.png)

Every architecture firm operates in a project-driven world. Every design concept, master plan, or site evaluation is not just a creative endeavor—it is a financial unit with its own costs, timelines, and revenue streams. Unlike traditional accounting that looks at the business as a whole, project accounting gives an architecture firm a clear view into the financial health of individual projects and overall profitability.

This approach is not just useful, it is critical for effective financial management. Architecture firms that do not track project-level performance often struggle with cash flow shortages, underbilling, scope creep, and client disputes. As projects scale, these issues multiply and can significantly impact the firm's ability to maintain healthy cash flow and consistent profitability.

Understanding key performance indicators (KPIs) such as utilization rate, multiplier effectiveness, and direct labor costs is essential for any architect looking to build a sustainable practice. These metrics provide insight into both project-level and firm-wide financial health.

In this guide, we will break down the key components of project accounting for architecture firms. We will explain how to set up systems to track profitability, monitor essential KPIs, forecast performance, allocate costs correctly, and make more informed decisions. Whether you are a small studio or a growing mid-size practice, this article will help you implement a project-focused accounting approach that supports sustainable growth.

Project accounting is a financial management method that tracks the revenues, costs, and profitability of individual projects. It goes beyond general ledger accounting by attaching every transaction to a specific project code or cost center, enabling detailed analysis of each project's contribution to the firm's overall financial health.

For an architecture firm, this means every hour billed, invoice issued, software license used, subcontractor hired, or travel expense logged is categorized under the relevant project. This granular approach allows firms to calculate accurate KPIs such as utilization rate and multiplier for each project and team member.

The result is a detailed financial picture of each project's performance. You can see which projects are profitable, which ones are off-budget, and which clients or services generate the best profit margins. This data is essential for maintaining healthy cash flow and making strategic decisions about future work.

Architecture is a project-centric profession where effective project management directly impacts profitability. Traditional accounting reports cannot answer critical questions like:

Without project accounting, all income and costs are pooled, making it impossible to spot problems early or reward high-performing teams. This lack of visibility can severely impact cash flow and overall financial health.

Architecture firms that implement project accounting gain:

These benefits translate into higher profitability, reduced write-offs, better cash flow management, and improved client satisfaction.

