.png)

If you've recently started freelancing, consulting, or side hustling, you've likely heard about 1099 taxes, and maybe panicked a bit when you realized no one is withholding taxes for you anymore.

That's one of the biggest shifts when moving from W-2 employment to working as an independent contractor: taxes are now your responsibility.

And it's not just about "saving a little extra." If you don't set aside enough for taxes on your 1099 income, you could face a massive, unexpected bill (plus penalties) come tax season, draining your hard-earned income and creating unnecessary stress.

So, much should I set aside for taxes on 1099 income?

The short answer: at least 25-30% of your net income, but your exact number depends on your income, state of residence, and tax deductions.

This guide will break it down clearly so you can:

Before you can confidently save for 1099 taxes, you need to understand exactly how income from self-employment is taxed and why it differs so much from the W-2 paychecks many are used to.

This is where many freelancers and new independent contractors stumble. They see payments hit their bank accounts and assume all of it is theirs to keep, only to get hit with a large, unexpected tax bill later. By understanding what taxes you're responsible for, you can plan ahead and protect your cash flow.

When you work for yourself or take on gigs outside of traditional employment, you're considered self-employed. Instead of receiving a W-2 that shows your wages and tax withholdings, you'll typically receive a 1099-NEC form at the end of the year from each client who paid you $600 or more.

This applies to many income streams, including:

Freelance work like writing, design, consulting, or coding.

Side hustles like tutoring, pet sitting, or photography.

Rideshare and delivery driving.

Working as an independent contractor with agencies or direct clients.

Work on platforms like Upwork, Fiverr, or Etsy (platform reporting can vary, but all income must still be reported).

It's important to note that even if you don't receive a 1099 form from a client, you are legally required to report and pay taxes on that income when you file their tax returns.

When you're a W-2 employee, your employer automatically withholds:

Federal income tax.

State income tax (if applicable).

Social Security and Medicare (FICA taxes), splitting the contribution with you.

With 1099 income, no one is withholding taxes for you. You receive the full payment, but it's up to you to set aside a portion for taxes each year. You're also responsible for paying both the employer and employee portions of Social Security and Medicare through what's called self-employment tax.

This shift can feel daunting at first, but it's manageable with a clear understanding and consistent planning.

Your tax requirements on 1099 income typically include:

Federal Income Tax: You pay based on your total taxable income, including your 1099 earnings and any W-2 wages or other income you have for the year. Rates range from 10% to 37%, depending on your tax bracket.

State Income Tax: This varies by state. Some states like Texas and Florida have no state income tax, while states like California and New York have higher rates. Don't overlook local taxes in some areas.

Self-Employment Tax: This is the tax that surprises many new freelancers. Self-employment tax covers Social Security and Medicare and is currently 15.3% of your net self-employment income, which includes:

One of the most important points to understand is that you don't pay taxes on the total amount you receive (gross income). You pay taxes on your net income after deducting qualified business expenses.

Net income is calculated as:

Gross 1099 income – deductible business expenses = net income.

Allowable tax deductions include business expenses such as:

Tracking these expenses accurately throughout the year helps reduce your taxable income and, in turn, your overall tax burden.

Understanding taxes as a 1099 contractor is the foundation for knowing how much to set aside for taxes. If you don't plan, you could find yourself owing a significant amount of taxes during tax season, along with potential penalties for underpayment.

Taking the time to understand your tax obligations helps you:

In the next section, we'll break down self-employment tax in detail so you can see how it directly impacts your income, your estimated tax calculations, and your plan for setting aside money as you earn throughout the year.

When you move from a regular W-2 paycheck to working for yourself, one of the biggest surprises is self-employment tax, and how much of your 1099 income it eats up if you don't plan for it.

Many new freelancers assume they only need to worry about regular income tax brackets. But self-employment tax (SE tax) is a separate hit, and it's often the reason people underestimate how much they need to set aside for taxes on 1099 income.

