No one enjoys the idea of a tax audit, and if you're reading this, you're probably asking a very specific question:

How far back can the IRS go if they decide to audit your return?

The short answer: usually three years. But like most things with the IRS, the real answer is, "It depends on the specific circumstances and the years from the date of filing."

Whether you're self-employed, run a business, or just want peace of mind about a past return, it's important to understand what the Internal Revenue Service can (and can't) do when it comes to audit timelines. In most cases, audits are limited to the last three tax years, but under certain conditions, the IRS can look back six years, or even audit without any time limit.

In this guide, we'll break down exactly how far back you can be audited, what triggers longer lookback periods, and how to protect yourself if the IRS ever comes knocking.

For most taxpayers, the IRS has three years after you file your tax return to initiate an audit, which is crucial to remember when considering your place of business and financial records. This is known as the standard audit statute of limitations, and it applies to both individuals and businesses that file timely, accurate returns.

The IRS sets this window to balance enforcement with fairness. It gives the agency enough time to flag issues without keeping taxpayers in limbo forever. If you file your 2022 return by the April 15, 2023 deadline, the audit clock generally runs until April 15, 2026.

This 3-year limit applies in most routine cases, including:

According to the IRS: "We usually don't go back more than the past three years unless a substantial error is identified."

The audit period starts from the later of:

So even if you file early, say in February, the IRS still counts from the April deadline , not the early filing date.

Practical Tip:

Keep your tax records, receipts, and documentation for at least three years; that's the minimum period the IRS can ask questions. This three-year audit timeline is the standard expectation when you file your tax return.

However, not all audits follow this timeline. In some cases, the IRS can look back as far as six years, or even add additional years to the investigation. That's what we'll cover next.

Most people think the IRS is only allowed to audit your taxes for three years, and in most cases, that's true. But under certain conditions, the IRS has six years to audit your return and can extend beyond the standard timeline.

So what triggers a 6-year audit?

The IRS can go back six years to audit if it discovers that you've underreported more than 25% of your gross income on a tax return. This isn't just a rule buried in the fine print; it's a well-established threshold under 26 U.S. Code § 6501(e)(1)(A), extending the tax assessment period significantly.

Here's how that plays out in real life:

Real-world triggers that can push you into 6-year territory:

The IRS doesn't need to prove intent here. Just crossing the 25% income omission threshold gives them the legal authority to audit that return up to six years back.

Because many taxpayers only keep records for three years, assuming that's all the IRS will look at. But if you've ever:

...you could be leaving yourself open to scrutiny years later.

And the thing is, the IRS doesn't always tell you they're invoking the 6-year rule right away. It's often discovered during the course of a regular audit, when discrepancies start surfacing in items on your tax return.

