The Research and Development (R&D) tax credit is one of the most underutilized tools available to small businesses in the United States. Despite being in the tax code since 1981, thousands of eligible companies still miss out on this powerful incentive each year.

That is not due to lack of innovation. In fact, small businesses are some of the most active contributors to research, product development, and process improvement across the economy. The issue is awareness, documentation, and a mistaken belief that only tech giants qualify.

If you are improving products, developing prototypes, testing materials, writing software, or streamlining internal systems, there is a good chance your work qualifies as research and development under the IRS definition.

The tax cuts and jobs act has made these credits even more valuable for growing companies, particularly when it comes to offsetting tax liabilities. These federal credits can provide significant tax savings for eligible businesses.

At Madras Accountancy, we help U.S.-based CPA firms support their small business clients with accurate and optimized R&D tax credit claims. Through our offshore team, firms gain additional capacity for credit calculations, project tracking, and documentation review, all while reducing costs and improving compliance.

In this guide, we explain exactly what the R&D tax credit is, who qualifies, how to document your activities, and how small businesses can maximize their credit without running into red flags.

The IRS outlines a specific four-part test to determine whether an activity qualifies for the R&D tax credit. Each part must be satisfied. If your project fails to meet any one of these criteria, it will not qualify for qualified research activities.

The purpose of the research must be to develop or improve a product, process, software, formula, or invention. The improvement must relate to function, performance, reliability, or quality. Aesthetic changes do not qualify.

For example:

The research must rely on hard sciences such as engineering, biology, chemistry, computer science, or physics. This requirement ensures that the work involves a technical foundation.

Examples of qualifying fields include:

There must be uncertainty about the capability, method, or appropriate design of the product or process. If the solution is already known or obvious, it does not qualify.

Uncertainty may involve:

The activity must involve a process of evaluating alternatives through modeling, simulation, trial and error, or other scientific methods. You need to show that you considered different approaches and systematically tested them.

Examples of experimentation:

Meeting this four-part test is critical. The IRS is strict about documentation, and vague project descriptions will not be sufficient. That is why proper tracking of qualified research is essential.

