.png)

Private equity has exploded into a $4.5 trillion global industry, but behind every successful fund lies sophisticated accounting that most people never see. Unlike trading stocks where prices are obvious, private equity accounting involves complex valuations, intricate fund structures, and specialized reporting that can make or break investment decisions. Whether you're an accounting professional entering this space or an investor trying to understand fund reports, this guide breaks down everything you need to know.

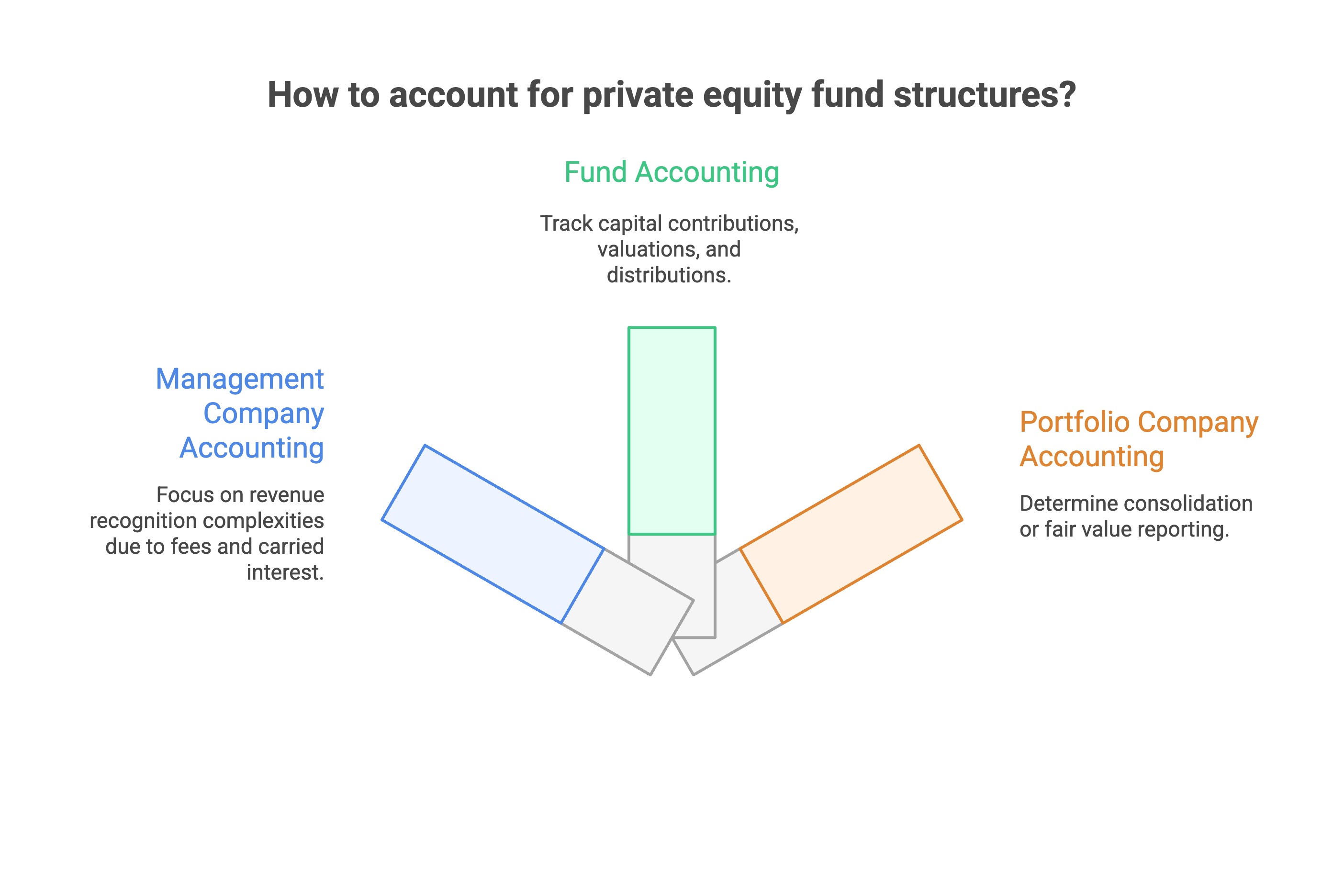

Private equity funds operate through complex structures that create unique accounting challenges. The most common setup is a limited partnership where general partners (GPs) manage the fund while limited partners (LPs) provide the money. This seemingly simple arrangement actually creates multiple accounting entities that must be tracked separately.

