For small business owners, freelancers, and partners in pass-through entities, the 20 percent deduction under section 199a has been a major opportunity to reduce taxable income. Introduced as part of the Tax Cuts and Jobs Act of 2017, this business income deduction allows eligible business owners to deduct up to 20 percent of their qualified business income, effectively lowering their federal income tax burden.

But there is a catch. The rules are filled with complex terms, income thresholds, limitations based on industry type, and additional criteria that confuse many taxpayers. While the deduction can be significant, mistakes or misunderstandings can lead to missed deductions or IRS issues.

At Madras Accountancy, we assist U.S.-based CPA firms in navigating section 199a for their clients, providing offshore support for calculations, documentation, and compliance reviews. This guide lays out exactly how the 199a deduction works, who can qualify, what income limits apply, and how to plan proactively to make the most of it.

Section 199a of the Internal Revenue Code provides a deduction of up to 20 percent on qualified business income (QBI) income earned through pass-through entities. These include:

The deduction applies to business income reported on the individual's tax return. It is not available for income earned through a C corporation.

For example, if your qualified trade or business earns $100,000 in QBI and you qualify for the deduction, you may be eligible for a $20,000 deduction, which reduces your taxable income.

This deduction is available in addition to standard deductions and other personal deductions. It is not an itemized deduction. Instead, it is taken directly from your taxable income after adjustments, appearing on Form 1040.

The goal of section 199a is to provide tax relief for small and mid-sized business owners who do not benefit from the flat 21 percent corporate tax rate introduced for C corporations.

Not all business income is eligible. To claim the deduction, income must meet the definition of QBI. According to the internal revenue service, QBI includes:

It does not include:

Only the net income from the trade or business, after expenses but before the section 199a deduction itself, is considered QBI.

Let's look at an example. If you own a single-member LLC with $250,000 in gross revenue and $100,000 in business expenses, your qualified business income would be $150,000. From there, the potential deduction could be up to 20 percent, or $30,000, depending on other factors and whether you qualify under the various limitations.

Most owners of pass-through businesses are eligible, but the deduction phases out or is limited based on:

For 2024 tax returns, the income thresholds are:

If your taxable income is below these levels, you can claim the full 20 percent deduction without limits, regardless of the business type. Taxpayers who qualify at this level can take the full business income deduction without worrying about wage or property limitations.

If your taxable income is above the threshold, restrictions may apply, especially if you operate a specified service trade or business.

SSTBs include fields where the principal asset is the reputation or skill of one or more of its employees or owners. These include:

Business owners of SSTBs begin to lose eligibility for the deduction once their taxable income exceeds the threshold. The deduction is completely phased out at:

This means a solo consultant earning $250,000 would not qualify for any deduction, while a small manufacturer earning the same amount could still claim a partial or full deduction.

For high-income taxpayers whose business is not a service trade or business, the deduction is limited to the greater of:

This provision was designed to prevent passive investors or owners with no payroll from claiming the deduction in full.

W-2 wages include compensation reported on Form W-2 for employees, excluding independent contractor payments.

Qualified property includes tangible property that is subject to depreciation, such as machinery or equipment, which is held and used in the trade or business.

Let's say your qualified trade or business earns $500,000 in QBI but has no employees. You will not be able to claim the full 20 percent deduction unless the property-based limitation covers the gap. The deduction may be significantly reduced or eliminated in such cases.

Understanding how to compute the section 199a deduction helps clarify what your business may actually benefit from. Here are three practical examples based on different scenarios.

A freelance graphic designer files as a sole proprietor and reports:

Since the taxpayer's income is below the threshold, they qualify for the full 20 percent deduction.

Calculation: 20 percent of $100,000 QBI = $20,000 deduction

This amount is deducted from the taxable income on the tax return, offering direct tax savings. Because they qualify without limitations, they can claim the full business income deduction.

A couple owns a small manufacturing business structured as an S corporation. Their joint taxable income is $400,000. The business:

Since they exceed the income threshold, wage and property limitations apply.

Step 1: Calculate limits

The allowable deduction is the lesser of 20 percent of QBI ($60,000) or the greater of the two limits above. So, in this case, they qualify for a $60,000 deduction.