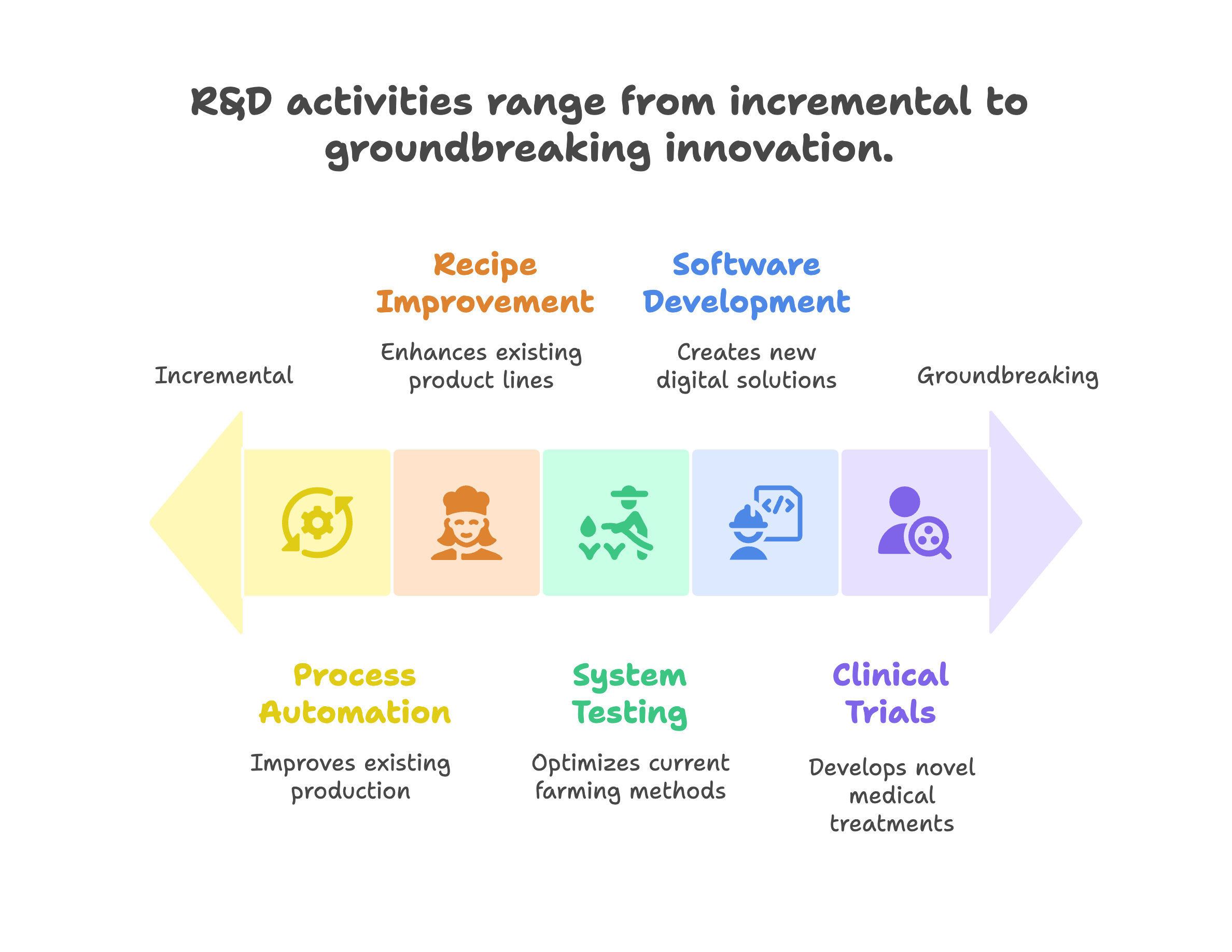

Small businesses in many industries perform qualifying research activities without labeling them as R&D. Identifying these activities is key to claiming the credit successfully.

These examples are not exhaustive. Any activity that meets the four-part test and involves uncertainty, technical problem solving, and experimentation may qualify — even if it is part of routine operations.

Once you determine that your business has eligible activities, the next step is identifying and tracking Qualified Research Expenses. These are the costs you can include in your credit calculation.

Employee compensation is often the largest QRE. This includes:

Only the portion of wages tied to qualified activities is counted. Payroll records and time tracking systems can help allocate time accurately.

Supplies used in the conduct of research may be included, as long as they are non-depreciable and consumed during the process. This includes:

Tools or equipment that are capitalized for depreciation purposes are not included.

If you hire third parties to perform qualified research, a percentage of those costs can be claimed. The default rate is 65 percent of the amount paid, as long as you retain rights to the results and are at economic risk for the outcome.

Make sure contracts specify who owns the work product and how the results will be used.

If you use leased servers or cloud-based environments for software testing or development, those costs may qualify. Examples include:

Documentation should clearly link cloud costs to specific R&D activities.

One of the most valuable features of the R&D tax credit is the payroll tax offset. This is especially useful for startup companies and early-stage companies that are not yet profitable.

Under the PATH Act, qualified small businesses can apply up to $500,000 of the R&D tax credit each tax year against their payroll tax liabilities.

To qualify for the payroll tax offset, your company must:

This option allows eligible startup businesses to receive immediate value from the credit, rather than waiting until they become profitable.

The offset applies to the employer portion of Social Security taxes, beginning with the quarter after the credit is elected on Form 6765. This payroll tax credit mechanism helps businesses must manage their cash flow more effectively while pursuing innovation.

Good documentation is the foundation of a strong R&D tax credit claim. It not only supports the credit in the event of an audit, but also helps maximize the amount you can claim.

Use time tracking tools or spreadsheets to allocate employee time to qualified projects. It does not need to be minute-by-minute, but it should reasonably reflect actual work performed.

For each qualifying project, create a short write-up that describes:

These narratives help establish the four-part test and create a clear record of your efforts.

Maintain invoices, receipts, and payment confirmations for all claimed expenses. Use cost centers or tags in your accounting system to flag R&D-related purchases.

If you are developing software, keep changelogs, version histories, and testing notes. This shows the process of experimentation and supports wage allocation.

For contract research or cloud costs, keep copies of service agreements, statements of work, and correspondence that confirm scope and ownership.

Strong documentation does not require a separate system. It can be built into your existing workflows if you set up the right processes early.

There are two primary methods for calculating the federal R&D tax credit. Choosing the right method depends on your business history, available documentation, and strategic goals.

This method offers a credit equal to 20 percent of qualified research expenses that exceed a base amount. The base amount is calculated based on:

This method typically benefits companies with consistent or increasing R&D spending over time. However, it can be more complicated to calculate, especially if older financial records are incomplete.

