.png)

Auditing isn't just about ticking boxes. It's about trust.

When a company's financial statements are audited, what's really being tested is whether the process behind the numbers was done right, thoroughly, independently, and with care. That's where GAAS comes in.

Generally Accepted Auditing Standards (GAAS) form the foundation of U.S. audit quality. They're issued by the AICPA and define what a "good audit" should look like, no matter the firm, the client, or the size of the engagement. Whether you're a CPA, a student prepping for the AUD section of the CPA exam, or someone managing audit quality in a firm, understanding GAAS isn't optional. It's essential.

In this guide, we're focusing on the General Standards, the first and arguably most important layer of GAAS. These are the principles that shape every stage of an audit, from planning to execution. They determine who's qualified to audit, how impartial they must be, and what counts as a professionally sound job.

We'll break down what each standard means in practice, why they matter, and how to apply them in the real world. No jargon for the sake of it, just clear guidance for anyone who needs to understand what quality looks like in an audit.

Let's start with the full GAAS framework, and see where the General Standards fit in.

The phrase "Generally Accepted Auditing Standards" (GAAS) gets thrown around a lot, in textbooks, audit training, even peer reviews, but few take the time to really understand how it's structured or why it still matters in day-to-day practice.

GAAS, as issued by the American Institute of Certified Public Accountants (AICPA)'s Auditing Standards Board (ASB), outlines the minimum standards required for conducting an audit of private company financial statements in the U.S. Think of it as the blueprint for audit integrity, a way to standardize how audits are planned, executed, and reported so that users of financial statements (banks, investors, regulators) can trust the outcome.

GAAS is traditionally divided into three categories, each one targeting a critical stage of the audit process:

These standards govern the auditor's qualifications and ethics. It doesn't matter how well an audit is executed, if the person doing it isn't trained, impartial, or working diligently, the entire process is compromised. The general standards ensure:

These are the foundational expectations, and we'll dive into each one in the next section.

Once we know the auditor is qualified and ethical, the next concern is how the audit is carried out. These reporting standards focus on the audit process itself:

Poor planning or weak evidence gathering can tank an audit, even if the auditor is technically skilled. That's why fieldwork standards are so critical, they keep the audit grounded in real, verifiable work.

Finally, the output of the audit, the audit report, must accurately reflect what was found, and must be written in a way that doesn't mislead users. These standards govern:

This is where judgment, communication, and transparency all come into play.

GAAS operates within a broader framework of professional standards. For government entities, auditors must also comply with government auditing standards, commonly known as the yellow book, issued by the Government Accountability Office under the comptroller general. These generally accepted government auditing standards provide additional requirements for audits of federal programs and entities.

The Public Company Accounting Oversight Board (PCAOB) sets standards for publicly traded companies, while the Financial Accounting Standards Board establishes accounting standards. The Governmental Accounting Standards Board provides guidance for state and local government accounting.

Because if the auditor isn't competent, objective, or careful, none of the other standards matter. You can have perfect checklists and documentation, but without professional skepticism and sound judgment, the audit won't stand up under scrutiny.

In the next section, we'll break down each General Standard and explain what it really looks like in practice, whether you're preparing for a CPA exam or running quality control inside an audit firm.

Let's start there.

