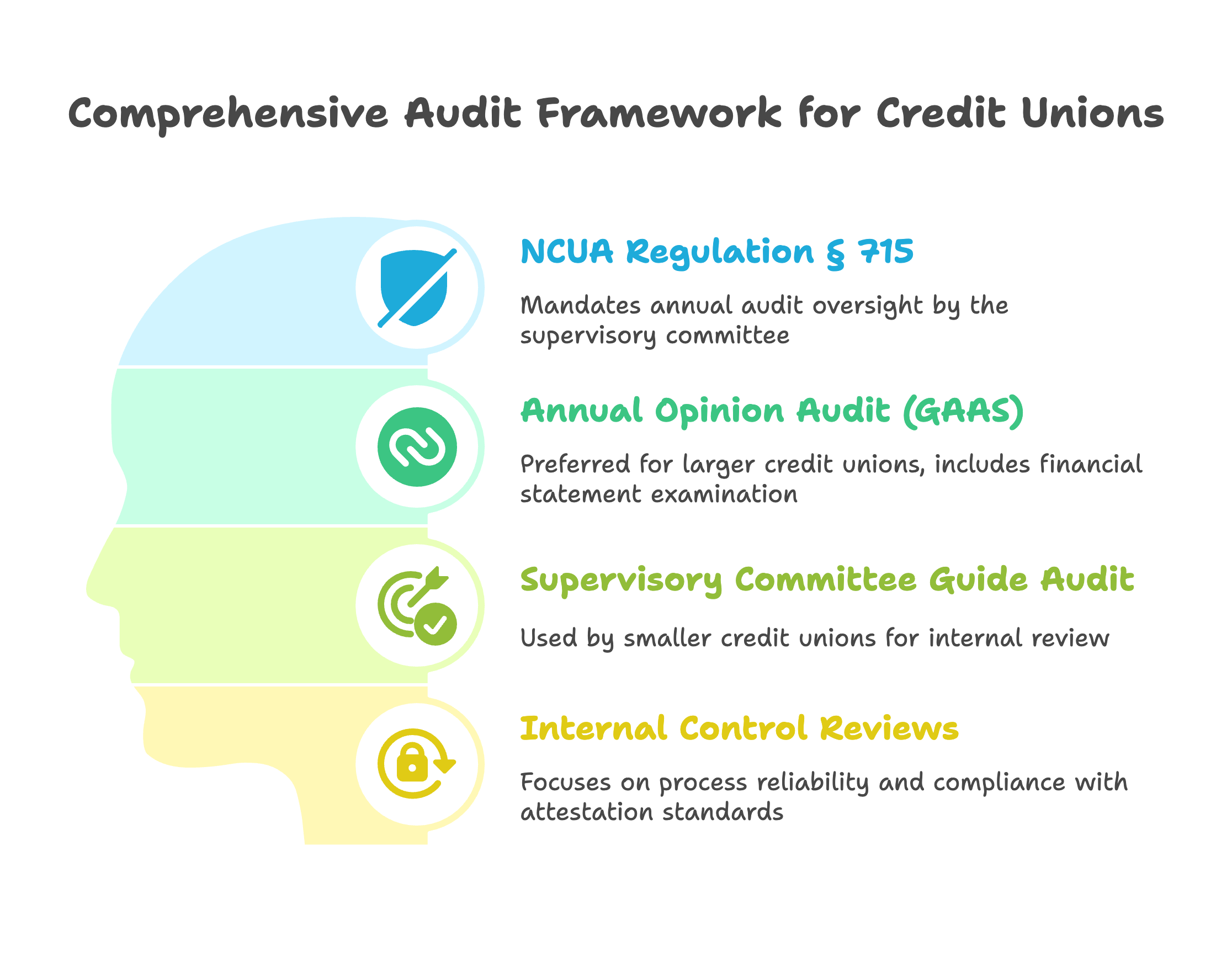

Audit obligations differ based on a credit union’s charter type, asset size, and whether it is federally or state-regulated. However, all credit unions must comply with the foundational requirements set by the NCUA.

The NCUA mandates annual audit oversight by the supervisory committee or its equivalent. The committee must either:

Credit unions with assets above $500 million are generally expected to obtain an annual independent opinion audit conducted in accordance with GAAS (Generally Accepted Auditing Standards).

For larger credit unions, the preferred option is a full opinion audit. This includes:

Opinion audits provide the most assurance and are typically conducted by an external CPA firm.