Most small businesses and startups choose the ASC method due to its simplicity. It provides a credit equal to 14 percent of QREs that exceed 50 percent of the average QREs from the previous three years.

If your company has no prior QREs, you may claim 6 percent of current-year QREs.

Why the ASC is Popular for Small Businesses:

Once the credit amount is determined, it is claimed on IRS Form 6765 and filed with your federal tax return.

In addition to the federal credit, more than 35 U.S. states offer their own version of the R&D tax credit. While rules vary by state, many follow similar qualification criteria.

States with Popular R&D Incentives:

Key Differences to Watch:

Your CPA or outsourced accounting partner should conduct a state-by-state analysis to determine where additional credits may be claimed. This is especially important if your business operates in multiple jurisdictions.

Even legitimate R&D claims can be denied due to documentation gaps, misunderstanding of eligibility rules, or misallocated expenses. Avoiding the following pitfalls can save time and reduce audit risk.

The most common reason for credit denial is lack of supporting evidence. Vague project descriptions, missing timesheets, or undocumented expenses make it difficult to prove eligibility.

Not all product development is R&D. Activities like market research, user testing, or routine bug fixes may not meet the four-part test. Misclassifying these tasks can trigger IRS scrutiny.

Only non-depreciable supplies are eligible. Businesses sometimes include the cost of machinery, buildings, or IT infrastructure by mistake.

Failing to review state-level credits leaves money on the table. Each tax year, thousands of eligible companies miss out on substantial savings because they do not know state incentives exist.

For contract research to qualify, your business must retain rights to the research results and bear the financial risk. Contracts that shift ownership or liability may disqualify the expense.

To get the most value from the credit, small businesses should move from passive to proactive. This involves planning, process improvement, and collaboration with tax professionals who understand the nuances.

Set up processes to track eligible activities as they occur. This includes:

The more you capture in real-time, the less you have to recreate during tax season.

R&D is not limited to engineering teams. Review marketing, operations, and customer support teams for qualifying activities such as software automation, internal tools, or improved workflows.

Tax professionals who specialize in R&D credits can identify expenses that generalists may overlook. They also understand how to navigate IRS requirements and minimize audit risk while maximizing tax savings.

If you qualify, the payroll tax offset allows you to see benefits faster, especially if you are not yet profitable. This improves cash flow and supports reinvestment in future projects. Qualified small businesses can offset payroll tax liabilities rather than waiting to offset income tax liability.

Even if your federal claim remains steady, changes in your business or location may open new opportunities at the state level. A yearly review ensures you do not miss these updates.

The ability to offset payroll tax represents a significant advantage for early-stage companies. Unlike traditional tax credits that reduce income tax liability, the payroll tax credit allows businesses to receive immediate cash flow benefits.

This feature is particularly valuable because businesses must pay payroll taxes regardless of profitability. By allowing qualified small businesses to offset payroll against R&D credits, the government has created an incentive that works even for companies that are not yet generating taxable income.

At Madras Accountancy, we work with CPA firms across the U.S. to strengthen their R&D credit services. Our offshore team provides:

This helps CPA firms scale their R&D credit practice without adding internal cost or complexity. Small businesses benefit from accurate filings, faster turnarounds, and lower audit exposure.

We ensure every eligible dollar is captured and justified with audit-ready documentation, helping maximize both traditional tax liabilities reduction and payroll tax benefits.

The R&D tax credit is not just for tech giants. It is a powerful tool that can help small businesses reduce tax liabilities, improve cash flow, and reinvest in future innovation. Whether you are writing software, developing better packaging, or building a new product prototype, your work may qualify.

Understanding the four-part test, tracking expenses properly, and maintaining clear documentation are key. By collaborating with specialists and using the payroll tax offset when possible, small businesses can fully realize the value of the R&D tax credit.

The credits can provide substantial benefits, particularly for early-stage companies that can offset payroll tax obligations rather than traditional income tax liabilities. This makes the R&D credit especially valuable during the critical growth phases when cash flow is most important.

If you are unsure whether your business qualifies or want help optimizing claims for your clients, Madras Accountancy is here to support you.

Question: What are R&D tax credits and how can small businesses qualify for them?

