You just collected rent from your fourth tenant this month. The money hit your personal checking account along with your paycheck, grocery receipts are scattered across your kitchen counter, and you're not sure if that $450 repair bill counts as maintenance or a capital improvement. Tax season is 90 days away.

Rental property accounting organizes every financial transaction tied to your properties so you can track rental income accurately, claim every legitimate deduction, and avoid IRS penalties. Whether you manage one duplex or ten single-family homes, proper accounting separates profitable landlords from those who overpay taxes by thousands each year.

This guide shows you exactly how to set up rental accounting systems, choose the right software, avoid costly mistakes, and build financial records that support portfolio growth. No accounting degree required, just practical steps you can implement this week.

Rental property accounting tracks and manages all financial activities related to your rental properties, including rent payments, operating expenses, maintenance costs, and tax obligations. Unlike personal finance tracking, rental accounting requires separate books for each property, proper expense categorization for IRS reporting, and documentation that supports deductions during audits.

This specialized bookkeeping handles unique landlord scenarios most businesses never face: security deposits that aren't income until forfeited, depreciation deductions spanning 27.5 years, and 1031 exchanges that defer capital gains taxes indefinitely. Each rental generates multiple income streams (rent, late fees, pet fees, parking) and dozens of expense categories (repairs, property management, insurance, utilities) that need separate tracking.

The numbers reveal whether your properties generate positive cash flow or drain resources. Accurate records support loan applications, justify rent increases to tenants, and become essential evidence if the IRS questions your Schedule E deductions. Most landlords who struggle financially can trace problems back to poor accounting practices, they simply don't know where their money goes.

Proper rental accounting transforms raw transaction data into actionable intelligence for your investment decisions.

Tax Savings You Can Actually Claim: The average landlord with three properties loses $2,500-$4,000 annually in unclaimed deductions simply because they lack proper documentation. Rental real estate offers powerful tax benefits like depreciation (worth $3,636 yearly on a $100,000 property), mortgage interest deductions, repair write-offs, and travel deductions. However, these benefits only work if you can prove every expense with organized records.

Clear Investment Performance: Which properties in your portfolio actually make money? Many landlords assume rental income minus mortgage payment equals profit. Real accounting reveals the complete picture: vacancy costs, maintenance reserves, property management fees, property tax increases, and insurance premiums that determine true return on investment.

Faster Decision-Making: Should you sell that underperforming rental or raise rents to market rates? Accurate financial statements let you compare properties objectively, spot problems before they worsen, and capitalize on opportunities while other landlords still search for last year's receipts.

Audit Protection: The IRS audits rental property owners at higher rates than regular employees because rental income creates more opportunities for errors and fraud. Clean books with proper documentation turn a stressful audit into a straightforward conversation. Sloppy records cost you thousands in disallowed deductions plus penalties that compound annually.

Rental property accounting isn't about enjoying spreadsheets, it's about keeping more of what you earn and building wealth faster through real estate investment.

Income Tracking by Source: Record every revenue stream separately for each property: monthly rent, late fees, pet deposits, parking fees, laundry income, and application fees. Separate tracking helps you identify which income sources perform best and reveals opportunities you might miss if everything flows into one account. Document the source, date, and tenant name for each deposit so tax season doesn't become guesswork.

Expense Management and Categorization: Rental properties generate dozens of expense categories that the IRS treats differently. Your accounting system must separate repairs (deducted immediately) from capital improvements (depreciated over years), ordinary expenses from startup costs, and property-specific costs from portfolio-wide expenses. A $5,000 roof replacement treated as maintenance instead of a capital improvement could trigger an audit.

Depreciation Tracking: Residential rental properties depreciate over 27.5 years, creating annual deductions that reduce your tax bill without requiring any cash outlay. Your system needs to calculate and track these non-cash deductions automatically. Most landlords overlook depreciation on appliances, carpeting, and property improvements that qualify for faster 5-7 year schedules.

Cash Flow Monitoring: Positive cash flow means rental income exceeds all expenses including mortgage payments, maintenance, insurance, and reserves. Negative cash flow requires you to cover the difference from other income. Track both monthly cash flow and year-to-date totals to identify seasonal patterns and plan for lean periods when vacancies spike.

