Shops run on cash and trust. Both slip when returns spike, chargebacks pile up, or tax numbers do not tie to payouts. This playbook turns those moving parts into a simple, auditable routine for US and UK teams, including those working with offshore accountants. It covers how to model return reserves, manage card disputes, and reconcile marketplace facilitator taxes without guesswork. It is a practical guide to Ecommerce Finance Ops: Return Reserves, Chargebacks, and Sales Tax Reconciliation.

What this section covers

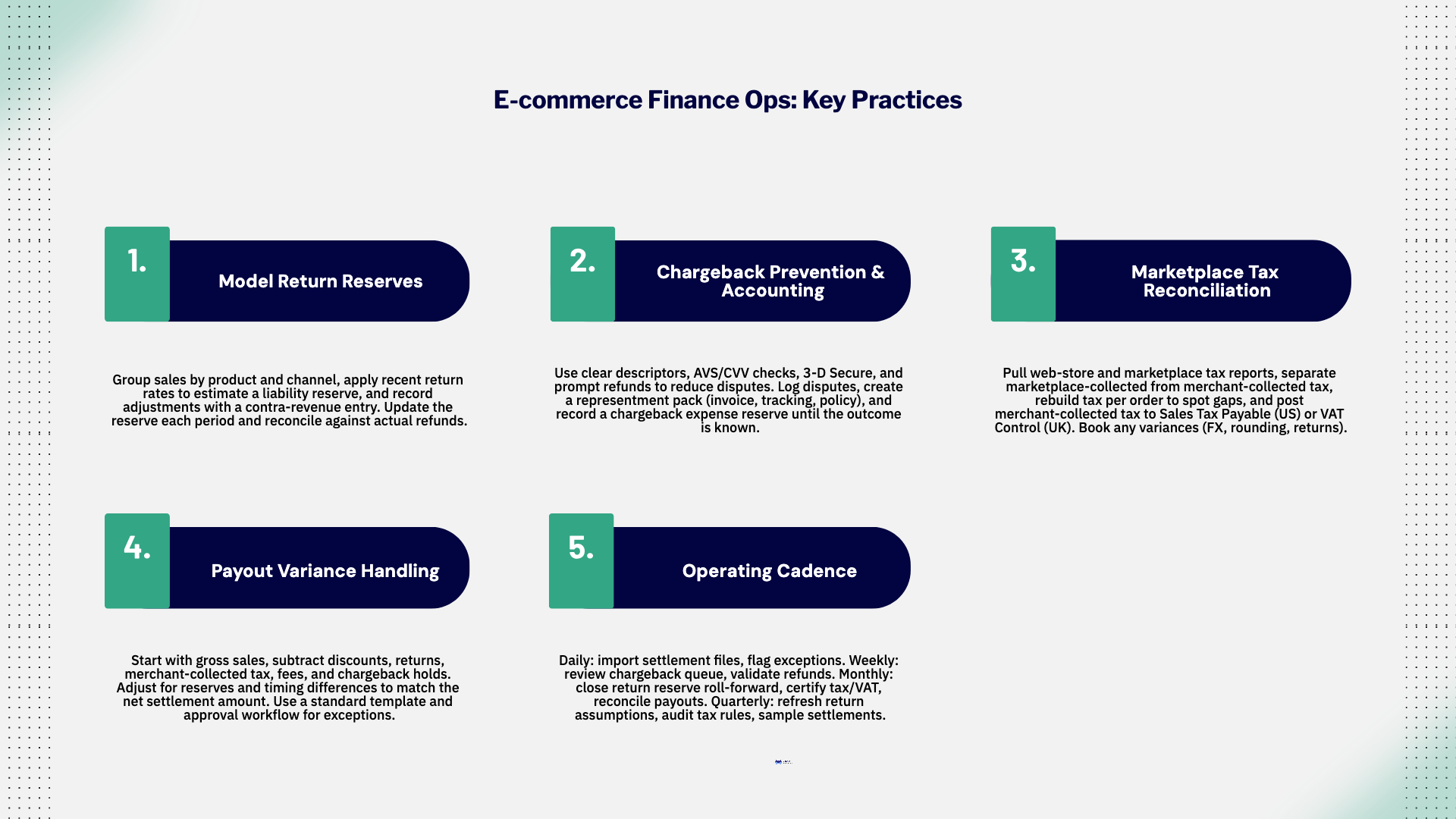

- A clean method to forecast and book return reserves and allowances

- A step-by-step chargeback process with prevention and accounting treatment

- A monthly sales tax/VAT reconciliation across marketplaces and your web store

- Payout variance handling so settlements, fees, and refunds tie to the GL

Key definitions

- Return reserve (refund liability). An estimate of future refunds on current-period sales. Booked as a liability with a matching expense or contra-revenue.

- Chargeback. A cardholder dispute that reverses a payment and adds network/acquirer fees.

- Marketplace facilitator tax. Sales tax (US) or VAT (UK) collected and remitted by marketplaces (e.g., Amazon, eBay) on your behalf.

- Settlement report. The marketplace or PSP file that shows gross sales, tax, fees, refunds, chargebacks, and the net payout.

