.png)

Maryland's sales and use tax system offers more simplicity than many states, but it still requires careful attention to specific rules and exemptions. Whether you're opening a new business in Baltimore, expanding throughout the state, or selling into Maryland from elsewhere, understanding the tax requirements will help you stay compliant and avoid costly penalties.

Let's walk through everything you need to know about Maryland sales tax for 2025, from basic rates to filing procedures and special exemptions.

Maryland operates a straightforward sales and use tax system administered by the Comptroller of Maryland. The state maintains a uniform statewide rate without additional local sales taxes, which simplifies compliance compared to states with varying local rates.

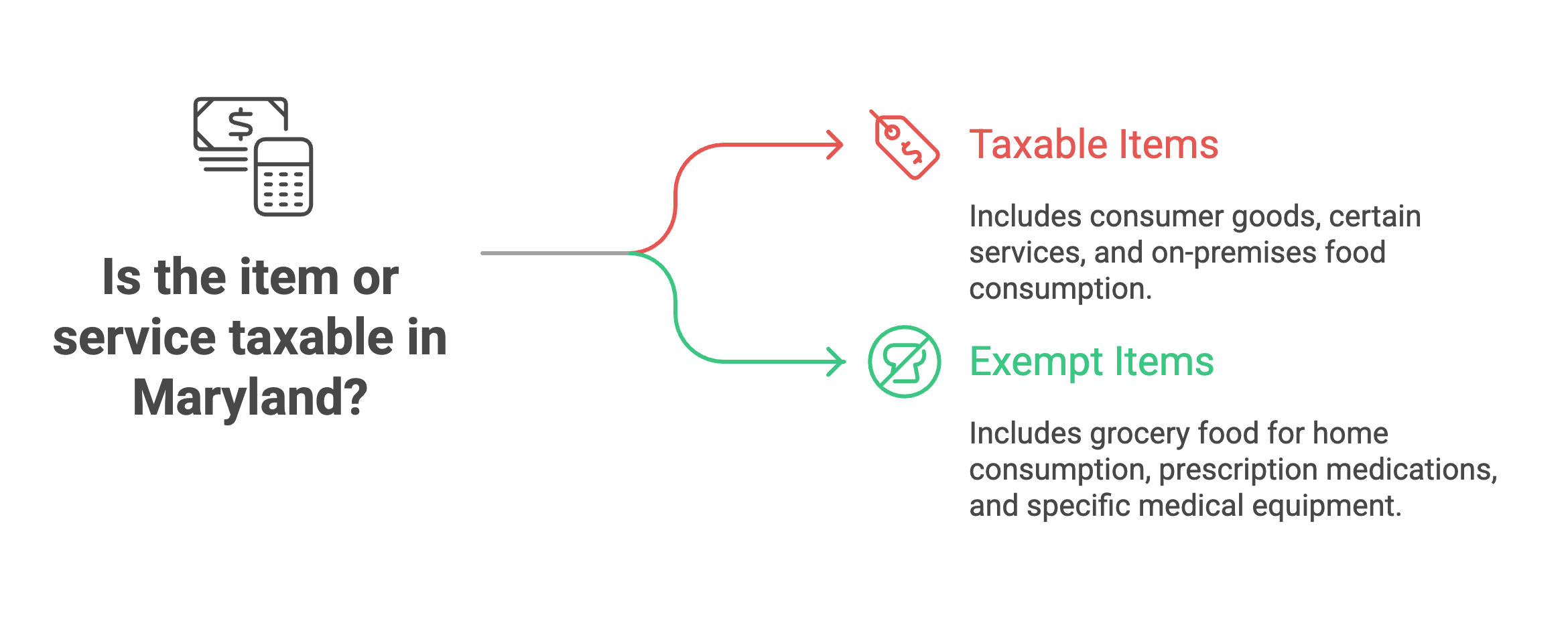

The Maryland sales tax applies to retail sales of most tangible personal property and certain taxable services. This covers typical retail transactions while providing specific exemptions for necessities and certain business activities.

Sales and use tax work together to ensure Maryland gets its tax revenue regardless of where purchases originate. When you buy items from out-of-state vendors who don't collect Maryland tax, you owe use tax at the same rate as the sales tax.

Maryland law requires businesses with nexus in the state to register for a sales and use tax license and collect tax on all taxable transactions. The registration process establishes your tax obligations and filing requirements.

Maryland maintains a simple rate structure with a statewide sales tax rate of 6% on most retail purchases. This rate applies uniformly across all counties and cities, eliminating the complexity of varying local rates found in many other states.

