.png)

You just sold your business for $5 million.

The capital gains tax bill? About $1.2 million. You could write that check to the IRS, or you could invest the full $5 million pre-tax into an opportunity zone and potentially eliminate taxes on future appreciation entirely.

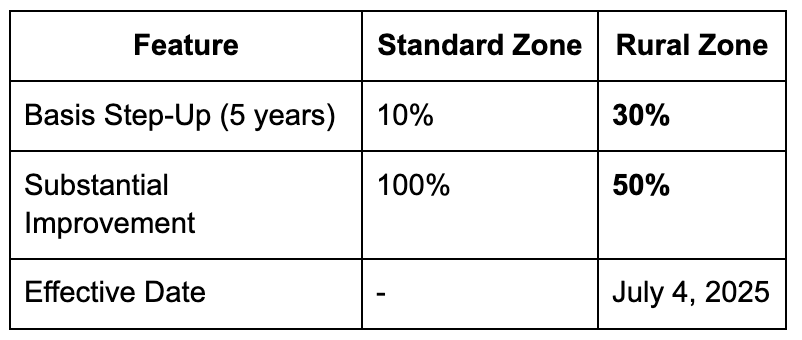

Opportunity zone tax benefits allow investors to defer capital gains taxes until December 31, 2026 by investing in Qualified Opportunity Funds, receive a 10% basis step-up after holding investments for 5 years (30% for rural zones), and pay zero taxes on appreciation if they hold investments for at least 10 years. The 2017 Tax Cuts and Jobs Act created this program to spur economic development in distressed communities, and the July 2025 One Big Beautiful Bill made it permanent with enhanced rural incentives.

What's New: On September 30, 2025, the IRS identified 3,309 rural opportunity zones that now qualify for triple the standard tax benefits.

If you're sitting on unrealized capital gains from stocks, real estate, or business sales, the math just shifted dramatically in your favor- but only if you understand the new rules and move within the 180-day investment window.

This guide explains the three-tier tax benefit structure, how the 2025 legislation transformed rural zone investing, which capital gains qualify, and the compliance requirements that determine whether you keep or lose these substantial tax advantages.

Opportunity zone tax benefits provide three distinct tax advantages for investors who reinvest capital gains into designated economically distressed communities through Qualified Opportunity Funds. These benefits work as a package:

The mechanics are straightforward but precise. When you sell an appreciated asset and realize a capital gain, you normally pay taxes on that gain in the same tax year. Opportunity zones flip this script. Instead of paying taxes immediately, you invest that gain amount into a Qualified Opportunity Fund within 180 days. You file an election with your tax return to defer the gain, and the taxes get pushed to December 31, 2026, or whenever you sell the QOF investment, whichever comes first.

Here's the critical distinction: you're not eliminating tax on the original gain initially (though you will reduce it through the basis step-up). You're deferring it while your investment grows tax-free. The real power of opportunity zone tax benefits comes from what happens during that deferral period and after 10 years of holding.

The Treasury Department designated 8,764 Qualified Opportunity Zones across all 50 states, Washington D.C., and U.S. territories in 2018 based on governor nominations. These are census tracts, specific geographic areas identified by 11-digit codes, that qualified as economically distressed based on income and poverty metrics.

You can verify whether a property sits in an opportunity zone using the IRS geocoder tool or checking IRS Notices 2018-48 and 2019-42.

A Qualified Opportunity Fund (QOF) is the investment vehicle that makes opportunity zone tax benefits accessible. It's an investment entity organized as a corporation or partnership that files either Form 1120 or Form 1065, and it self-certifies by filing Form 8996 with its tax return.

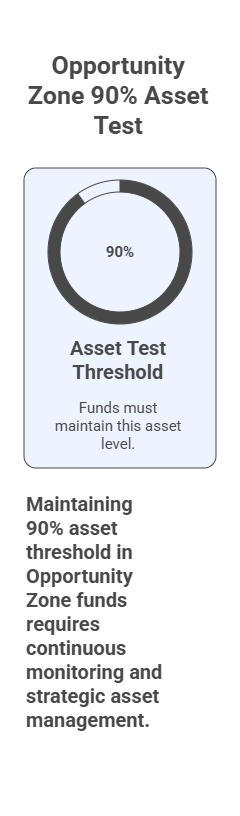

The QOF must hold at least 90% of its assets in qualified opportunity zone property, tested twice annually:

If it fails the 90% test, the fund pays a monthly penalty equal to the underage multiplied by the underpayment rate under IRC Section 6621 until compliance is restored.

This 90% asset test is where many funds stumble. The requirement demands continuous monitoring and strategic asset management. A QOF must invest capital quickly enough to maintain the threshold while also ensuring investments meet the qualified property standards. Working capital safe harbor provisions provide some flexibility, allowing funds to hold cash temporarily while pursuing investments, but these provisions have strict timing requirements and documentation standards.

