You work hard, profits are finally steady, and now the question hits: what’s the most tax-efficient way to pay yourself without tripping payroll rules, overpaying social taxes, or making your first audit a nightmare? This guide gives US and UK owner-managers a clean, side-by-side playbook for 2025 so you can choose the right mix of salary, dividends, pensions/retirement, and benefits; especially if your team or vendors sit offshore.

What this section covers

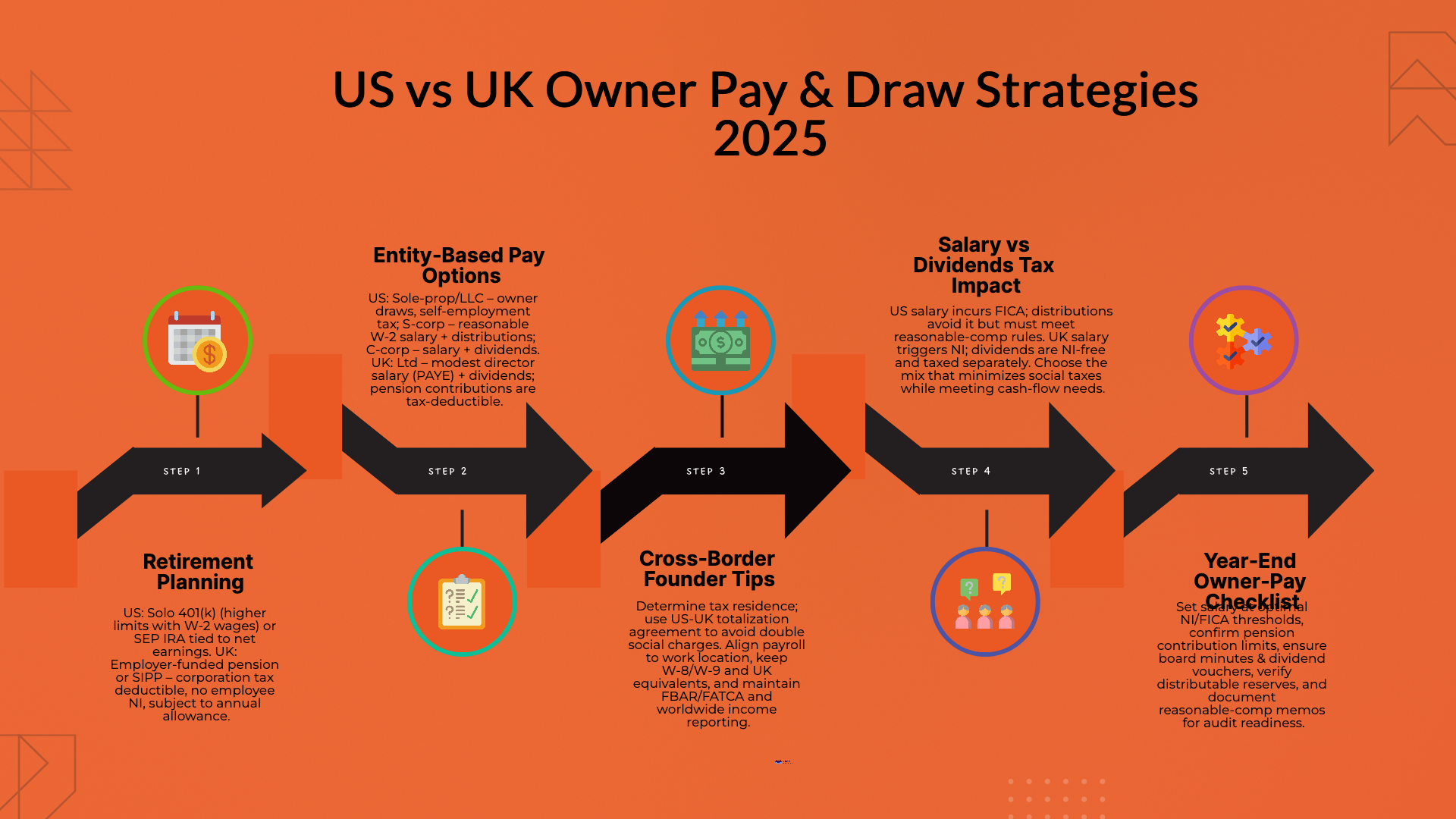

- Owner compensation options by entity type in the US and UK

- How FICA/self-employment tax compares to UK National Insurance (NI)

- When to use dividends/distributions vs salary

- Retirement schemes (Solo 401(k), SEP, workplace pension, SIPP) and who can contribute

- Benefits, deductions, and common traps for cross-border founders

Key definitions you will use (plain English)

- Salary (Payroll). Pay subject to withholding. In the US it attracts FICA (Social Security + Medicare) or self-employment tax. In the UK salary goes through PAYE and National Insurance (NI).

- Dividends / Distributions. Owner profit withdrawals. US tax depends on entity type; UK dividends are separate from salary and not subject to NI.

- Reasonable Compensation (US S-corp). The IRS expects S-corp owner-employees to take a market-rate salary before distributions.

- Workplace Pension (UK). Employer pension contributions for directors/employees; typically deductible for the company and not subject to employee NI. A SIPP is a personal pension you or the company can fund within UK limits.

- Solo 401(k) / SEP IRA (US). Owner-only retirement plans with high annual limits tied to W-2 wages (Solo 401(k)) or net earnings (SEP).

