.png)

Claiming the R&D tax credit can provide substantial tax savings for your business, but getting it wrong can trigger costly audits and penalties. The Internal Revenue Service has specific documentation requirements that you must meet to substantiate your research credit claim, and these requirements are more detailed than many business owners realize.

If you're thinking about claiming the R&D credit or you've already been claiming it, understanding what documentation the IRS expects can make the difference between a smooth audit experience and a nightmare that drags on for years. The good news is that proper documentation isn't complicated when you know what's required, but it does require systematic record-keeping throughout the year.

The IRS requires comprehensive documentation to support any research credit claim because the R&D credit represents significant tax savings that require careful substantiation. Under Section 41 of the Internal Revenue Code, businesses must maintain detailed records that demonstrate their qualified research activities and expenses meet all statutory requirements.

The documentation serves multiple purposes: it supports your credit calculation, demonstrates compliance with IRS regulations, and provides evidence needed during audits or examinations. Without proper documentation, the IRS can disallow your entire credit claim, potentially resulting in additional taxes, penalties, and interest charges.

The key principle is that your documentation must tell a complete story about your research activities, from the business purpose and technical challenges through to the specific individuals involved and expenses incurred. This comprehensive approach ensures you can defend your credit claim effectively.

The IRS requires you to identify all research activities performed during the tax year and maintain records that clearly describe each project or initiative. This documentation must demonstrate that your activities meet the four-part test for qualified research under Section 41.

Your records should include project descriptions that explain the business purpose, technical uncertainties being addressed, and the process of experimentation used to resolve those uncertainties. The documentation should be detailed enough that an IRS agent can understand what you were trying to accomplish and why traditional methods were inadequate.

Project timelines, meeting notes, technical specifications, and progress reports all serve as valuable supporting documentation. The goal is creating a paper trail that demonstrates legitimate research activities rather than routine business operations or ordinary problem-solving.

One of the most critical aspects of R&D tax credit documentation involves tracking the individuals who performed each research activity and documenting their time allocation. The IRS wants to see detailed records showing which employees participated in qualified research activities and what percentage of their time was dedicated to these activities.

Time tracking doesn't necessarily require minute-by-minute logs, but you need reliable methods for determining how much time each person spent on qualified research versus other activities. Many companies use timesheets, project management software, or periodic surveys to capture this information.

The documentation should identify specific employees by name and role, describe their research-related responsibilities, and provide reasonable estimates of time allocation. General statements or broad assumptions typically won't satisfy IRS scrutiny during examinations.

Qualified research expenses must be thoroughly documented with supporting financial records that tie directly to your research activities. This includes wages for employees performing research, supplies consumed in research activities, and contract research expenses paid to third parties.

For wage expenses, you need payroll records that support the time allocation documentation mentioned above. The IRS wants to see the connection between personnel involved in research and the actual compensation paid for their research-related work.

Supply expenses require documentation showing what materials were purchased, how they were used in research activities, and that they were consumed rather than remaining in inventory. Contract research expenses need agreements that clearly establish the research nature of the work and payments that can be traced to qualified activities.