Unlike states with additional local taxes, you don't need to worry about rates by county or city variations in Maryland. The consistent 6% rate makes tax calculation straightforward for businesses operating statewide.

A Maryland sales tax calculator becomes useful mainly for determining which items qualify for exemptions rather than calculating different rates. The uniform rate structure simplifies most calculations significantly.

The state sales tax rate of 6% applies to most taxable goods and services, but certain items have special rates or complete exemptions. Understanding these variations helps ensure accurate tax collection.

Maryland sales tax rates remain stable compared to states that frequently adjust local rates. This consistency helps businesses plan and budget more effectively for tax obligations.

Most retail sales of tangible personal property are subject to Maryland sales tax. This includes typical consumer goods like clothing, electronics, furniture, and general merchandise sold to end users.

Certain taxable services also require sales tax collection, though Maryland taxes fewer services than many other states. Taxable services typically include telecommunications, some repair services, and specific business services.

Food items receive special treatment in Maryland's tax system. Most grocery or market food items for home consumption are exempt from sales tax. However, prepared food consumed on the premises is generally taxable.

The distinction between exempt and taxable food sales depends on several factors. Food for consumption off the premises is typically exempt, while food consumed on the premises usually requires tax collection.

Alcoholic beverages follow different rules than other food items. While some food sales are exempt, alcoholic beverages are generally subject to sales taxes regardless of where they're consumed.

A person operating a substantial grocery or market business sells food items under special exemption rules. The grocery or market business sells the food for consumption off premises without collecting sales tax in most cases.

Prescription medications are exempt from Maryland sales tax, but over-the-counter drugs typically aren't. Medical equipment and devices may qualify for exemptions under specific circumstances.

Before you can collect sales tax in Maryland, you need to register for a sales and use tax license through the Comptroller of Maryland. This registration establishes your authority to collect tax and your filing obligations.

Maryland requires businesses with physical or economic nexus in the state to register and collect sales tax. Economic nexus thresholds require registration when you exceed certain sales volumes to Maryland customers.

The combined registration application allows you to register for multiple Maryland taxes simultaneously. This streamlines the process if you need licenses for sales tax, withholding tax, or other state obligations.

You'll need your federal employer identification number and basic business information to complete the registration process. The state uses this information to establish your tax account and determine filing requirements.

Most businesses receive monthly filing assignments, but smaller operations might qualify for quarterly filing based on expected tax liability. The comptroller assigns filing frequency during registration.

Most Maryland businesses must file sales tax returns monthly, with returns due by the 20th of the month following the reporting period. This means January sales get reported by February 20th.

Electronic filing has become the standard method for Maryland sales tax compliance. The online system guides you through the process and provides confirmation of successful filing.

When you file sales tax returns, you'll report total sales, exempt sales, and taxable sales for the reporting period. The system calculates tax due based on the 6% rate applied to taxable transactions.

Use tax reporting often gets combined with sales tax returns. If you made purchases from out-of-state vendors without paying Maryland tax, you'll report and pay use tax on the same return.

Payment can be made electronically along with your return filing. Maryland encourages electronic filing and payment through slightly extended due dates for online submissions.

Record keeping requirements in Maryland are comprehensive. You need to maintain detailed records of all sales, exemption certificates, and tax collections for at least four years.

Sales for resale represent the most common exemption in Maryland. When you sell to other businesses for resale, you don't collect sales tax if you receive proper exemption certificates from your customers.

Exemption certificates must be completed properly and kept on file to support tax-free sales. Maryland provides standard forms for resale exemptions and other common exemption situations.

Manufacturing exemptions may apply to certain equipment and materials used in production. These exemptions can provide significant savings but require careful documentation and compliance with specific requirements.

Agricultural exemptions cover certain farm equipment and supplies used in qualifying agricultural activities. Farmers should review these provisions to ensure they're claiming appropriate exemptions.

Nonprofit organizations may qualify for sales tax exemptions, but they need to provide proper certificates and meet specific criteria. Not all nonprofit activities qualify for exemption.

Government entities typically receive exemptions from Maryland sales tax, but they need to provide appropriate documentation to support tax-free purchases.

Understanding when you need to collect sales tax in maryland depends on your nexus with the state. Physical nexus includes having employees, offices, inventory, or other business presence in Maryland.

Economic nexus rules require remote sellers to collect Maryland sales tax when they exceed certain thresholds of sales or transactions to Maryland customers. These rules apply even without physical presence in the state.