Smaller credit unions may use the NCUA Supervisory Committee Guide. This is a step-by-step tool for performing a comprehensive internal review. It does not offer the same level of assurance as an opinion audit but is acceptable for credit unions below certain asset thresholds.

The guide covers:

The committee must maintain documentation and provide reports to management and the board.

Some credit unions opt for Agreed-Upon Procedures (AUP) engagements or internal control audits that focus on process reliability rather than full financial statement testing. These engagements must comply with attestation standards and require clear definition of scope and methodology.

Credit union audits go beyond just financial statements. There are broader compliance requirements set by different regulatory authorities.

The NCUA is the primary regulator for federally chartered credit unions. It sets audit expectations, supervises financial safety, and ensures credit unions follow consumer protection laws.

Key audit-related functions of the NCUA include:

State-chartered credit unions must follow the audit rules set by their respective state regulators. These often align with NCUA guidelines but may include extra procedures or expanded scope.

CPA firms auditing state-chartered credit unions must understand both NCUA and state-specific regulations.

The FFIEC provides guidance on cybersecurity, BSA/AML compliance, IT audits, and examination protocols. FFIEC manuals often serve as references during the audit of IT systems or compliance functions.

While the CFPB does not directly mandate audit procedures, its regulations (e.g., Truth in Lending, Fair Lending, RESPA) impact credit union policies and disclosures. Auditors may need to test compliance with these regulations as part of operational audits.

Loan portfolios are often the largest asset category. Auditors must:

Documentation, internal modeling, and historical loss analysis are all reviewed for accuracy.

Deposit accounts must be verified for accuracy and compliance with disclosures. Auditors check:

Segregation of duties in handling member funds is also reviewed.

Credit unions often maintain investment portfolios to manage liquidity. Auditors evaluate:

Audit procedures should align with NCUA investment guidelines.

Credit unions must have effective internal controls over:

Auditors test control design and implementation, focusing on fraud risk mitigation.

Given the rise in cybersecurity threats, auditors must review:

Some firms use IT audit specialists or follow FFIEC IT handbooks.

Bank Secrecy Act and Anti-Money Laundering compliance are critical. Audit procedures include:

A BSA audit is typically conducted annually as a separate engagement or integrated into the supervisory audit.

Many credit unions operate with a three-line defense model:

CPA firms may assist in developing internal audit programs or provide co-sourced support for:

Credit unions occupy a unique position in the financial ecosystem, balancing fiduciary responsibility with a member-first mission. This makes audits not just a compliance formality but a vital tool to safeguard members’ assets, improve operations, and strengthen oversight.

CPA firms serving credit unions must bring not only technical audit knowledge but also an understanding of regulatory expectations, operational nuances, and cooperative principles. By adopting a risk-based approach, leveraging modern audit tools, and building collaborative relationships, both auditors and credit union leaders can foster a strong culture of transparency and control.

Question: What are the primary audit requirements that apply to credit unions?

Answer: Credit union audit requirements include annual independent audits for credit unions with assets over $500 million, supervisory committee audits for smaller credit unions, and compliance with National Credit Union Administration (NCUA) regulations. Federal credit unions must follow NCUA audit requirements while state-chartered credit unions comply with both state and federal regulations. Audit requirements cover financial statement accuracy, internal control evaluation, regulatory compliance assessment, and risk management review. Additional requirements include Bank Secrecy Act compliance, member account verification, loan portfolio testing, and investment portfolio evaluation. Professional audits must be conducted by independent CPAs with credit union experience and knowledge of regulatory requirements. Audit scope includes operational efficiency, fraud prevention, and adherence to credit union industry standards and best practices.

Question: How do NCUA regulations affect credit union audit procedures and scope?

Answer: NCUA regulations significantly affect credit union audit procedures by establishing specific requirements for audit scope, timing, auditor qualifications, and reporting standards. Regulations mandate evaluation of lending practices, investment compliance, liquidity management, and capital adequacy. NCUA examination procedures influence audit risk assessments, testing requirements, and regulatory compliance evaluation. Auditors must understand NCUA rules regarding member business lending, field of membership compliance, and prompt corrective action requirements. Regulatory changes require ongoing audit procedure updates and auditor training on credit union-specific requirements. Professional auditors must maintain knowledge of NCUA regulations, examination procedures, and enforcement actions affecting audit planning and execution. Coordination with NCUA examinations helps ensure comprehensive coverage while avoiding duplication of effort.

Question: What specific compliance areas require focus during credit union audits?