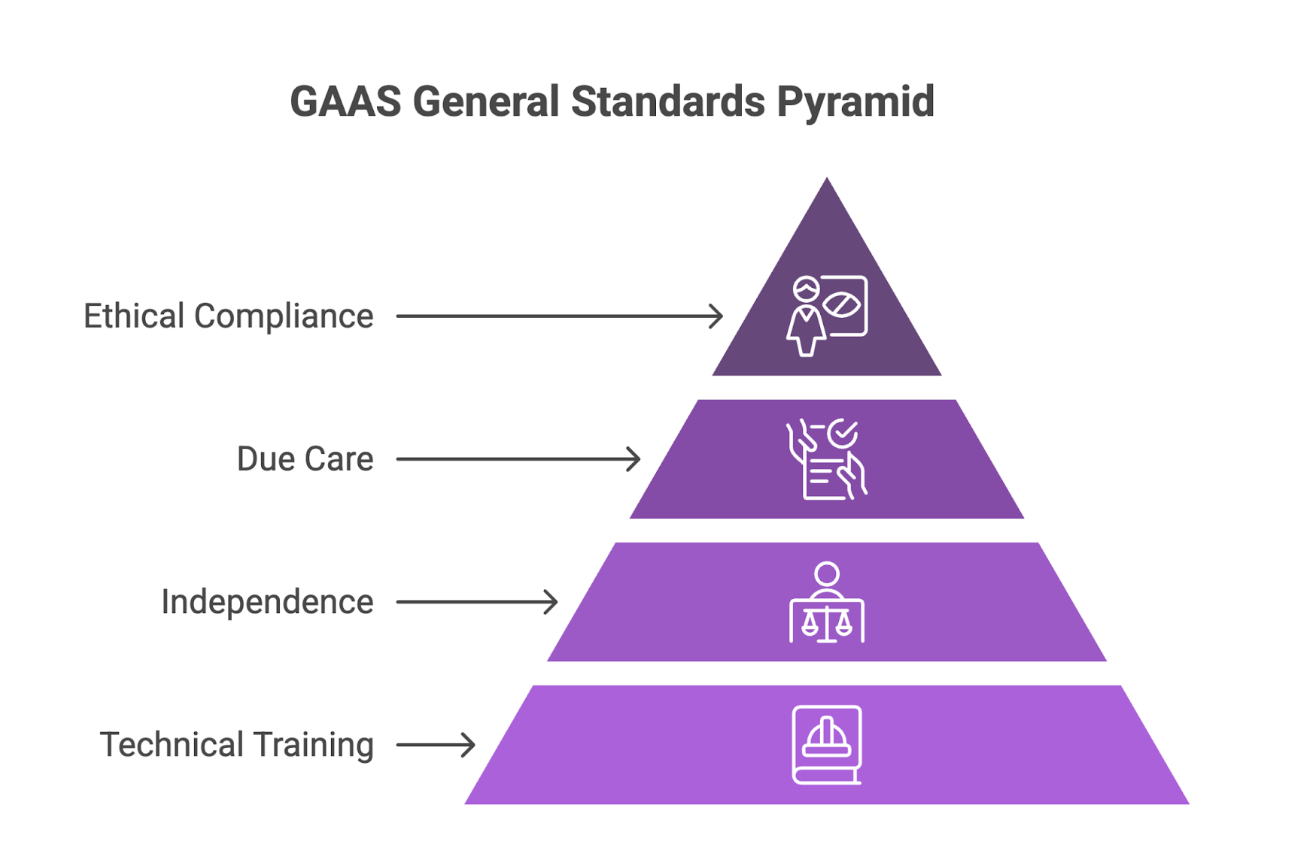

The General Standards under GAAS are the foundation of every quality audit. They focus entirely on the auditor, their qualifications, mindset, and the professional rigor they bring to the job.

Here's the big idea: Even before you test controls, document procedures, or issue an opinion, the credibility of your work hinges on you, the auditor.

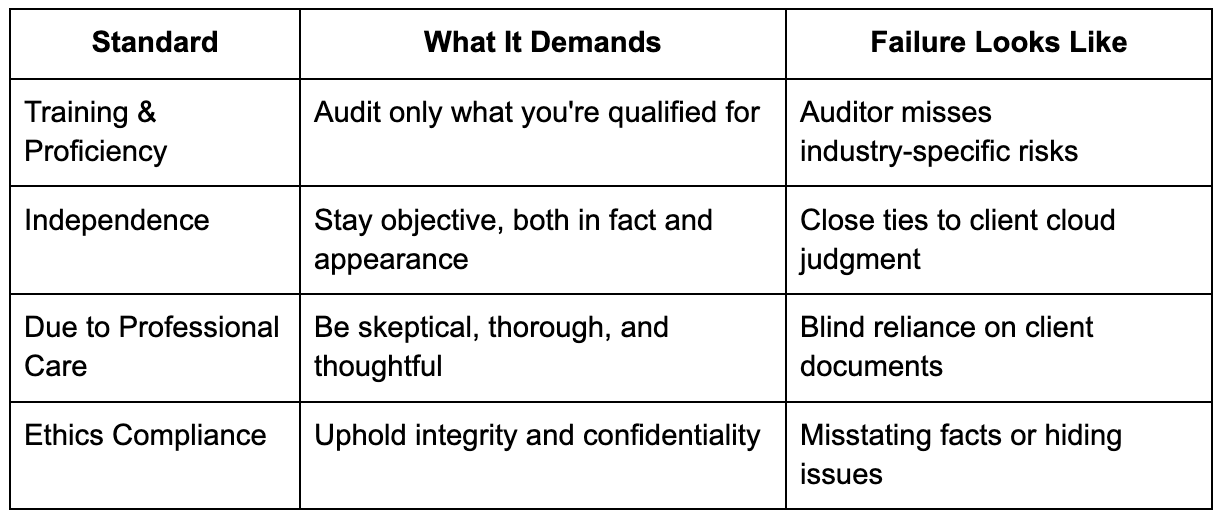

These standards are codified in AU Section 150, and while most lists summarize them in three, the clarified standards break them down into four key responsibilities under the AICPA's audit clarity project. These complement other professional standards like statements on auditing standards and quality control standards:

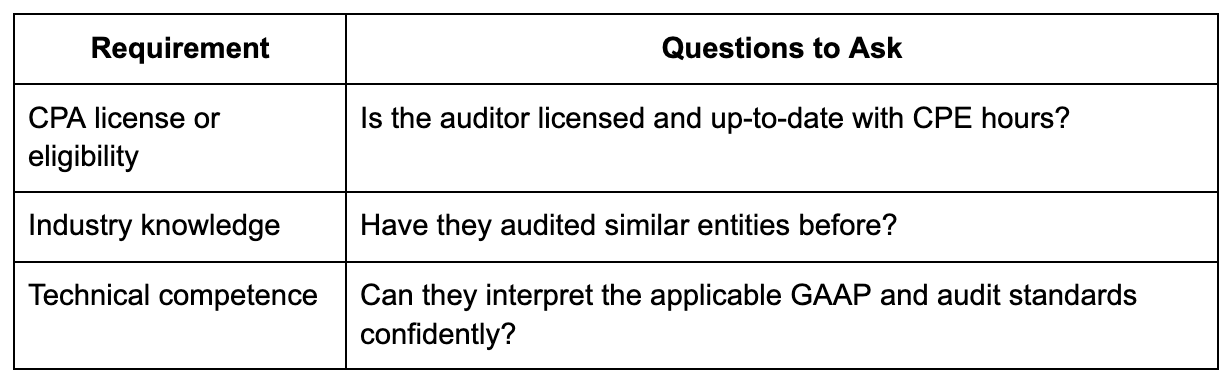

Definition: The audit must be performed by a person or persons having adequate technical training and proficiency as an auditor.

What it means in practice: Auditing isn't just about knowing accounting principles, it's about interpreting them in messy, real-world scenarios. This standard ensures that the auditor:

Real example: An auditor reviewing a construction firm's percentage-of-completion revenue must know how to test WIP schedules, evaluate contract modifications, and assess revenue recognition under ASC 606. That requires industry-specific training, not just general knowledge.

Checklist for compliance:

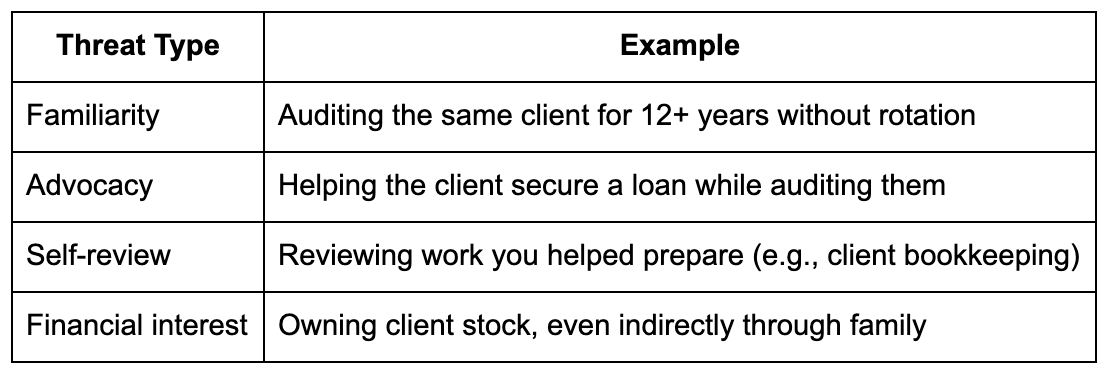

Definition: In all matters relating to the assignment, independence in mental attitude is to be maintained by the auditor or auditors.

What it means in practice: Independence isn't just about not owning stock in a client, it's about having the mental objectivity to challenge management's assertions, even when the pressure's on.

