Retail Inventory Accounting Methods: FIFO vs LIFO vs Weighted Average

Inventory is often the largest current asset on a retail company's balance sheet. How you value that inventory can significantly influence your profitability, tax liability, and financial reporting. This is why choosing the right inventory valuation method is not just a compliance task but a strategic decision that affects every aspect of inventory management.

Retail businesses have three common inventory accounting methods to account for inventory costs:

First-In, First-Out (FIFO)

Last-In, First-Out (LIFO)

Weighted Average Cost

Each inventory valuation method has different implications for cost of goods sold (COGS), net income, inventory valuations, and taxes. The choice can also impact how your business appears to lenders, investors, and even buyers. Understanding how each method affects inventory value and overall accounting practices is crucial for effective inventory management.

This guide explains each inventory costing method in depth, compares their effects on your financials, and helps you choose the most appropriate option based on your retail operation, inventory type, and market conditions.

Why Inventory Accounting Matters in Retail

Inventory accounting is about more than keeping track of stock levels. Proper inventory management affects:

Tax Liability: The inventory method you choose can change how much taxable income you report based on how inventory cost flows through your accounting system.

Financial Health Indicators: Gross margin, working capital, and asset turnover are all impacted by your inventory valuations and how you calculate the cost of goods sold.

Lending Relationships: Banks evaluate your inventory value when considering loans, making accurate inventory reporting crucial for credit access.

Investor Trust: Accurate and consistent inventory valuations build financial credibility and support business growth.

For high-volume retailers where inventory turns over rapidly, these differences in inventory accounting can add up quickly. A change in accounting method can lead to shifts in reported income by tens or even hundreds of thousands of dollars per year, significantly affecting inventory balance sheet presentation.

Understanding the Basics of Inventory Costing

Before comparing FIFO, LIFO, and weighted average methods, it is important to understand what inventory costing involves and how inventory cost flows through your accounting system.

When a retailer buys inventory for resale, the cost of inventory is recorded as an asset on the balance sheet. As inventory items are sold, a portion of that inventory becomes cost of goods sold on the income statement. The remaining inventory stays on the balance sheet as ending inventory.

The challenge arises when purchase prices change over time due to inflation, supplier pricing, or seasonal shifts. If you bought the same inventory item at $10 and $15 in different months, which price should be used to calculate the cost of goods sold when that inventory item is sold?

This is where inventory costing methods come in. They provide the rules for how to assign inventory cost to cost of goods sold and how to determine inventory value for the items that remain unsold. Each inventory valuation method affects how you calculate the cost and manage changes in inventory levels.

1. FIFO (First-In, First-Out)

How the FIFO Method Works

The FIFO method assumes that the oldest inventory items are sold first. This inventory costing method means the cost of goods sold reflects the cost of your earliest purchases, while the inventory on hand reflects your most recent (usually higher) purchase prices. FIFO inventory management closely matches the physical flow for many retail businesses.

FIFO Example

A clothing store buys:

100 T-shirts at $10 in January

100 T-shirts at $12 in February

If the store sells 150 T-shirts in March, the FIFO method would record:

100 inventory items at $10 (sold first)

50 inventory items at $12 (sold next)

Cost of Goods Sold Calculation: COGS = (100 × $10) + (50 × $12) = $1,000 + $600 = $1,600

Ending Inventory = 50 shirts at $12 = $600

This example shows how FIFO affects both cost of goods sold and ending inventory valuations.

Advantages of FIFO

Higher Net Income: Produces higher net income during periods of rising prices, improving financial statement presentation

Current Inventory Value: Shows inventory on the balance sheet at more current prices, providing accurate inventory valuations

Physical Flow Match: Matches actual physical flow for many retail inventory management situations

IFRS Compliance: Accepted under international financial reporting standards

Disadvantages of FIFO

Higher Tax Liability: Results in higher taxable income in inflationary environments

Overstated Profitability: Can overstate profitability during inflation periods

Cash Flow Impact: Higher taxes reduce available cash flow for inventory management

Best Use Cases for FIFO

Retailers with fast-moving inventory where inventory first in should be sold first

Businesses where inventory closely matches FIFO assumptions (e.g., food, fashion)

Companies prioritizing strong financial statement presentation for investors

2. LIFO (Last-In, First-Out)

How the LIFO Method Works

The LIFO method assumes that the most recently purchased inventory is sold first. This inventory costing method means the cost of goods sold reflects the latest prices, and older, cheaper inventory cost stays on the books as ending inventory.