Tenant and Lease Records: Connect financial transactions to specific tenants and lease agreements. When rent arrives late or damage deposits need reconciliation, you'll need quick access to lease terms, move-in condition reports, and payment history. Your accounting software should link these records seamlessly.

Many landlords discover they're significantly more (or less) profitable than assumed once they implement proper rental accounting. The data eliminates emotional decision-making and reveals exactly which properties build wealth versus drain resources.

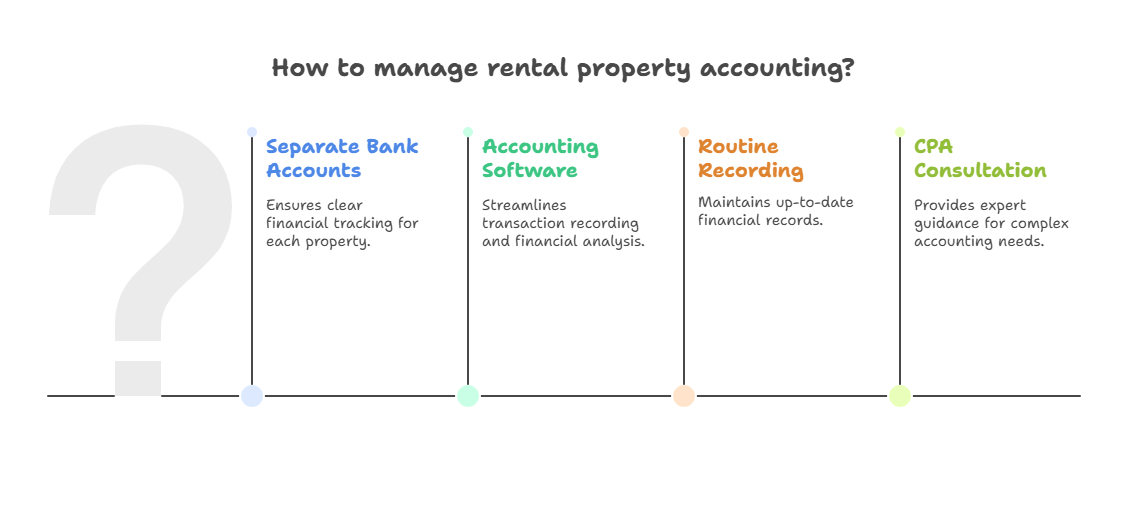

Separate Business and Personal Finances Completely: Open dedicated bank accounts and credit cards exclusively for rental properties. This single step saves hours during tax preparation, provides liability protection, and prevents the IRS from reviewing personal finances during audits. Many landlords create separate accounts for each property to track performance independently.

Implement Real-Time Recording: Log transactions within 24 hours while details remain fresh in memory. Waiting until month-end means you'll forget whether that $275 charge was for plumbing repairs or appliance maintenance. Successful landlords spend 10 minutes daily updating books rather than facing 6-hour weekend marathons quarterly.

Digitize Everything Immediately: Use mobile receipt scanning apps to photograph and categorize expense receipts the moment you receive them. This eliminates shoebox accounting and ensures you never lose documentation for legitimate deductions. The IRS allows 3-7 years to audit returns depending on circumstances, so maintain digital records for at least that period.

Review Monthly Financial Statements: Generate profit and loss statements, balance sheets, and cash flow reports monthly. These reports reveal trends before they become crises. Rising maintenance costs might indicate a property needs major repairs soon, or declining rent collection rates might signal tenant screening problems worth addressing.

Budget for Vacancy and Maintenance: Set aside reserves equal to 3-6 months of operating expenses. Rental properties surprise you with unexpected costs like HVAC failures, tenant turnover, plumbing emergencies, and special assessments. Adequate reserves prevent scrambling for emergency funding when properties need immediate attention.