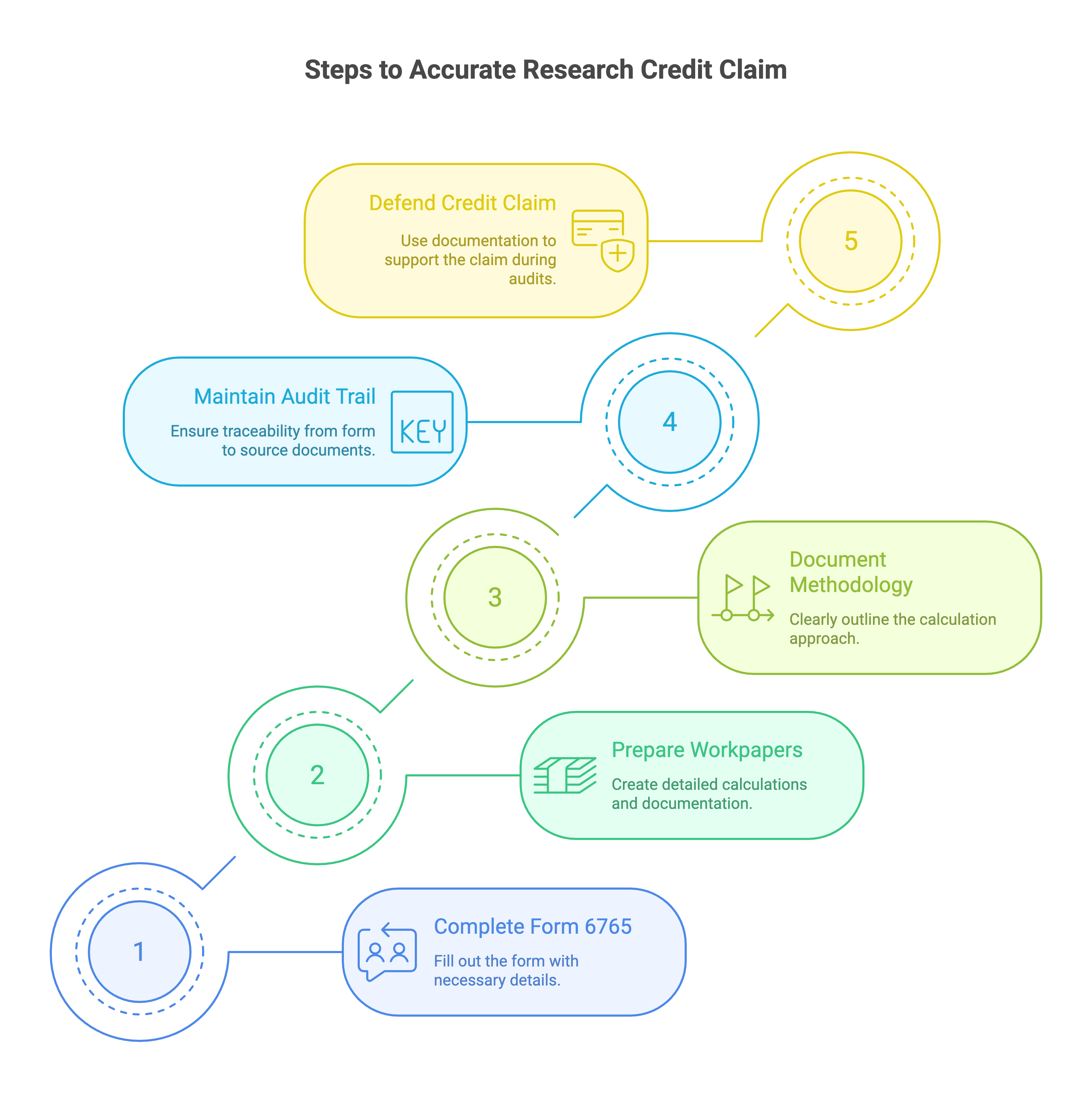

Form 6765 is the vehicle for claiming the research credit, and proper completion requires detailed supporting calculations and documentation. The form requires specific information about your research expenses and credit calculation methodology that must be supported by your underlying records.

The IRS expects your Form 6765 to be supported by detailed workpapers showing how you calculated each component of the credit. This includes base period calculations for the traditional method or alternative simplified credit calculations if you chose that approach.

Your supporting documentation should enable an IRS examiner to trace from your Form 6765 through your calculations back to the underlying source documents. This audit trail is essential for defending your credit claim during examinations.

The research credit calculation involves complex computations that require detailed documentation of your methodology and underlying assumptions. Whether you're using the traditional method or the alternative simplified credit, your approach must be clearly documented and consistently applied.

For companies claiming significant credits, consider preparing detailed memoranda explaining your calculation methodology, key assumptions, and how you addressed any gray areas or interpretational issues. This proactive documentation demonstrates good faith compliance efforts.

Keep detailed spreadsheets or workpapers showing your calculations, including any adjustments made for non-qualifying activities or expenses. These supporting schedules become crucial evidence during IRS examinations.

Technology companies face unique documentation challenges because software development activities often blur the lines between qualified research and routine development work. The IRS scrutinizes these claims carefully, making comprehensive documentation even more important.

Document your development process, including technical challenges encountered, alternative approaches considered, and experimentation performed to resolve uncertainties. User requirements, technical specifications, testing protocols, and code review processes all provide valuable supporting evidence.

Be particularly careful to distinguish between qualified research activities and routine debugging, maintenance, or adaptation of existing software. The documentation should clearly demonstrate genuine technological innovation rather than ordinary business activities.

Manufacturing companies claiming the R&D credit must document the development or improvement of products, processes, or formulas. This requires detailed records of design changes, testing procedures, and the business reasons driving development activities.

Maintain records of prototypes, test results, design iterations, and failed experiments. The IRS recognizes that research activities don't always succeed, so documentation of unsuccessful approaches can actually strengthen your credit claim by demonstrating genuine experimentation.

Engineering drawings, test reports, quality control data, and production records all serve as valuable supporting documentation for manufacturing-related research activities.