LIFO Example

Using the same T-shirt scenario:

Cost of Goods Sold Calculation: COGS = (100 × $12) + (50 × $10) = $1,200 + $500 = $1,700

Ending Inventory = 50 shirts at $10 = $500

This shows how the LIFO method affects inventory valuations differently than FIFO.

Advantages of LIFO

Lower Tax Liability: Results in lower taxable income when prices rise, improving cash flow

Current Cost Matching: Matches recent inventory cost to revenue, improving income statement accuracy

Inflation Protection: Helps offset inflationary impacts on profitability

Disadvantages of LIFO

IFRS Restriction: Not allowed under international financial reporting standards, limiting global applicability

Understated Inventory Value: Inventory balance on balance sheet may be significantly undervalued

Complex Tracking: May complicate inventory management for older stock

LIFO Conformity Rule: If you use LIFO for tax purposes, you must also use it for financial reporting

Best Use Cases for LIFO

U.S. retailers concerned with minimizing income tax in inflationary periods

Businesses with stable or increasing purchase prices

Companies prioritizing tax savings over financial statement presentation

3. Weighted Average Cost Method

How Weighted Average Works

The weighted average cost method averages the cost of inventory across all inventory units and applies the same average cost to every inventory item sold. Each time inventory is purchased, a new weighted average cost is calculated, creating consistent inventory valuations.

Weighted Average Example

Using the T-shirt scenario:

Calculate Weighted Average Cost:

Total Cost of Inventory = (100 × $10) + (100 × $12) = $1,000 + $1,200 = $2,200

Total Units = 200

Weighted Average Cost = $2,200 ÷ 200 = $11 per shirt

If 150 shirts are sold:

Cost of Goods Sold = 150 × $11 = $1,650

Ending Inventory = 50 × $11 = $550

Advantages of Weighted Average

Simplified Tracking: Simplifies inventory management and valuation processes

Smoothed Fluctuations: Smooths out price fluctuations in inventory cost

High-Volume Efficiency: Useful for high-volume, low-cost inventory items

Lost Cost Trends: Does not reflect most recent inventory cost trends

Distorted Profitability: May distort profitability if prices shift quickly

Less Precision: Provides less precise inventory valuations than specific identification methods

Best Use Cases for Weighted Average

Retailers with large quantities of indistinguishable inventory items (e.g., hardware, small parts)