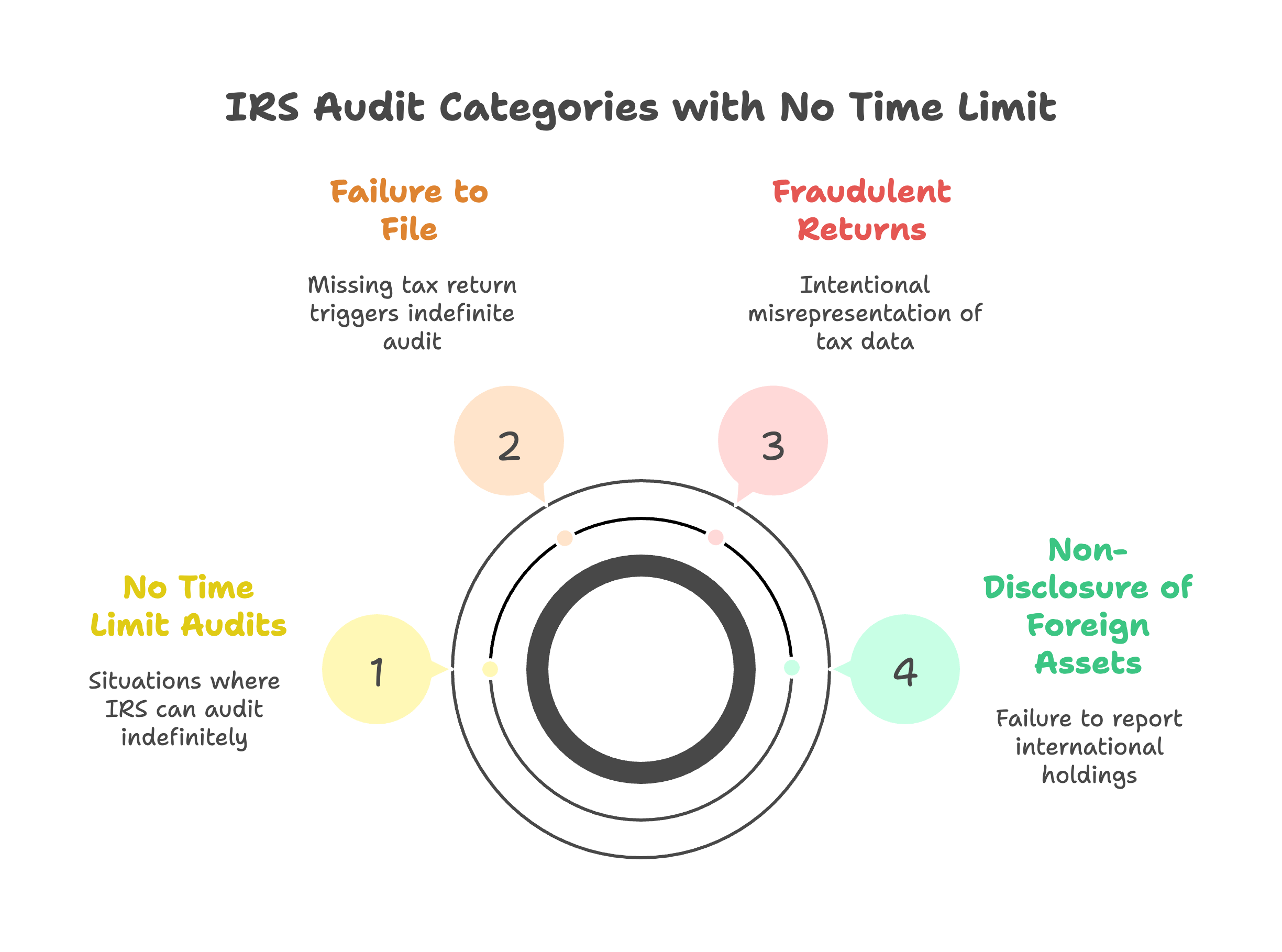

Yes, you read that right. In some cases, the IRS has no statute of limitations and can audit your tax return forever, no 3-year limit, no 6-year window. Just an open-ended statute with no expiration date.

So, how far back can you be audited with no limit?

If you fall into one of these three categories, the IRS can legally audit you at any time:

No return filed? No deadline for an audit. The IRS clock only starts ticking after a return is filed. If you skipped a year, intentionally or not, the IRS can go back and audit that year even decades later.

Example: A freelancer who earned income in 2015 but never filed for that year. Even in 2025, the IRS can still audit and assess taxes, penalties, and interest for 2015.

Fraud wipes out the IRS audit statute of limitations. If the IRS has evidence that a return was intentionally misleading, through fake deductions, made-up numbers, or deliberate omissions, they can open an audit at any point in the future.

And this isn't just for criminal tax fraud. Even civil fraud (which doesn't lead to jail but carries massive penalties) removes the time cap. In serious cases, the IRS criminal investigation division may become involved.

Thanks to the Foreign Account Tax Compliance Act (FATCA), the IRS is serious about offshore accounts. If you didn't file Form 8938 or FBAR (Report of Foreign Bank and Financial Accounts), and you had more than the disclosure threshold abroad, the IRS can audit those years with no time limit.

This is especially important for:

Tip: Foreign income and asset reporting errors don't just extend the audit window, they can also come with huge penalties.