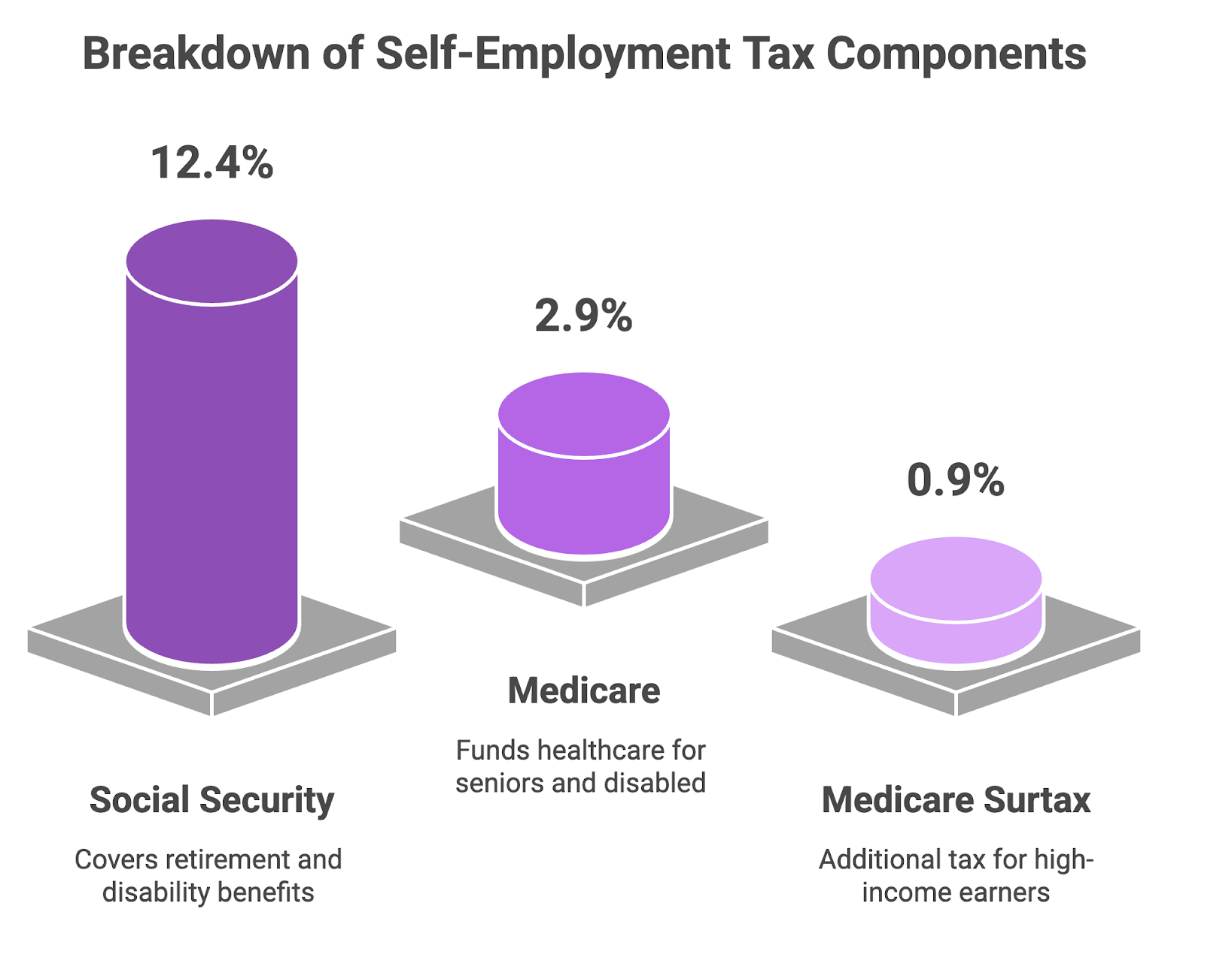

The self employment tax exists because, as an independent worker, you wear both hats: you're the "employer" and the "employee." For traditional W-2 workers, your employer covers half of social security tax and Medicare taxes automatically. But when you're self-employed, you cover both sides yourself.

This is why the self-employment tax rate is 15.3%, it's basically the full version of FICA taxes:

If your total income exceeds $200,000 (single) or $250,000 (married filing jointly), there's an extra 0.9% Medicare surtax on the amount above that threshold.

It's helpful to think of SE tax as its own separate obligation. Federal income tax is what you pay based on your total taxable income and your tax bracket. Self-employment tax is on top of that, it's a fixed percentage of your net self-employment income, not just any leftover profit after paying yourself.