A married couple runs a financial advisory firm with $500,000 in taxable income. Because it is a specified service trade or business and above the full phaseout limit, they are not eligible for the deduction and do not qualify for any tax year benefits under section 199a.

Business owners with multiple related entities may be able to aggregate their businesses for section 199a purposes. This can help maximize the deduction when one entity has W-2 wages and another generates QBI.

To qualify for aggregation, the following conditions must be met:

When properly applied, aggregation allows you to combine qualified business income, wages, and property across entities, which can increase the allowable deduction. This strategy helps pass-through business owners who qualify maximize their overall tax benefits.

Tip: Aggregation must be consistently applied each tax year and properly disclosed on your tax return.

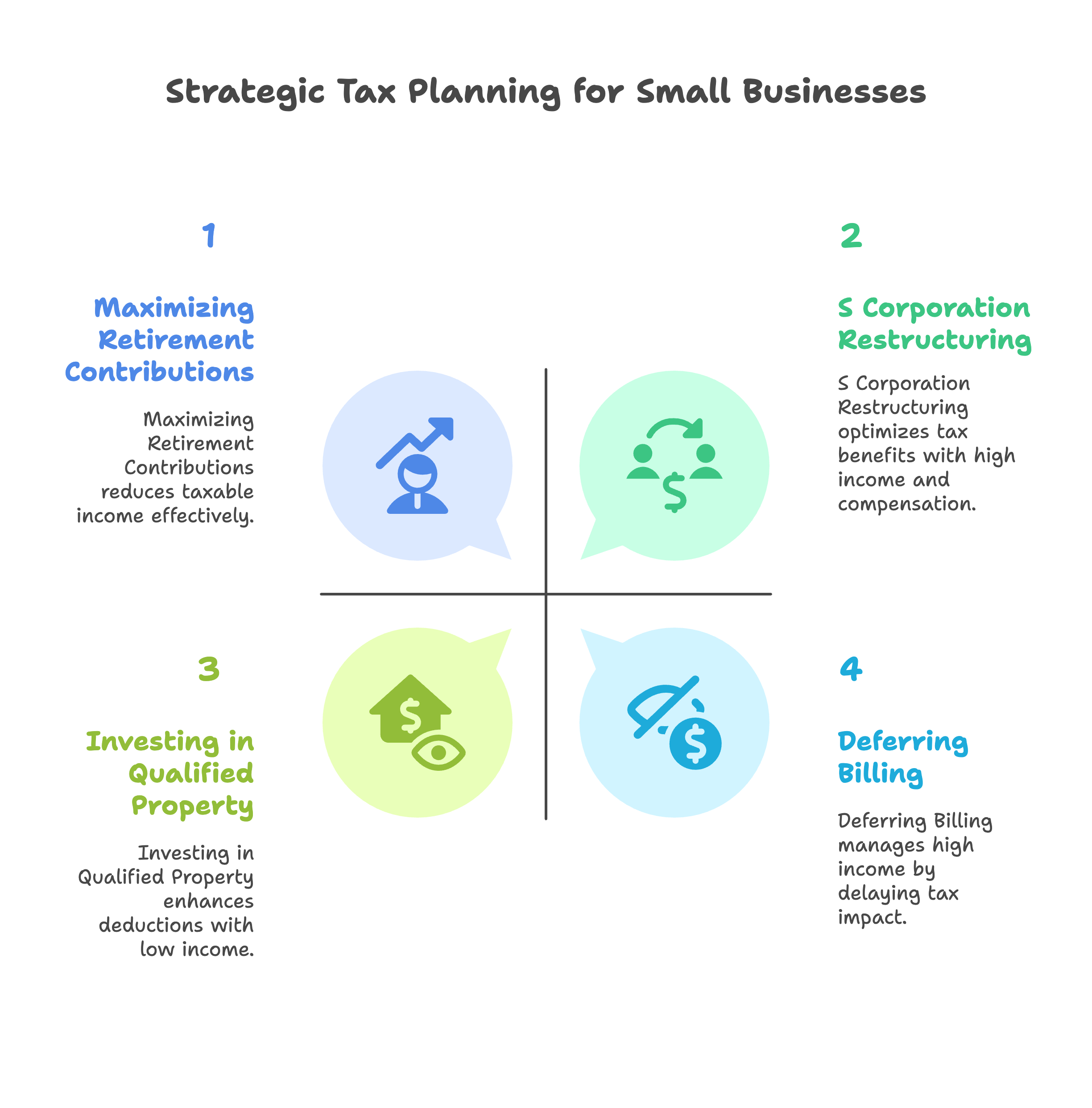

Even with limitations, most small businesses can take proactive steps to structure their operations for optimal tax savings.

