.png)

Small businesses face many of the same financial risks as larger enterprises, but often with fewer resources and less formal infrastructure. This makes internal control testing not just important, but essential. Without it, businesses expose themselves to fraud, compliance failures, and costly financial errors that can significantly impact business operations.

Internal control systems are the policies and procedures designed to ensure reliable financial reporting, safeguard assets, and ensure compliance with laws and regulations. Testing these internal control systems is how a business knows they are operating effectively and achieving their intended control objectives.

Understanding best practices for internal control testing helps small businesses reduce the risk of fraud and operational failures while maintaining regulatory compliance. An effective internal control system provides checks and balances that protect the organization and support sound business processes.

In this guide, we break down internal control testing for small businesses. You will learn what internal control frameworks involve, how to test them systematically, common control deficiencies to avoid, and the best practices for ongoing monitoring and improvement.

Internal control refers to the mechanisms a company uses to manage risk and achieve its objectives. A comprehensive internal control framework is typically divided into five main categories:

The control environment sets the tone at the top, establishing ethical culture, organizational structure, and management philosophy. This foundation influences how internal control activities are designed and implemented throughout the organization.

Risk assessment involves the business's ability to identify and assess risks that could prevent achievement of objectives. This process helps organizations understand where internal control is most needed to mitigate risk effectively.

Control activities are the policies and procedures that help ensure management directives are carried out. These internal control mechanisms are designed to mitigate risk and achieve specific control objectives.

Information and communication systems allow for effective reporting and decision-making. These systems support the internal control framework by ensuring relevant information flows throughout the organization.

Monitoring activities are processes that ensure the other internal control components are functioning correctly. Regular monitoring helps identify when internal control systems need improvement or modification.

Examples of internal control activities controls include:

For small businesses, some internal control measures might be informal, but they still play a critical role in preventing errors and fraud while supporting compliance objectives.

Small businesses are often more vulnerable to internal fraud and operational risks. A lack of oversight or understaffed finance departments can create opportunities for theft, misreporting, or regulatory issues that threaten business survival.

Key reasons to implement and test internal control systems include:

Fraud Prevention: Effective internal control systems can prevent fraud by creating multiple approval layers and maintaining clear audit trails. These controls help detect and deter fraudulent activities such as asset misappropriation or payroll fraud.

Accurate Financial Reporting: Internal control over financial reporting ensures that financial statements reflect the true position of the business. This accuracy is essential for management decision-making and external stakeholder confidence.

Regulatory Compliance: Strong internal control helps ensure compliance with laws and regulations, avoiding penalties and legal risks related to tax, labor, and industry-specific requirements. For some businesses, sox compliance may also be required.

Operational Efficiency: Well-designed internal control systems ensure business processes work as intended and resources are used effectively. This operational efficiency can significantly impact profitability and growth.

Stakeholder Confidence: Strong internal control increases credibility with investors, lenders, and other external stakeholders. An auditor reviewing your business will look for evidence of effective internal control systems.

Testing these internal control measures provides evidence that they are not just documented, but actually functioning to achieve their intended control objectives.