Example: If your 1099 business brings in $80,000 in gross income and you have $15,000 in deductible expenses:

Self-employment tax is calculated using Schedule SE, which attaches to your personal Form 1040 when you file their taxes. Unlike W-2 taxes that are withheld from their paychecks every pay period, SE tax isn't automatically deducted, so you're expected to pay it yourself throughout the year.

This is why freelancers and contractors must make quarterly estimated tax payments. If you wait until the end of the year and underpay, you can get hit with penalties and interest.

There's a small break: you can deduct the "employer" half of your self-employment tax when calculating your taxable income. For example, if your SE tax is $9,945, you can deduct half of that ($4,972.50) as an adjustment to income on your Form 1040. This doesn't reduce your SE tax directly, but it does slightly lower your total taxable income for federal income tax.

This is why many tax pros recommend setting aside at least 25% to 30% of your net income for taxes on 1099 income. For high earners or people in states with higher income tax rates, setting aside 30% to 35% is safer.

The self-employment tax is a big chunk of that estimate. It's predictable , unlike income tax brackets, which vary with tax deductions and credits, SE tax is a flat rate on your net business income.

Let's say you're a freelancer earning $100,000 in gross 1099 income:

Without setting this money aside as you earn, you could face a huge shortfall come tax season.

Now that you understand how 1099 income is taxed and why self-employment tax can eat a chunk of your earnings, let's answer the big question:

How much should you actually set aside for taxes on your 1099 income?

The short, practical answer most tax professionals recommend:

Set aside 25% to 30% of your net income for federal taxes alone.

If you live in a state with income tax, consider 30% to 35% total to cover both federal and state obligations.

But let's unpack why, so you can adapt this to your specific situation.

When you earn 1099 income, you are responsible for:

Because self-employment tax is fixed, and your federal income tax will depend on your bracket, 25-35% is a safe starting range to avoid coming up short.

It's crucial to remember that you only pay taxes on your net self-employment income:

Gross 1099 income – deductible business expenses = net income.

For example, if you earn $60,000 in 1099 income and have $10,000 in business expenses:

While 25-35% is a good rule of thumb, your exact set-aside should consider:

Scenario 1: Full-Time Freelancer

Scenario 2: Side Hustler with W-2 Job

1. Open a Separate 1099 Bank Account Every time you get paid, transfer 25-35% of the payment into this account immediately.

2. Track Income and Expenses Weekly or Monthly Use a spreadsheet or bookkeeping software to update your numbers regularly.

3. Review Quarterly Check your year-to-date income and adjust your set-aside rate if you are earning more (or less) than expected.

4. Make Quarterly Estimated Tax Payments The IRS expects you to pay as you go. If you owe more than $1,000 in taxes for the year, you may need to make quarterly estimated tax payments to avoid penalties.

The biggest mistake freelancers and side hustlers make is spending everything they receive, assuming taxes will sort themselves out later. By consistently setting aside 25-35% of your net 1099 income, you:

In the next section, we'll cover Quarterly Estimated Taxes: Why They Matter and How to Calculate Them, so you can move from guessing to a clear, stress-free tax system throughout the year.

Once you understand how much to set aside for taxes on your 1099 income, the next step is actually sending those payments to the IRS before tax season arrives.

This is where estimated quarterly taxes come in.

Many freelancers and side hustlers are surprised to learn that the IRS expects you to pay estimated taxes throughout the year, not just in April. If you wait and pay everything at once, you could face underpayment penalties and interest charges, even if you pay the full amount by the filing deadline.

Unlike W-2 employees, where taxes are withheld from their paychecks automatically, 1099 workers receive their full payment with no taxes taken out.

To keep the system fair and cash flowing, the IRS requires self-employed individuals to pay taxes as they earn income using quarterly tax payments.

You generally need to pay quarterly taxes if:

Estimated quarterly tax payments are due four times a year:

If the due date falls on a weekend or holiday, it shifts to the next business day.

Step 1: Estimate Your Net Income: Project your gross 1099 income for the year and subtract expected deductible business expenses to determine your estimated net income.

Step 2: Calculate Your Estimated Tax Liability

Apply:

Step 3: Divide by Four: Take your total estimated annual tax liability and divide by four to find your quarterly payment amount.