What counts as qualified opportunity zone property? It includes:

The "original use" requirement means either you're the first person to use the property in the zone, or you're making substantial improvements that essentially create new property for tax purposes.

"Substantially improved" has a specific meaning critical to maximizing opportunity zone tax benefits: you must invest in improvements at least equal to your adjusted basis in the property within 30 months of acquisition.

Example: If you buy a building for $3 million and your adjusted basis is $2.5 million, you need to invest at least $2.5 million in improvements. The land isn't counted in this calculation, only the building. This substantial improvement requirement ensures that opportunity zone investments create real economic activity and development, not just passive ownership transfers.

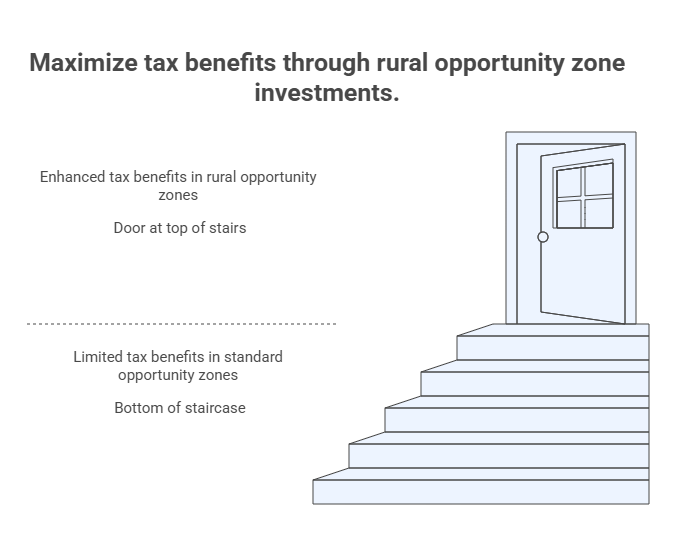

Rural Zone Advantage: For rural zones, this requirement drops to just 50% of adjusted basis, making renovation projects far more financially viable.

This change has opened up numerous rehabilitation opportunities in small towns and rural areas where the economics of 100% improvement ratios were prohibitive.

The One Big Beautiful Bill Act, signed into law on July 4, 2025, permanently extended the opportunity zone program and introduced Qualified Rural Opportunity Funds with enhanced tax benefits that triple the standard basis step-up. This legislation fundamentally changed opportunity zone tax benefits from a temporary tax break expiring in 2026 to a permanent wealth-building tool with even more powerful incentives for rural investments.

The permanence matters enormously for long-term planning. Originally, the opportunity zone program was set to sunset after December 31, 2026, with no mechanism for extending zone designations or continuing benefits beyond existing investments. Investors faced uncertainty about whether their long-term investments would maintain favorable treatment, creating hesitation around the critical 10-year holding period required for full appreciation exclusion.

The new law eliminated that uncertainty and created a rolling 10-year designation cycle, ensuring opportunity zones remain a reliable component of tax strategy indefinitely.

Here's what changed specifically for all opportunity zones under the new framework:

The rural opportunity zone provisions are where opportunity zone tax benefits became dramatically more attractive. Treasury identified 3,309 census tracts, representing 38% of all opportunity zones, as entirely rural based on a specific definition: any area that isn't in a city or town with population greater than 50,000, and isn't in an urbanized area adjacent to such a city or town.

Investments in these rural zones through Qualified Rural Opportunity Funds receive three times the standard basis step-up: 30% after five years instead of 10%.

Let's put numbers to these enhanced opportunity zone tax benefits:

At the current 23.8% federal capital gains rate (20% long-term capital gains plus 3.8% Net Investment Income Tax), you're looking at an additional $95,200 in tax savings just from that enhanced basis step-up.

When you combine this with the eventual appreciation exclusion, the total opportunity zone tax benefits can exceed several hundred thousand dollars on a single investment.

The substantial improvement requirement also got easier for rural zones, amplifying the practical application of these opportunity zone tax benefits:

Example: If you buy a $4 million building with $3 million adjusted basis:

This change took effect immediately on July 4, 2025, making rural rehabilitation projects financially feasible where they weren't before.

The legislation also established the new designation cycle that will keep opportunity zone tax benefits relevant for decades:

Timeline:

This creates fresh opportunities while potentially removing designation from zones that have improved economically and no longer need incentives.

New reporting requirements came with these enhancements to ensure opportunity zone tax benefits serve their intended purpose:

QOF Requirements:

Penalties:

Understanding eligible gains is crucial to accessing opportunity zone tax benefits.

Capital Gains:

Section 1231 Gains:

✓ Must be recognized for federal income tax purposes before January 1, 2027

✓ Cannot be from transactions with related persons

✓ Can defer all or part of the eligible gain

The distinction between gain and proceeds trips up many investors exploring opportunity zone tax benefits.

