.png)

Revenue recognition is the most important figure on a SaaS company's income statement. Yet, implementing proper revenue recognition is anything but simple for a SaaS business. Subscription billing, freemium models, onboarding delays, and customer churn create timing gaps between when cash is collected and when revenue can be officially recorded.

This is where ASC 606 comes into play. It is the current revenue recognition standard issued by the Financial Accounting Standards Board (FASB) and adopted by all U.S. companies, including private SaaS companies. The goal is to provide consistency and clarity in how businesses report revenue from customer contracts under modern accounting standards.

For SaaS companies, ASC 606 brings specific challenges to revenue recognition. Software is often delivered over time, bundled with services, or subject to refunds. Revenue must be allocated precisely, recognized in the correct periods, and supported with strong documentation to ensure each performance obligation is properly addressed.

In this guide, we walk through the complete ASC 606 framework and how SaaS companies can operationalize revenue recognition effectively. We also explain common pain points and how CPA firms can help their SaaS clients stay compliant while presenting financials investors can trust.

ASC 606 is the accounting standard titled "Revenue from Contracts with Customers." This revenue recognition standard replaced previous industry-specific guidance such as ASC 985-605 (software revenue) and applies to all entities that enter into contracts to provide goods or services.

The core principle of ASC 606 is this: Revenue recognition should occur when control of the promised goods or services is transferred to the customer in an amount that reflects the consideration the company expects to receive.

To apply this revenue recognition standard, SaaS companies must follow a five-step framework that aligns how revenue is recognized with contract performance rather than billing schedules or cash receipts. This approach fundamentally changes how many SaaS businesses recognize revenue compared to previous accounting standards.

A contract is an agreement between two or more parties that creates enforceable rights and obligations. For SaaS businesses, contracts may be written, digital (clickwrap), or even implied through terms of service and payment acceptance.

Key considerations for SaaS revenue recognition:

Even if the contract is auto-renewed or month-to-month, it must be assessed for enforceable terms and scope before any revenue can be recognized.

A performance obligation is a distinct good or service promised in the contract. SaaS contracts often include multiple deliverables such as:

Each component must be evaluated to determine whether it is distinct or part of a single performance obligation. If a service can be used on its own or with other readily available resources, it is considered distinct and must be accounted for separately in the revenue recognition process.

This step is crucial for SaaS revenue recognition because many SaaS companies bundle multiple services that may constitute separate performance obligations under ASC 606.

The transaction price is the amount the SaaS business expects to be entitled to in exchange for transferring goods or services.

Adjustments to the transaction price may include:

Estimating the transaction price may involve probability-weighted approaches when the price depends on customer usage or performance milestones. This is particularly important for SaaS companies with usage-based pricing models.

Once the performance obligations and total transaction price are identified, the next step is to allocate the price across the obligations. This must be done based on relative standalone selling prices for each performance obligation.

For example, if a customer signs a one-year SaaS subscription bundled with onboarding for $1,200, and the standalone prices are:

The $1,200 transaction price must be allocated proportionately:

This allocation directly impacts how and when SaaS companies can recognize revenue for each performance obligation.