Service companies can qualify for the R&D credit when developing new or improved business processes, but documentation requirements focus on demonstrating genuine innovation rather than routine business improvements.

Document the technical challenges you were trying to solve, alternative approaches considered, and systematic experimentation used to develop solutions. Process flowcharts, efficiency studies, and performance metrics can provide valuable supporting evidence.

Be prepared to demonstrate that your activities involved technological innovation rather than simple business process reengineering or cost reduction initiatives that don't qualify for the credit.

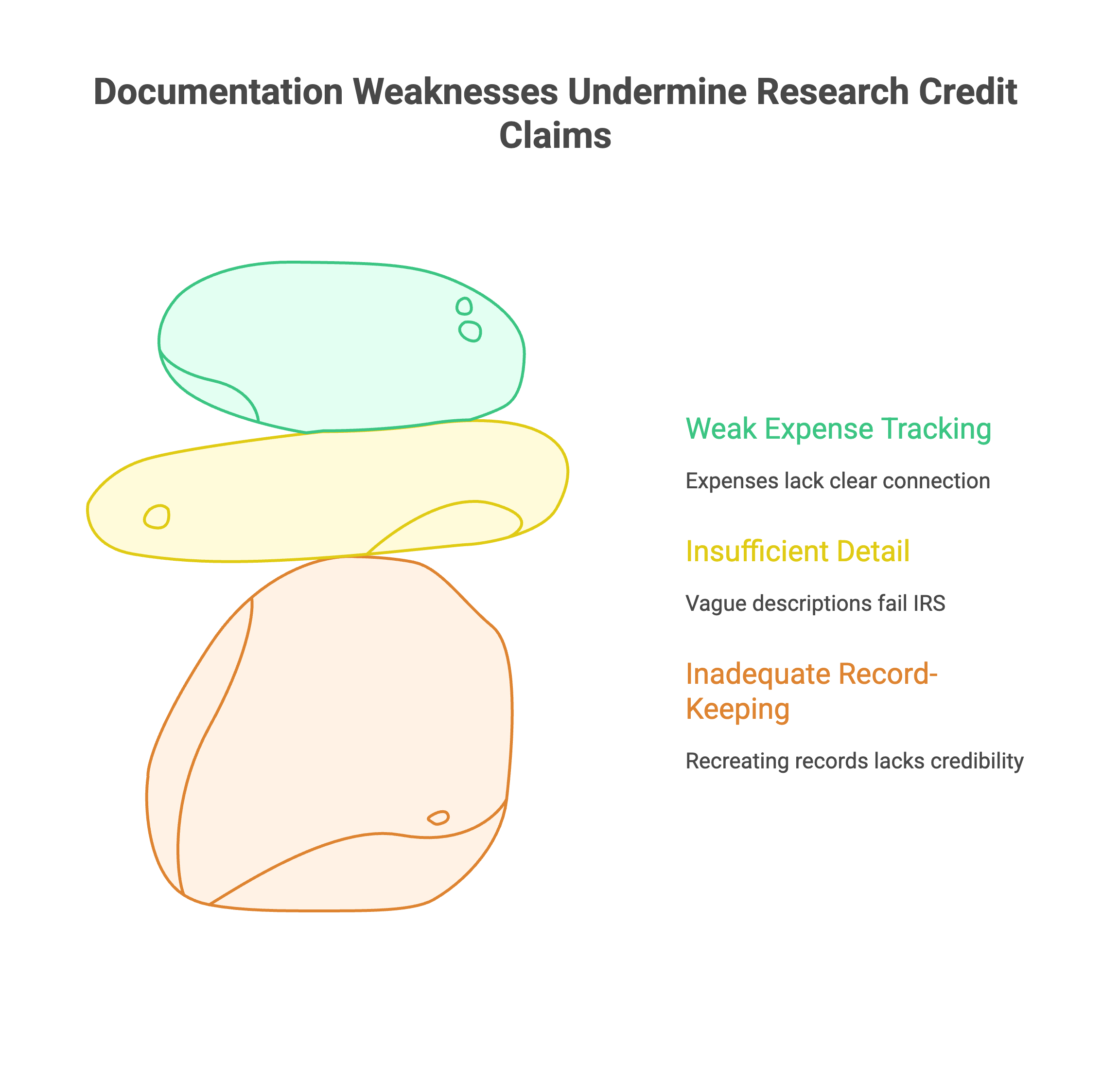

One of the most common mistakes is attempting to recreate documentation after the fact, particularly when facing an IRS examination. The IRS gives much more weight to contemporaneous records created during the research activities than to reconstructed documentation.

