.png)

In a manufacturing business, not all costs are directly tied to a specific product. While raw materials and direct labor are easy to track, many overhead costs remain hidden in the background. These include utilities, factory rent, depreciation of machinery, indirect costs for supervision, and maintenance. Collectively, these are known as manufacturing overhead or factory overhead.

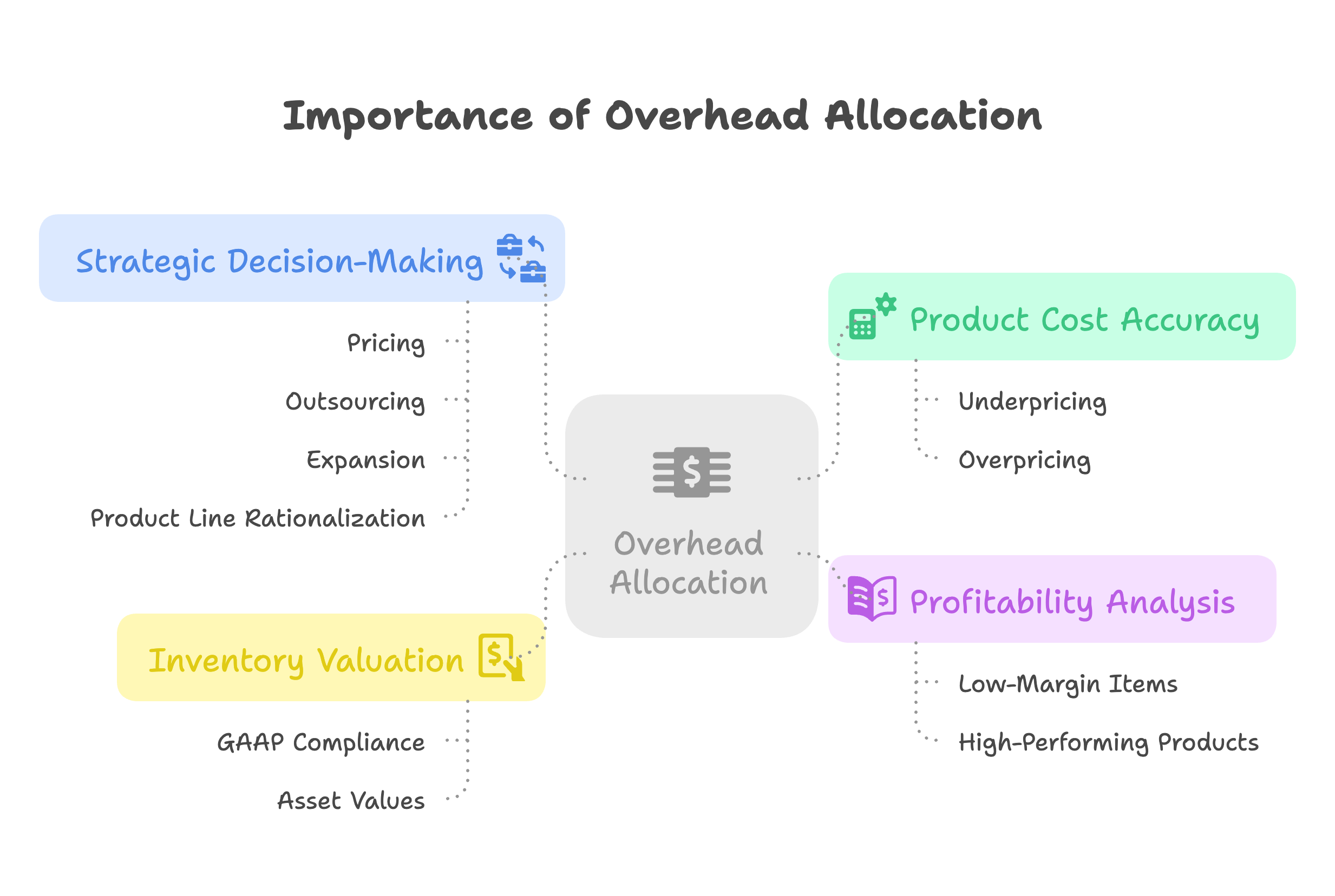

Accurately implementing overhead allocation is essential for calculating product costs, pricing decisions, inventory valuation, profitability analysis, and financial reporting. Poor overhead allocation can distort your cost of goods sold and lead to incorrect business decisions. The choice of allocation method significantly impacts how overhead cost is distributed across products and affects overall cost allocation accuracy.