Many taxpayers assume that if they haven't heard from the IRS within the last two years, they're safe. But if your return was never filed, was fraudulent, or missed required foreign disclosures, the IRS isn't bound by time.

And they do act on old returns, especially if triggered by whistleblowers, partner audits, or improved data-matching systems. Understanding tax law and these exceptions to the audit statute helps you avoid becoming a target.

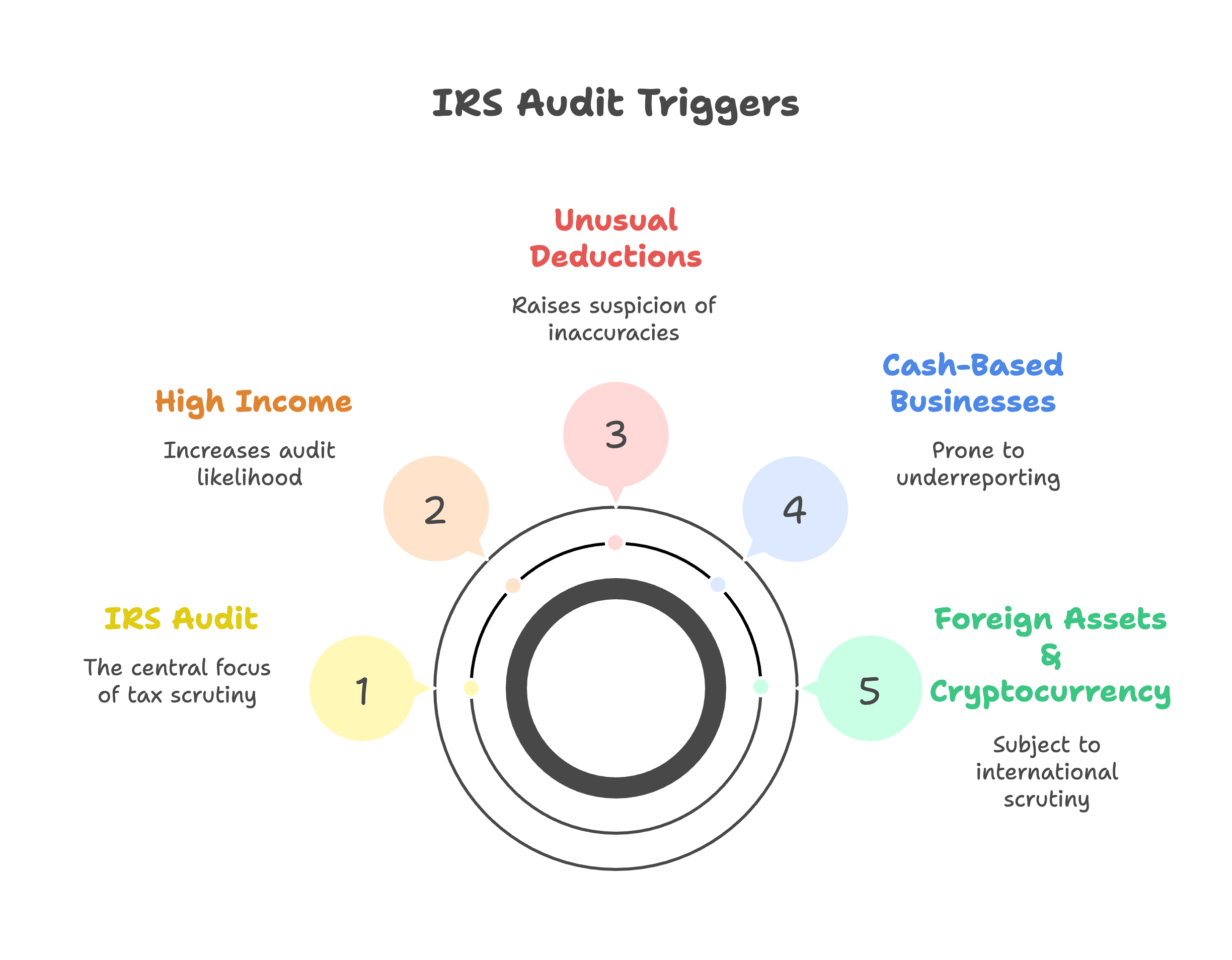

Contrary to popular belief, IRS tax audit selections aren't always about catching wrongdoing. Sometimes, it's just the result of a statistical flag. But understanding what acts as a trigger for an audit can help you avoid unnecessary scrutiny.

