.png)

Tax season rolls around every year, and you're faced with the same question: should you take the standard deduction or itemize your deductions on your tax return? If you're like most taxpayers, you want to make sure you're getting every dollar you deserve back from the IRS, but figuring out which approach saves you more money can feel overwhelming.

The good news is that understanding when to itemize deductions on Form 1040 isn't as complicated as it might seem. With the right information, you can make a smart decision that puts more money back in your pocket and reduces your tax bill. Let's walk through everything you need to know about itemized tax deductions and how they work with your Form 1040.

The standard deduction is like a guaranteed discount on your taxes. For the 2024 tax year, the standard deduction amounts are $14,600 for single filers, $29,200 for married filing jointly, and $21,900 for heads of household. These amounts are provided by the IRS and automatically reduce your taxable income without requiring any documentation.

When you itemize deductions, you're choosing to list specific expenses instead of taking that automatic discount. This makes sense when your total itemized deductions exceed your standard deduction amount. Think of it this way: if you can prove you spent more on deductible expenses than the IRS's standard allowance, you'll save more money by itemizing.

The decision comes down to simple math. Calculate your potential itemized deductions and compare them to your standard deduction for your filing status. Whichever number is higher will give you the larger tax savings and reduce your tax liability more effectively.

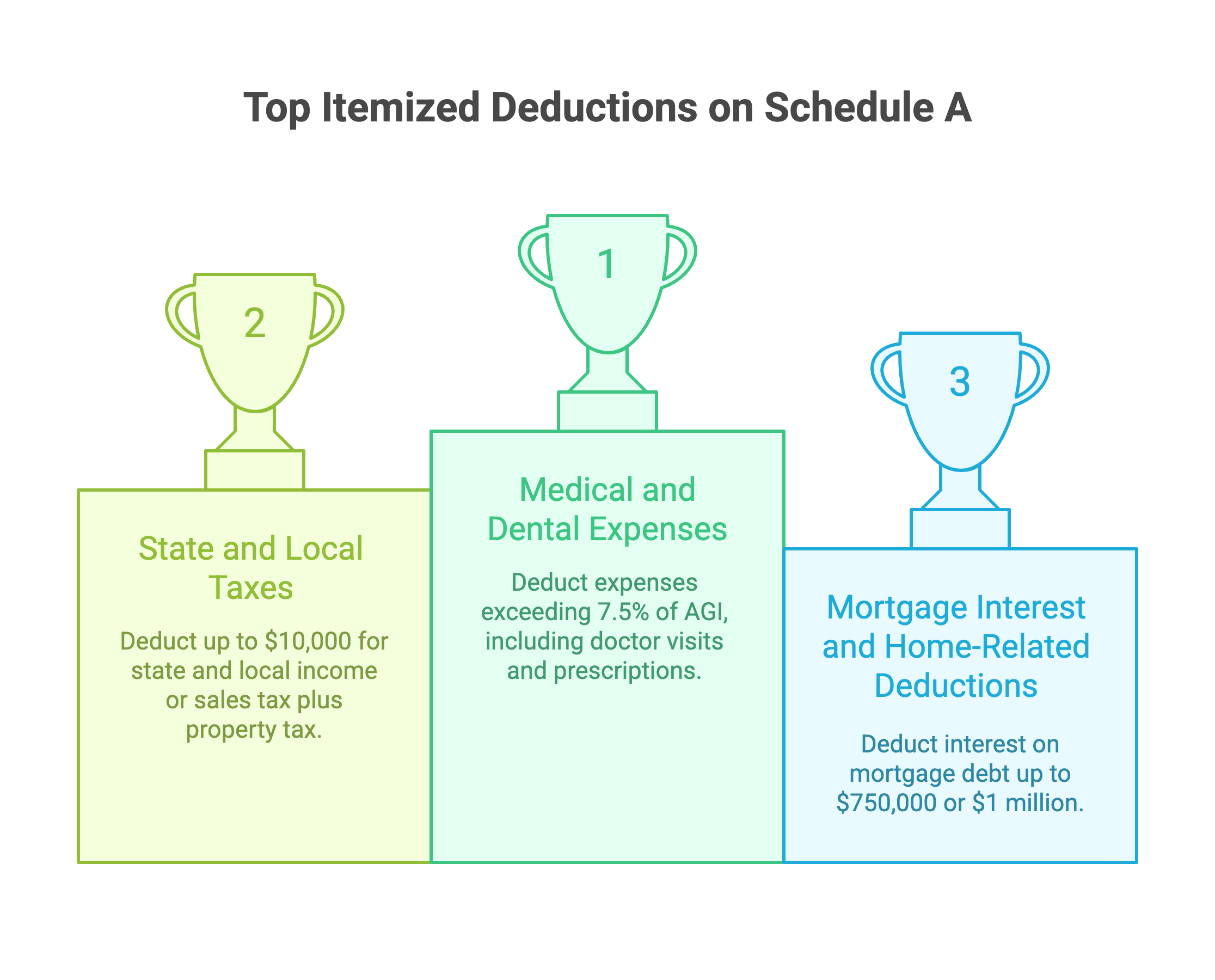

You can deduct medical and dental expenses that exceed 7.5% of your adjusted gross income (AGI). This includes doctor visits, prescription medications, dental work, and even some travel expenses for medical care. The threshold means you need significant medical expenses to benefit, but for those with chronic conditions or major medical events, this deduction can be substantial.

Keep detailed records of all medical expenses throughout the year. Even if you don't think you'll reach the threshold, unexpected medical costs can quickly add up, especially if you face emergency treatments or procedures.

The state and local tax deduction, often called the SALT deduction, allows you to deduct either state and local income taxes or sales tax, plus property taxes. However, the Tax Cuts and Jobs Act limited this deduction to $10,000 total for all state and local taxes combined.

This limitation significantly impacts taxpayers in high-tax states. Even if you paid more than $10,000 in state taxes and property taxes combined, you can only deduct up to the $10,000 limit on your federal return.