Auditors must be:

Common independence threats:

Best practices:

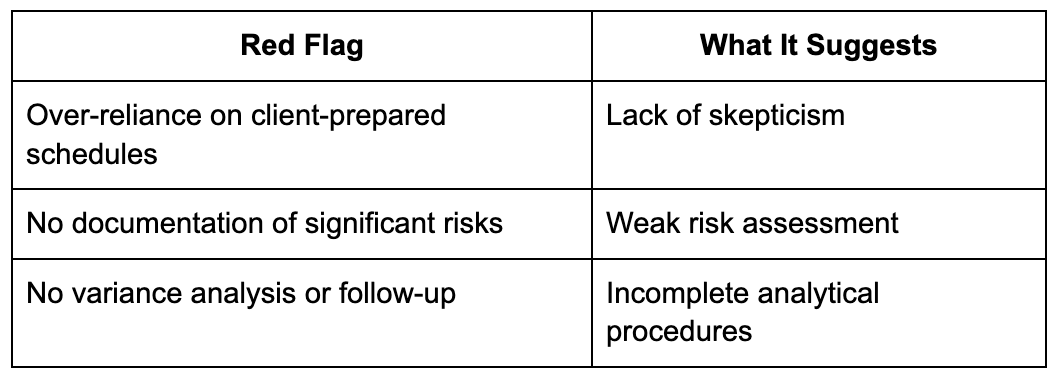

Definition: Due professional care is to be exercised in the performance of the audit and the preparation of the report.

What it means in practice: This is about how the work is done, the mindset, skepticism, and attention to detail. It's not enough to "follow the steps"; you need to apply professional judgment every step of the way.

Due care includes:

Example: If AR balances don't reconcile, due care means investigating and escalating, not just noting it and moving on because "it was close enough."

Key indicators of failure:

4. Compliance with Ethical Requirements

Definition: The auditor must comply with relevant ethical requirements, including integrity, objectivity, professional competence, confidentiality, and professional behavior.

Why this was added: In the clarified GAAS structure, this standard was added to reinforce that beyond technical rules, ethical conduct is non-negotiable.

Practical expectations:

Example: If a firm receives pressure to issue a clean report before year-end bonuses, ethical standards demand resisting, even if the client threatens to leave.

These four standards aren't optional, they're what regulators, peer reviewers, and litigation attorneys look for when something goes wrong.

Quick Summary Table:

Understanding the Broader Standards Framework

For auditors working with government entities, understanding the relationship between GAAS and government auditing standards is crucial. The yellow book, published by the Government Accountability Office, builds upon GAAS with additional requirements. These yellow book standards include 10 standards organized into three categories that mirror GAAS but with enhanced requirements for government audits.

When auditors perform attestation engagements for government entities, they must comply with both GAAS and the applicable yellow book standards. This dual compliance ensures that government audits meet both professional and governmental oversight requirements.

The audit profession operates within an interconnected framework of standards:

The Auditing and Assurance Standards Board continues to update these standards, with many changes becoming effective for financial statements for periods beginning December 15 of specific years.