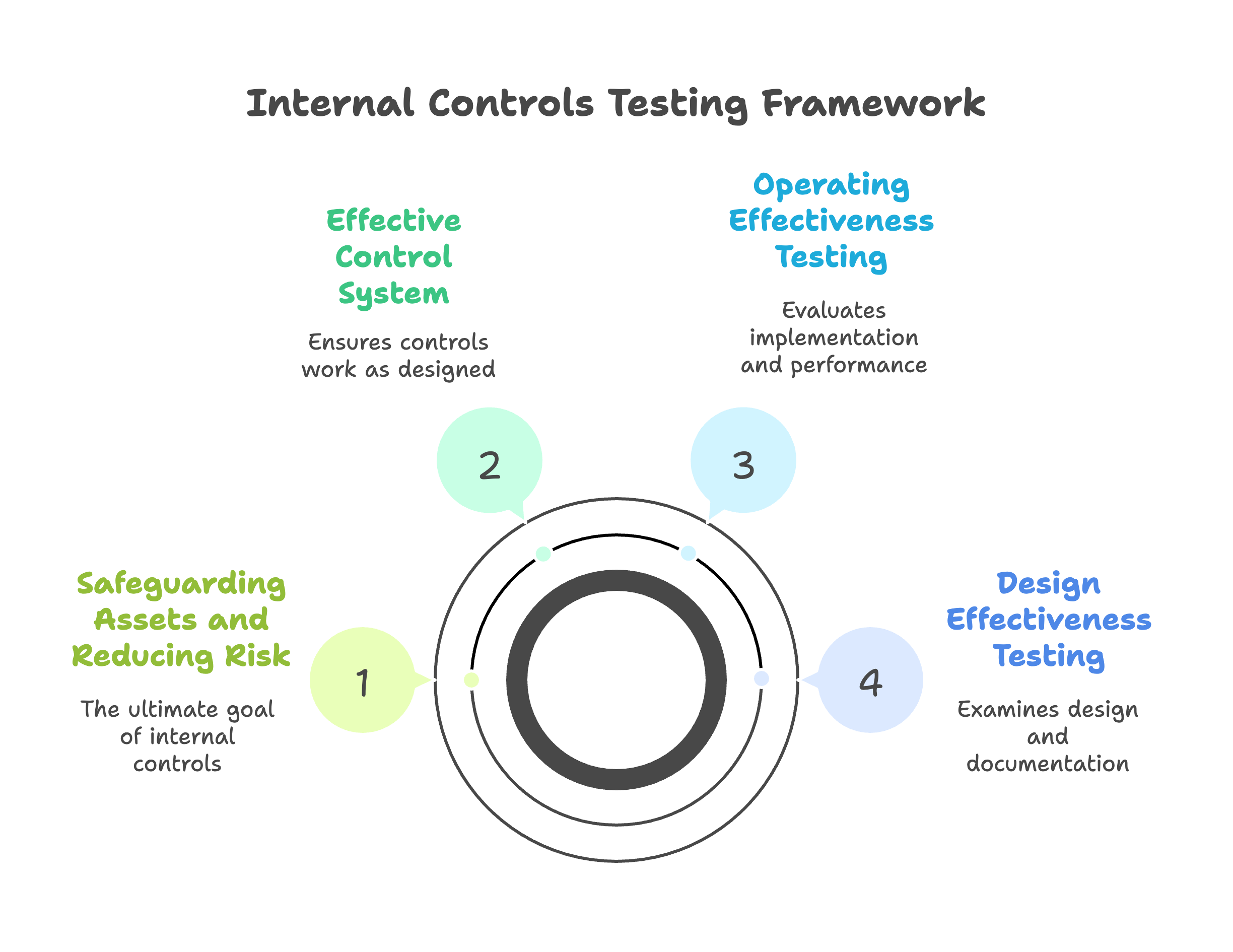

Internal control testing involves evaluating whether policies and procedures are being followed and whether they are effective at achieving their control objectives. This testing process helps determine if the control environment is working as designed and whether it will continue operating effectively in the future.

There are two main types of internal control testing that organizations should perform:

This examines whether internal control measures are appropriately designed to prevent or detect errors and fraud. Design testing answers critical questions like:

If an internal control is poorly designed, it will not matter how well it is implemented or followed.

This evaluates whether internal control has been implemented and is being performed as intended. Operating effectiveness testing involves:

Both design and operating effectiveness must be evaluated to confirm that an internal control system is working properly to safeguard assets and reduce risk.