Home mortgage interest is often the largest itemized deduction for homeowners. You can deduct interest on mortgage debt up to $750,000 for homes purchased after December 15, 2017, or $1 million for homes purchased before that date. Your lender should provide Form 1098 showing the interest you paid.

Property taxes paid on your home also count toward your itemized deductions, but remember they're included in the $10,000 state and local tax limitation mentioned above.

Donations to qualified charitable organizations can be deducted when you itemize. This includes cash donations, donated goods, and even some volunteer expenses. Keep receipts for all donations, and for donations over $250, you need written acknowledgment from the charity.

The deduction amount for charitable contributions can be substantial, especially if you made significant donations during the tax year. Some taxpayers bunch their charitable giving into certain years to maximize the deduction benefit.

If you faced significant medical expenses, it might push your total deductions above the standard deduction amount. Major surgeries, ongoing treatments, or caring for family members with medical needs can result in substantial deductible expenses.

Calculate whether your medical expenses exceed 7.5% of your AGI. If they do, and when combined with other deductions like mortgage interest or state taxes, your total might exceed your standard deduction.

Homeowners often benefit from itemizing, especially in the early years of a mortgage when interest payments are highest. If you have a significant mortgage, pay substantial property taxes, or live in a state with high income taxes, itemizing frequently provides better tax savings.

The combination of mortgage interest, property taxes, and state income taxes can quickly add up to more than the standard deduction, even with the SALT limitation.

If you made substantial charitable contributions during the year, itemizing might be worthwhile. This is particularly true if you had a year with higher income and made correspondingly larger donations to favorite charities or causes.

Before you start filling out the schedule A form, gather all your supporting documents. This includes Form 1098 for mortgage interest, receipts for charitable donations, medical expense records, and documentation of state and local taxes paid.

Good record-keeping throughout the year makes tax filing much easier. Consider keeping a dedicated folder or digital file for tax-deductible expenses to avoid scrambling during tax season.

Schedule A is organized into clear sections that correspond to different types of deductions. Start with medical and dental expenses, then move through each category systematically. The form provides clear instructions for calculating deduction amounts and applying relevant limitations.

Take your time with each section to ensure accuracy. Errors on Schedule A can result in IRS notices or audits, so double-check your calculations and make sure you have proper documentation for all claimed deductions.