Answer: Key compliance areas for credit union audits include Bank Secrecy Act and anti-money laundering procedures, member eligibility and field of membership requirements, lending regulation compliance, and investment policy adherence. Additional focus areas cover consumer protection regulations, truth in lending compliance, fair credit reporting adherence, and privacy regulation implementation. Operational compliance includes board governance, committee responsibilities, insurance coverage requirements, and record retention policies. Safety and soundness compliance covers capital adequacy, asset quality, management effectiveness, earnings adequacy, and liquidity management (CAMEL ratings). Professional audit procedures must address regulatory examination findings, corrective action compliance, and ongoing monitoring of regulatory requirements. Technology compliance includes cybersecurity, data protection, and system security requirements.

Question: How do credit union audits differ from bank audits in terms of scope and approach?

Answer: Credit union audits differ from bank audits due to unique regulatory structure, member-owned cooperative structure, tax-exempt status, and specific NCUA requirements. Credit unions focus on member service rather than profit maximization, affecting performance evaluation and strategic assessment. Field of membership restrictions, member business lending limitations, and investment restrictions create unique compliance considerations. Governance structures differ with member-elected boards, supervisory committees, and volunteer leadership affecting internal control evaluation. Tax compliance involves different considerations due to federal income tax exemption and potential unrelated business income. Risk assessment must consider cooperative philosophy, member loyalty factors, and community-focused lending practices. Professional auditors need specialized knowledge of credit union operations, regulations, and industry characteristics for effective audit performance.

Question: What are the supervisory committee audit responsibilities and requirements?

Answer: Supervisory committee audit responsibilities include overseeing independent audits, conducting verification procedures, ensuring regulatory compliance, and reporting findings to membership and regulators. Committees must verify member accounts, review loan documentation, evaluate internal controls, and assess management performance. Requirements include quarterly financial reviews, annual audit oversight, examination of significant transactions, and evaluation of fraud prevention procedures. Supervisory committees ensure auditor independence, review audit findings, monitor management responses, and communicate with regulators when necessary. Professional responsibilities include maintaining confidentiality, exercising due diligence, and ensuring adequate audit coverage. Training requirements help committee members understand their oversight role, regulatory expectations, and effective audit monitoring procedures. Clear documentation and reporting procedures ensure accountability and regulatory compliance.

Question: What internal control considerations are critical in credit union audits?

Answer: Critical internal control considerations in credit union audits include segregation of duties, approval hierarchies, dual control procedures, and member account protection measures. Key controls cover lending authorization, investment approval, cash handling, and information technology security. Evaluate controls over member eligibility verification, account opening procedures, loan origination, and funds transfer authorization. Technology controls include system access, data integrity, backup procedures, and cybersecurity measures. Fraud prevention controls cover employee background checks, transaction monitoring, and whistleblower procedures. Professional evaluation considers control design effectiveness, operating efficiency, and regulatory compliance. Small credit union controls may rely heavily on management oversight and board involvement due to limited staff segregation capabilities. Documentation requirements ensure audit evidence supports control evaluation conclusions.

Question: How should credit union auditors address cybersecurity and information technology risks?

Answer: Address credit union cybersecurity and IT risks through comprehensive risk assessment, control testing, incident response evaluation, and regulatory compliance review. Evaluate information security policies, access controls, data encryption, and network security measures. Test backup and recovery procedures, business continuity planning, and incident response capabilities. Review vendor management for third-party service providers, cloud computing arrangements, and technology outsourcing agreements. Assess member data protection, privacy compliance, and breach notification procedures. Professional procedures include penetration testing evaluation, vulnerability assessment review, and security awareness training effectiveness. Consider NCUA cybersecurity examination procedures and industry best practices for credit union technology environments. Coordination with IT specialists may be necessary for complex technology environments and emerging cyber threats.

Question: What are the emerging challenges and trends affecting credit union audits?

Answer: Emerging credit union audit challenges include fintech integration, digital banking transformation, cryptocurrency considerations, and regulatory technology compliance. Trends include increased focus on cybersecurity, data analytics utilization, remote auditing capabilities, and environmental, social, and governance (ESG) considerations. Artificial intelligence and machine learning applications require new audit approaches and risk assessments. Open banking, API integrations, and third-party partnerships create expanded audit scope and vendor risk considerations. Professional development requirements include technology training, regulatory update education, and specialized industry knowledge maintenance. Future challenges may include central bank digital currencies, enhanced payment systems, and evolving member expectations for digital services. Auditor adaptability and continuous learning ensure effective audit performance in changing credit union environments while maintaining regulatory compliance and member protection.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.