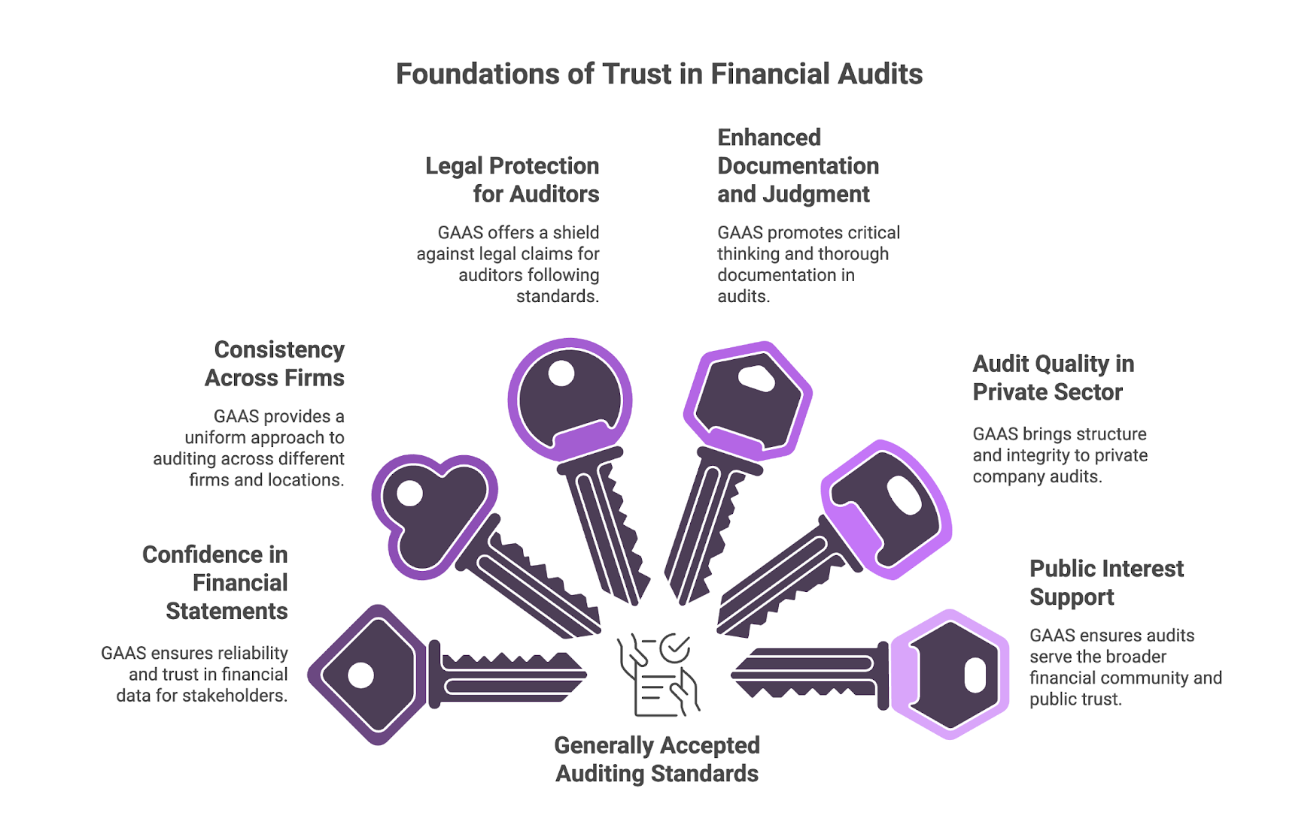

At its core, Generally Accepted Auditing Standards (GAAS) exist for one reason: to protect the credibility of the financial audit.

These standards are not just regulatory checkboxes, they form the foundation of professional trust between private companies, auditors, regulators, lenders, and investors. When followed with integrity, GAAS helps ensure that financial statements aren't just numbers on paper, they're reliable, reviewable, and decision-ready.

Let's unpack why GAAS is so critical in real-world audit environments:

Stakeholders rely on financial statements to make funding, hiring, acquisition, and growth decisions. When an auditor performs an audit under GAAS, it signals that:

Without these signals, banks won't lend, boards can't govern, and private equity firms won't move forward. GAAS makes financial data trustworthy, even when no one in the room knows the accountant personally.

GAAS acts like a national playbook. It ensures that an audit done in Kansas looks and feels like one done in California, even if the industries or firm sizes differ.

This standardization:

Inconsistent audits erode credibility. GAAS ensures that, even with professional judgment involved, there's a consistent floor for quality.

Audit firms, especially small to mid-size ones, face growing litigation risks. One misstep can trigger lawsuits or regulatory enforcement. GAAS provides a legal and procedural shield.

If an auditor:

…then they're typically protected from negligence claims. The standards become their defense, proving the audit wasn't careless, even if something went wrong later.

GAAS isn't just about ticking boxes. It requires the auditor to:

This raises the overall bar for audit thinking. In practice, it pushes teams to look beyond rote procedures and think critically, especially on high-risk or judgment-heavy accounts like revenue, goodwill, or related-party transactions.

Public company audits have PCAOB oversight. But GAAS governs the far larger world of private businesses, startups, and nonprofits, where financial reporting often lacks the same rigor.

GAAS helps bring:

This is especially valuable when private companies are preparing for their first institutional funding round or acquisition, and suddenly, their audit matters in a big way.

Though audits are paid for by clients, GAAS helps ensure that the work ultimately serves the broader financial ecosystem. Lenders, regulators, and even the IRS rely on audited statements to function. Without GAAS:

In that sense, GAAS helps the profession earn its social license to operate and provides a framework that CPAs can attest to when certifying financial statements.