Here's a breakdown of the most common IRS audit triggers, including the less obvious ones.

The higher your income, the more likely to be audited you become. Taxpayers making over $500,000/year face significantly higher audit rates than average earners.

But it's not just income alone, the IRS cross-checks your reported income against:

If what you report doesn't match third-party data, your return gets flagged. The IRS data matching systems are increasingly sophisticated.

Claiming large deductions or credits that are uncommon for your income bracket, like massive charitable donations, home office deductions, or research credits, can prompt the IRS to investigate further.

Example: You make $60K but claim $25K in charitable deductions, expect a letter.

If you're self-employed or operate a business with a lot of cash transactions (restaurants, salons, laundromats, etc.), the IRS pays closer attention. Why? Because cash is easy to underreport.

A mismatch between declared income and lifestyle expenses (like luxury car leases or multiple mortgages) can also trigger audits. The IRS tries to audit tax returns as soon as they identify potential discrepancies.

If your tax return is full of perfect round numbers, like $1,000 for marketing or $10,000 for travel, it signals that you may be estimating instead of keeping actual records. That's a red flag.

The IRS sees too many "guesstimates" as sloppy bookkeeping, or worse, fabrication.

Didn't report your Coinbase account or offshore holdings? The IRS can include these in their audit scope and is now aggressively using data-matching tools and international treaties to flag:

If you're hiring offshore accountants for your CPA firm, this is especially relevant, make sure they understand U.S. foreign income rules.

Filing a late amendment or claiming a large refund? You're asking the IRS to take a second look. This doesn't always trigger an audit, but it significantly increases the chances.

Understanding what can cause you to avoid an audit helps you make better decisions when preparing your returns.

Understanding the IRS audit process top-to-bottom helps you prepare strategically, not reactively. Here's a full breakdown, complete with documented timelines, communication methods, and audit types:

Expect a formal audit notice delivered by mail, this letter outlines:

Always respond in writing or mail; the IRS never initiates audits by phone or email.

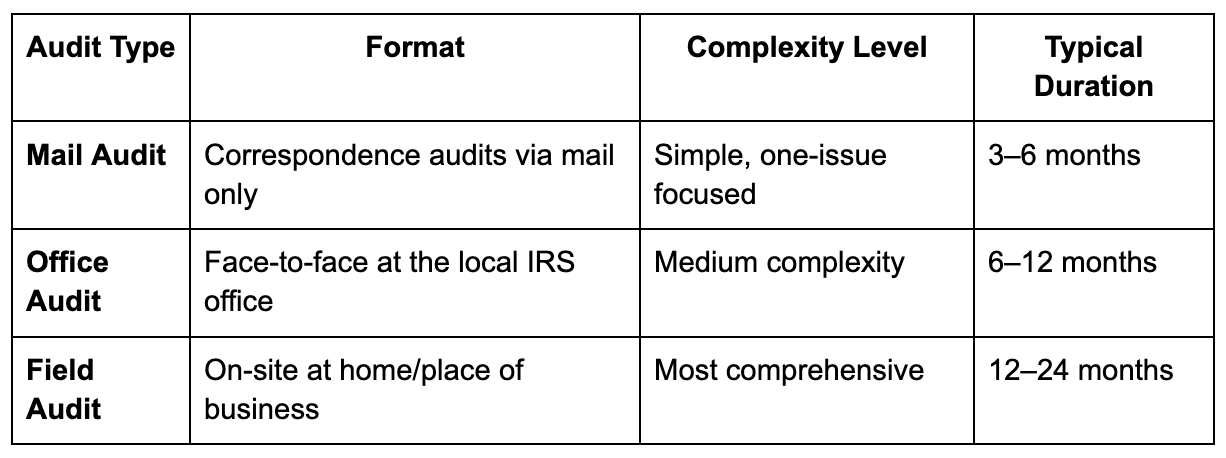

2. Audit Types: What You're Facing

About 75% of audits are mail-based (audit by mail), with the remainder split between office and field audits.