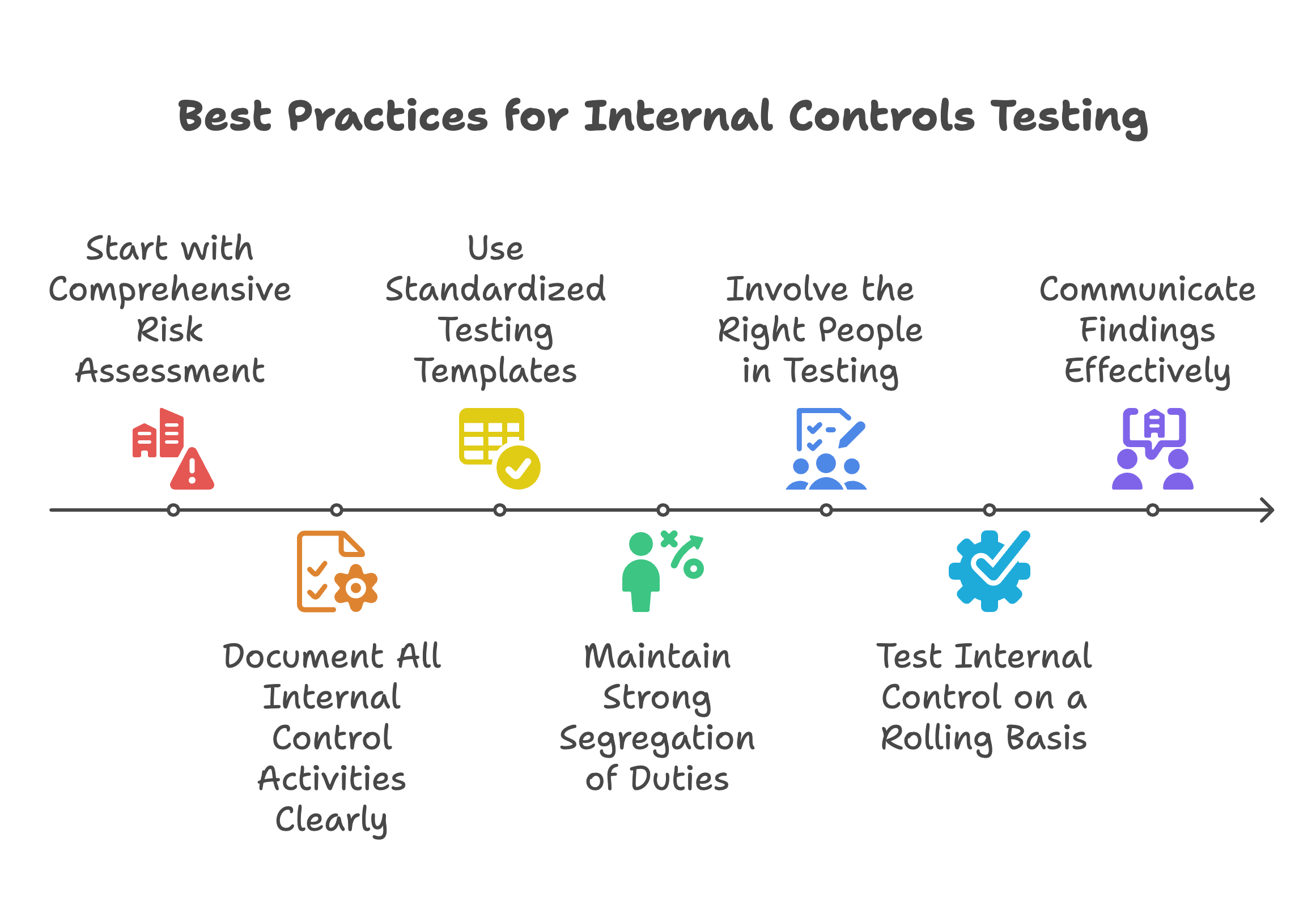

To ensure a thorough and efficient internal control testing process, organizations should follow these established best practices:

Identify areas of highest risk first. Focus internal control testing on activities related to:

Use a risk assessment matrix to categorize risks by likelihood and impact. This risk and control analysis helps prioritize which internal control systems to test first and allocate resources effectively.

Each internal control should be described in detail with specific control objectives:

Poor documentation is one of the top reasons internal control frameworks fail during audit reviews or regulatory examinations.

Develop templates that help testers evaluate both the design and operational aspects of internal control systems. Your template should include:

Templates improve consistency and make reporting of internal control testing results easier and more reliable.

Many small businesses have limited personnel, which leads to overlapping roles. This concentration of duties is a major risk factor that can undermine internal control effectiveness.

Ensure that segregation of duties prevents any single individual from being responsible for authorizing, recording, and reviewing the same transaction. If proper segregation of duties is not feasible due to size constraints, implement compensating controls like owner reviews or third-party oversight.

Include both internal stakeholders and, when necessary, external advisors in internal control testing. Employees involved in performing the internal control should not be the ones testing it to maintain objectivity.

In small companies, an external auditor or accounting firm can help conduct or validate internal control testing without conflicts of interest, providing independent assessment of control effectiveness.

Instead of testing all internal control systems at once, spread the workload throughout the year. This approach allows for continuous improvement and ensures that control deficiencies are identified and addressed early.