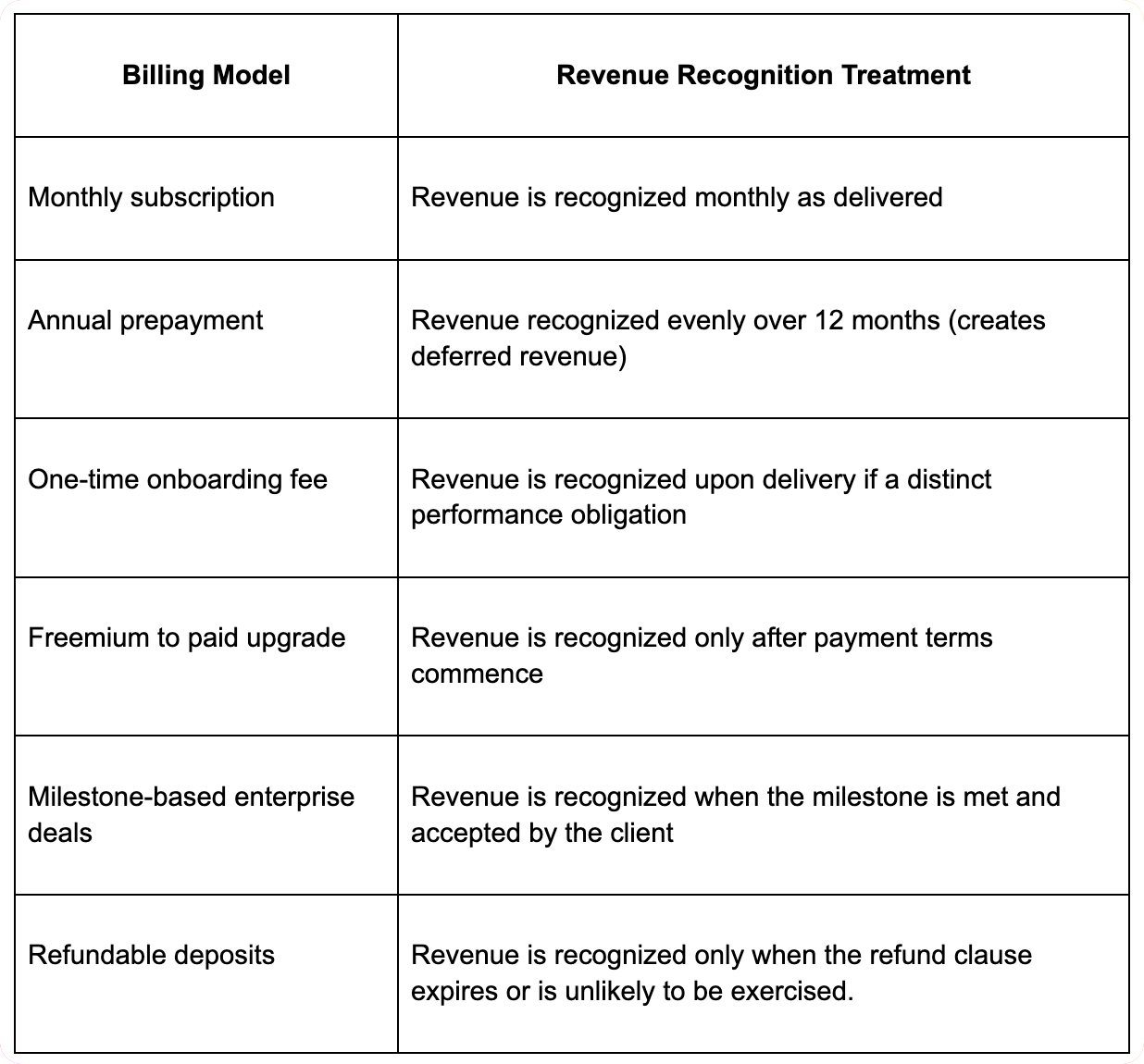

SaaS revenue recognition usually occurs over time rather than at a point in time. This means SaaS companies recognize revenue ratably as the service is delivered, typically on a straight-line basis over the subscription term.

One-time services like onboarding may qualify to recognize revenue at a point in time if they are delivered upfront and not tied to ongoing use of the product. However, each performance obligation must be evaluated individually to determine the appropriate revenue recognition pattern.

A customer pays $12,000 upfront for one year of access to a cloud-based software.

This creates deferred revenue on the balance sheet that is recognized monthly as the performance obligation is satisfied.

A customer signs a 12-month agreement with $10,000 software access and $2,000 onboarding fee.

This example shows how different performance obligations can have different revenue recognition timing within the same contract.

A customer pays $100 per month base fee plus $10 per API call over 1,000 calls.

Deferred revenue is a critical balance sheet component for most SaaS companies. When customers pay upfront for services to be delivered over time, the SaaS business must record deferred revenue (a liability) until the performance obligation is satisfied and revenue can be recognized.