Let's say:

Many independent contractors find it helpful to use a tax calculator specifically designed for self-employment income. A 1099 tax calculator can help you estimate your quarterly payments more accurately by factoring in your specific income, deductions, and tax bracket.

Many states also require estimated quarterly taxes, so check your state's tax website to ensure you're compliant locally.

Freelance and side hustle income often fluctuates. If you have a lower-income quarter, you can adjust your payments down. If you earn more than expected, you can increase your payment to avoid underpayment penalties later.

Tracking your income and expenses monthly or quarterly helps you adjust your estimated quarterly tax payments to reflect your real earnings, rather than guessing blindly.

As a 1099 independent contractor, there are several other tax considerations that can help you better manage your tax obligations and potentially lower your tax bill.

When you work on a 1099 contract basis, you're subject to self-employment tax rather than traditional employment tax. This distinction is important because it affects how much you owe in taxes and how you make estimated tax payments.

Taking advantage of all available tax deductions can significantly reduce your taxable income. Common deductions for independent contractors include:

Understanding both self-employment and income tax obligations is crucial for proper tax planning. Federal estimated quarterly taxes cover both components, so make sure your quarterly payments account for both when you make estimated tax payments.

If you're earning substantial income as an independent contractor or have complex tax situations, it's wise to consult with a tax professional. They can help you:

At tax time, having organized records makes filing your federal income tax return much easier. Keep detailed records of:

When you file their tax returns, all your 1099 income will be reported on your individual income tax return. This includes income from multiple clients, even if some didn't send you a 1099 form.

Successfully managing taxes as a freelancer requires ongoing attention throughout the year, not just during tax season.

Create systems that help you track your income and taxes consistently:

As your income grows or changes, you may need to adjust how much you set aside for taxes. Higher earners might need to increase their savings rate to 35% or more to cover their tax liability.

The IRS requires estimated tax for individuals who expect to owe $1,000 or more in taxes. Missing these payments can result in penalties, even if you pay the full amount when you file your income tax return.

Consider how your tax strategy fits into your overall financial plan. As your freelance income grows, you might want to explore:

Handling taxes on 1099 income doesn't have to be overwhelming. By understanding how 1099 income is taxed, why self-employment tax matters, and how much to set aside consistently, you give yourself the power to protect your cash flow and avoid painful surprises.

Whether you're freelancing full-time, consulting on the side, or scaling a solo business, treating tax planning as part of your business operations is one of the best decisions you can make for your financial stability.

The key is to start early, stay organized, and be consistent with setting aside money for taxes. By following the strategies outlined in this guide, you can confidently manage your tax obligations and focus on growing your business without the stress of unexpected tax bills.

At Madras Accountancy, we help freelancers, consultants, and growing business owners navigate the complexities of 1099 income, bookkeeping, quarterly estimated payments, and strategic tax planning.

If you're looking to simplify your tax life while focusing on what you do best, our team is ready to support you.

Talk to Madras Accountancy today and stay ahead of your 1099 taxes without the stress.

Question: What percentage of 1099 income should be set aside for taxes?

Answer: Set aside 25-30% of 1099 income for taxes as a general rule, though actual amounts depend on total income, deductions, and tax brackets. This includes approximately 15.3% for self-employment taxes (Social Security and Medicare) plus federal and state income taxes. Higher earners may need to set aside 35-40% or more, while lower-income taxpayers might need 20-25%. Calculate specific percentages based on projected annual income, filing status, deductible business expenses, and applicable tax rates. Consider both current year obligations and quarterly estimated payment requirements to avoid underpayment penalties. Regular review and adjustment help ensure adequate tax reserves as income and circumstances change throughout the year.

Question: How do you calculate self-employment tax on 1099 income?

Answer: Calculate self-employment tax on 1099 income by applying 15.3% (12.4% Social Security + 2.9% Medicare) to net earnings from self-employment over $400 annually. Net earnings equal gross 1099 income minus allowable business deductions, then multiplied by 92.35% to account for the employer-equivalent portion of self-employment tax. Social Security tax applies to the first $160,200 of combined wages and self-employment income (2023 limit), while Medicare tax applies to all self-employment income. Additional Medicare tax of 0.9% applies to self-employment income over $200,000 (single) or $250,000 (married filing jointly). Use Schedule SE to calculate exact amounts and claim half of self-employment tax as an above-the-line deduction on Form 1040.