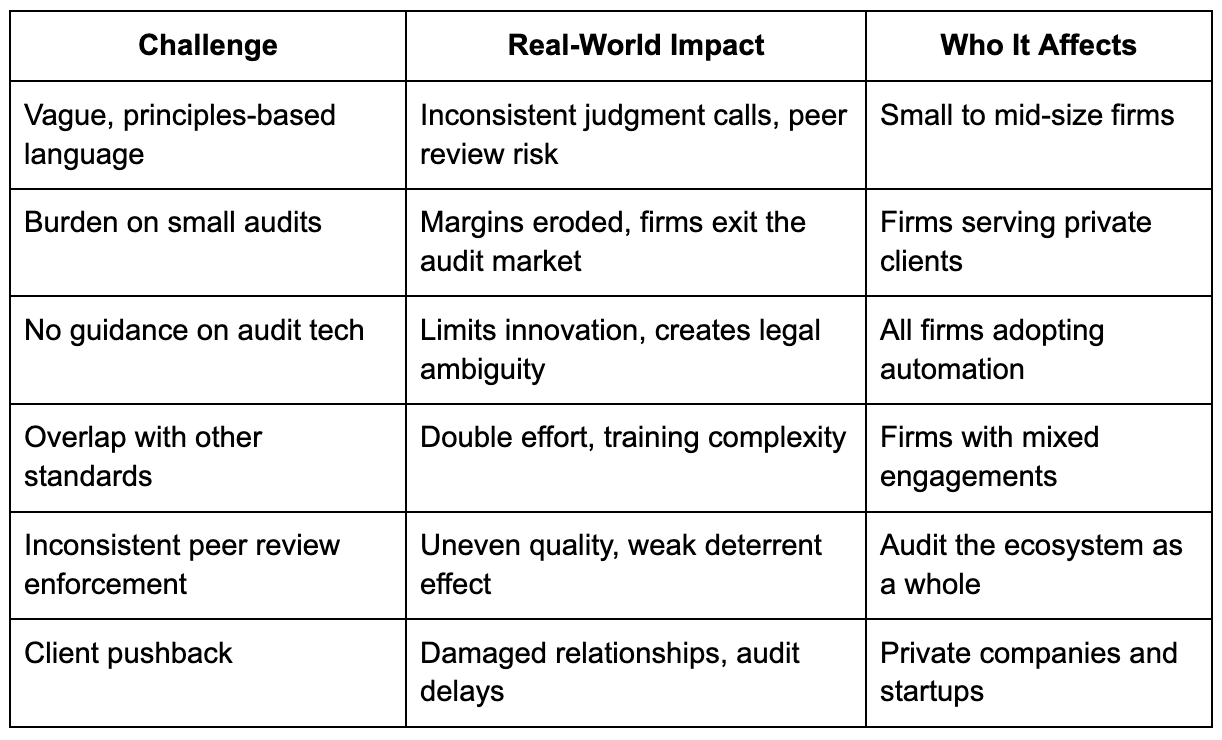

While GAAS provides a necessary structure for private company audits, it's often viewed as outdated, overgeneralized, or burdensome in the context of today's dynamic audit environment. Below, we break down six key friction points, with practical examples and a table summarizing real-world impact.

GAAS is intentionally broad, which gives auditors room to apply professional judgment. But in practice, that "flexibility" often turns into second-guessing.

Example: A small firm auditing a startup may struggle to define what "sufficient appropriate evidence" looks like for an intangible asset with no market comparables. Larger firms have templates and legal backing. Smaller firms? They're left with book standards and crossed fingers.

Why it matters:

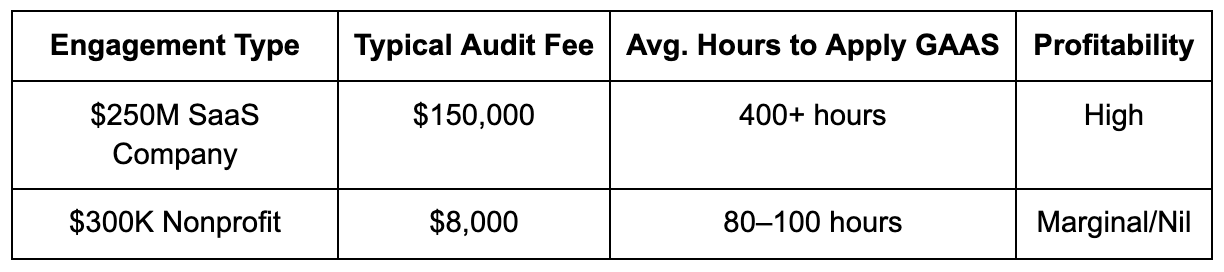

A single-owner LLC earning $300K in annual revenue might need a full GAAS-compliant audit due to lender or regulatory requests. But applying every standard, from internal control walkthroughs to full documentation, takes dozens of hours.

Result: Firms either raise prices (and lose the client) or cut corners (and risk peer review consequences).

GAAS hasn't kept pace with the modern audit stack. Cloud-based GLs, AI sampling tools, and continuous risk monitors are here, but GAAS doesn't say much about them.

Common auditor questions today:

Without guidance, teams fall back on legacy methods, slowing innovation and draining margin.