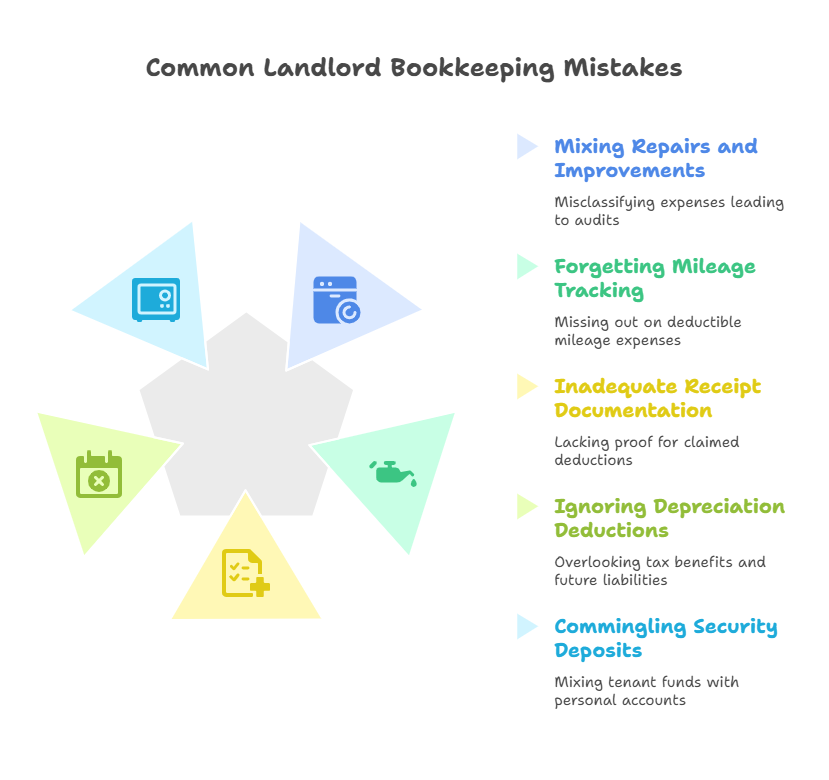

Mixing Repairs with Capital Improvements: The IRS distinguishes between repairs (fixing existing functionality) and improvements (adding value or extending useful life). Replace a broken dishwasher with a similar model and deduct it immediately as a repair. Install a high-efficiency model that reduces utility costs and you must depreciate it as an improvement over several years. Misclassifying these expenses triggers audits and costs immediate deductions.

Forgetting Mileage Tracking: Every mile driven to inspect properties, meet contractors, show units, or buy supplies qualifies as a deductible expense at $0.67 per mile in 2025. Most landlords forget to track mileage, leaving thousands in legitimate deductions unclaimed annually. Simple mileage tracking apps automate this process through GPS.

Inadequate Receipt Documentation: Claiming deductions without supporting documentation is like playing audit roulette. The IRS requires receipts, invoices, canceled checks, or credit card statements for every deduction. A $800 repair becomes an $800 problem if you can't prove it happened. Take photos before and after repairs, save contractor invoices, and maintain tenant correspondence about maintenance requests.

Ignoring Depreciation Deductions: Depreciation reduces your tax bill now but increases capital gains when you sell. Many landlords forget to track cumulative depreciation over years of ownership, leading to surprise tax bills at sale time. Your accounting system should automatically calculate both annual depreciation and lifetime totals for accurate basis tracking.

Commingling Security Deposits: Security deposits aren't rental income when received, they're liabilities you owe back to tenants. Only deductions for actual damages convert security deposits to income. Track deposits separately in dedicated accounts to avoid accidentally spending money that belongs to tenants and to stay compliant with state escrow requirements.

Modern accounting software eliminates manual spreadsheet updates, automates transaction categorization, and generates professional financial reports with minimal effort.

Must-Have Features: Look for software that handles multiple properties simultaneously, integrates with bank feeds for automatic transaction import, calculates depreciation schedules automatically, generates Schedule E tax forms, and tracks security deposits separately. Mobile apps with receipt scanning save hours of administrative work by letting you photograph and categorize expenses on-site.

Popular Landlord Platforms: Property-specific software like Stessa, Baselane, and Landlord Studio offer features tailored to rental owners including rent collection, maintenance tracking, and tenant portals. These platforms often provide better user experience for real estate operations than general business tools. QuickBooks Online works well for landlords who need broader business accounting capabilities beyond just rental properties.

