A quick reality check

You add a UK buyer to a US storefront and everything shifts. Prices must show differently, tax gets applied at another point in the flow, and a simple refund now needs a tax-adjusted credit note. This section explains how to run checkout, pricing, and refunds cleanly when selling across the US and UK/EU. It is written for finance and ops teams that may also work with an offshore partner.

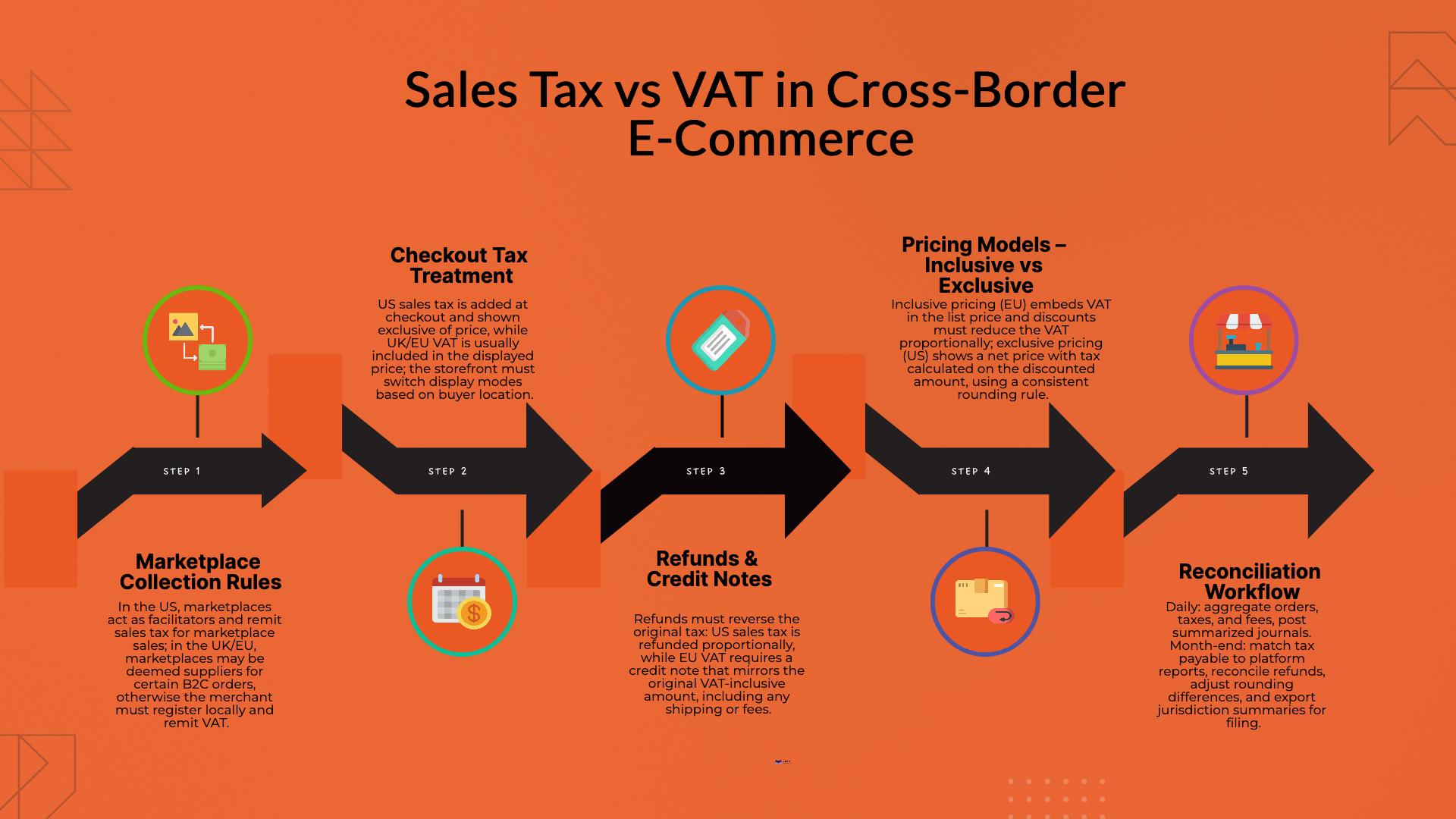

What this section covers

- How sales tax and VAT behave at checkout

- Inclusive vs exclusive pricing and how to choose

- Marketplace collection rules in practice

- Returns, refunds, and credit-note mechanics

- Reconciliation workflows that tie orders, tax, and ledger

Sales tax vs VAT at checkout: the core difference

Sales tax (US)

- Applied at the point of sale.

- Usually shown exclusive of list price on product pages, then added at checkout.

- Rate depends on destination and product taxability.