Marketplace sellers often discover nexus through third-party fulfillment arrangements or other business relationships within Maryland. Using fulfillment centers or having sales representatives can create nexus obligations.

Once you establish nexus in the state, you need to register for a sales tax permit in maryland and begin collecting tax on all taxable sales. The obligations are the same regardless of whether nexus is physical or economic.

Maryland law requires immediate registration once nexus is established. Delaying registration can result in penalties and back-tax assessments.

Maryland's use tax ensures the state collects revenue on purchases made outside Maryland for use within the state. The use tax rate matches the 6% sales tax rate.

Businesses owe use tax when they purchase items from out-of-state vendors who don't collect Maryland tax. This includes everything from office supplies to equipment purchases.

You can claim credit for taxes paid to other states, but only up to the amount that would be due in Maryland. If you paid less tax elsewhere, you owe the difference as Maryland use tax.

Many businesses overlook use tax obligations, but Maryland has increased enforcement efforts. Keeping detailed records of out-of-state purchases helps ensure compliance.

Consumer use tax returns may be required for individuals who make significant out-of-state purchases without paying Maryland tax. This ensures compliance across all taxpayer categories.

Modern point-of-sale systems can integrate with Maryland's tax requirements to ensure proper tax collection. Since Maryland has a uniform rate, integration is simpler than in states with varying local rates.

A maryland sales tax calculator helps verify exemption applications and ensures accurate tax collection on complex transactions. These tools become particularly useful for businesses with diverse product lines.

The Comptroller of Maryland provides online tools for registration, filing, and account management. Their system allows you to handle most tax-related activities through a single portal.

Automated compliance systems can handle maryland sales tax registration, ongoing filing requirements, and exemption certificate management. These tools reduce errors and save time on routine compliance activities.

Retail businesses need to understand food exemption rules and properly handle exemption certificates. Training staff on when items qualify for exemptions helps avoid compliance issues.

Restaurant and food service businesses must distinguish between taxable prepared food and exempt grocery items. The consumption location and preparation method often determine tax treatment.

Service businesses should review whether their activities fall under Maryland's taxable service categories. While Maryland taxes fewer services than many states, certain activities are specifically covered.

E-commerce businesses need systems that can properly apply Maryland tax to qualifying transactions while handling exemptions correctly. This includes understanding when customers qualify for resale exemptions.

Maryland's tax laws and regulations change periodically, making it important to stay current with updates. The Comptroller of Maryland publishes notices about rate changes and new requirements.

While Maryland's rate structure remains more stable than states with local variations, exemption rules and compliance procedures can change. Regular review ensures ongoing compliance.

Working with tax professionals familiar with Maryland requirements helps ensure you're staying current with all obligations. Professional guidance becomes particularly valuable for businesses with complex exemption situations.

What is the current Maryland sales tax rate for 2025?

Maryland has a uniform statewide sales tax rate of 6% that applies to all retail sales of taxable goods and services. Unlike many states, Maryland doesn't allow local jurisdictions to add additional sales taxes, so the rate is consistent throughout the state.

Do I need to collect Maryland sales tax if I only sell online?

Yes, if you meet Maryland's economic nexus requirements or have any physical presence in the state. Remote sellers must register and collect Maryland sales tax when they exceed certain sales thresholds to Maryland customers, even without physical locations in the state.

Are food items exempt from Maryland sales tax?

Most grocery or market food items purchased for consumption off the premises are exempt from Maryland sales tax. However, prepared foods, restaurant meals, and food consumed on the premises are generally taxable. Alcoholic beverages are typically taxable regardless of consumption location.

How often do I need to file Maryland sales tax returns?

Most businesses file monthly returns due by the 20th of the month following the reporting period. Some smaller businesses may qualify for quarterly filing based on their tax liability. The Comptroller of Maryland assigns your filing frequency when you register.

What exemption certificates do I need to keep on file?

You need to maintain proper exemption certificates for any sales where you don't collect tax, such as resale transactions, sales to nonprofits, or sales to government entities. Maryland provides standard exemption certificate forms, and you must keep these on file for at least four years.

Do I owe use tax on out-of-state purchases for my business?

Yes, you owe Maryland use tax on purchases from out-of-state vendors who don't collect Maryland sales tax. The use tax rate is 6%, matching the sales tax rate. You can claim credit for taxes paid to other states, but you owe the difference if you paid less than Maryland's rate.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.