Don't forget about the various limitations that apply to different deductions. The 7.5% AGI threshold for medical expenses and the $10,000 cap on state and local taxes are easy to overlook but crucial for accurate calculations.

Also, avoid the temptation to inflate deductions or claim expenses that don't qualify. The IRS has sophisticated systems for detecting unusual deduction patterns, and having proper documentation is essential if you're selected for an audit.

The only way to know for sure which option saves you more money is to calculate both scenarios. Add up all your potential itemized deductions and compare that total to your standard deduction amount for your filing status.

Don't forget that itemizing requires more time and documentation, so factor in the effort involved when making your decision. If itemizing only saves you a small amount, the simplicity of the standard deduction might be worth considering.

Some situations make itemizing more attractive even when the numbers are close. If you expect higher deductible expenses in future years, establishing a pattern of itemizing might be beneficial. Similarly, if you're close to the itemizing threshold, small additional deductible expenses might tip the scales in favor of itemizing.

If you're unsure whether to itemize deductions or take the standard deduction, consider consulting with a tax professional. They can review your specific situation, identify potential deductions you might have missed, and help you make the decision that maximizes your tax savings.

Tax professionals also stay current on tax law changes that might affect your decision. Given the complexity of tax regulations and the potential for significant savings, professional guidance often pays for itself.

Start planning for next year's taxes now by establishing good record-keeping habits. Keep receipts for all potentially deductible expenses, even if you take the standard deduction this year. Your situation might change, making itemizing beneficial next year.

Consider using digital tools or apps to track expenses throughout the year. This makes tax preparation easier and ensures you don't miss any deductible expenses when it's time to file.

Understanding itemized deductions can help you make strategic financial decisions throughout the year. For example, if you're close to the itemizing threshold, bunching deductible expenses into one year might provide tax benefits.

This might involve timing charitable donations, medical procedures, or other deductible expenses to maximize their tax benefit.

When should I itemize deductions instead of taking the standard deduction on Form 1040?

You should itemize when your total itemized deductions exceed your standard deduction amount. For 2024, this means more than $14,600 for single filers or $29,200 for married filing jointly. Calculate both options to determine which saves more money.

What are the main itemized deductions I can claim on Schedule A?

Major itemized deductions include medical and dental expenses exceeding 7.5% of AGI, state and local taxes up to $10,000, mortgage interest on qualified home loans, and charitable contributions to qualified organizations.

How do I know if my medical expenses qualify for the itemized deduction?

Medical expenses must exceed 7.5% of your adjusted gross income to be deductible. Include doctor visits, prescriptions, dental work, and medical travel. Keep all receipts and calculate the total against your AGI threshold.

What's the limit on state and local tax deductions for itemizing?

The state and local tax (SALT) deduction is limited to $10,000 total for all state and local taxes combined, including income taxes, sales taxes, and property taxes. This limit applies regardless of filing status.

Can I deduct mortgage interest if I itemize deductions?

Yes, you can deduct mortgage interest on loans up to $750,000 for homes purchased after December 15, 2017, or $1 million for earlier purchases. Your lender provides Form 1098 showing deductible interest paid.

How do charitable contribution deductions work when itemizing?

You can deduct donations to qualified charitable organizations when itemizing. Keep receipts for all donations, and obtain written acknowledgment for donations over $250. The deduction reduces your taxable income dollar-for-dollar.

What records do I need to support my itemized deductions?

Keep receipts, canceled checks, and official statements for all claimed deductions. This includes Form 1098 for mortgage interest, medical bills and insurance statements, tax payment records, and charitable donation receipts.

Can I switch between itemizing and standard deduction from year to year?

Yes, you can choose each year whether to itemize or take the standard deduction based on which provides better tax savings. Calculate both options annually, as your deductible expenses and the standard deduction amounts change over time.

Deciding whether to itemize deductions on your Form 1040 comes down to understanding your expenses and doing the math. While the standard deduction offers simplicity and works well for many taxpayers, itemizing can provide significant tax savings for those with substantial deductible expenses. Take the time to calculate both options, keep good records throughout the year, and don't hesitate to seek professional help when the decision isn't clear. The effort you put into understanding your options can result in meaningful tax savings that make the process worthwhile.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.