Businesses prioritizing simplicity in inventory accounting

Companies with frequently changing inventory costs

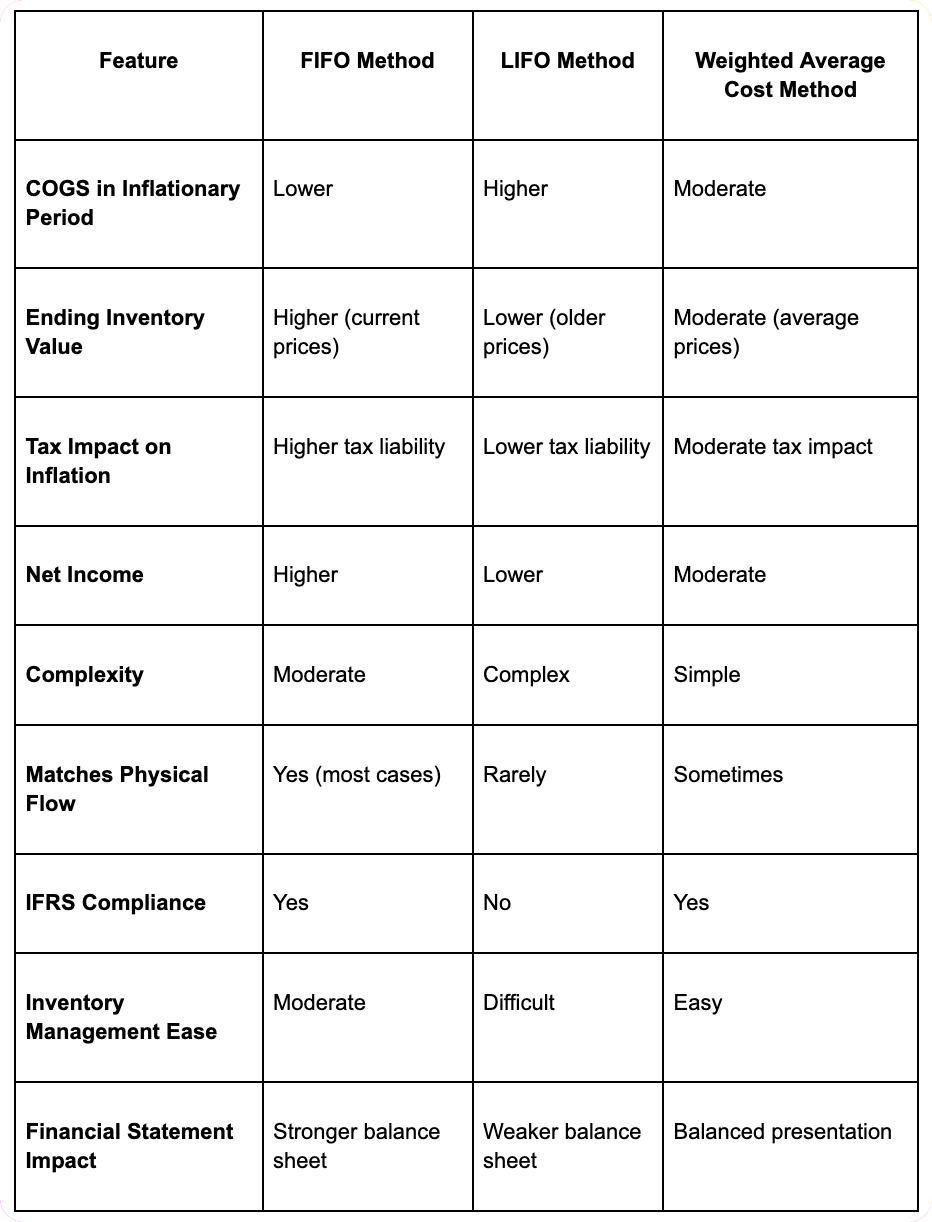

Comprehensive Comparison: FIFO vs LIFO vs Weighted Average

Tax Implications of Inventory Methods

The inventory valuation method you choose has a direct effect on taxable income and overall accounting treatment:

FIFO Tax Impact

Increases net income during inflation

Results in higher taxes when inventory costs rise

May require larger tax payments, affecting cash flow for inventory management

LIFO Tax Impact

Lowers net income during inflation

Reduces tax liability in inflationary times

Improves cash flow but may affect borrowing capacity

Subject to LIFO conformity rule requiring consistent use for both tax and financial reporting

Weighted Average Tax Impact

Falls between FIFO and LIFO in tax effects

Provides moderate and consistent tax treatment

Balances tax optimization with financial reporting needs

Important Note: Once an inventory method is chosen and used in filed tax returns, you generally need IRS approval to change it, making the initial selection crucial for long-term inventory management strategy.

Strategic Decision Framework: When to Use Each Method

Choose FIFO When:

You want stronger-looking financials for investors or lenders

You operate in a deflationary or stable price environment

You prioritize accurate inventory balance sheet presentation

Your physical inventory flow matches FIFO assumptions

You need compliance with international financial reporting standards

Choose LIFO When:

You want to reduce taxable income in inflationary environments

You operate only in the U.S. (since international financial reporting standards do not allow LIFO)

You prioritize tax savings over financial statement presentation

You can handle more complex inventory accounting requirements

Cash flow optimization is more important than reported earnings

Choose Weighted Average When:

You handle high-volume, low-cost inventory with frequent purchases

You want simplicity in inventory management and accounting

You are not concerned with matching exact physical inventory flow

You prefer consistent and predictable inventory valuations

You want to avoid the complexity of tracking specific inventory cost layers

Industry-Specific Applications

Fashion Retail

Often uses the FIFO method since inventory moves quickly and aligns with physical flow. Higher ending inventory values also help reflect the cost of current season goods, supporting accurate inventory valuations for seasonal merchandise.

Electronics and Technology Stores

Frequently employ the weighted average cost method because inventory costs fluctuate regularly, and tracking exact batches is not always practical for inventory management purposes.

Wholesale Distributors

Some may use LIFO to lower taxes on large volumes of goods, particularly in inflation-heavy industries like building materials or fuel where inventory cost increases significantly impact profitability.

Grocery and Perishables

Typically use FIFO method due to the perishable nature of inventory items and the need to sell inventory first in to maintain product quality and avoid spoilage.