This guide is designed to help business owners, controllers, and CPA firms understand how overhead allocation works, why it matters, and how to apply different allocation methods based on business size, production complexity, and reporting needs. Understanding various overhead allocation methods is crucial for effective cost management and accurate financial reporting.

Manufacturing overhead refers to all indirect costs incurred during the production process. These overhead costs are not directly traceable to a specific product unit but are necessary for manufacturing operations. Unlike direct costs such as raw materials and direct labor, these overhead expenses require systematic allocation to products.

Common examples of overhead cost include:

These costs must be systematically allocated to products to determine accurate production cost. Unlike direct cost components such as materials and direct labor, which can be easily assigned, overhead allocation requires specific allocation methods to distribute overhead costs fairly across all products.

If overhead allocation is insufficient, your product costs will appear artificially low, leading to underpricing and margin erosion. Over-allocation of overhead cost inflates costs, making you uncompetitive. Proper cost allocation ensures accurate product costing.

Without proper overhead allocation, it is difficult to determine which products or product lines are truly profitable. You might scale up low-margin items or discontinue high-performing products based on faulty cost allocation data.

In accounting, inventory must include an appropriate allocation of overhead cost to comply with GAAP. Inaccurate overhead allocation skews asset values and affects cost of goods manufactured calculations.

Decisions around pricing, outsourcing, expansion, or product line rationalization depend on reliable cost allocation information. The total cost of products must reflect accurate overhead allocation to support informed decision-making.