For example:

Prepare a comprehensive internal control testing report with:

Make sure management understands the findings and implications for business operations and risk management.

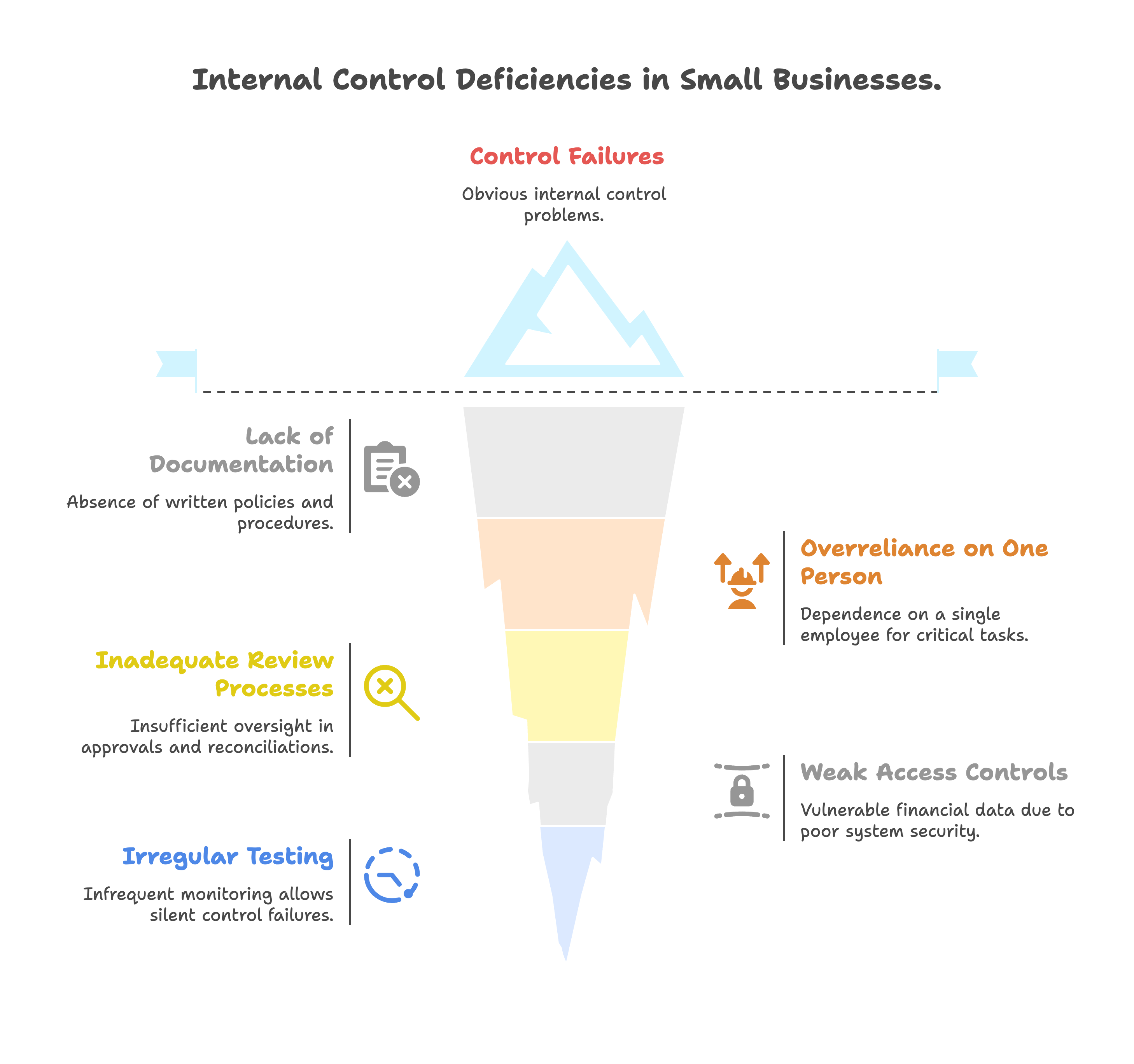

Understanding common control failures helps organizations prevent them and maintain effective internal control systems.

Without proper documentation, it is impossible to prove that internal control exists or is operating effectively. This is a common issue in businesses where policies and procedures are verbal or informal rather than formally documented.

