A clear comparison of internal and external audits for US and UK organizations. It explains who performs each, the purpose, when a business needs them, what standards apply, and how findings are reported. It also notes coordination points if you use offshore accounting support.

Quick definitions

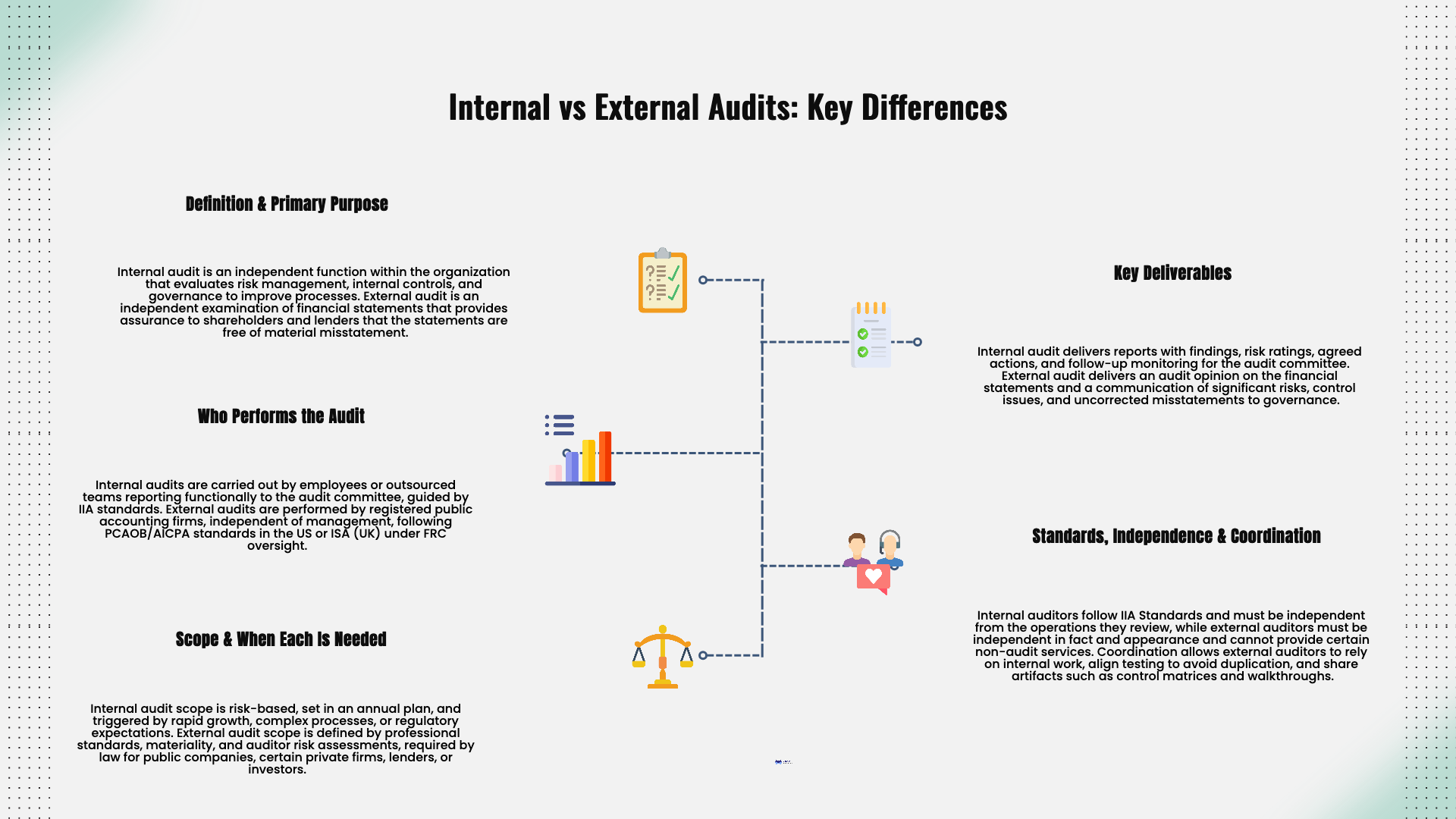

Internal audit

An independent function inside the organization that evaluates risk management, internal controls, and governance. It improves processes and helps management and the board protect value.