Your notice will specify exactly what's needed, common requests include:

Organize responses clearly, label files by issue and line item for easier review.

Mail audits: You typically have 30 days to respond; resolution can take another 30 days. With one issue, the entire process often wraps in under six months.

Office audits: Usually scheduled within a year of filing; meetings last a few hours, but combined back-and-forth can stretch the case to 6–12 months. You can request a face-to-face audit if you prefer personal interaction.

Field audits: In-depth and time-consuming; expect multiple site visits and exchanges, often resolving over a year or more.

Delays often stem from incomplete responses, complex issues, or appeals. The IRS time to complete the audit varies significantly based on complexity.

Once you provide documents:

You have 30 days to appeal after receiving a proposed audit report. If you disagree with the audit findings, you may pursue U.S. Tax Court or other venues. You can also request a conference with an IRS manager if the audit is not resolved satisfactorily.

The audit can end in one of three ways:

Regardless, you get a formal closing letter outlining next steps to conclude an audit.

🔧 Proactive Best Practices

When dealing with complex issues, seeking tax advice from a tax attorney or tax lawyer may be beneficial, especially if you need to meet the IRS in formal proceedings.

Audits are procedural and document-driven, not personal. They follow a rigorous sequence of mail notice, response, review, and resolution or appeal. With proactive organization and timely responses, most audits are completed within a year and resolved favorably.

If you're selected for an audit, remember that having professional representation can make a significant difference in the outcome.

If you're audited and lack receipts, the IRS may disallow your deductions, increasing your taxable income, and they may assess additional tax, penalties and interest. In some cases, bank statements, credit card records, invoices, or even calendar logs may serve as backup. Without any documentation, expect a reassessment, possibly owing more tax.

For most taxpayers, the IRS can audit returns filed within the last three years, based on the statute of limitations. Under certain conditions (missing over 25% of income), they can go back the last six years, and in cases of fraud or no return filed, there are no limitations for an audit. We discussed these situations earlier in the guide.

Using 2022 as an example, if you filed by April 15, 2023, the IRS can audit that return until April 15, 2026. Similarly, your 2021 return can be audited until April 15, 2025. These default 3-year periods apply unless you're in one of the extended-lookback scenarios.

If the IRS determines your return was fraudulent or intentionally deceptive, they may pursue civil penalties (up to 75% of the underpayment) or refer you for criminal charges, which could lead to fines or imprisonment. These cases are rare, but serious. Most audits result in agreed or no-change resolutions, rarely criminal action.

Audit rates vary significantly. Returns of high-income earners face greater scrutiny:

These red flags often prompt audits:

Audit length depends on complexity:

Efficient document turnaround and professional help shorten these timelines substantially. The time to complete the audit also depends on how quickly you respond to IRS requests.

IRS audits can feel intimidating, but understanding how far back they can go , and why , gives you a real edge. Whether it's the standard three years in an audit situation or rare cases stretching up to 6 years (or beyond), being prepared is your best defense.

The IRS may audit tax returns as soon as they identify discrepancies, so maintaining accurate records and understanding the audit process is crucial. If an IRS agent contacts you, having professional representation can make a significant difference.

If you're unsure whether your financial records can withstand scrutiny, or just want to stay ahead of potential red flags, it's smart to bring in professionals who've been there before.

At Madras Accountancy, we work with U.S. businesses and CPAs to handle tax filings, compliance, and bookkeeping with precision and care. From audit prep to full offshore accounting support, we're your behind-the-scenes financial ally.

👉 Talk to our team today to keep your taxes airtight, before the IRS ever asks.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.