Many small businesses depend on one trusted employee for accounting or operations. While this approach may seem efficient, it creates significant risk if that person makes an error or commits fraud, as there are no compensating controls in place.

Approvals, reconciliations, and financial statement preparations often lack proper oversight. Review processes should be documented and conducted regularly by someone other than the preparer to maintain effective internal control.

If accounting or point-of-sale systems lack password protection, audit logs, or proper access controls, your financial data is vulnerable to tampering and unauthorized changes.

Implementing internal control is not enough. If controls are not monitored and tested regularly, they can fail silently for months without detection, undermining their ability to safeguard assets and reduce the risk of errors or fraud.

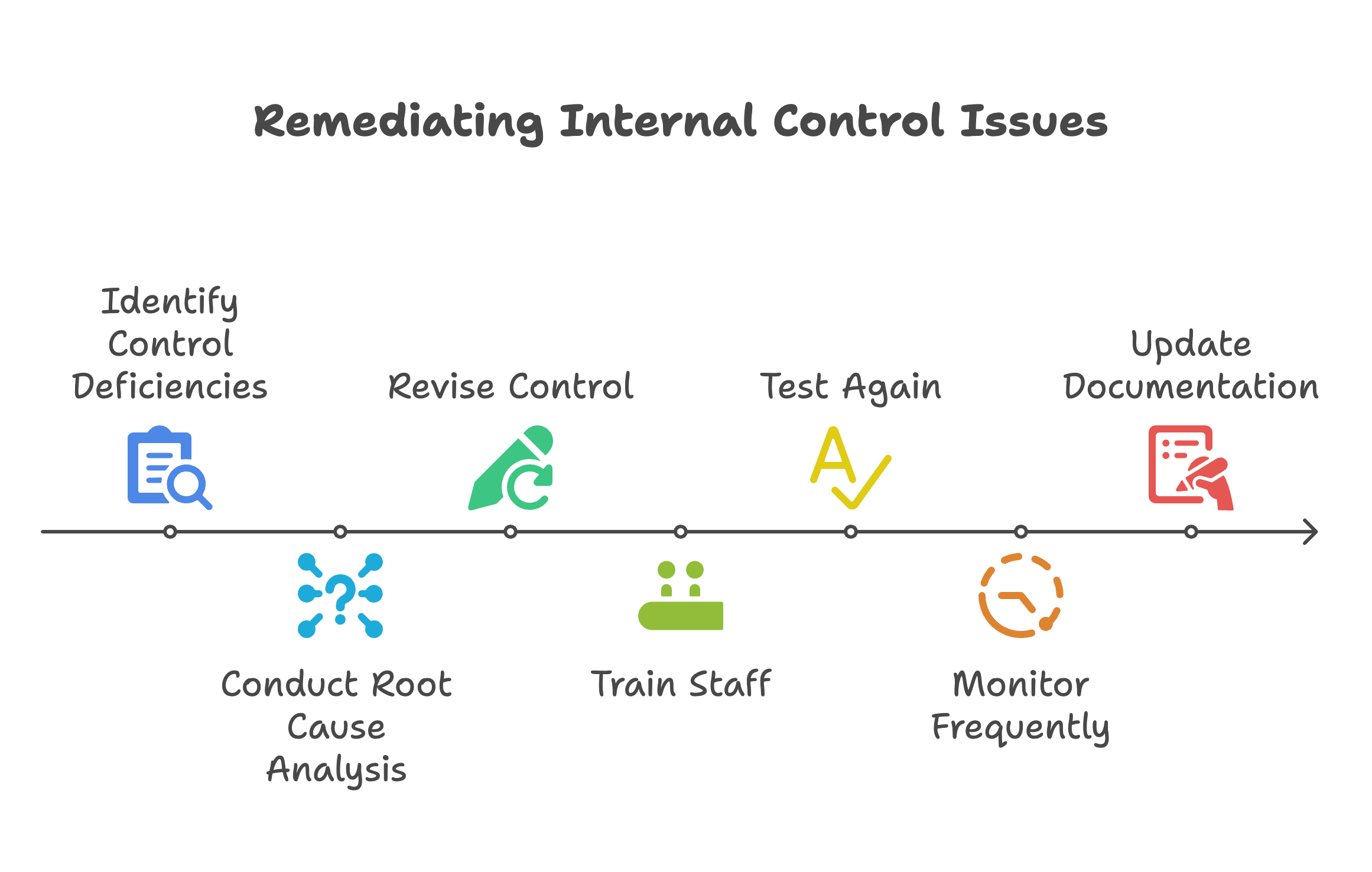

Once control deficiencies are identified through testing, organizations must act quickly to resolve them and restore effective internal control. Here is a standard approach:

Understand why the internal control issue occurred and what factors contributed to the control deficiency.