GAAS is the AICPA's standard. But depending on the client, firms may also have to cross-reference:

This creates:

For example, a firm auditing a nonprofit with federal grants must toggle between GAAS and the yellow book, a recipe for inconsistency unless well-managed. The yellow book report requirements often exceed standard GAAS reporting requirements.

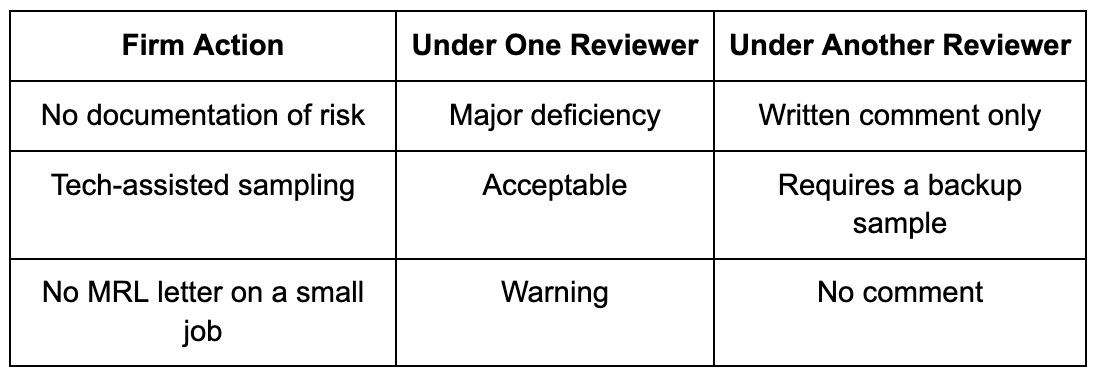

The profession relies heavily on peer review to enforce compliance. But interpretations vary by reviewer, and consequences for non-compliance can be mild or delayed.

This inconsistency weakens the overall integrity of GAAS, and disincentivizes full compliance for low-risk engagements.

GAAS expects auditors to document, test, and challenge assumptions, but clients often view this as "overkill," especially when they're cash-constrained or under pressure.

Examples of tension:

This misalignment can cause delays, scope disputes, and even client churn, particularly in fast-moving sectors like tech or retail where audits feel intrusive rather than value-add.

Whether you're an auditor navigating new tech or a founder trying to understand why your audit takes so long, GAAS matters more than it seems.

These standards aren't just bureaucratic hurdles, they exist to ensure integrity, objectivity, and trust in financial reporting. But yes, they come with challenges: outdated language, slow adaptation to automation, and rising complexity for small firms.

The future of auditing will depend on how we modernize these standards without losing their core purpose. As government auditing standards continue to evolve in the yellow book and new statements on auditing standards are issued, the profession must balance innovation with the fundamental principles that make audits valuable.

If you're a firm dealing with complex audits, shifting client expectations, or just want to streamline your compliance process without cutting corners, it's worth having a strategic partner who understands GAAS from the ground up.

That's where Madras Accountancy can help. From audit prep to back-office support, our team is built to support U.S. firms with the rigor GAAS demands, and the flexibility today's clients expect.

Let's make audits smarter, not harder.

Question: What are Generally Accepted Auditing Standards (GAAS) and why are they important for auditors?

Answer: Generally Accepted Auditing Standards (GAAS) are the framework of professional standards that govern the conduct of financial statement audits in the United States, established by the Auditing Standards Board (ASB) of the American Institute of CPAs. GAAS are important because they ensure audit quality, consistency, and public trust by establishing minimum standards for auditor qualifications, audit performance, and reporting requirements. These standards protect public interests by requiring auditors to maintain independence, exercise professional skepticism, and obtain sufficient appropriate evidence to support audit opinions. GAAS compliance is mandatory for all CPA-conducted audits and provides legal protection for auditors while ensuring stakeholders receive reliable financial information for decision-making purposes.

Question: What are the ten generally accepted auditing standards and how are they categorized?

Answer: The ten generally accepted auditing standards are categorized into General Standards, Standards of Field Work, and Standards of Reporting. General Standards include adequate technical training and proficiency, independence in mental attitude, and due professional care. Standards of Field Work require adequate planning and supervision, sufficient understanding of internal control, and sufficient appropriate audit evidence. Standards of Reporting mandate adherence to GAAP, consistency identification, adequate disclosure assessment, and proper opinion expression. These standards provide comprehensive framework covering auditor qualifications, audit performance requirements, and reporting obligations. Each standard includes detailed implementation guidance through Statements on Auditing Standards (SAS) that provide specific procedures and requirements for various audit situations and circumstances.