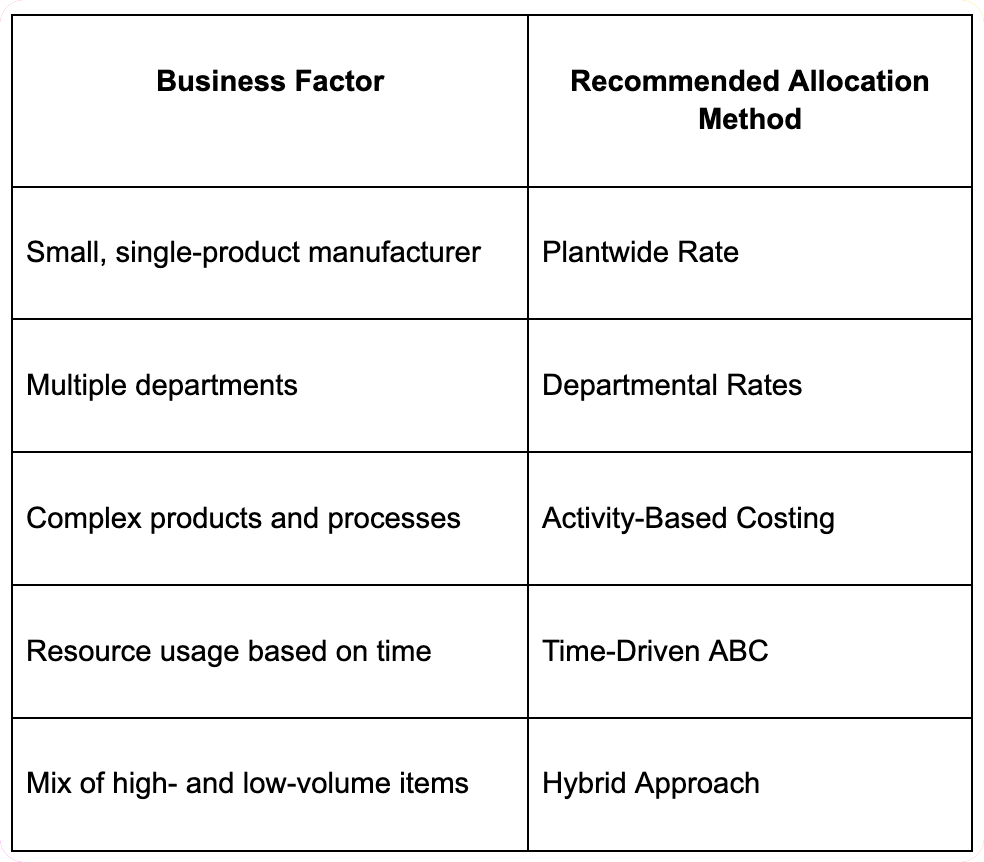

There is no one-size-fits-all allocation method for overhead allocation. Businesses typically choose among the following overhead allocation methods:

Each allocation method varies in complexity, cost, and accuracy. The choice depends on the size of the business, the diversity of its products, and available data for overhead allocation calculations.