Implementation Considerations for Inventory Management

Technology Requirements

Your chosen inventory valuation method must be supported by your:

Point-of-sale (POS) systems

Enterprise resource planning (ERP) software

Inventory management systems

Accounting software

Process Documentation

Proper implementation requires:

Written accounting policies describing your inventory method

Staff training on inventory tracking procedures

Regular review processes to ensure accurate inventory accounting

Documentation supporting inventory valuations for audit purposes

Internal Controls

Effective inventory management requires:

Regular physical inventory counts

Reconciliation between perpetual and physical counts

Approval processes for inventory adjustments

Segregation of duties in inventory management

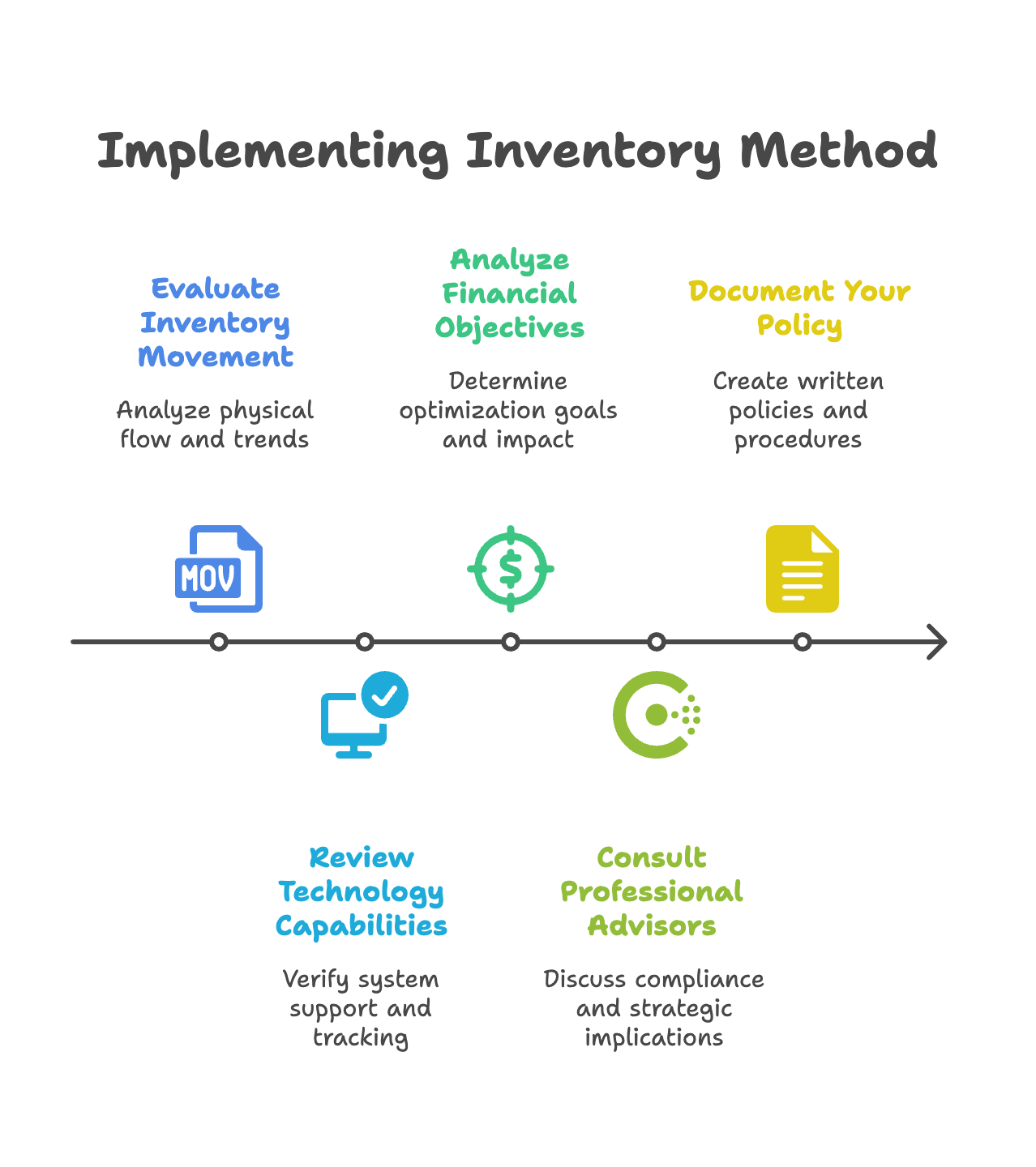

How to Implement the Right Inventory Method

Choosing an inventory costing method requires careful analysis of your specific business situation:

Step 1: Evaluate Your Inventory Movement

Analyze whether your physical inventory flow matches any particular method

Review historical inventory cost trends and price volatility

Assess the nature of your inventory items and turnover rates

Step 2: Review Technology Capabilities

Verify your POS or ERP system supports your preferred inventory method

Ensure you can accurately track inventory cost layers

Confirm reporting capabilities meet your accounting needs

Step 3: Analyze Financial Objectives

Determine whether you're optimizing for cash flow or reported income

Consider the impact on key financial ratios and metrics

Evaluate how inventory valuations affect your overall financial strategy

Step 4: Consult Professional Advisors

Discuss compliance requirements and audit risks with your CPA

Review long-term strategic implications

Ensure alignment with generally accepted accounting principles

Step 5: Document Your Policy

Create written policies for inventory accounting

Establish procedures for maintaining consistent application

Switching inventory methods is possible but requires careful planning and has significant implications:

IRS Requirements

File Form 3115 (Application for Change in Accounting Method)

Obtain IRS approval before implementing the change

Calculate Section 481(a) adjustment for the change

Financial Impact Analysis

Adjusted beginning inventory for the year of change

Impact on cost of goods sold and ending inventory

Effect on financial ratios and covenant compliance

Changes in inventory balance sheet presentation

Documentation Requirements

Supporting documentation for the reason for change

Coordination with accounting software setup

Updated inventory management procedures

Staff retraining on new procedures

Professional Guidance: Work with your CPA to run scenarios and understand the tax timing differences before making a decision to change inventory methods.

Advanced Inventory Management Considerations

Inventory Valuation Accuracy

Maintaining accurate inventory requires:

Regular physical counts to verify perpetual records

Investigation and resolution of inventory discrepancies

Proper treatment of damaged, obsolete, or slow-moving inventory

Consistent application of your chosen inventory method

Seasonal Inventory Planning

Consider how your inventory method affects:

Seasonal buying patterns and inventory levels

Cash flow requirements for inventory purchases

Financial reporting during peak and off-peak periods

Tax planning opportunities related to inventory timing

International Operations

For businesses with global operations:

LIFO is not permitted under international financial reporting standards

Consider the impact of currency fluctuations on inventory cost

Ensure compliance with local accounting requirements

Maintain consistent inventory accounting across jurisdictions

Financial Strategy and Inventory Valuation

Your inventory method influences broader business decisions beyond basic accounting:

Inventory accounting method affects business valuation multiples

Buyer preferences may influence optimal method selection

Historical consistency in inventory accounting enhances credibility

Best Practices for Ongoing Inventory Management

Monthly Procedures

Calculate cost of goods sold using your chosen method

Reconcile perpetual inventory records to general ledger

Review inventory aging and identify slow-moving items

Analyze gross margin trends and investigate variances

Quarterly Reviews

Perform cycle counts to verify inventory accuracy

Review inventory valuation method effectiveness

Assess changes in inventory cost trends

Update inventory forecasts and purchasing plans

Annual Assessments

Conduct comprehensive physical inventory counts

Review inventory accounting policy effectiveness

Consider changes in business operations affecting inventory

Evaluate technology upgrades for inventory management

Common Mistakes to Avoid

Implementation Errors

Inconsistent application of chosen inventory method

Inadequate staff training on inventory procedures

Poor integration between inventory and accounting systems

Insufficient documentation of inventory accounting policies

Ongoing Management Issues

Failure to maintain accurate inventory records

Inconsistent treatment of inventory adjustments

Inadequate review of inventory valuation assumptions

Poor coordination between operational and accounting teams

Strategic Oversights

Choosing method based solely on short-term tax benefits

Failing to consider long-term business implications

Ignoring technology limitations in method selection

Inadequate professional consultation on method choice

Conclusion

For retail businesses, inventory represents both a significant asset and a complex accounting challenge. The choice between FIFO, LIFO, and weighted average cost methods affects every aspect of financial reporting, from cost of goods sold calculation to ending inventory valuations on the balance sheet.

Selecting the right inventory valuation method depends on your inventory cost trends, financial goals, and operational requirements. Whether you prioritize tax optimization, financial statement presentation, or operational simplicity, there is an inventory accounting approach that aligns with your business strategy.

The key to successful inventory management lies in understanding how each inventory costing method affects your business, implementing consistent procedures, and maintaining accurate inventory records. With proper planning and professional guidance, your inventory accounting can become a strategic advantage rather than just a compliance requirement.

Most importantly, remember that consistency is crucial. Once you select an inventory method and begin using it in your accounting system, maintaining consistent application ensures reliable financial reporting and supports informed business decision-making. Work with qualified accounting professionals to ensure your inventory management practices align with generally accepted accounting principles and support your long-term business objectives.

Table of Contents

Ready to Hire?

Talk to our team — we’ll scope your needs and start in days.

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.

.png)

%2075-100%20(12).png)

%2075-100%20(9).png)