Initial Recognition:

Revenue Recognition Process:

Financial Reporting Impact:

Many SaaS startups use informal or evolving contracts. Vague terms can make it difficult to determine performance obligations or pricing for proper revenue recognition. Legal and finance teams should collaborate on standardized language that supports ASC 606 compliance.

If billing, usage tracking, and accounting live in separate systems, it becomes difficult to track fulfillment of performance obligations and adjust revenue recognition accordingly. Integration between CRM, billing, and accounting tools is crucial for accurate SaaS revenue recognition.

Many SaaS companies collect cash upfront, creating deferred revenue on the balance sheet. If not tracked properly, this leads to incorrect revenue recognition and tax issues that can significantly impact financial reporting.

Bundled pricing often combines software, support, and implementation in one figure. ASC 606 requires unbundling these into separate performance obligations and applying fair value allocations before revenue can be recognized.

Lack of documentation for performance obligations, pricing estimates, or contract amendments can result in revenue restatements during audits. SaaS companies must maintain detailed records supporting their revenue recognition decisions.

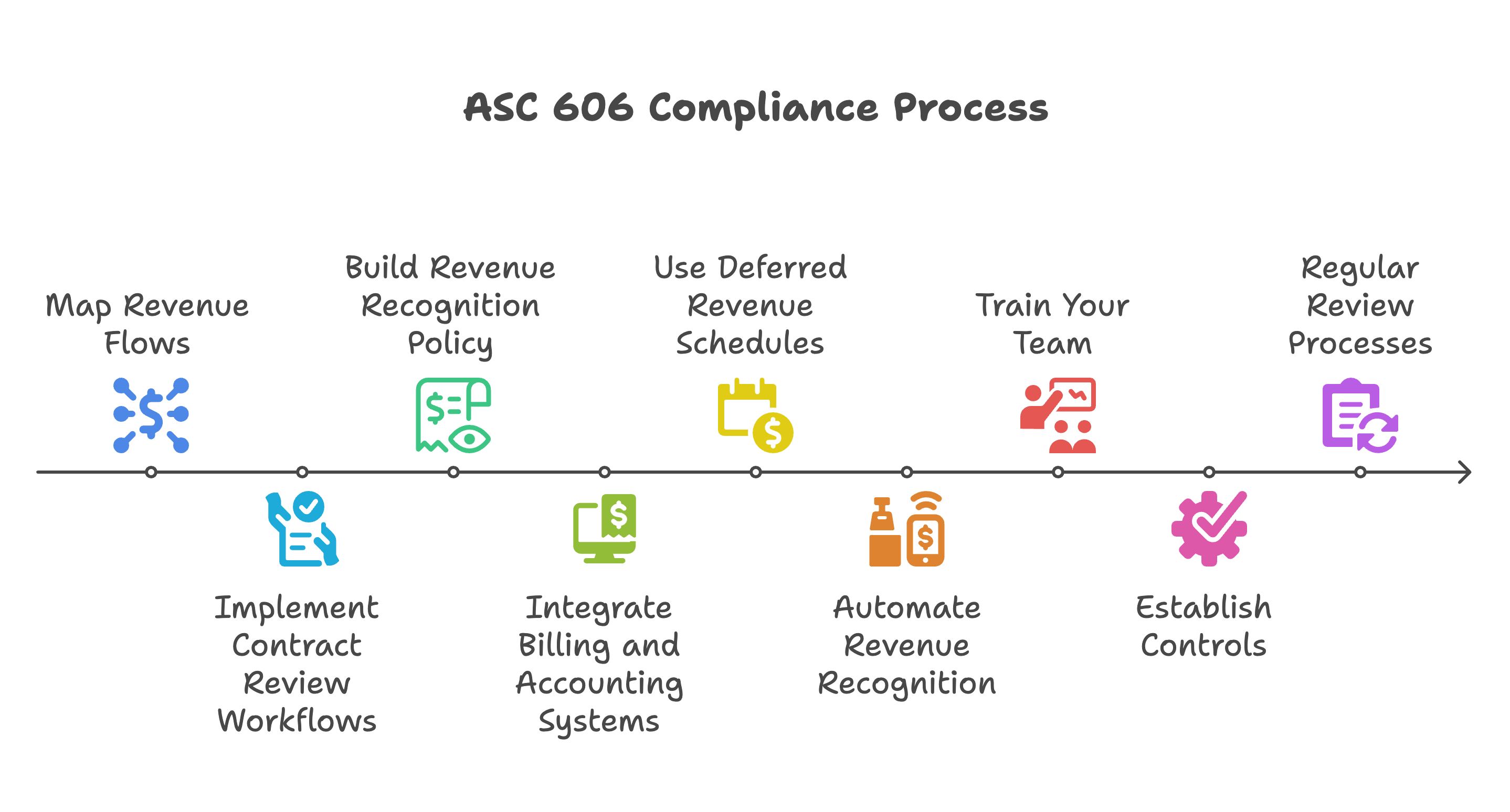

Map out your revenue flows: Document how revenue is generated, what services are included, and how customers use your product to identify all performance obligations.

Implement contract review workflows: Have a process for identifying distinct performance obligations and classifying contract types for proper revenue recognition.

Build a revenue recognition policy: Document your accounting policies with detailed examples and ensure consistency across clients and teams.

Integrate billing and accounting systems: Tools like NetSuite, Chargebee, or Zuora help automate revenue recognition processes and ensure compliance with ASC 606.

Use deferred revenue schedules: Track prepaid amounts and align them with revenue recognition timing using rolling schedules that automatically calculate when revenue should be recognized.

Automate revenue recognition: Implement systems that can automatically recognize revenue based on predefined rules and performance obligation satisfaction.

Train your team: Educate sales, product, and finance departments on how their activities affect revenue recognition under ASC 606.

Establish controls: Create approval processes for contract modifications that could impact performance obligations or revenue recognition timing.