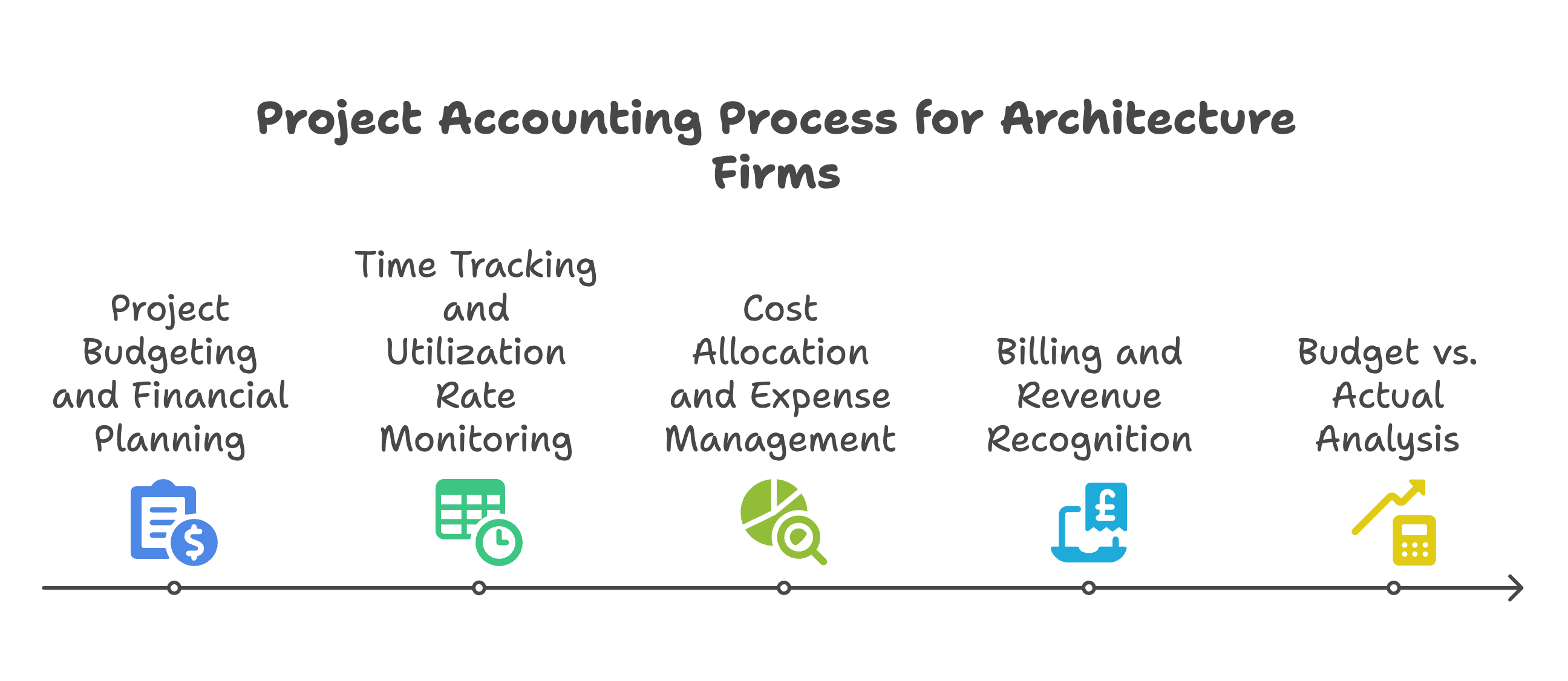

To successfully adopt project accounting, an architecture firm must break down their finances into project-level units. The system must capture the following components:

Every project needs a comprehensive financial plan that includes:

Budgets must be realistic and aligned with the scope of work. Successful architecture firms create detailed budgets using architectural phases such as Concept Design, Schematic Design, Design Development, Construction Documents, Bidding, and Construction Administration.

Employee timesheets must be recorded by project and, ideally, by phase or task. This data is essential for calculating utilization rate and other key KPIs. Effective time tracking allows the firm to:

Modern time-tracking tools such as Harvest, BigTime, or Deltek Ajera are designed specifically for project-based firms and can automatically calculate utilization rates and other important metrics.

Project-related expenses must be assigned to the right job to ensure accurate profitability analysis. Common direct costs include:

Indirect expenses, such as rent, utilities, or software subscriptions, can be allocated using overhead rates or applied based on direct labor hours. The multiplier approach helps ensure that indirect expenses are properly covered across all projects.

Billing methods vary by client and contract structure, and each approach has different implications for cash flow and financial health. Architecture firms typically use:

Each billing method requires different approaches to revenue recognition and cash flow management. Accurate tracking ensures you are billing for all services rendered and not leaving net revenue on the table.

At the heart of project accounting is the ability to compare what was planned versus what actually happened. This analysis is crucial for maintaining profitability and includes:

This analysis helps architecture firms detect problems early and take corrective action before profits evaporate.

Successful financial management requires monitoring specific KPIs that indicate the firm's performance and financial health:

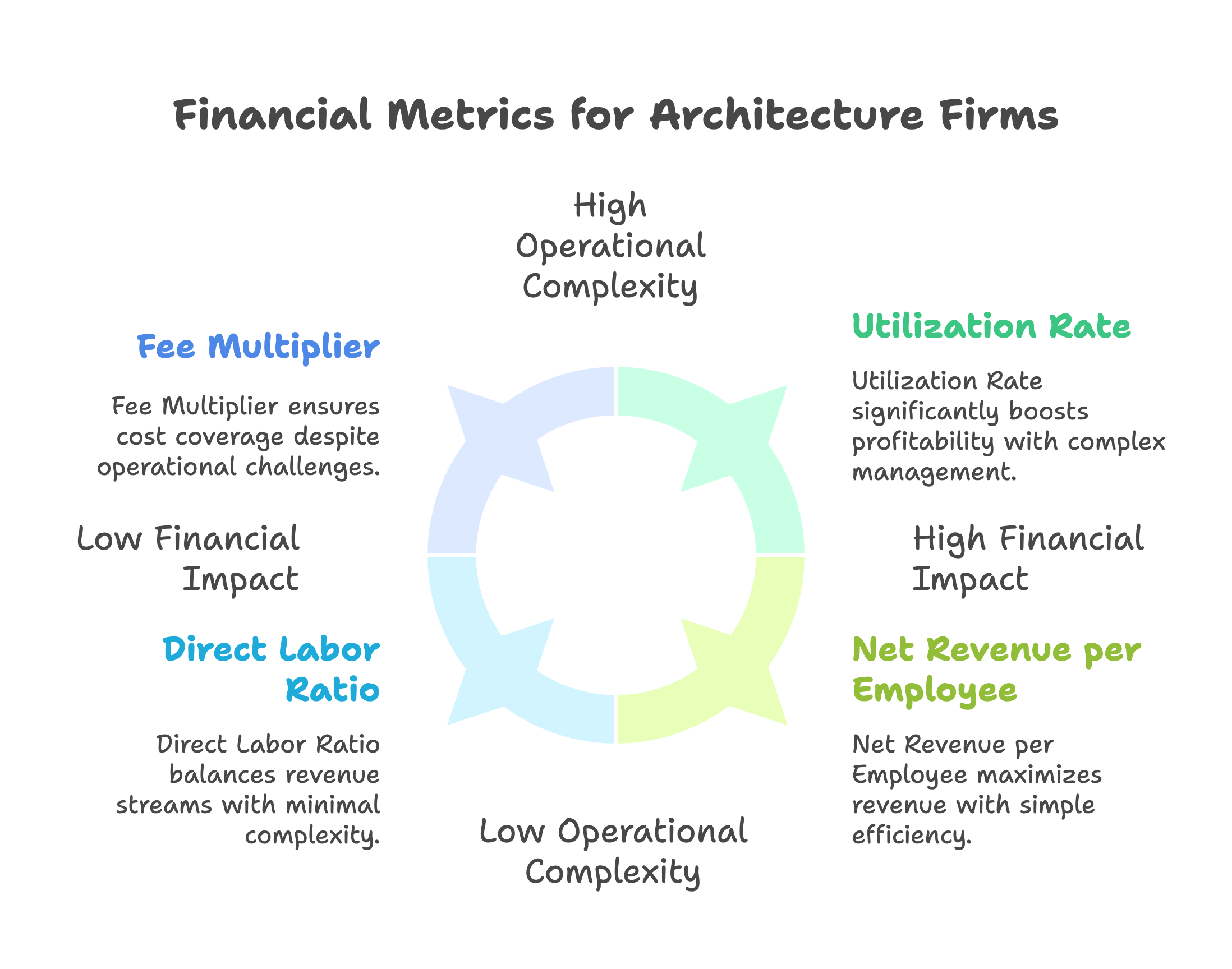

The utilization rate measures the percentage of an employee's time that is billable to projects. This is one of the most critical metrics for any architecture firm.

The multiplier indicates how much the firm charges for direct labor compared to the actual salary costs.

This metric shows what percentage of total revenue comes from direct labor versus other sources.

This KPI measures the firm's ability to generate revenue per team member.

Individual project profitability analysis is essential for understanding which types of work generate the best returns.

Cash flow management is particularly challenging for architecture firms due to the project-based nature of the business and varying payment terms. Effective cash flow management requires:

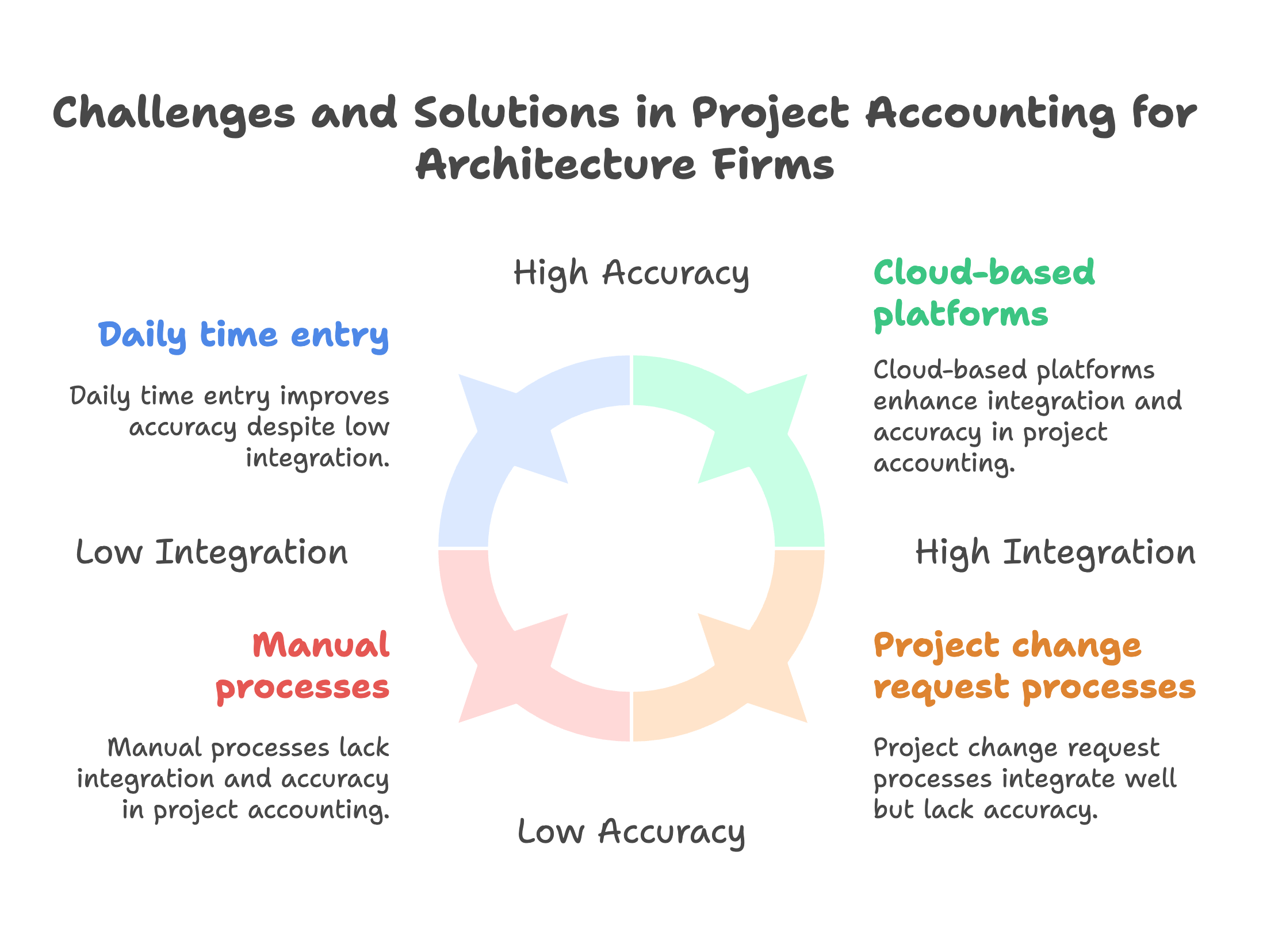

Despite the benefits, many architecture firms struggle with project accounting due to several common obstacles:

Time tracking, billing, accounting, and project management tools often operate in silos. Without integration, financial data becomes fragmented and difficult to reconcile, making it challenging to calculate accurate KPIs or maintain visibility into cash flow.

Solution: Use cloud-based platforms that integrate project management, time tracking, and accounting. Examples include Deltek, BQE Core, and Monograph.

When employees delay submitting timesheets or estimate their billable hours, data becomes unreliable. This impacts both billing accuracy and utilization rate calculations, ultimately affecting profitability analysis.

Solution: Encourage daily time entry and use mobile apps to make the process easier. Explain how accurate tracking benefits both the firm's financial health and employee development.

Clients often request additional work that falls outside the original scope. If not tracked and billed properly, this erodes profit margins and negatively impacts cash flow.

Solution: Set up project change request processes. Ensure that any out-of-scope work is logged, estimated, approved, and billed separately to maintain profitability.

Many architecture firms either do not budget projects properly or do so at too high a level. This prevents detailed analysis of utilization rates, multiplier effectiveness, and other crucial metrics.

Solution: Create budgets by phase and task. Base estimates on historical data and adjust based on team productivity, utilization rate trends, and specific project requirements.

Adopting project accounting is just the beginning. To drive real results, architecture firms must implement continuous improvement strategies:

Use consistent naming conventions and cost codes across projects. This makes it easier to compare performance, calculate accurate KPIs, and build benchmarks for future projects.