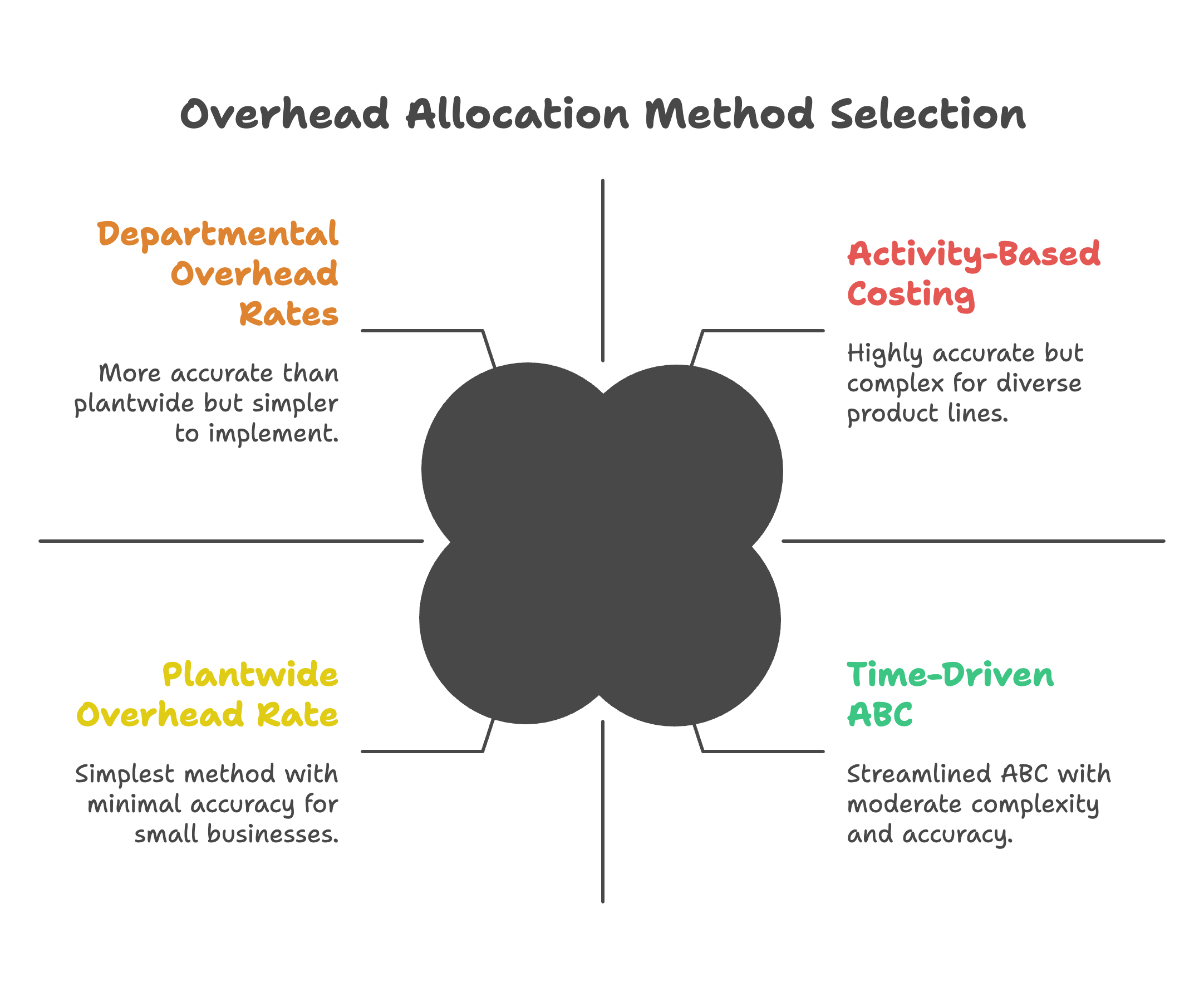

This is the simplest overhead allocation method. The company applies a single overhead rate to all products, based on one allocation base such as direct labor hours, machine hours, or direct labor cost.

If a product uses 5 machine hours, its allocated overhead cost is: 5 hours × $20 = $100

Instead of using a single overhead rate, overhead allocation is separated by department. Each department calculates its own allocation rate based on the most appropriate allocation base for that department's overhead cost.

If a product uses 2 hours in Machining and 1 hour in Assembly: (2 × $30) + (1 × $40) = $100 total overhead allocation

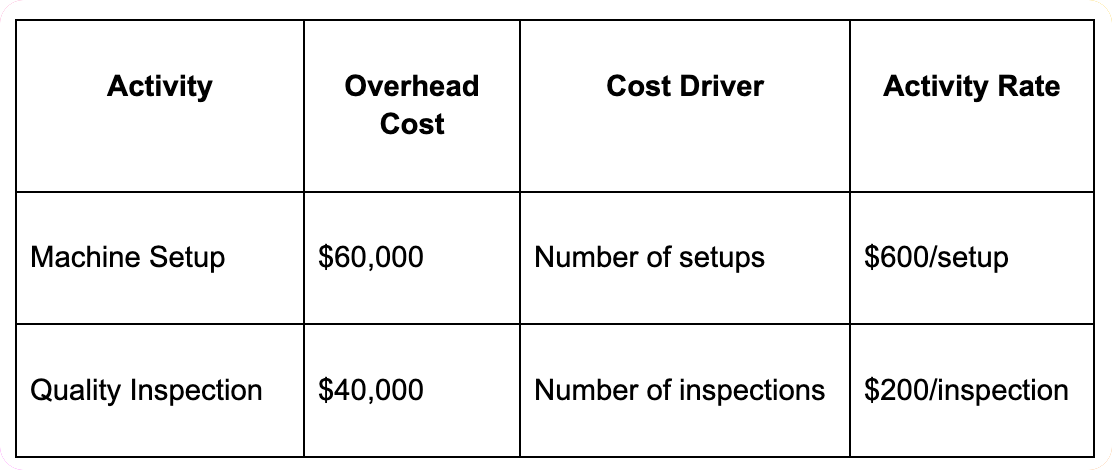

ABC represents a sophisticated overhead allocation method that allocates overhead costs based on activities that drive costs, not just departments or volume. This cost method identifies multiple cost drivers across the production cycle and assigns overhead costs more accurately.

If a product requires 3 setups and 2 inspections: (3 × $600) + (2 × $200) = $2,200 in overhead allocation

ABC is particularly useful for manufacturers with complex products, high overhead costs, and diverse production activities.

TDABC is a streamlined version of ABC that simplifies overhead allocation. Instead of tracking every transaction, this allocation method estimates how long activities take and uses time as the primary cost driver for overhead allocation.

Some companies blend allocation methods to suit different types of overhead costs or product lines. For example:

The goal is to balance cost allocation accuracy with implementation effort while ensuring proper overhead allocation across all products.