Question: How do Statements on Auditing Standards (SAS) relate to GAAS?

Answer: Statements on Auditing Standards (SAS) are authoritative interpretations and applications of GAAS issued by the Auditing Standards Board to provide detailed guidance for specific audit situations and emerging issues. SAS documents clarify GAAS requirements, establish specific procedures, and address new auditing challenges while maintaining consistency with fundamental GAAS principles. Recent significant SAS include AS 3101 (risk assessment), AS 3105 (fraud consideration), and AS 3110 (analytical procedures). SAS are binding on AICPA members conducting audits and provide practical implementation guidance for complex audit areas. Regular SAS updates ensure GAAS remain current with business environment changes, technological advances, and emerging risks while maintaining high audit quality standards and public protection.

Question: What are the key changes and updates to GAAS that auditors should know for 2025?

Answer: Key GAAS updates for 2025 include enhanced cybersecurity risk assessment requirements, expanded going concern evaluation procedures, clarified related party transaction auditing, and updated internal control assessment guidance. Recent changes emphasize technology impacts on audit procedures, data analytics integration, and remote auditing considerations following COVID-19 adaptations. Environmental, social, and governance (ESG) reporting considerations are increasingly integrated into audit standards. Additional updates cover cryptocurrency and digital asset auditing, cloud computing controls evaluation, and enhanced professional skepticism requirements. Auditors must stay current with continuing education requirements, technology proficiency expectations, and evolving risk assessment procedures. Professional development and training ensure compliance with updated standards while maintaining audit effectiveness in changing business environments.

Question: How do GAAS requirements for independence affect auditor-client relationships?

Answer: GAAS independence requirements strictly prohibit financial, business, and family relationships that could impair auditor objectivity or create conflicts of interest in auditor-client relationships. Independence rules cover direct and indirect financial interests, business relationships, family connections, and non-audit service provisions that could compromise audit objectivity. Auditors must evaluate independence annually, document independence assessments, and establish safeguards for potential independence threats. Recent updates strengthen independence requirements for technology services, data analytics, and advisory services provided to audit clients. Violations of independence requirements can result in disqualification from audit engagements, professional sanctions, and legal liability. Professional independence evaluation and documentation procedures ensure compliance while maintaining audit credibility and public trust.

Question: What documentation and working paper requirements exist under GAAS?

Answer: GAAS documentation requirements mandate that auditors prepare and maintain audit working papers that provide sufficient detail to enable experienced auditors to understand audit procedures performed, evidence obtained, and conclusions reached. Working papers must document audit planning, risk assessments, internal control evaluations, substantive testing, and audit conclusions. Documentation requirements include engagement letters, independence confirmations, management representations, and audit committee communications. Retention periods typically require seven years for audit documentation with specific requirements for public company audits. Electronic working papers must maintain security, integrity, and accessibility throughout retention periods. Professional documentation standards ensure audit quality, support audit opinions, and provide evidence of GAAS compliance during peer reviews and regulatory inspections.

Question: How do GAAS address fraud detection and reporting responsibilities?

Answer: GAAS establish specific auditor responsibilities for fraud risk assessment, detection procedures, and reporting requirements while recognizing that audits cannot guarantee fraud discovery. Auditors must assess fraud risks, design appropriate responses, maintain professional skepticism, and evaluate fraud indicators throughout audit engagements. Required procedures include management inquiry, analytical procedures, journal entry testing, and revenue recognition evaluation. When fraud is identified, auditors must evaluate impacts on audit opinions, communicate with appropriate governance levels, and consider reporting obligations to regulators or law enforcement. Professional skepticism requirements emphasize questioning contradictory evidence and challenging management representations. However, auditors are not responsible for fraud prevention or detection of immaterial fraud that doesn't affect financial statement reliability.

Question: What are the current challenges and future developments affecting GAAS implementation?

Answer: Current GAAS implementation challenges include technology integration requirements, cybersecurity risk assessment complexity, remote auditing procedures, and evolving business model auditing. Emerging technologies like artificial intelligence, blockchain, and data analytics require new audit approaches and professional competency development. International harmonization efforts seek consistency between US GAAS and International Standards on Auditing while maintaining US-specific requirements. Future developments may include enhanced ESG reporting standards, cryptocurrency auditing guidance, and automated audit procedure standards. Professional education and training requirements continue evolving to ensure auditor competency with technological advances and emerging risks. Standard setters regularly evaluate GAAS effectiveness and relevance while balancing audit quality, cost considerations, and public interest protection in dynamic business environments.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.