Create a regular cadence for reviewing budget vs. actual reports with project managers. Focus on:

Use these insights to adjust staffing, timelines, or client communication strategies.

Not all work is equally profitable. Some clients require more revisions, while certain project types have thin profit margins or challenging cash flow patterns.

Tag projects by client type, size, sector, and service line. Analyze trends in profitability, utilization rates, and cash flow to make better strategic decisions.

Streamline billing to improve cash flow and reduce administrative burden:

Project managers are responsible for outcomes but may not be comfortable with budgets, KPIs, or financial management concepts. Provide training on:

When project managers understand the financial impact of their decisions, they make better daily choices that support the firm's profitability and financial health.

Compare your firm's performance against industry standards and similar practices:

Use historical project data to model different business scenarios:

Evaluate your client base and project mix for optimal financial performance:

The right software stack can simplify project accounting and provide real-time visibility into KPIs and financial health. Look for the following features:

Deltek Ajera – Comprehensive platform tailored for AEC firms with robust project accounting and KPI tracking

BQE Core – Combines time tracking, billing, and accounting with strong financial reporting

Monograph – Designed specifically for architecture firms with clean UI and project planning features

Harvest – Simple time tracking and expense reporting with good integration options

FreshBooks – Entry-level option for smaller studios with basic project accounting features

Choose based on your architecture firm's size, budget, complexity of projects, and existing workflow requirements.

For architecture firms that want to focus on design rather than spreadsheets, partnering with a CPA firm or offshore accounting provider can streamline project accounting and financial management.

Outsourced teams can help with:

At Madras Accountancy, we work with CPA firms and directly with AEC clients to implement and maintain project accounting systems that are both accurate and efficient. With specialized teams trained in AIA billing, cost allocation, and time-based contracts, we provide support that drives profitability without adding in-house overhead.

Project accounting is not just a tool—it is a strategic advantage that enables architecture firms to thrive in a competitive market. Architecture firms that track revenue and costs at the project level, monitor essential KPIs like utilization rate and multiplier, and maintain strong cash flow management can:

Effective financial management requires commitment to tracking the right metrics, understanding what drives profitability, and maintaining healthy cash flow through all phases of business growth. The integration of project accounting with broader financial management practices creates a comprehensive view of the firm's performance.

For any architect serious about building a sustainable practice, implementing robust project accounting is essential. The visibility into direct labor costs, indirect expenses, utilization rates, and profit margins provides the foundation for making informed decisions that support both creative excellence and financial success.

For growing architecture firms seeking expert support, a CPA partner or offshore finance team can provide the structure, tools, and ongoing oversight needed to turn accounting into a profit-driving asset that supports the firm's creative mission while ensuring long-term financial health.

Question: What are the unique project accounting challenges that architecture firms face?

Answer: Architecture firms face unique project accounting challenges including tracking time across multiple project phases, managing complex fee structures, allocating overhead costs to projects, and handling change orders and scope modifications. Projects often span extended periods with varying staffing levels, multiple deliverables, and phased billing arrangements. Revenue recognition becomes complex with retainer structures, milestone payments, and percentage-of-completion considerations. Additional challenges include tracking reimbursable expenses, managing consultant costs, and allocating indirect costs like marketing, business development, and administrative support. Professional liability insurance, continuing education, and software licensing costs require proper allocation to projects. Accurate project accounting is essential for profitability analysis, pricing decisions, and client relationship management in competitive architectural markets.

Question: How should architecture firms set up their chart of accounts for effective project tracking?

Answer: Set up architecture firm chart of accounts with detailed project codes, phase tracking, expense categories, and revenue classification systems. Create hierarchical project codes identifying client, project type, project phase, and specific tasks or deliverables. Establish expense categories for direct labor, consultant costs, reimbursable expenses, and allocated overhead. Revenue accounts should distinguish between fee types including hourly services, fixed fees, and reimbursable costs. Implement cost centers for different departments or service lines while maintaining project-level detail. Consider integration with time tracking systems, project management software, and client billing platforms. Professional chart of accounts design enables accurate project profitability analysis, supports billing processes, and provides management reporting for strategic decision-making and operational improvements.

Question: What are the best practices for time tracking and labor cost allocation in architecture firms?