CPA firms should assess the manufacturer's size, systems, data availability, and overhead cost structure before recommending an overhead allocation method.

The selection of appropriate allocation bases is crucial for accurate overhead allocation. Common allocation bases include:

The choice of allocation base should reflect the actual relationship between overhead cost incurrence and the allocation base to ensure accurate cost allocation.

Overhead allocation affects several areas of financial reporting:

Includes direct materials, direct labor, and applied overhead through proper allocation methods

Understated overhead allocation leads to undervalued inventory and affects cost of goods sold

Misallocated overhead distorts margins and profitability analysis

Decisions around product continuation rely on accurate overhead allocation and cost information

Manufacturers undergoing audits or preparing for M&A should ensure overhead allocation methods are well-documented, consistently applied, and aligned with GAAP requirements.

When actual overhead costs differ from applied overhead, manufacturers must account for the variance:

These variances require adjustment at period-end to ensure accurate cost of goods and inventory valuation.

Some overhead costs vary seasonally, requiring adjusted allocation rates:

Manufacturers should consider these patterns when establishing overhead allocation rates to ensure consistent cost per unit throughout the year.

Modern ERP systems can automate much of the overhead allocation process:

Professional accountants add value in selecting, implementing, and optimizing overhead allocation methods. Their responsibilities include:

Outsourcing cost allocation functions or seeking fractional CFO services can be especially helpful for growing manufacturers without internal finance expertise to manage complex overhead allocation requirements.

Manufacturing overhead allocation is more than a compliance task. It is the backbone of product costing, profitability analysis, and strategic planning. Choosing the right allocation method depends on the complexity of operations and the availability of accurate data for overhead allocation.

Whether you adopt a simple plantwide allocation rate or a detailed ABC cost method, the key is consistency, accuracy, and alignment with your financial goals. The total cost of products must reflect appropriate overhead allocation to support informed decision-making about pricing, product mix, and operational efficiency.

Effective overhead allocation requires careful selection of allocation bases, consistent application of the chosen allocation method, and regular review of allocation accuracy. Understanding how to allocate overhead costs properly enables manufacturers to make better decisions about product pricing, capacity utilization, and strategic investments.

CPA firms and manufacturing accountants must guide businesses through this process to support transparency and competitiveness. By implementing appropriate overhead allocation methods and maintaining accurate cost allocation systems, manufacturers can achieve better cost control, improved profitability analysis, and enhanced financial reporting accuracy.

Question: What is manufacturing overhead and why is proper allocation important for businesses?

Answer: Manufacturing overhead includes all indirect costs of production that cannot be directly traced to specific products, such as factory rent, utilities, maintenance, supervisory salaries, and equipment depreciation. Proper overhead allocation is important because it enables accurate product costing, supports pricing decisions, helps identify profitable products and customers, and ensures compliance with financial reporting standards. Accurate allocation also supports inventory valuation, cost control efforts, and strategic decision-making about product mix and capacity utilization. Poor overhead allocation can lead to incorrect pricing, unprofitable product decisions, and distorted financial results that mislead management and stakeholders about true product profitability and business performance.

Question: What are the traditional methods for allocating manufacturing overhead costs?

Answer: Traditional manufacturing overhead allocation methods include direct labor hours, direct labor costs, machine hours, and units of production as allocation bases. Direct labor hour allocation divides total overhead by total labor hours and applies overhead based on labor hours used per product. Direct labor cost allocation uses labor costs as the base for proportional overhead assignment. Machine hour allocation works well for automated processes where machine time drives overhead costs. Units of production allocation simply divides overhead equally among all units produced. These methods are simple to implement and understand but may not reflect actual overhead consumption patterns in modern manufacturing environments with diverse products and processes.

Question: How does activity-based costing (ABC) improve overhead allocation accuracy?