Management Company: This entity collects management fees (typically 2% of committed capital annually) and eventually receives carried interest (usually 20% of profits above a hurdle rate). From an accounting perspective, revenue recognition becomes complex because of clawback provisions and performance contingencies.

The Fund Itself: Must track capital contributions from investors, investment acquisitions, ongoing valuations, and eventual distributions back to partners. The complexity multiplies with "waterfall" distribution models that prioritize returns based on predefined thresholds.

Portfolio Companies: When a fund controls a company (typically >50% ownership), consolidation questions arise. However, most funds use the "investment company exception" under ASC 946, allowing them to report investments at fair value rather than consolidating balance sheets.

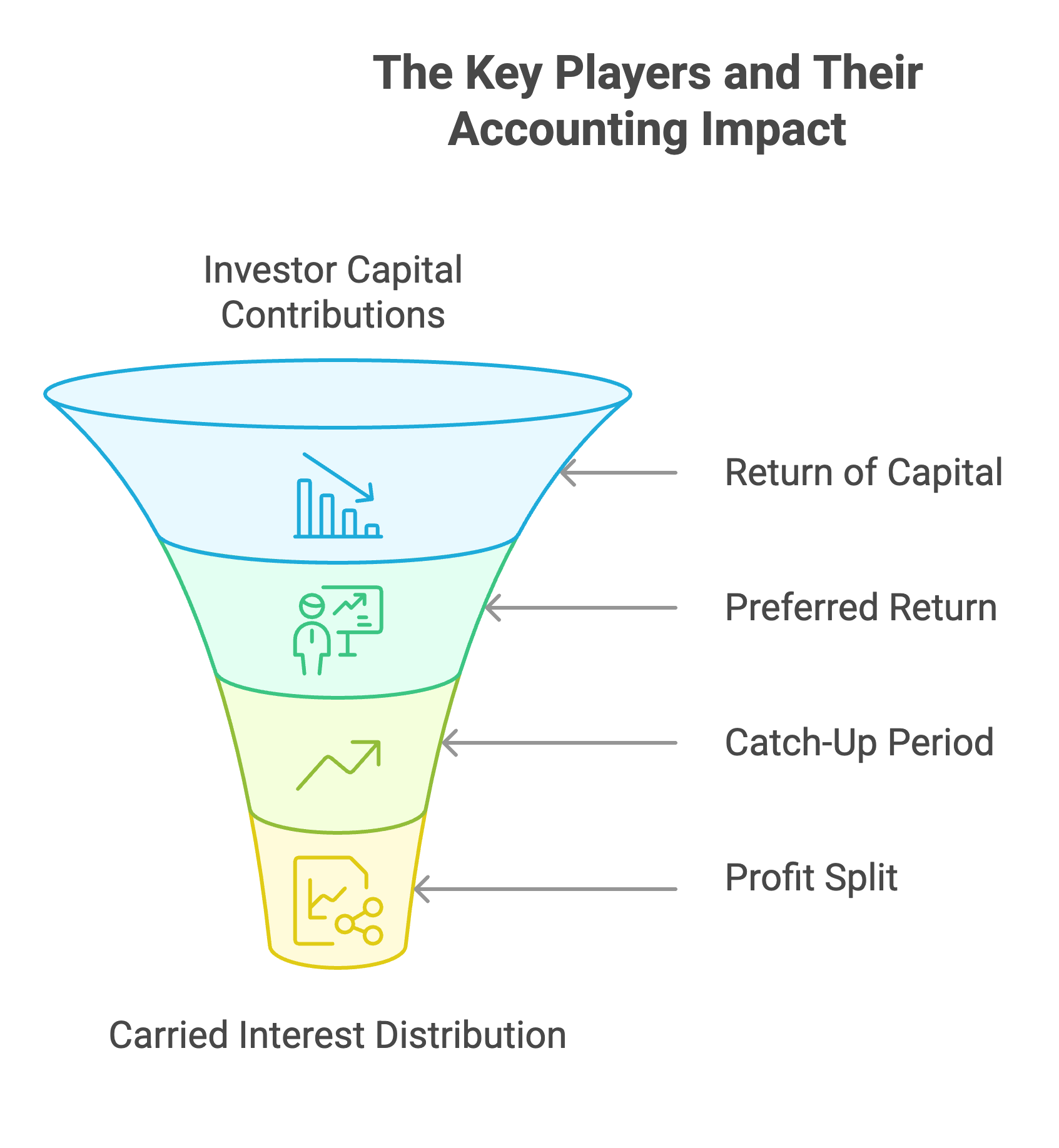

Consider a typical waterfall arrangement:

Each stage requires different accounting treatment and affects when revenue can be recognized. This isn't just academic, getting it wrong can lead to incorrect performance reporting and regulatory issues.

While public stocks have market prices, private companies require judgment-based valuations that directly impact everything from performance reporting to carried interest calculations. The stakes are high: a 10% valuation error on a $100 million investment means $10 million in reported value difference.

This method looks at similar companies to determine value. Here's how it works in practice:

Step 1: Identify comparable public companies based on industry, size, and growth profile.

Step 2: Apply relevant multiples (EV/EBITDA, EV/Revenue, P/E ratios) to your portfolio company's metrics.

Step 3: Adjust for differences. Private companies typically trade at 15-30% discounts to public peers due to liquidity constraints.

Example: A mid-market software company might be valued at 5-7x EBITDA compared to public peers trading at 8-10x EBITDA after applying appropriate discounts.

This method projects future cash flows and discounts them to present value. Key considerations include:

Discount Rates: Typically 12-25% for private equity portfolio companies, reflecting higher risk profiles than public markets.

Terminal Values: Often represent 60-80% of total enterprise value, making assumptions critical.

Projection Periods: Usually 5-10 years, requiring detailed business plan analysis.

When portfolio companies raise money, those valuations provide observable data points. However, complexities arise:

Robust valuation policies are crucial for auditor acceptance and regulatory compliance. Leading firms establish valuation committees with independent members to enhance objectivity and maintain detailed assumption documentation.

Private equity accounting operates under multiple frameworks that continue evolving. Understanding these standards is crucial for accurate reporting and regulatory compliance.

ASC 946 (US GAAP): Provides specialized guidance for investment companies, permitting fair value accounting for investments regardless of ownership percentage. This significantly simplifies reporting compared to consolidation requirements.

IFRS 10: Offers similar investment entity exceptions but with important differences. For instance, IFRS requires investment entities to consolidate service subsidiaries rather than measuring them at fair value.

Fair Value Hierarchy Disclosures: Both ASC 820 and IFRS 13 mandate extensive disclosures. Most private equity investments fall into Level 3 (unobservable inputs), requiring:

SEC Requirements: Firms managing over $150 million must register as investment advisers and file Form PF, reporting detailed fund operations, leverage, and portfolio company information.

International Compliance: The EU's AIFMD imposes similar requirements for European managers or those marketing to EU investors.

ERISA Considerations: Funds with U.S. pension plan investors face additional fiduciary responsibilities and prohibited transaction rules.

The 2017 Tax Cuts and Jobs Act introduced significant changes:

Carried interest accounting represents one of the most complex areas in private equity, requiring careful consideration of recognition timing and clawback risks.