Regular review processes: Implement monthly and quarterly reviews to ensure revenue recognition accuracy and identify any issues early.

Performance obligations are central to ASC 606 revenue recognition for SaaS companies. Proper identification and treatment of each performance obligation directly impacts when and how much revenue can be recognized.

Software Access:

Implementation Services:

Training and Support:

Custom Development:

To determine if a service is a distinct performance obligation, SaaS companies must assess:

NetSuite Revenue Management:

Sage Intacct Contracts:

Zuora Revenue (formerly RevPro):

Chargebee Revenue Recognition:

Automated Processing:

Performance Obligation Management:

Reporting and Compliance:

SaaS founders often lack deep accounting knowledge and may misreport revenue unintentionally. CPA firms and fractional CFOs play a key role in:

For CPA firms serving tech clients, ASC 606 expertise is now a baseline expectation. Offering advisory services around contract structuring, compliance automation, and financial modeling creates long-term value for SaaS companies.

ASC 606 introduced complexity, but it also brought clarity to SaaS revenue recognition. For SaaS companies, revenue recognition is no longer just a timing issue—it's a strategic requirement that affects compliance, cash flow modeling, valuation, and investor confidence.

By understanding the five-step framework, properly identifying performance obligations, and building the right systems to automate revenue recognition, SaaS businesses can avoid costly errors and build stronger financial reporting foundations. Proper management of deferred revenue and accurate tracking of when revenue is recognized across all performance obligations is essential for SaaS business success.

The key to successful SaaS revenue recognition lies in thorough understanding of ASC 606 requirements, proper system implementation, and ongoing compliance monitoring. SaaS companies that invest in robust revenue recognition processes will be better positioned for growth, fundraising, and eventual exit opportunities.

CPA firms, controllers, and finance leaders should use ASC 606 not only as a compliance task but also as an opportunity to elevate internal processes and decision-making. With proper implementation, revenue recognition becomes a competitive advantage that supports accurate financial reporting and informed business decisions.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.