If your taxable income is near the limit, explore strategies like:

Lowering your taxable income by even a few thousand dollars could make the difference between getting the full deduction or missing out. Business owners who qualify below the thresholds can claim the deduction without wage or property limitations.

If you operate as an S corporation, the salary you pay yourself impacts your qualified business income. A lower salary increases QBI but must remain "reasonable" under IRS guidelines.

Balancing your W-2 wages and distributions can help optimize the deduction while staying compliant. This strategy particularly helps pass-through entities that qualify for section 199a benefits.

Businesses with limited wages can still qualify using the property-based calculation. Investing in eligible equipment or machinery not only supports operations but also opens the door to a higher deduction.

Some taxpayers benefit from restructuring their business. For example:

Work with a CPA who understands your industry and can model these scenarios properly to help you qualify for maximum benefits.

Claiming the 199a deduction requires careful documentation. Audits around this deduction have increased, and errors can lead to penalties or lost benefits.

Here are best practices:

Use reliable accounting software or outsourced services to ensure everything is recorded accurately and consistently.

At Madras Accountancy, we help CPA firms handle QBI calculations, test compliance with limitations, and prepare supporting documentation through our offshore processing teams.

It is important to know that many states do not conform to the federal section 199a deduction. That means you may receive the deduction benefit at the federal level, but your state taxable income may not be affected.

Some states have introduced their own versions of pass-through entity deductions or workarounds for the SALT (state and local tax) cap. Coordination with a state-specific tax professional is recommended to understand your overall liability.

CPA firms working with small business clients must be proactive when it comes to the 199a deduction. This includes:

Given the complexity and calculation intensity, many firms choose to outsource 199a support to offshore teams like Madras Accountancy. This allows firms to:

The section 199a deduction becomes more complex in certain situations:

Business owners who operate multiple pass-through businesses must calculate the deduction separately for each qualified trade or business, then combine the results. Each entity must qualify independently, and losses from one cannot offset gains from another for deduction purposes.

Whether rental real estate activities qualify as a trade or business for section 199a purposes depends on the level of activity and involvement. Passive rental activities typically do not qualify, but more active rental businesses may qualify for the deduction.

Pass-through entities owned by trusts or estates have special rules for calculating the deduction. The deduction may be allocated between the trust and beneficiaries based on the distribution of qualified business income.

When claiming the deduction, business owners should avoid these common errors:

The section 199a deduction can be a game-changer for small business owners, but only if it is applied correctly. With thresholds, wage limits, SSTB restrictions, and property tests in play, even experienced business owners and advisors can miss opportunities or fall out of compliance.

By understanding the rules and working with knowledgeable professionals, businesses can claim the deduction with confidence. Whether you are optimizing compensation, structuring new entities, or planning purchases of qualified property, there is room to make the numbers work in your favor.

The key is to understand whether you qualify under the various tests and limitations, properly calculate your qualified business income, and maintain adequate documentation to support your position.

At Madras Accountancy, we provide white-labeled offshore accounting support to U.S. CPA firms, helping them manage section 199a compliance, optimize client returns, and handle complex calculations at scale.

If your firm is looking for reliable, experienced partners to help maximize tax credits and deductions, we are ready to support you.

Question: What is the Section 199A deduction and which businesses qualify for this tax benefit?

Answer: The Section 199A deduction, also known as the qualified business income (QBI) deduction, allows eligible taxpayers to deduct up to 20% of qualified business income from pass-through entities including sole proprietorships, partnerships, S corporations, and some trusts. The deduction applies to domestic business income and doesn't require additional investment or hiring. Qualifying businesses include most trades or businesses operated as pass-through entities, though specified service trades or businesses (SSTBs) face income limitations. The deduction is available through 2025 unless extended and provides significant tax savings for eligible taxpayers with qualified business income.