Answer: Best practices for architecture time tracking include using integrated software systems, requiring daily time entry, implementing project phase coding, and establishing clear guidelines for non-billable time allocation. Implement automated time tracking tools integrated with project management and accounting systems to reduce manual data entry and improve accuracy. Establish detailed project phase codes for concept design, design development, construction documents, and construction administration. Train staff on proper time allocation procedures, handling of administrative time, and project code usage. Include time for project management, client communication, and quality review in project budgets and tracking. Regular time entry reviews, variance analysis, and utilization reporting help identify trends and optimization opportunities. Professional time tracking enables accurate project costing, billing accuracy, and profitability analysis essential for architectural practice management.

Question: How can architecture firms track and allocate overhead costs to projects accurately?

Answer: Track and allocate overhead costs to architecture projects through systematic allocation methods based on direct labor, project revenue, or square footage utilization. Common overhead costs include rent, utilities, insurance, marketing, administrative staff, and technology expenses. Establish allocation bases that reflect actual overhead consumption by projects - direct labor hours often work well for labor-intensive services while square footage may be appropriate for space-related costs. Calculate overhead rates regularly, typically monthly or quarterly, and apply consistently across all projects. Track overhead by cost center or department to improve allocation accuracy and identify cost management opportunities. Consider activity-based costing for complex firms with diverse service offerings. Professional overhead allocation ensures accurate project profitability analysis and supports pricing decisions for future projects.

Question: What financial metrics and KPIs should architecture firms monitor for project profitability?

Answer: Key financial metrics for architecture project profitability include gross margin by project and phase, utilization rates by staff level, project budget variance analysis, and collection rates by client type. Monitor metrics including project profitability percentages, average hourly rates achieved, project duration versus estimates, and scope change impact analysis. Track key performance indicators covering new project win rates, project pipeline value, client satisfaction scores, and repeat business percentages. Additional metrics include overhead allocation accuracy, reimbursable expense recovery rates, and cash flow timing by project type. Benchmark metrics against industry standards and historical performance to identify trends and improvement opportunities. Regular monitoring enables proactive project management, pricing optimization, and strategic planning for sustainable profitability in architectural practice.

Question: How should architecture firms handle change orders and scope modifications in project accounting?

Answer: Handle architecture project change orders through systematic documentation, approval processes, cost tracking, and revenue recognition procedures. Establish clear change order procedures including client authorization requirements, scope documentation, and fee calculation methods. Track change order costs separately from original project budgets to maintain accurate profitability analysis. Implement approval workflows for internal change authorization and client communication. Consider impacts on project schedules, resource allocation, and overall profitability when evaluating change requests. Document all scope modifications, fee adjustments, and timeline impacts for billing and legal protection. Use project management software to track change order status and integration with financial systems. Professional change order management protects firm interests while maintaining positive client relationships through transparent communication and fair pricing practices.

Question: What technology solutions support effective project accounting for architecture firms?Answer: Technology solutions for architecture project accounting include integrated practice management software, time tracking applications, project management platforms, and financial reporting systems. Popular solutions include BQE CORE, Deltek Vision, ArchOffice, and specialized time tracking tools like Toggl or Harvest. Seek platforms offering project budgeting, time tracking, expense management, billing integration, and financial reporting capabilities. Consider integration with CAD software, document management systems, and client communication platforms. Mobile capabilities enable real-time time entry and expense tracking while cloud-based solutions provide accessibility and collaboration benefits. Evaluate features including project templates, automated workflows, custom reporting, and integration with QuickBooks or other accounting software. Professional technology selection should consider firm size, complexity, budget, and growth plans for optimal return on investment.

Question: How can architecture firms improve their project profitability through better accounting practices?

Answer: Improve architecture project profitability through accurate project budgeting, regular variance analysis, improved time tracking procedures, and strategic pricing decisions based on historical data. Implement systematic project review processes, cost allocation accuracy improvements, and overhead management initiatives. Use historical project data for more accurate future project estimates, pricing strategies, and resource planning. Establish project management procedures that identify and address profitability issues early in project lifecycles. Improve billing processes, collection procedures, and client communication to optimize cash flow and reduce project cycle times. Consider value-based pricing alternatives to hourly billing where appropriate. Professional analysis of project profitability patterns helps identify service lines, client types, and project characteristics that generate optimal returns while enabling strategic business

Question: What are the consequences of not reporting income without 1099 forms?