Implementation Strategy: Start with free trials to test functionality before committing to annual subscriptions. Most platforms offer data migration services to import existing records, though expect to invest 3-5 hours on initial setup. The payoff comes monthly with automated bookkeeping that reduces manual work from hours to minutes.

Integration Capabilities: Choose software that connects seamlessly with your bank accounts, property management systems, and accountant's platform. Automated data flow between systems reduces errors, eliminates duplicate entry, and ensures everyone works from the same accurate financial information.

Schedule E Reporting: Rental income and expenses get reported on IRS Schedule E (Supplemental Income and Loss), not Schedule C like regular business income. This distinction affects how the IRS treats passive activity losses and which deductions you can claim. Most rental accounting software generates Schedule E automatically from your transaction data.

Passive Activity Loss Rules: The IRS classifies most rental activities as passive, limiting your ability to deduct rental losses against ordinary W-2 income. Active participation rules let you deduct up to $25,000 in rental losses annually if your modified adjusted gross income stays below $100,000. Understanding these thresholds helps you structure investments optimally and avoid surprise tax bills.

Depreciation Recapture: Every depreciation deduction you claim reduces your property's tax basis. When you sell, the IRS taxes cumulative depreciation at up to 25% through depreciation recapture rules. Plan for this tax hit when calculating sale proceeds, or use 1031 exchanges to defer taxes by rolling proceeds into replacement properties.

Deductible Expenses: The IRS allows landlords to deduct ordinary and necessary business expenses including mortgage interest, property taxes, insurance premiums, repairs, maintenance, property management fees, advertising, legal services, and accounting costs. However, acquisition costs like down payments and closing costs aren't immediately deductible but instead get added to your property basis and recovered through depreciation.

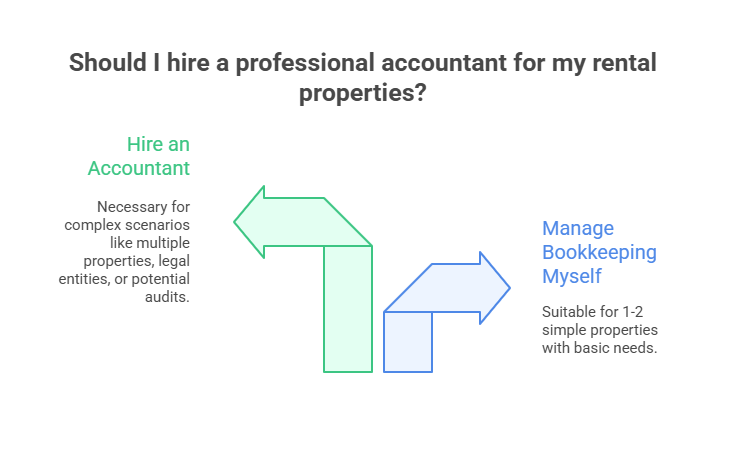

Most landlords can handle basic bookkeeping for 1-2 simple rental properties using quality software and self-education. The need for professional accounting emerges as complexity increases beyond basic rent collection and expense tracking.

Consider hiring an accountant when you: acquire your third rental property, form an LLC or other legal entity, complete 1031 exchanges, invest in commercial real estate, partner with other investors, hire property managers, or face potential IRS audits. These scenarios introduce tax implications and reporting requirements that exceed typical software capabilities.

A specialized rental property accountant provides value beyond annual tax preparation. They identify deductions most landlords miss, structure deals to minimize tax liability, explain when cost segregation studies make financial sense, advise on entity structure for liability protection, and represent you during IRS examinations. The right accountant pays for themselves through tax savings and strategic guidance.

When choosing an accountant, prioritize rental property specialization over general practice experience. Ask how many landlord clients they serve, request references from investors at your experience level, and discuss their availability throughout the year for questions beyond tax season. The best accounting relationships involve regular communication and proactive planning, not just annual transactions.

Proper categorization of rental transactions ensures accurate tax reporting and helps you understand true property performance. Here's a breakdown of the most common categories landlords need to track:

Understanding these categories helps you make better financial decisions and ensures you're claiming every legitimate deduction the IRS allows. Most tax software and rental property accounting platforms include these categories pre-configured, but you'll need to verify transactions get assigned correctly.