Example:

You don't have to invest the full $1 million in proceeds. You could invest just $300,000 of the gain and pay taxes on the other $300,000 normally, giving you flexibility in how much exposure you want to opportunity zones versus other investments. This partial gain election allows sophisticated investors to balance opportunity zone tax benefits against portfolio diversification and liquidity needs.

Both short-term and long-term capital gains qualify for opportunity zone tax benefits, though the timing implications differ significantly:

Section 1231 gains from business property create additional opportunities for opportunity zone tax benefits. These gains come from selling depreciable property or real property used in your trade or business for more than one year. Because Section 1231 gains receive long-term capital gains treatment when gains exceed losses for the year, they fit seamlessly into the opportunity zone framework.

The 180-day deadline is perhaps the most important technical requirement for claiming opportunity zone tax benefits.

The clock starts ticking on the date you realize the capital gain, not when you receive proceeds:

⚠️ WARNING: Missing the 180-day deadline means permanently losing access to opportunity zone tax benefits for that specific gain. There are no extensions, no do-overs, and no hardship exceptions.

Pass-through entities offer extended investment windows that can maximize opportunity zone tax benefits. If you own an S corporation or partnership interest and that entity realizes a gain, you can choose between two 180-day periods:

For calendar-year entities recognizing gains early in the year, this provision could extend your investment window by nearly a full year, providing substantial additional time to identify and vet optimal opportunity zone investments.

Opportunity zone tax benefits offer three primary advantages working in combination:

Example: For a $1 million investment that doubles in value over 10 years, you'd pay zero capital gains tax on that $1 million gain. This combination creates a powerful wealth-building mechanism that's unmatched by most other tax incentive programs.

The July 2025 legislation transformed opportunity zone tax benefits in four major ways:

These changes significantly increase the program's long-term value and accessibility for investors.

You have exactly 180 days from the date you realize a capital gain to invest that gain into a Qualified Opportunity Fund and defer the tax. The clock starts on the date the gain would normally be recognized for federal income tax purposes.

Example: If you sell stock on March 15, 2025, you have until September 11, 2025 to invest in a QOF.

Missing this deadline means losing the tax deferral benefit permanently for that specific gain. For pass-through entities, special rules may extend this window to the last day of the entity's taxable year, potentially providing additional time to access opportunity zone tax benefits.

Yes. Nonresident aliens and foreign corporations can elect to defer eligible capital gains through opportunity zone investments if those gains are otherwise subject to U.S. federal income tax. This includes:

Foreign investors must waive any applicable income tax treaty benefits to participate in the program. The opportunity zone tax benefits for foreign investors operate identically to domestic investors, making this one of the few U.S. tax incentive programs fully accessible to international capital.

Eligible gains for opportunity zone tax benefits include:

Capital Gains:

Section 1231 Gains:

Requirements:

Qualified Rural Opportunity Funds investing in the 3,309 designated rural opportunity zones receive significantly enhanced opportunity zone tax benefits:

Real Impact:

For a $2 million deferred gain, that's the difference between $200,000 and $600,000 excluded from taxation, representing an additional $95,200 in tax savings at current capital gains rates. The reduced improvement requirement makes rural real estate projects economically feasible in markets where construction costs would otherwise prevent development.

On January 1, 2027, a new round of opportunity zone designations takes effect based on governor nominations starting July 1, 2026.

Key Points:

This permanent structure ensures opportunity zone tax benefits remain a viable long-term wealth-building tool.

Opportunity zone tax benefits represent one of the most powerful wealth-building tools in the current tax code, but only if you understand how they actually work and avoid the common pitfalls that cost investors their benefits- or worse, their principal. The 2025 legislation transformed the program from a temporary incentive to a permanent fixture, with rural zones now offering triple the tax advantages of standard zones.

The math is compelling:

For the right investor with the right gains at the right time, opportunity zone tax benefits can save hundreds of thousands or even millions in taxes while building long-term wealth in communities that need capital and development.

Here's what matters most when pursuing opportunity zone tax benefits:

Understanding whether the complexity, illiquidity, and risk are worthwhile for your particular financial situation is essential.

Ready to explore whether opportunity zone tax benefits fit your tax strategy and financial goals? Understanding the mechanics is just the first step. The second is finding investments that make economic sense independent of the tax benefits, because favorable tax treatment can't rescue a poor underlying investment.

Let's discuss how you can access these substantial tax advantages while meeting all compliance requirements and building real wealth.

%2075-100%20(3).png)

How the foreign tax credit works on Form 1116: who files, the income baskets, the limitation, carryovers, credit vs deduction, and 2026 changes.

%2075-100%20(2).png)

How GILTI works on Form 8992, who files, the Section 250 deduction, foreign tax credits, and the 2026 switch to Net CFC Tested Income (NCTI).

%2075-100%20(1).png)

A plain guide to Form 5471 for US owners of foreign corporations: the five filer categories, which schedules you attach, penalties, and 2026 changes.