Answer: Consequences of not reporting income without 1099 forms include substantial failure-to-pay penalties (0.5% per month), failure-to-file penalties (5% per month up to 25%), accuracy-related penalties (20% of underpayment), and potential fraud penalties (75% of underpayment) for willful non-reporting. The IRS can assess taxes, penalties, and interest going back three years for substantial underreporting or six years for significant omissions over 25% of reported income. Additional consequences include potential criminal prosecution for tax evasion, liens and levies on assets, and damaged credit from tax collection actions. Self-employment tax penalties also apply to unreported self-employment income. Voluntary disclosure before IRS discovery often results in reduced penalties compared to enforcement actions after audit or investigation.

Question: How can self-employed taxpayers estimate taxes owed on unreported 1099 income?

Answer: Estimate taxes on unreported 1099 income by calculating both income tax and self-employment tax obligations using current tax rates and brackets. Self-employment tax equals 15.3% (12.4% Social Security + 2.9% Medicare) on net earnings from self-employment over $400. Income tax rates depend on total income and filing status, ranging from 10% to 37% for federal taxes plus applicable state rates. Use tax software or professional assistance to calculate accurate estimates considering deductible business expenses, other income sources, and available tax credits. Make quarterly estimated payments if expecting to owe $1,000 or more to avoid underpayment penalties. Consider both current year obligations and potential amended return requirements for prior years with unreported income.

Question: What business expenses can be deducted against unreported 1099 income?

Answer: Business expenses deductible against unreported 1099 income include ordinary and necessary costs directly related to earning that income such as supplies, equipment, professional services, marketing costs, travel expenses, and home office deductions. Common deductions cover business insurance, professional development, licensing fees, equipment purchases or depreciation, and vehicle expenses for business use. Maintain detailed records linking expenses to income-generating activities, keep receipts and documentation, and ensure expenses meet IRS requirements for business necessity and reasonableness. The same expense documentation standards apply whether or not you receive 1099 forms. Proper expense deductions reduce net self-employment income subject to both income tax and self-employment tax, providing significant tax savings for legitimate business costs.

Question: Should self-employed taxpayers contact clients who failed to issue required 1099 forms?

Answer: Self-employed taxpayers should consider contacting clients who failed to issue required 1099 forms, as this may help with tax compliance and documentation while potentially prompting clients to issue missing forms or correct their own reporting. However, the primary responsibility for accurate income reporting remains with taxpayers regardless of client compliance with 1099 requirements. Document your efforts to obtain missing 1099 forms for potential penalty relief arguments if questioned by the IRS. Some clients may be unaware of 1099 requirements or may have issued forms to incorrect addresses. Professional consultation helps determine appropriate actions for specific situations while ensuring your own compliance obligations are met properly.

Question: How does the IRS detect unreported income without 1099 forms?

Answer: The IRS detects unreported income through bank deposit analysis, lifestyle audits, third-party information matching, cash transaction reporting, and document matching programs that compare reported income to various information sources. Bank deposit analysis compares reported income to total deposits, identifying potential unreported amounts requiring explanation. Lifestyle audits examine living expenses relative to reported income to identify discrepancies suggesting unreported income. Payment processors like PayPal and Venmo report transaction information that the IRS matches against tax returns. Cash-intensive businesses face additional scrutiny through informant reports and industry-specific audit programs. Modern technology and data analytics enable sophisticated income detection methods that make unreported income increasingly difficult to hide from IRS enforcement efforts.

Question: What steps should taxpayers take if they discover previously unreported income without 1099 forms?

Answer: Taxpayers discovering previously unreported income should file amended returns (Form 1040X) for affected years, calculate additional taxes and penalties owed, and consider voluntary disclosure to minimize penalties before IRS discovery. Gather documentation supporting the unreported income and any related business expenses, calculate accurate tax obligations including self-employment taxes, and file amended returns promptly after discovery. Consider professional assistance for complex situations, multiple years, or significant amounts. Pay additional taxes owed as quickly as possible to minimize interest charges. Voluntary disclosure often results in reduced penalties compared to IRS enforcement actions. Maintain detailed records of the amendment process and communications with tax authorities throughout the resolution process.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.