- Merchant or marketplace collects based on nexus and marketplace rules.

VAT (UK/EU)

- A consumption tax on value added at each stage.

- Often shown inclusive of VAT in consumer pricing.

- Rate depends on destination, product type, and B2C vs B2B status.

- Merchant charges VAT or uses a marketplace regime or import scheme where applicable.

Why this matters at checkout

- US buyers expect a pre-tax price with tax added in cart.

- UK/EU consumers expect the final price on the product page to already include VAT.

- Your storefront needs two display modes and clear tax messaging to avoid cart drop-off.

Pricing models: inclusive vs exclusive, coupons, and rounding

Inclusive pricing (typical for UK/EU B2C)

- List price includes VAT.

- Discount logic should reduce the VAT proportionally, not after-tax.

- Rounding needs to be stable at line level and order level.

Exclusive pricing (common in US)

- List price excludes sales tax.

- Discounts apply to the net price; tax calculates on the discounted base.

- Display “estimated tax” in cart and “final tax” at payment confirmation.

Operational guardrails

- Store the tax basis, tax amount, and total as separate fields per line.

- Fix a single rounding policy (round half up) and apply it at line level to avoid penny drift.

- Document how coupons affect tax. For VAT-inclusive pricing, the VAT element must reduce with the price.

Marketplace rules: who actually collects and remits

US marketplace facilitator rules

- Most large marketplaces calculate, collect, and remit sales tax for marketplace sales.

- First-party sales on your own site remain your responsibility where you have nexus.

- Reconcile marketplace tax reports separately from your web store.

UK/EU marketplace and import regimes

- Marketplaces may be the deemed supplier for certain cross-border B2C sales and will handle VAT for those orders.

- For direct sales into the EU or UK, you may need local VAT registration or to use import schemes.

- Keep marketplace order IDs and tax documents separate to avoid double remittance.

Action for finance

- Tag each order as “marketplace collected” or “merchant collected.”

- Store the tax registration used per order (for example, your UK VAT number) to support audits and refunds.

Returns and refunds: how tax should reverse

Sales tax (US)

- Refund original tax in proportion to the refunded amount.

- If you keep restocking fees, calculate tax on the net refunded base.

- Post a negative tax line to your sales tax payable account.

VAT (UK/EU)

- Issue a credit note that mirrors the original VAT treatment.

- For VAT-inclusive pricing, the refunded amount includes VAT; the VAT portion must be shown on the credit note.

- Exchange-driven returns need a linked document trail that shows price and VAT adjustments.

Operational checklist

- Credit note or refund memo references original invoice and lines.

- Proportional VAT or tax is recalculated and posted.

- Shipping and gift-wrap logic is consistent with your original tax treatment.

- Refund reports tie to payment processor payouts and GL.

Reconciliation workflow: daily and month-end

Daily

- Pull orders, refunds, and fees from storefront, marketplace, and PSP.

- Aggregate tax by jurisdiction and registration.

- Post summarized journals: net revenue, discounts, tax payable, shipping, and fees.

Month-end

- Tie tax payable to platform tax reports and marketplace statements.

- Match refunds and chargebacks to negative tax lines and credit notes.

- Review rounding differences and penny drift; post one adjusting entry if needed.

- Export jurisdiction summaries for filing.

Data you need on every line

- Tax basis, tax rate code, tax amount.

- Jurisdiction or registration used.

- Marketplace-collected flag.

- Original document link for refunds.

Selection criteria for your tax and checkout stack

- Display control: supports both VAT-inclusive and sales-tax-exclusive pricing and can switch by buyer location.

- Exemption handling: B2B VAT numbers and US resale or exemption flags with approval workflow.

- Refund engine: creates credit notes with correct tax reversal and posts to the GL.

- Marketplace parity: imports marketplace tax documents without trying to re-tax those orders.

- Reporting: jurisdiction summaries, audit trails, and API access for your BI tools.

- Access and privacy: role-based access, SSO, activity logs, and masked PII for offshore teams.

Working with an offshore team on cross-border tax

What to document

- Pricing mode by region and product type.

- Discount and coupon tax logic with examples.

- Refund playbook with sample credit notes.

- Who files returns for each jurisdiction and where reports live.

- Approval paths for tax overrides and exemptions.

What to restrict

- No local downloads of order exports with full PII.

- Time-bound credentials and activity logging for tax reports and PSP portals.

Takeaway

Use this guide to navigate Sales Tax vs VAT for Cross-Border Ecommerce: Checkout, Pricing, Refunds without guesswork. If you need a clean rollout with dual pricing modes, marketplace reconciliations, and refund-ready credit notes, Madras Accountancy can design the flow, document the SOPs, and run a short pilot with your stack.

%2075-100%20(12).png)

%2075-100%20(9).png)