Modify the existing internal control or create a new one to address the root cause and achieve the intended control objective.

Ensure everyone involved understands the revised internal control and their specific role in its execution.

Reassess the revised internal control to ensure it is operating effectively and meeting its control objectives.

Increase monitoring until the internal control proves reliable and consistently operating effectively.

Documentation should be updated to reflect all changes and ensure the internal control framework remains current and comprehensive.

Small businesses can use various tools to automate and streamline controls management and testing processes. Some popular options include:

Look for tools that offer reporting features, reminders for recurring internal control activities, and user access tracking to support your internal control framework.

An auditor examining your business will focus heavily on internal control systems, particularly those related to financial reporting. Understanding what an auditor looks for can help you prepare:

For small businesses that work with CPA firms, internal control testing may be part of broader audit readiness or financial oversight services. CPA firms can provide:

At Madras Accountancy, we help CPA firms expand their internal control testing capabilities through dedicated offshore support. This includes:

Offshore support helps small firms offer more comprehensive internal control services without overloading their internal teams, while maintaining high standards for quality and compliance.

While most small businesses are not subject to sox compliance requirements, understanding these standards can help improve your internal control framework:

Different industries may have specific internal control requirements:

All businesses should consider internal control related to:

Creating an effective internal control system starts with establishing the right control environment. Management must demonstrate commitment to internal control through:

All employees should understand their role in the internal control framework:

An effective internal control system requires ongoing attention and improvement:

Organizations should establish metrics to measure internal control effectiveness:

Establish regular reporting on internal control status:

Internal control systems are the foundation of sound financial management and operational effectiveness. For small businesses, implementing and testing effective internal control ensures that finances are accurate, business operations run smoothly, and risks are minimized through appropriate safeguard measures.

By focusing on high-risk areas, documenting every process clearly, and testing both design and operating effectiveness, small businesses can protect themselves from errors and fraud while ensuring compliance with relevant laws and regulations.

An effective internal control framework provides the checks and balances necessary to prevent fraud, maintain accurate financial reporting, and support operational efficiency. Regular testing of internal control systems also builds credibility with lenders, investors, and regulators who rely on these controls to assess business risk.

The key to success lies in understanding that internal control is not a one-time implementation but an ongoing process that requires regular attention, testing, and improvement. Controls help organizations achieve their objectives, but only when they are properly designed, implemented, and monitored.

With the right tools, training, and partner support, even small teams can maintain strong, compliant internal control systems that effectively mitigate risk and support business growth. The investment in effective internal control pays dividends through reduced risk of fraud, improved operational efficiency, and enhanced stakeholder confidence.

If your CPA firm wants to offer internal control testing as a service or improve your current process, Madras Accountancy can help. Our offshore support model allows you to scale efficiently while maintaining high-quality standards for internal control assessment and testing.

Question: What are internal controls and why are they important for small business financial management?

Answer: Internal controls are processes, policies, and procedures designed to ensure reliable financial reporting, prevent fraud, protect assets, and ensure compliance with laws and regulations. For small businesses, internal controls are important because they reduce fraud risks, improve financial accuracy, enhance operational efficiency, and provide assurance to lenders, investors, and stakeholders. Effective controls help detect errors early, prevent unauthorized transactions, and ensure proper authorization for business activities. While small businesses may have limited resources for complex control systems, basic controls significantly reduce risks and improve business operations. Strong internal controls also facilitate growth by providing frameworks for consistent operations as businesses expand.

Question: What are the key components of effective internal controls for small businesses?