Owner pay at a glance: entity vs options

JurisdictionEntity (common)How owners usually pay themselvesSocial tax exposureNotesUSSole Prop / LLC (default)Owner draws; no W-2 salarySelf-employment tax on business profitSimpler, but all profit faces SE tax; retirement via SEP or Solo 401(k) if eligibleUSLLC taxed as S-corpW-2 salary + distributionsSalary subject to FICA; distributions notMust support “reasonable comp”; enables Solo 401(k) with higher deferralsUSC-corpW-2 salary + dividendsFICA on salary; no FICA on dividendsDouble tax risk at corp + shareholder levels; useful for reinvestment or benefitsUKLimited CompanyDirector salary (often modest) + dividendsSalary subject to NI; dividends no NICompany pension contributions are often NI-efficient; dividends taxed separately

Always model with current-year thresholds and bands for 2025 before deciding.

Strategy patterns that actually move the needle

US playbook (owner-managed, profitable, stable)

- S-corp split (salary + distributions).

- Pay a market-based W-2 salary for your role.

- Take periodic distributions once salary is in place. This may reduce exposure to self-employment tax compared with a default LLC, while keeping income tax on total profits.

- Keep a comp file: role description, market data, time records.

- Retirement first, then perks.

- Solo 401(k) usually beats SEP when you pay W-2 wages, because employee deferrals are not tied to the profit calc and can front-load savings.

- Add employer contributions up to annual limits once cash allows.

- Health and fringe benefits.

- Self-employed health insurance deduction may apply.

- For >2% S-corp owners, fringe benefit rules are special—track in payroll correctly (e.g., shareholder health).

- §199A QBI check.

- Test eligibility and wage/UBIA limitations. Your salary level affects the deduction; run the calc before year-end.

- State payroll and nexus.

- If your team works across states or offshore, confirm state UI and withholding obligations and contractor rules.

UK playbook (owner-managed limited company)

- Director salary at efficient band + dividends.

- Set salary around thresholds that secure a qualifying NI year while keeping NI cost efficient.

- Pay dividends on retained profits after corporation tax; dividends do not attract NI.

- Company-paid pension contributions.

- Employer pension payments for directors are typically corporation tax deductible and outside employee NI, subject to wholly-and-exclusively, annual allowance, and any tapering.

- A SIPP can be funded by the company or personally; plan around allowances.

- Benefits and P11D/Class 1A NI.

- Cash vs benefit trade-offs matter; some benefits trigger Class 1A NI.

- Use trivial benefits carefully and capture everything on P11D where required.

- Dividends admin.

- Keep board minutes, dividend vouchers, and interim accounts to support distributions.

Cross-border founders: keep these in view

- Tax residence and treaty ties. Your residence drives where you pay and how credits apply. Use the US–UK treaty tie-breaker if needed.

- Social security totalization. The US and UK have a totalization agreement; with the right certificate you can often avoid double social charges on the same earnings.

- Payroll where you work. If you physically work in both countries, you may trigger payroll in both unless the treaty and certificates are in place.

- Company vs personal contributions. In the UK, company pension contributions can be more NI-efficient than extra salary. In the US, Solo 401(k) limits depend on W-2 pay; too-low salary caps your deferral.

- Withholding and forms. Keep W-8/W-9, 1099/1042-S and UK equivalents correct for any cross-border payments.

- Reporting hygiene. FBAR/FATCA (US) and worldwide income rules (UK) still apply even if you operate through companies.

When to favor salary vs dividends/distributions

GoalUS leaningUK leaningWhyMax retirement savings this yearHigher W-2 salary + Solo 401(k)Company pension contributionsSalary enables bigger 401(k) deferrals; UK employer pension avoids employee NIReduce social tax on mature profitsS-corp distributions after reasonable salaryLower salary + dividendsDistributions (US S-corp) and dividends (UK) are outside FICA/NIQualify for mortgages/visasHigher salary, steady W-2Steady PAYE salaryUnderwriters favor consistent payroll incomeSimplify admin in year 1Default LLC or payroll-onlyPAYE salary onlyFewer moving parts while processes matureAudit readinessDocument reasonable comp; payroll/tax reconciliationsMinutes, dividend vouchers, PAYE/RTI reconciliationsEvidence keeps year-end clean

Example workflows you can copy

US S-corp monthly rhythm

- Run payroll at agreed reasonable salary.

- Post employer taxes and retirement contributions.

- Quarterly, declare owner distributions based on cash and projected tax.

- Maintain a reasonable comp memo and board acknowledgment.

UK Ltd monthly rhythm

- Run PAYE for director salary; pay RTI on time.

- Fund employer pension to planned schedule.

- Quarterly, assess profits and declare dividends with minutes and vouchers.

- File P11D/Class 1A where benefits exist.

Common traps (and how to avoid them)

- US: Paying tiny S-corp salaries with large distributions. The comp file should stand on its own.

- US: Missing state payroll registrations where remote staff sit.

- UK: Declaring dividends without sufficient distributable reserves.

- UK: Paying personal expenses through the company without correct benefit treatment.

- Both: Underfunding retirement because salary was set too low to allow desired contributions.

- Both: No board minutes or resolutions supporting key owner-pay decisions.

Quick checklist before year-end

- Salary set at the right thresholds for your plan (US FICA base tests; UK NI bands).

- Retirement contribution plan agreed and timed before deadlines.

- Board minutes and dividend/distribution paperwork complete.

- PBC trail ready: payroll reports, tax filings, pension statements, dividend vouchers, comp memo.

- Cross-border residency and totalization confirmed for the current year.

Takeaway

If you want a numbers-backed plan tailored to your profits, residency, and team location, Madras Accountancy will model Small Business Tax Planning 2025: US vs UK Owner Pay & Draw Strategies, set salary/dividend bands, map FICA vs NI, and schedule retirement and benefits so you stay compliant and efficient.

%2075-100%20(12).png)

%2075-100%20(9).png)