Question: What business expenses can reduce taxable 1099 income?

Answer: Business expenses that reduce taxable 1099 income include office supplies, equipment purchases, professional services, marketing costs, travel expenses, vehicle expenses, home office deductions, and professional development costs. Common deductions cover business insurance, licensing fees, professional memberships, telecommunications expenses, and equipment depreciation. Maintain detailed records with receipts, document business purposes, and ensure expenses are ordinary and necessary for your business activities. Home office deductions can be significant for home-based businesses using dedicated workspace exclusively for business. Vehicle expenses can be deducted using either actual costs or standard mileage rates. Proper expense tracking and documentation significantly reduce net 1099 income subject to both income and self-employment taxes.

Question: How should quarterly estimated tax payments be calculated for 1099 income?

Answer: Calculate quarterly estimated tax payments by projecting annual 1099 income, estimating deductible business expenses, calculating both income and self-employment taxes, and dividing by four for quarterly amounts. Use Form 1040ES worksheets or tax software to calculate estimates based on current year projections. Safe harbor rules allow payments of 100% of prior year tax (110% if prior year AGI exceeded $150,000) to avoid penalties regardless of current year obligations. Make payments by quarterly due dates (January 15, April 15, June 15, September 15) to avoid underpayment penalties. Adjust payments throughout the year based on actual income and expense patterns, increasing payments if income exceeds projections or decreasing if income falls short of estimates.

Question: What are effective strategies for managing tax savings throughout the year?

Answer: Effective tax savings strategies include opening separate business savings accounts for tax reserves, automating transfers of estimated tax percentages from each payment received, and tracking income and expenses monthly to adjust savings rates. Set up automatic transfers to move tax money immediately upon receiving 1099 payments, preventing spending of tax reserves on business or personal expenses. Use high-yield savings accounts to earn interest on tax reserves while maintaining liquidity for quarterly payments. Track actual versus projected income to adjust savings rates quarterly, and maintain spreadsheets or software tracking cumulative income, expenses, and tax obligations. Consider working with tax professionals for complex situations or significant income variations requiring sophisticated planning strategies.

Question: How do state taxes affect 1099 income tax planning?

Answer: State taxes significantly affect 1099 income tax planning as rates vary from 0% to over 13% depending on state residence and income levels. Some states have no income tax (Florida, Texas, Nevada, etc.), while others impose significant tax burdens requiring additional tax savings. State tax calculations may differ from federal calculations regarding deductions, credits, and tax rates. Many states also impose their own self-employment or disability taxes requiring separate consideration. Factor state tax obligations into overall savings percentages, consider state estimated payment requirements, and understand state-specific deductions and credits available. Multi-state operations create additional complexity requiring professional guidance to ensure compliance with all applicable state tax obligations and optimize overall tax strategies.

Question: What common mistakes should be avoided when setting aside taxes for 1099 income?

Answer: Common mistakes include underestimating total tax obligations by focusing only on income tax while ignoring self-employment taxes, mixing business and personal funds making tax money unavailable when needed, and failing to make quarterly estimated payments resulting in underpayment penalties. Avoid using tax savings for business expenses or personal needs, neglecting to track business expenses that reduce taxable income, and failing to adjust savings rates when income changes significantly. Don't ignore state tax obligations or assume prior year tax amounts will be sufficient for current year obligations. Other mistakes include waiting until year-end to address tax planning and failing to maintain adequate records supporting income and expense reporting. Professional assistance helps avoid costly mistakes and optimize tax strategies.

Question: How can 1099 workers optimize their tax situation beyond just setting aside money?

Answer: Optimize 1099 tax situations through strategic business expense planning, retirement plan contributions, health savings account utilization, and entity structure consideration for higher earners. Maximize legitimate business deductions through proper record-keeping, consider equipment purchases for depreciation benefits, and optimize home office deductions where applicable. Contribute to SEP-IRAs or solo 401(k) plans for significant tax deferral opportunities while building retirement savings. HSA contributions provide triple tax benefits for those with high-deductible health plans. Higher-income 1099 workers may benefit from forming LLCs or S Corporations to optimize self-employment tax obligations. Regular tax planning reviews help identify optimization opportunities and ensure strategies remain appropriate as income and circumstances change over time.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.