1) Return reserves and allowances

The model

- Cohort the sales. Group by product category and channel (website, Amazon, eBay, etc.).

- Measure observed return rates. Use a rolling lookback (e.g., last 8–12 weeks) by cohort.

- Exclude non-refundable items. Gift cards, final sale, per policy.

- Apply the expected rate to current-period gross sales to estimate the reserve.

- Layer reasons. Size, damage, late delivery. Some reasons imply restocking fees or write-off of COGS.

Formula (period-end):

Return reserve = Σ (Eligible sales by cohort × Expected return rate × Expected refund %)

Example entries

- To set or adjust the reserve:

- Dr Returns and Allowances (contra-revenue)

- Cr Refund Liability (returns reserve)

- When refund is issued:

- Dr Refund Liability

- Cr Cash / Payments Payable

- Inventory effect (if goods return saleable):

- Dr Inventory / Cr COGS per policy and actual condition.

Controls and evidence

- Document method, cohorts, and lookback window.

- Tie reserve rollforward to refunds paid the next period.

- Keep a reason code report to prove assumptions.

Cut-off: Freeze the return file at period-end and track post-period approvals separately.

2) Chargebacks: prevention and accounting

Anatomy of a dispute

- Triggers: Fraud, item not received, not as described, duplicate charge, credit not processed.

- Windows: Networks set timeframes for merchant response; treat all alerts as urgent.

- Outcomes: Represented (won), written off (lost), or auto-closed (no response).

Prevention playbook

- Clear billing descriptor and customer emails with order details.

- AVS/CVV checks, 3-D Secure where appropriate, velocity rules, and device profiling.

- Delivery proof for physical goods; usage logs for digital services.

- Refunds processed promptly with notification.

Representment pack

- Order invoice, tracking and delivery confirmation, customer communication, refund/return policy excerpt, and proof of usage where relevant.

- Submit within the acquirer’s window; track by dispute reason code.

Accounting treatment

- On notification (dispute hold):

- Dr Chargeback Expense (or a separate dispute reserve)

- Cr Payments Payable / Chargebacks Clearing

- If won: reverse the expense and clear the hold when funds are released.

- If lost: keep the expense and record any network fees.

KPI: Chargeback rate (count or amount) as a percent of processed payments by channel; dispute win rate; average response time.

3) Sales tax and VAT: marketplace facilitator reconciliation

What changes on marketplaces

- US: Many states require marketplaces to collect and remit sales tax on your marketplace sales. Your web store often remains your liability.

- UK: Marketplaces can be deemed suppliers for certain transactions, especially cross-border B2C; they may collect VAT on your behalf. Your own site typically requires VAT registration and returns if you meet thresholds.

Monthly reconciliation steps

- Pull source data:

- Web store tax report from your tax engine (e.g., by jurisdiction).

- Marketplace settlement reports with tax collected by the marketplace.

- Split by channel: “Marketplace-collected” vs “Merchant-collected.”

- Compute expected tax: Rebuild tax per order from your ledger to spot configuration gaps (shipping taxability, discounts, exemptions, rounding).

- Tie to GL:

- Marketplace-collected tax should not sit in your tax payable; treat as pass-through shown in settlement reports.

- Merchant-collected tax should roll to Sales Tax Payable (US) or VAT Control (UK).

- Book variances: FX differences, rounding, late refunds, or jurisdiction mapping fixes.

Common breaks

- Returns posted after the marketplace payout.

- Ship-from vs ship-to misconfiguration.

- Tax on shipping mis-set.

- Missing exemption certificates (US) or zero-rating rules (UK) not applied.

4) Payout variance handling

Why payouts rarely equal your GL

- Timing: refunds, chargebacks, and reserve releases hit after the sales day.

- Fees: card network, acquirer, marketplace, and cross-border or FX fees.

- Reserves: PSP rolling reserves or marketplace holds.

Reconciliation pattern

- Start with gross sales per channel.

- Less discounts/returns (by posting date).

- Less tax (merchant-collected only).

- Less fees (PSP, marketplace, FX).

- Adjust for chargebacks/holds and prior-period corrections.

- The result should match the net settlement for the batch.

Controls: A standard reconciliation template per channel; ticketed approvals for write-offs above threshold.

Operating cadence (offshore-friendly)

- Daily: Import settlement files; flag exceptions; send dispute alerts to a shared inbox.

- Weekly: Review chargeback queue; validate refunds vs reserve usage.

- Monthly: Close return reserve rollforward; certify sales tax/VAT by channel; complete payout recs with sign-off.

- Quarterly: Refit return rate assumptions; review tax engine rules; sample settlements to original orders.

Audit-ready evidence you should keep

- Reserve methodology memo and rollforward.

- Chargeback case files and outcomes; fee schedules.

- Marketplace tax reports and web store tax engine exports; filings and payments.

- Payout reconciliation workbooks with tie-outs to the GL and bank.

Summary

Strong ecommerce finance ops are built on simple, repeatable math. Model returns by cohort, treat disputes as a process not a fire drill, and reconcile taxes and payouts by channel every month. Do that consistently and cash stays predictable, fees stay low, and audits go smoothly.

%2075-100%20(12).png)

%2075-100%20(9).png)