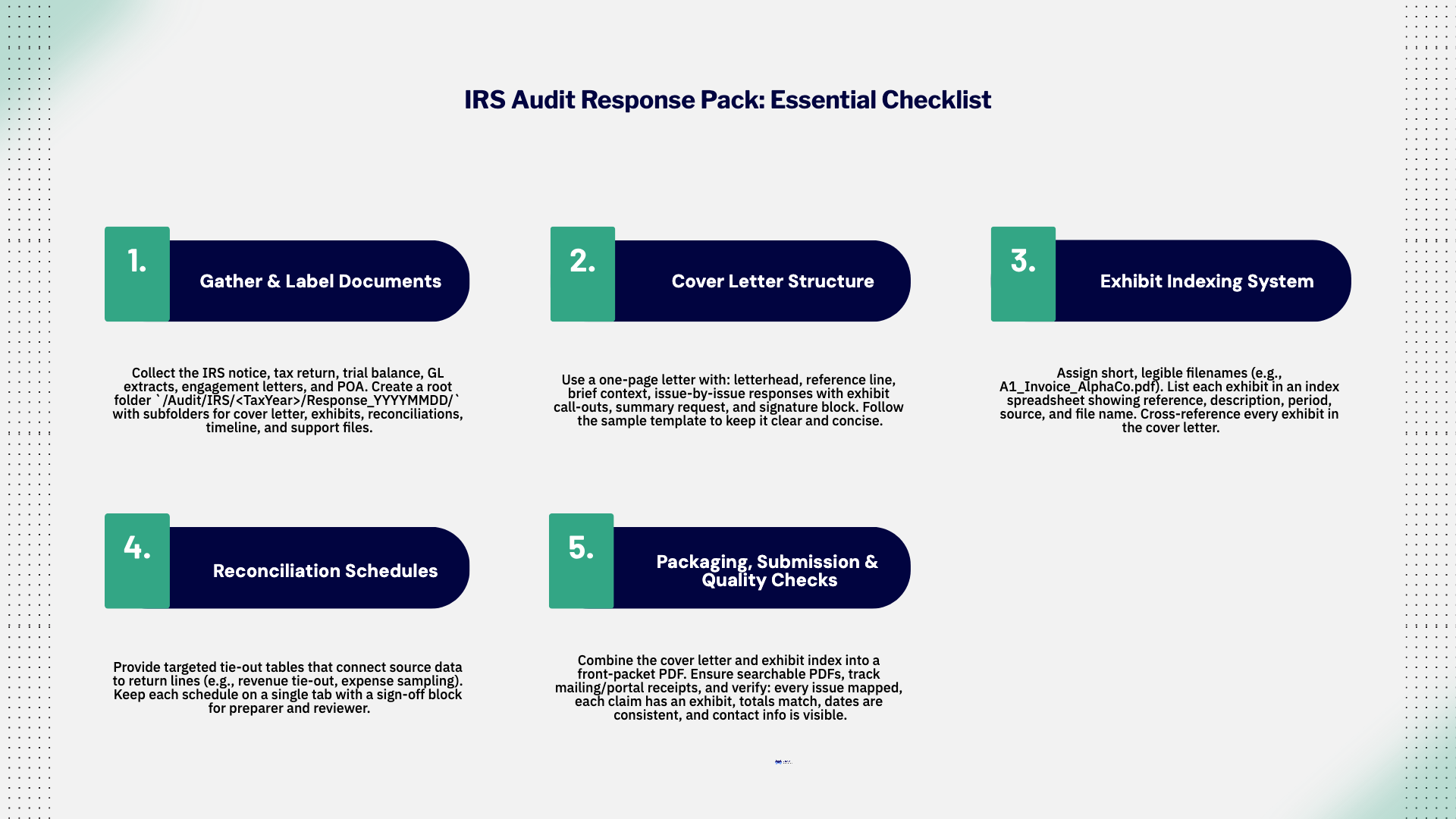

An audit letter arrives and the clock starts. What slows teams is not the facts. It is scattered documents, unclear explanations, and long responses that miss the point. This pack shows a clean structure you can copy, so you can answer once, answer clearly, and move on.

A practical response structure for US IRS audits that also maps well to UK HMRC enquiries. You get a concise cover letter model, an exhibit indexing system, reconciliation schedules, and a fact timeline template. It suits in-house teams and companies working with offshore accountants. Use it as your IRS Audit Response Pack: Sample Cover Letter, Indexing, and Exhibits (Download).

Set a single folder root:/Audit/IRS/<TaxYear>/Response_YYYYMMDD/

Create subfolders: 01_Cover_Letter, 02_Exhibits, 03_Recons, 04_Timeline, 05_Support.

Frame the response, map each request to exhibits, and state the outcome you seek. Keep to one or two pages.