Answer: Activity-based costing (ABC) improves overhead allocation accuracy by identifying specific activities that drive overhead costs and assigning costs based on actual activity consumption rather than simple volume measures. ABC identifies cost drivers such as setup activities, quality inspections, material handling, and engineering support, then traces these costs to products based on actual usage. This method provides more accurate product costs for complex manufacturing environments with diverse products, varying batch sizes, and different support requirements. ABC helps identify high-cost activities, supports process improvement efforts, and provides better information for pricing, product mix, and customer profitability decisions. However, ABC requires more detailed data collection and analysis than traditional methods.

Question: What factors should businesses consider when selecting overhead allocation methods?

Answer: Businesses should consider production process characteristics, product diversity, cost structure, and information system capabilities when selecting overhead allocation methods. Evaluate whether overhead costs are driven by labor, machine time, or other activities to choose appropriate allocation bases. Consider product complexity differences, batch size variations, and customer service requirements that might affect overhead consumption patterns. Assess information system capabilities for tracking allocation bases and cost data accuracy. Balance accuracy benefits against implementation and maintenance costs, considering materiality of overhead amounts and decision-making requirements. Professional consultation helps evaluate alternatives and select methods providing optimal balance of accuracy, practicality, and cost-effectiveness for specific business circumstances.

Question: How do predetermined overhead rates work and when should they be used?

Answer: Predetermined overhead rates are calculated before production periods by dividing estimated overhead costs by estimated activity levels, then applied to products throughout the period based on actual activity consumption. These rates enable timely product costing without waiting for actual overhead amounts, support consistent pricing decisions, and smooth out seasonal overhead variations. Use predetermined rates when timely costing information is important, overhead costs vary seasonally, or when job costing systems require immediate cost assignment. At period end, compare applied overhead to actual overhead and adjust for over- or under-applied amounts. Predetermined rates work best when overhead estimates are reasonably accurate and activity levels are predictable, requiring regular review and updating to maintain accuracy.

Question: What are the advantages and disadvantages of different overhead allocation methods?

Answer: Traditional volume-based methods offer simplicity, low implementation costs, and ease of understanding but may provide inaccurate product costs in complex environments. Direct labor allocation works well for labor-intensive processes but becomes less relevant in automated environments. Machine hour allocation suits automated processes but requires detailed machine time tracking. Activity-based costing provides greater accuracy for complex operations but involves higher implementation and maintenance costs. Predetermined rates enable timely costing but may create over/under-applied overhead requiring adjustment. Each method involves trade-offs between accuracy, complexity, and cost that businesses must evaluate based on their specific circumstances, decision-making requirements, and cost-benefit considerations.

Question: How should businesses handle over-applied or under-applied overhead?

Answer: Handle over-applied or under-applied overhead by analyzing variances to understand causes, then disposing of amounts through cost of goods sold adjustments for immaterial amounts or proportional allocation to inventory and cost of goods sold for material amounts. Investigate significant variances to identify problems with overhead estimates, activity level projections, or cost control issues requiring management attention. For predetermined rate systems, expect some variance but investigate unusual amounts that might indicate estimation problems or operational changes. Consider adjusting predetermined rates for future periods based on variance analysis and improved estimates. Document variance analysis and disposal methods for audit purposes and maintain consistency in treatment approaches. Regular variance analysis helps improve future estimates and overhead management.

Question: What role does technology play in modern overhead allocation systems?

Answer: Technology enables sophisticated overhead allocation through automated data collection, real-time costing systems, and advanced analytics for identifying cost drivers and allocation bases. ERP systems integrate overhead allocation with production tracking, financial reporting, and management reporting functions. RFID and sensor technologies provide detailed activity data for ABC systems, while machine monitoring systems track equipment usage for machine-hour allocations. Business intelligence tools analyze overhead patterns and identify optimization opportunities. Cloud-based systems enable real-time collaboration and reporting across multiple locations. Technology reduces manual overhead allocation effort, improves accuracy through automated calculations, and provides detailed reporting for management decision-making. However, technology investments must be justified by accuracy improvements and decision-making benefits relative to implementation and maintenance costs.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.