Answer: Key internal control components for small businesses include control environment (tone at the top, ethical standards), risk assessment procedures, control activities (authorization, segregation of duties), information and communication systems, and monitoring activities. Control environment establishes organizational culture and management commitment to integrity. Risk assessment identifies potential problems and vulnerabilities in operations and reporting. Control activities include specific policies and procedures for authorization, documentation, and verification. Information systems ensure accurate data capture and reporting. Monitoring involves regular review and testing of control effectiveness. Even small businesses can implement basic versions of these components appropriate to their size and complexity.

Question: How should small businesses implement segregation of duties with limited staff?

Answer: Small businesses can implement segregation of duties by separating authorization, recording, and custody functions even with limited staff. Key separations include having different people authorize transactions, record them, and maintain custody of assets. When complete segregation isn't possible, implement compensating controls like management review, independent verification, and regular reconciliations. Use technology to create automatic controls, establish approval limits requiring multiple signatures for large transactions, and implement regular rotation of responsibilities. Bank reconciliations should be performed by someone other than the person writing checks or making deposits. External accountants can provide independent reviews and oversight to supplement limited internal segregation capabilities.

Question: What internal control testing procedures should small businesses perform regularly?

Answer: Small businesses should perform regular testing procedures including bank reconciliation reviews, cash count verifications, accounts receivable confirmation testing, and expense approval documentation reviews. Test segregation of duties compliance, authorization procedures for large transactions, and access controls for financial systems. Conduct surprise cash counts, verify inventory records accuracy, and review vendor payment authorization procedures. Test backup and recovery procedures, review user access rights, and verify approval workflows. Document testing results, investigate exceptions, and implement corrective actions for identified weaknesses. Regular testing helps ensure controls remain effective and identifies problems before they become significant issues. Professional assistance may help design testing procedures appropriate for business size and risk levels.

Question: How can small businesses document and maintain their internal control systems?

Answer: Document internal controls through written policies and procedures manuals, organizational charts showing responsibilities, authorization matrices specifying approval limits, and process flowcharts illustrating transaction flows. Maintain documentation of control testing results, exception reports, and corrective actions taken. Create employee handbooks covering financial procedures, establish job descriptions with control responsibilities, and document system access rights and approval procedures. Regular updates ensure documentation remains current with business changes and regulatory requirements. Simple documentation approaches work for small businesses - focus on clarity and completeness rather than complexity. Proper documentation supports training, provides audit trails, and ensures continuity during staff changes or business growth.

Question: What are common internal control weaknesses in small businesses and how can they be addressed?

Answer: Common small business internal control weaknesses include inadequate segregation of duties, lack of management oversight, insufficient documentation, and weak IT controls. Address segregation issues through compensating controls, technology solutions, and external oversight. Improve management oversight through regular financial review meetings, exception reporting, and performance monitoring. Strengthen documentation by creating written procedures, approval matrices, and process flowcharts. Enhance IT controls through password policies, access restrictions, and regular security updates. Other common weaknesses include inadequate cash controls, weak vendor approval processes, and insufficient expense authorization procedures. Regular assessment helps identify and address control gaps before they result in losses or errors.

Question: How do internal controls support small business growth and scaling?

Answer: Internal controls support small business growth by providing frameworks for consistent operations, reducing key person dependencies, and enabling delegation of responsibilities with appropriate oversight. Strong controls facilitate access to capital by demonstrating operational maturity to lenders and investors. They enable geographic expansion by ensuring consistent procedures across locations and support technology implementation by providing structured approaches to system changes. Controls also help maintain quality standards during rapid growth periods when businesses might otherwise lose operational discipline. Scalable control systems grow with businesses, supporting larger transaction volumes, more complex operations, and additional locations while maintaining accuracy and fraud prevention capabilities.

Question: When should small businesses consider professional assistance with internal controls?

Answer: Consider professional assistance with internal controls when experiencing rapid growth, preparing for financing or investment, facing regulatory requirements, or after discovering control weaknesses or fraud incidents. Professional help is valuable when implementing new systems, conducting risk assessments, or preparing for audits. CPAs can design control systems appropriate for business size, conduct control testing and evaluation, and provide objective assessments of control effectiveness. Professional assistance is also beneficial when businesses lack internal expertise, need compliance with specific regulations, or want independent validation of control adequacy. Cost-benefit analysis should consider potential losses from control weaknesses versus professional fees, with many businesses finding professional assistance pays for itself through improved operations and risk reduction.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.