[Date]

Internal Revenue Service

[Address from notice]

Re: [Taxpayer Legal Name], EIN [XX-XXXXXXX] — Tax Year [YYYY]

Response to [Notice/IDR reference and date]

Dear Examiner,

We submit our response to the Service’s information request dated [date] for the items listed below. Each item is addressed briefly here and supported by indexed exhibits.

Issue A: [Short title]

- Response: [One to three sentences with the conclusion]

- Support: Exhibits A1–A3; Reconciliation R-A; Timeline T1

Issue B: [Short title]

- Response: [One to three sentences with the conclusion]

- Support: Exhibits B1–B2; Reconciliation R-B

We believe the enclosed materials resolve the requests as filed. Please contact [Name, Title, phone, email] for any clarifications.

Sincerely,

[Name]

[Title], on behalf of [Taxpayer Legal Name]

[Address | Phone | Email]

For UK enquiries, replace IRS references with HMRC, add UTR and VAT number as relevant.

Prefix by issue → Letter (A, B, C)

Sequence → 1, 2, 3

Example filenames:

A1_Invoice_AlphaCo_2024-03-17.pdf

A2_BankStatement_Chase_Apr2024_p1-4.pdf

B1_Contract_SaaS_2023-12-01.pdf

| Ref | Description | Period | Source |

|-----|------------------------------------------|-------------|-----------------|

| A1 | Customer invoice #INV-311 (Alpha Co.) | Mar 2024 | AR Subledger |

| A2 | Bank statement (Chase) p.1–4 | Apr 2024 | Bank Portal |

| A3 | Cash receipt screenshot (ID #8472) | Apr 2024 | ERP |

| R-A | Revenue tie-out: GL→Return (Sch. M-1) | FY 2024 | Close workbook |

| T1 | Factual timeline for Issue A | 2023–2024 | Prepared by Co. |

Save the index as 02_Exhibits/Exhibit_Index.xlsx and export a PDF copy in the same folder.

Use targeted schedules to connect source data to the filed return. Avoid long narratives.

| Line | Source (GL) | Amount | Adjustments | Return Line | Amount |

|------|-------------|--------|-------------|-------------|--------|

| 1 | GL 4000 | 1,245,220 | - Deferred Rev Δ (35,410) | Form 1120 Line 1a | 1,209,810 |

| 2 | GL 4010 | 58,600 | - Contra Rev (1,200) | Form 1120 Line 1a | 57,400 |

| | | | | Total per return | 1,267,210 |

| Sample ID | Vendor | Date | Amount | GL Acct | Exhibit Ref | Notes |

|-----------|--------|------|--------|---------|-------------|-------|

| S-01 | Beta Ltd | 02/14 | 4,820 | 6100 | A1 | Contract on file |

Keep each recon to one tab, with a clear sign-off block.

Summarize what happened, when, and who approved it. This helps resolve “why” without long emails.

| Date | Event / Document | Parties | Impact on Tax Position | Exhibit |

|------------|---------------------------|-----------------|------------------------|---------|

| 2024-01-05 | MSA executed | Taxpayer, Alpha | Revenue recognition start | B1 |

| 2024-03-17 | First invoice issued | Taxpayer | Performance obligation met | A1 |

| 2024-04-10 | Cash received | Bank | Cash application | A2, A3 |

For HMRC, follow the enquiry letter’s channel. Use the same indexing logic and keep a file note for any phone calls.

[Company Letterhead]

[Date]

IRS — [Unit/Address from notice]

Re: [Taxpayer], EIN [XX-XXXXXXX], Tax Year [YYYY]

Response to [Notice/IDR #] dated [Date]

[Opening paragraph: scope and summary]

Issue A — [Title]

Response: [2–3 sentences]

Support: Exhibits A1–A?, Reconciliation R-A, Timeline T1

Issue B — [Title]

Response: [2–3 sentences]

Support: Exhibits B1–B?, Reconciliation R-B

Requested disposition: [Close as filed / adjust as described]

Sincerely,

[Name, Title]

[Phone, Email]

Ref,Description,Period,Source,File

A1,Customer invoice #INV-311,Mar 2024,AR Subledger,A1_Invoice_AlphaCo_2024-03-17.pdf

A2,Bank statement p1-4,Apr 2024,Bank Portal,A2_Bank_Chase_Apr2024_p1-4.pdf

R-A,Revenue tie-out FY2024,FY2024,Close Workbook,RA_Revenue_TieOut_FY2024.xlsx

Prepared by: [Name, Date] Reviewed by: [Name, Date] Tickmarks: [Legend]

Matter: [Issue name] Period: [YYYY] Contact: [Name, Email]

Keep the response short at the front and heavy in the back. A clear cover letter, a tight index, reconciliations that tie to the return, and a dated timeline will answer most audit questions without back-and-forth. This structure helps US IRS and UK HMRC workflows and scales well with offshore support.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.