Under current revenue recognition standards (ASC 606/IFRS 15), carried interest can only be recognized when it's "highly probable" that significant revenue reversal won't occur. This constraint acknowledges clawback risk—the possibility that general partners might need to return previously distributed carried interest if subsequent losses reduce overall fund performance.

Conservative Approach: Most firms recognize carried interest only after clawback risk is substantially eliminated, typically when:

Carried interest calculations involve sophisticated models reflecting partnership agreement terms:

Traditional Waterfall:

Deal-by-Deal Waterfalls: Calculate carried interest on individual investments rather than total fund performance, requiring careful tracking of loss carryforwards and cross-collateralization provisions.

While seemingly straightforward, management fees present unique challenges:

Calculation Basis: Typically percentage of committed capital during investment period (years 1-5), then invested capital thereafter.

Fee Offsets: Transaction fees from portfolio companies often reduce management fees, requiring proper allocation across limited partners.

Fee Waivers: When general partners waive fees for additional carried interest, these arrangements require specialized accounting and tax treatment.

When private equity funds acquire companies, multiple standards apply:

Purchase Price Allocation (PPA): Required under ASC 805/IFRS 3, involving distribution of acquisition cost across identifiable assets and liabilities at fair value.

Intangible Asset Identification: Specialized valuation work identifies customer relationships, technologies, trade names, and non-compete agreements.

Push-Down Accounting: Often implemented to align subsidiary reporting with transaction economics, creating fresh starting points with revalued assets and liabilities.

Leveraged buyouts involve multiple debt tranches requiring careful analysis:

IPO Transitions: Require moving from private to public company standards, potential consolidation changes, and share-based compensation modifications.

Strategic Sales: Involve gain/loss calculations, earnout accounting, and continuing involvement analysis.

Secondary Buyouts: Create similar complexities with potential rollover equity requiring fair value analysis.

Asset vs. Stock Sales: Create different tax consequences and deferred tax accounting requirements.

International Exits: Introduce withholding taxes, foreign currency considerations, and treaty analysis.

Timing Considerations: Multi-stage exits require careful analysis of when control is lost and how remaining interests should be measured.

Modern private equity firms implement specialized platforms:

ESG Integration: Environmental, Social, and Governance considerations increasingly impact valuations and require new metrics.

AI and Analytics: Advanced modeling techniques and broader data incorporation promise enhanced valuation accuracy.

Regulatory Evolution: Continued SEC focus on private markets and international standard harmonization.

Private equity accounting requires specialized expertise that extends beyond traditional accounting knowledge. The intersection of accounting, finance, tax, and legal considerations creates a uniquely complex environment requiring interdisciplinary understanding.

At Madras Accountancy, we specialize in sophisticated financial structures and complex accounting challenges. Our experience with private equity and investment fund accounting enables us to support:

Ready to navigate private equity accounting complexities? Contact us today to discuss how our specialized expertise can support your fund operations, ensure compliance, and optimize your accounting processes for this demanding industry.

Private equity accounting represents one of the most sophisticated areas in financial reporting, combining complex valuations, intricate fund structures, and evolving regulatory requirements. Success requires not only technical accounting expertise but also deep understanding of investment strategies, tax considerations, and operational realities.

The industry's continued growth—with global assets under management exceeding $4.5 trillion—underscores the importance of sophisticated accounting practices. As regulatory scrutiny increases and investor demands for transparency grow, private equity firms that invest in robust accounting infrastructure gain significant competitive advantages.

Whether you're an accounting professional developing expertise in this area, a fund manager optimizing operations, or an investor seeking to understand complex structures, mastering private equity accounting principles provides valuable insights into one of finance's most dynamic sectors.

The future will likely bring additional complexity through ESG integration, enhanced regulatory requirements, and technological advancement. However, the fundamental principles—accurate valuation, transparent reporting, and stakeholder alignment—will remain constant, making solid accounting foundations essential for long-term success in private equity.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.