Answer: R&D tax credits provide dollar-for-dollar tax reductions for qualified research activities, with small businesses able to claim credits for wages, supplies, contractor costs, and overhead related to research and development efforts. Qualifying activities include developing new products, improving existing products, creating new processes, or enhancing performance, functionality, reliability, or quality. The research must involve technological uncertainty, systematic experimentation, and technological in nature. Small businesses qualify when conducting activities to discover technological information and eliminate uncertainty through systematic experimentation, process improvement, or product development efforts.

Question: What types of business activities and expenses qualify for R&D tax credits?

Answer: Qualifying R&D activities include software development, product design and testing, prototype creation, process improvement initiatives, and scientific experimentation. Eligible expenses cover employee wages for research activities, supplies consumed in research, contractor payments for qualified research, and allocated overhead costs for facilities used in R&D. Common qualifying activities include developing new software features, improving manufacturing processes, creating new formulations, testing product modifications, and engineering design work. Documentation requirements include time tracking, project descriptions, expense allocation, and evidence of systematic experimentation and technological uncertainty.

Question: How much can small businesses save through R&D tax credits?

Answer: Small businesses can claim R&D credits equal to 20% of qualified research expenses exceeding a base amount, or 14% of current year expenses under the alternative simplified credit method. Annual credit amounts vary widely based on research activities, but small businesses often claim $10,000-100,000+ in credits annually. Unused credits can be carried forward for 20 years, providing long-term tax benefits. Small businesses with minimal tax liability can elect to apply up to $250,000 in R&D credits against payroll taxes for up to five years, making credits valuable even for businesses with limited income tax obligations.

Question: What documentation and records must small businesses maintain for R&D tax credits?

Answer: Small businesses must maintain comprehensive documentation including detailed project descriptions, time records for employees engaged in research, expense receipts and allocation methods, and evidence of technological uncertainty and systematic experimentation. Required records include project objectives, methodologies used, results achieved, and explanations of how activities qualify as research. Maintain time tracking systems showing employee hours spent on qualifying activities, contractor agreements and invoices, supply purchase records, and overhead allocation calculations. Documentation should demonstrate the "four-part test" requirements and support credit calculations during potential IRS examinations.

Question: Can small businesses claim R&D credits for software development and technology projects?

Answer: Yes, small businesses can claim R&D credits for software development projects that involve technological uncertainty and systematic experimentation to develop new functionality, improve performance, or eliminate technical challenges. Qualifying software activities include developing new applications, creating algorithms, improving existing software capabilities, and integrating complex systems. However, routine maintenance, cosmetic changes, and standard customization typically don't qualify. Software development must involve uncertainty about capability, method, or design and require experimentation to achieve intended results. Documentation should clearly demonstrate technological challenges and experimental processes used to overcome them.

Question: How do small businesses calculate and claim R&D tax credits on their returns?

Answer: Small businesses calculate R&D credits using Form 6765, which requires detailed tracking of qualified research expenses including wages, supplies, contractor costs, and allocated overhead. Choose between the traditional credit method (20% of expenses over base amount) or alternative simplified credit method (14% of current year expenses). Calculate base amounts using historical averages or fixed-base percentages for established businesses. New businesses use simplified calculations without base amount requirements. File Form 6765 with annual tax returns and consider amended returns for prior years if previously unclaimed credits are identified.

Question: What common mistakes should small businesses avoid when claiming R&D credits?

Answer: Common R&D credit mistakes include inadequate documentation, failing to track time spent on qualifying activities, incorrectly categorizing routine activities as research, and missing opportunities to claim credits for eligible activities. Avoid claiming credits for general business operations, market research, routine testing, or activities without technological uncertainty. Don't overlook qualifying activities like process improvements, software development, or product modifications. Ensure proper expense allocation between qualifying and non-qualifying activities, maintain contemporaneous records, and avoid retroactive documentation. Consider professional assistance for complex situations to maximize credits while ensuring compliance.

Question: Should small businesses work with tax professionals for R&D credit claims?

Answer: Small businesses should strongly consider working with tax professionals specializing in R&D credits due to complex qualification requirements, documentation standards, and calculation methods. R&D credit specialists can identify qualifying activities often overlooked by general practitioners, ensure proper documentation procedures, maximize credit amounts through proper expense allocation, and provide audit defense if challenged by the IRS. Professional fees are often offset by additional credits identified and risk reduction from proper compliance. However, businesses with straightforward R&D activities and strong internal documentation may handle simple claims independently using appropriate software and guidance.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.