Establish systems for capturing research-related information as it occurs rather than trying to piece together records later. Project management software, electronic timesheets, and regular progress reporting can help create the contemporary documentation the IRS expects.

Train your staff to understand the importance of maintaining detailed records during research activities. The time invested in proper documentation during the research phase pays dividends if you face an IRS examination later.

Many businesses provide overly general descriptions of their research activities that don't demonstrate the specific technical challenges or experimentation performed. The IRS needs detailed information to evaluate whether activities truly qualify for the credit.

Avoid boilerplate language or generic descriptions that could apply to any business activity. Instead, provide specific details about the technical problems you were solving, why existing solutions were inadequate, and what systematic approach you used to develop solutions.

Consider having technical staff involved in preparing activity descriptions to ensure accuracy and appropriate level of detail. Their firsthand knowledge of the research activities often provides the specificity the IRS requires.

Simply showing that you incurred expenses isn't sufficient; you must demonstrate that those expenses relate specifically to qualified research activities. This requires clear connections between your financial records and your research activity documentation.

Implement chart of accounts structures that facilitate tracking of research-related expenses separately from other business costs. This segregation makes it easier to support your credit calculations and respond to IRS inquiries.

Regularly reconcile your research expense tracking with your general ledger to ensure consistency and identify any potential issues before they become problems during an examination.

If the IRS selects your R&D credit claim for examination, having well-organized documentation can significantly impact the audit experience. Create systems that allow you to quickly locate and present supporting records for any aspect of your credit claim.

Consider preparing an audit file that includes your key supporting documentation, organized by tax year and research project. This preparation demonstrates professionalism and can help expedite the examination process.

Maintain multiple copies of critical documentation and ensure that key personnel who can explain your research activities and documentation are available to assist during examinations.

R&D credit examinations are technically complex and require expertise in both tax law and the underlying technology or processes being examined. Consider engaging experienced tax professionals who specialize in research credit issues.

Your documentation should be organized in a way that enables your representatives to effectively present your case to IRS examiners. This includes clear executive summaries, detailed supporting schedules, and easy access to underlying source documents.

Maintain open communication with your tax advisors throughout the examination process and be prepared to provide additional documentation or clarification as requested by the IRS.

What specific documentation does the IRS require for R&D tax credit claims?

The IRS requires detailed records of research activities performed, individuals involved and their time allocation, qualified research expenses with supporting financial records, project descriptions demonstrating the four-part test, and comprehensive calculations supporting Form 6765.

How detailed should time tracking be for R&D credit documentation requirements?

Time tracking should identify specific employees by name, their roles in research activities, and reasonable estimates of time spent on qualified research. While minute-by-minute logs aren't required, you need reliable methods like timesheets, project management software, or periodic surveys.

What happens if I can't provide adequate documentation during an IRS audit?

Inadequate documentation can result in complete disallowance of your R&D credit claim, leading to additional taxes, penalties, and interest. The IRS places the burden of proof on taxpayers to substantiate their credit claims with proper documentation.

Can I recreate missing documentation after receiving an IRS audit notice?

While you can supplement existing records, the IRS gives much more weight to contemporaneous documentation created during the research activities. Reconstructed records after an audit notice are viewed skeptically and may not be accepted as adequate support.

How long should I retain R&D tax credit documentation?

Keep R&D credit documentation for at least six years after filing the return claiming the credit. For amended returns claiming refunds, the statute of limitations may be longer, so consider retaining records indefinitely for significant credit claims.

What types of expenses require the most detailed documentation?

Contract research expenses and supply costs typically require the most detailed documentation because they're more susceptible to challenge. You must demonstrate clear connections between these expenses and qualified research activities, including consumption rather than inventory retention for supplies.

How should software companies document R&D activities differently?

Software companies should focus on documenting technical uncertainties, experimentation processes, and genuine innovation versus routine development. Include technical specifications, testing protocols, alternative approaches considered, and clear distinctions between qualifying research and ordinary debugging or maintenance.

What documentation is needed for the four-part test under Section 41?

Document business purpose, technical information used in business, elimination of uncertainty through experimentation, and technological in nature. Each research project should have records demonstrating all four elements, including specific technical challenges and systematic approaches to resolution.

Proper R&D tax credit documentation isn't just about satisfying IRS requirements; it's about building a defensible case that protects your valuable tax benefits. The time and effort invested in maintaining comprehensive, contemporaneous records pays significant dividends by reducing audit risk and ensuring you can successfully defend your credit claims. Remember that documentation requirements are ongoing obligations, not something you can address retroactively, so establish robust systems from the beginning of your research activities.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.