A brown envelope lands on your desk and routine work stops. The questions arrive first, confidence second. The way you respond decides how long the enquiry lasts and how much it costs. Here is a clear path to move from request to resolution.

A step-by-step guide to How to Handle an HMRC Tax Investigation (UK). You will see what common letters mean, which documents to prepare, how to communicate, typical timelines, and when to involve advisors. It suits UK businesses and US-headquartered groups with UK entities, including teams that use offshore accounting support.

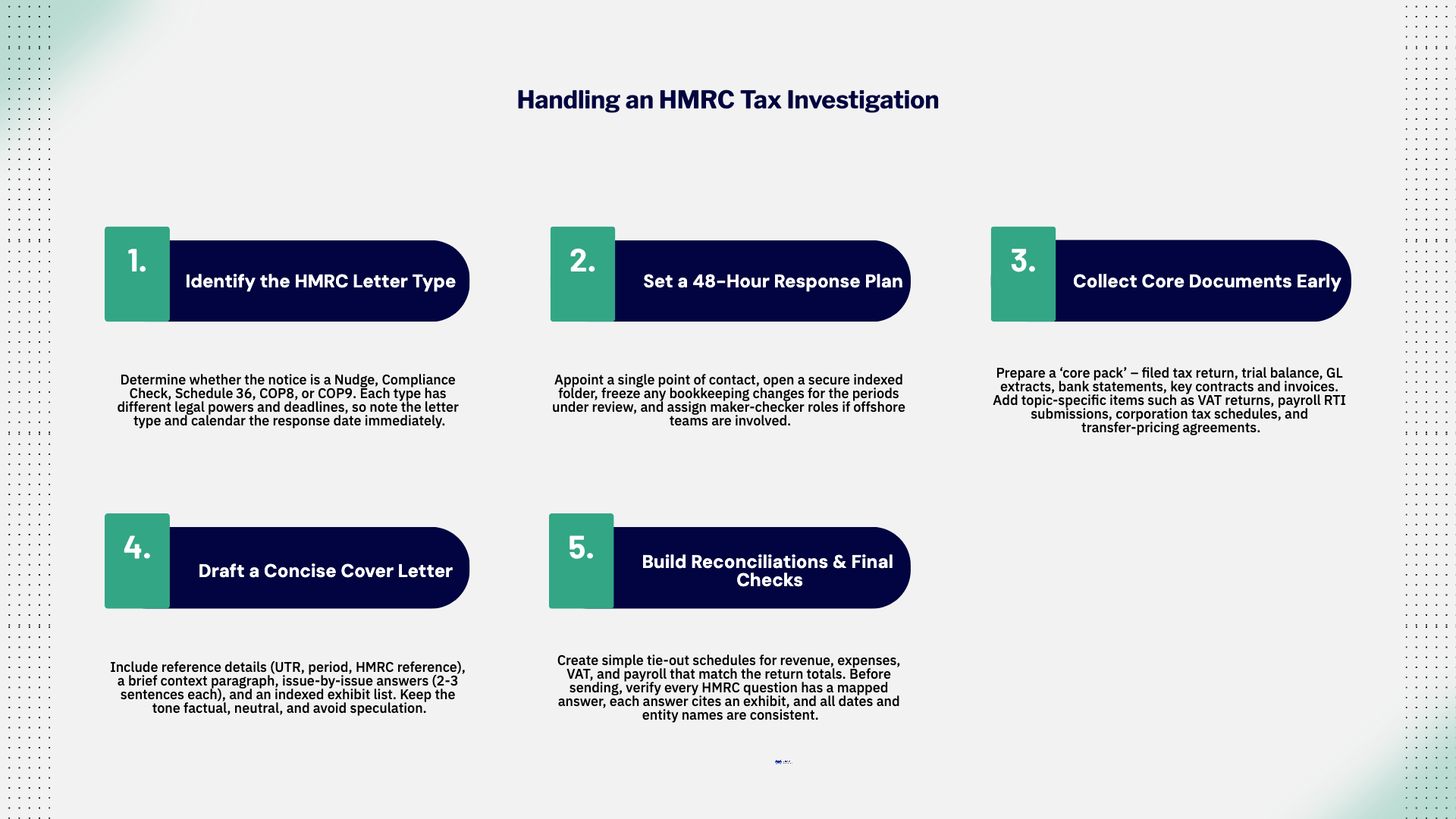

HMRC flags a risk area and asks you to review and correct if needed. No formal information powers are used. You should still check the point and reply.

Formal notice that HMRC is checking a return or a specific risk. It lists the period and topics under review and may request documents.

A legal request for records and explanations. It specifies what to provide and by when. Missing the deadline can lead to penalties.

Used for complex avoidance concerns. Technical, document-heavy, and often slower to close.

Used where HMRC suspects deliberate behaviour. Managed under the Contractual Disclosure Facility. You must seek specialist advice.

Action: Identify the letter type and the legal footing. Calendar the response date on the same day.

Core pack

Topic-specific

Keep filenames short and indexed, for example:A1_Contract_SaaS_2024-04-01.pdf, R1_GL_to_Return_TieOut_FY2024.xlsx.

Purpose: Frame the issues, tie each answer to an exhibit, and request the outcome you want.

Include:

Tone: Factual, neutral, and complete. Avoid speculation. If something needs time, state the date you will deliver it.

Create simple schedules that connect your GL and source documents to the filed return.

Each schedule should fit on one tab and show totals that match the return.

If deadlines are tight, request a short extension early and give a date you can meet.

Advisors can draft the response, prepare schedules, manage calls, and agree a practical closure route.

Move fast on structure, slow on claims. Know the letter type, collect only what proves your case, and answer with short explanations backed by indexed evidence. This reduces follow-ups and helps you close on the facts.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.