External audit

An independent examination of the company’s financial statements that provides assurance to shareholders and lenders that the statements are free of material misstatement.

Who performs each role

Internal audit

- Employees of the company or a co-sourced/outsourced team reporting functionally to the audit committee and administratively to management.

- Work guided by the Institute of Internal Auditors’ International Standards for the Professional Practice of Internal Auditing.

External audit

- A registered public accounting firm, independent of management.

- US: audits performed under PCAOB standards for issuers or AICPA GAAS for private companies.

- UK: audits performed under International Standards on Auditing (UK), overseen by the FRC.

Primary purpose and scope

Internal audit

- Tests the design and operating effectiveness of internal controls across finance, operations, IT, and compliance.

- Advises on process improvement and risk mitigation.

- Scope is risk-based and set in an annual audit plan approved by the audit committee.

External audit

- Obtains reasonable assurance that the financial statements are free from material misstatement due to error or fraud.

- Focuses on financial reporting controls and substantive testing of balances and disclosures.

- Scope is defined by professional standards, materiality, and auditor risk assessments.

When businesses need each audit

Internal audit: common triggers

- Rapid growth or multi-entity, multi-country operations.

- Regulatory expectations or listing rules that require stronger governance.

- Complex processes such as revenue recognition, inventory, payroll, and IT general controls.

- Management wants independent assurance on controls before an external audit or financing.

External audit: common triggers

- Statutory requirement based on size thresholds or public listing.

- US: public companies require annual audits. Many lenders require audits for private companies.

- UK: audit is mandatory when company size exceeds thresholds or by shareholder request.

- Investor, lender, or acquirer requires audited financial statements.

What each delivers

Internal audit outputs

- Reports with findings, risk ratings, and agreed actions with owners and due dates.

- Follow-up on remediation and periodic reporting to the audit committee.

External audit outputs

- An audit opinion on the financial statements.

- Communication to those charged with governance covering significant risks, control issues, and uncorrected misstatements.

Standards and independence

Internal audit

- Follows IIA Standards and Code of Ethics.

- Must be sufficiently independent from operations it reviews, with direct access to the audit committee.

- Can provide advisory work if it does not impair objectivity.

External audit

- Must be independent in fact and appearance from the client.

- Restricted from providing certain non-audit services to audit clients.

- Applies professional skepticism and documents evidence to support conclusions.

Coordination between internal and external auditors

- External auditors may consider internal audit work to adjust the nature and extent of external testing.

- Internal audit plans can align to key financial reporting risks to reduce duplication.

- Shared artifacts: process narratives, control matrices, walkthroughs, and test results.

- Clear protocols avoid management preparing the same evidence twice and help offshore teams package PBC items correctly.

Using offshore accounting support without raising audit risk

- Segregate duties for preparer, reviewer, and approver.

- Enforce role-based access, MFA, and activity logs for any offshore users.

- Maintain SOPs, reconciliations, and evidence with version control and dated sign-offs.

- Route “prepared by client” requests through a ticketing system with owners and due dates.

- Have internal audit sample offshore-processed transactions during busy season.

Practical decision guide

Choose to stand up or expand internal audit when you need:

- Continuous control testing, SOX-style discipline, or rapid remediation feedback.

- Independent review of operational and IT risks beyond financial reporting.

Choose or plan for external audit when you need:

- Statutory compliance, financing, listing, or investor confidence supported by audited financials.

- An independent opinion to accompany M&A or fundraising.

Wrap-up

Both audits strengthen trust, but they solve different problems. One improves how the business runs every day. The other validates what the business reports at year-end. Use both intentionally, coordinate the evidence, and the work of each will make the other more efficient.

%2075-100%20(2).png)

%2075-100%20(4).png)

%2075-100%20(7).png)