Question: What income limitations and thresholds apply to the Section 199A deduction?

Answer: Section 199A deduction limitations include taxable income thresholds of $182,050 for single filers and $364,100 for married filing jointly in 2023 (indexed annually for inflation). Below these thresholds, taxpayers generally qualify for 20% deduction on QBI without additional limitations. Above threshold amounts, deductions face more complex calculations involving W-2 wages and qualified property limitations. Specified service businesses (SSTBs) face complete phase-out of benefits above threshold amounts. The deduction cannot exceed 20% of taxable income minus net capital gains, creating an overall limitation for high-income taxpayers.

Question: What are specified service trades or businesses (SSTBs) and how do they affect the deduction?

Answer: Specified service trades or businesses (SSTBs) include health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, and businesses where reputation or skill of owners is the principal asset. SSTBs face complete phase-out of Section 199A benefits for taxpayers above income thresholds ($182,050 single, $364,100 married filing jointly). The phase-out occurs over ranges ending at $232,050 single and $464,100 married filing jointly. Engineering and architecture are specifically excluded from SSTB classification. Businesses should carefully analyze activities to determine SSTB status and plan accordingly for income threshold management.

Question: How do W-2 wages and qualified property limitations affect the Section 199A deduction?

Answer: For taxpayers above income thresholds, the Section 199A deduction is limited to the greater of 50% of W-2 wages paid by the business or 25% of W-2 wages plus 2.5% of the unadjusted basis of qualified property. These limitations only apply to non-SSTB businesses above threshold amounts. W-2 wages include all wages subject to federal income tax withholding paid by the business. Qualified property includes tangible property subject to depreciation used in the business and not fully depreciated. These limitations can significantly reduce available deductions for businesses with low W-2 wages or minimal qualified property.

Question: What strategies can businesses use to maximize their Section 199A deduction?

Answer: Maximize Section 199A deduction through income timing strategies, entity structure optimization, W-2 wage planning, and qualified property investments. Consider converting from sole proprietorship to S corporation for wage optimization, timing income and deductions to stay below thresholds, and investing in qualified depreciable property to increase basis limitations. Separate SSTB activities from non-SSTB activities through entity structuring, consider family employment to increase W-2 wages, and optimize retirement plan contributions to reduce taxable income. Professional planning helps navigate complex rules while maximizing available benefits within legal parameters.

Question: How do partnerships and S corporations calculate and allocate Section 199A benefits?

Answer: Partnerships and S corporations calculate Section 199A items at the entity level and report them separately to owners on Schedules K-1. Entities must separately state QBI, W-2 wages, unadjusted basis of qualified property, and any SSTB designations. Allocations must follow partnership agreement or S corporation ownership percentages. Entities should maintain detailed records for W-2 wages and qualified property to support owner deductions. Special rules apply for aggregation of multiple businesses, rental real estate activities, and publicly traded partnerships. Proper reporting and allocation procedures ensure owners receive accurate information for individual tax return calculations.

Question: What documentation and record-keeping requirements apply to Section 199A deductions?

Answer: Section 199A documentation requirements include maintaining detailed records of business income and expenses, W-2 wage reports, qualified property basis and depreciation schedules, and SSTB activity classifications. Keep separate records for each business activity, document aggregation elections and supporting analysis, and maintain payroll records supporting W-2 wage calculations. Property records should include acquisition dates, costs, depreciation methods, and disposition information. Document business activity descriptions, time allocation for multiple activities, and professional analysis supporting SSTB determinations. Proper documentation supports deduction claims and provides protection during potential IRS examinations.

Question: What common mistakes should taxpayers avoid when claiming Section 199A deductions?

Answer: Common Section 199A mistakes include incorrectly classifying SSTB activities, failing to properly track W-2 wages and qualified property, misunderstanding aggregation rules, and overlooking taxable income limitations. Avoid claiming deductions without proper entity-level reporting, misallocating items between business and investment activities, and failing to consider overall taxable income limitations. Don't ignore rental real estate safe harbor elections, incorrectly aggregate unrelated businesses, or claim deductions for guaranteed payments or reasonable compensation. Professional guidance helps navigate complex rules and avoid costly errors while ensuring maximum legitimate benefits under current regulations.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.