The accounting system that works perfectly for two single-family rentals will break down at eight properties. Plan for growth from day one to avoid painful transitions later.

Entity Structure Evolution: Many landlords start as sole proprietors but transition to LLCs or S-corporations as portfolios expand beyond 3-5 properties. Each structure offers different tax treatment, liability protection, and administrative requirements. Discuss optimal structure with your accountant based on current portfolio size and 3-year growth goals.

Systems and Processes: Document your accounting workflows including when you record transactions, how you file receipts, who handles which tasks, and what reports you review monthly. Written procedures let you delegate accounting work to bookkeepers or virtual assistants as your time becomes more valuable focusing on acquisitions and strategy.

Technology Stack: Your accounting software should integrate seamlessly with property management platforms, banking systems, tenant payment portals, and your accountant's tools. Automated data feeds eliminate duplicate entry, reduce errors, and ensure everyone works from identical information. Invest in technology that scales with portfolio growth rather than requiring platform switches later.

Team Building: Successful landlords with 10+ properties build teams including accountants, bookkeepers, property managers, attorneys, contractors, and mortgage brokers. Each specialist handles their domain expertise, freeing you to focus on finding deals and building tenant relationships. The goal isn't becoming an accounting expert, it's building systems that provide accurate data without consuming your time.

Open dedicated bank accounts exclusively for rental properties and never mix personal transactions with rental activity. Deposit all rental income (rent, fees, deposits) into the rental account and pay all property expenses from this account. This separation simplifies bookkeeping, provides audit protection, and takes about 30 minutes to set up at your bank. Many landlords create separate accounts for each property to track individual performance.

Spreadsheets work initially for 1-2 simple properties but become error-prone and time-consuming as portfolios grow. Specialized rental accounting software automates transaction categorization, calculates depreciation, generates Schedule E tax forms, and typically saves 150+ hours annually compared to manual spreadsheet tracking. Most platforms offer free trials so you can test before committing to paid subscriptions.

Landlords can deduct ordinary and necessary business expenses including mortgage interest, property taxes, insurance, repairs, maintenance, property management fees, utilities (if landlord-paid), advertising, legal and professional services, travel to properties, and depreciation. However, capital improvements must be depreciated over 27.5 years rather than deducted immediately. Keep receipts for everything to support deductions during potential audits.

Keep tax returns permanently and maintain supporting documentation (receipts, bank statements, depreciation schedules) for at least 7 years after filing. The IRS typically audits within 3 years but extends to 6 years for substantial income underreporting. Keep property acquisition documents, major improvement records, and cumulative depreciation schedules until 7 years after selling the property since these affect capital gains calculations.

Cash accounting records income when rent arrives and expenses when bills get paid, making it simpler for small landlords. Accrual accounting records transactions when earned or incurred regardless of payment timing, providing more accurate financial pictures. Most landlords with 1-3 properties use cash method, but switch to accrual once they exceed 3-5 units or seek bank financing that requires accrual-based statements.

Yes, tracking each property separately reveals which rentals generate profit versus drain resources. Separate accounting helps you make informed decisions about raising rents, selling underperformers, or reinvesting in high-performers. Most rental accounting software lets you run consolidated portfolio reports while maintaining property-level detail. The extra effort pays off through better investment decisions.

DIY accounting using software runs $0-$50 monthly depending on portfolio size. Hiring bookkeepers costs $150-$400 monthly for basic transaction recording. Comprehensive accounting including bookkeeping and tax preparation typically costs $2,000-$6,000 annually for landlords with 3-10 properties. However, proper accounting usually saves more in taxes than it costs in fees, making it a worthwhile investment.

Rental property accounting isn't optional if you want to build lasting wealth through real estate investment. The difference between profitable landlords and those who struggle often comes down to financial visibility, knowing exactly where money arrives from, where it flows to, and how to optimize the income stream.

Start today by opening separate bank accounts for rental properties, choosing accounting software appropriate for your portfolio size, and establishing a routine for recording transactions within 24 hours. If you manage 3+ properties or feel overwhelmed by accounting complexity, schedule consultations with rental property CPAs who specialize in real estate taxation.

Proper accounting can accelerate your rental property success while giving you time back for finding your next great investment opportunity.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.