.png)

Choosing between an S Corporation (S Corp) and a sole proprietorship might seem like a formality, but it's one of the most important financial decisions a small business owner can make.

This choice doesn't just affect how you register your business. It shapes how you pay taxes, how much personal risk you carry, how easily you can raise money, and even how much credibility you have with clients or lenders.

And while a sole proprietorship is the easiest way to start a business, an S Corp can unlock major tax advantages, if you've reached the right stage in your business journey.

In this guide, we'll break down:

Whether you're freelancing full-time or scaling a growing business, this comparison will help you understand which option fits your real-life goals and numbers.

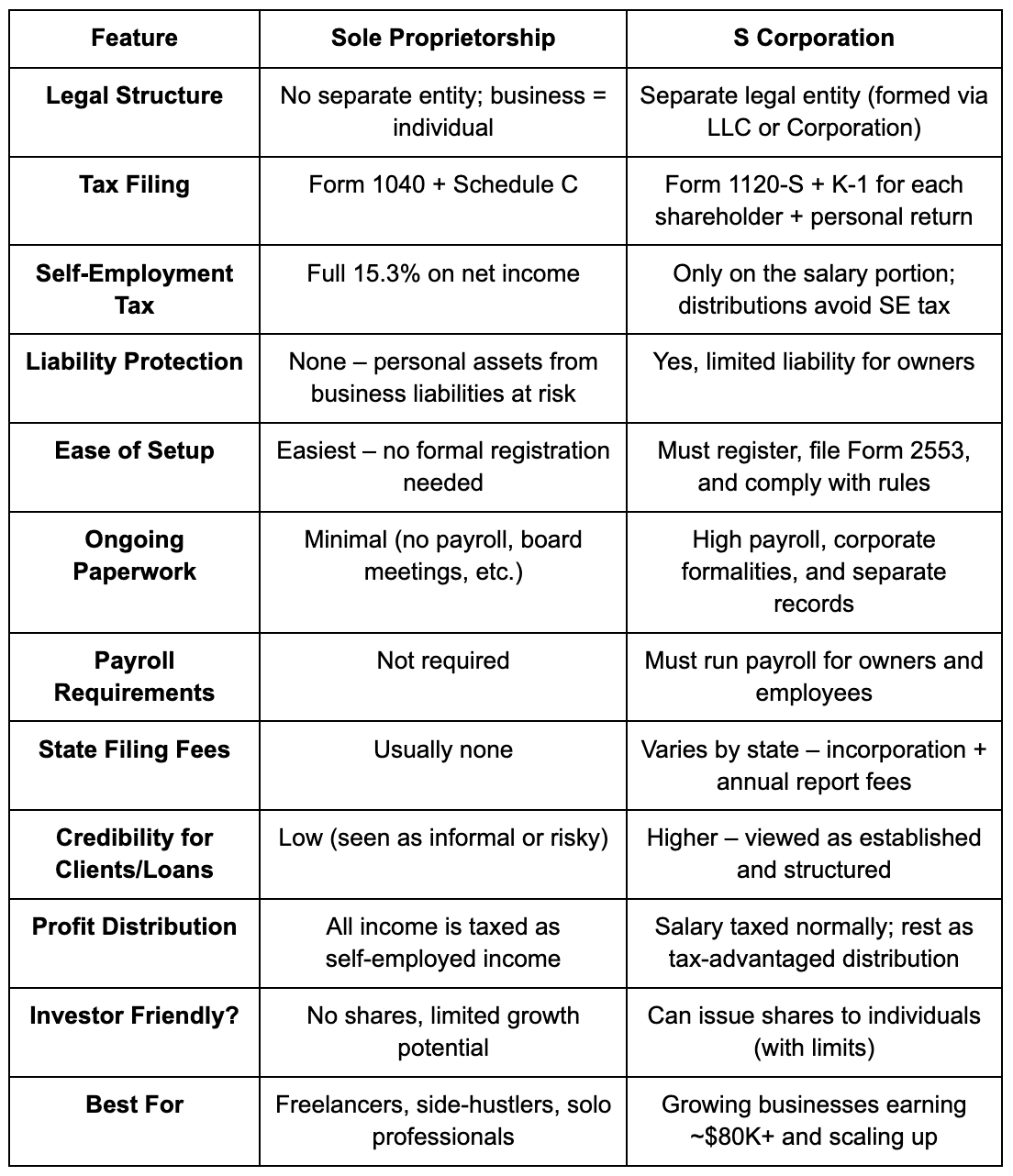

A sole proprietorship is the simplest form of business structure in the United States. It's not a formal legal entity like an LLC or corporation, instead, it's simply an individual operating a business under their name or a registered trade name.

There's no legal separation between the business and the owner. You don't need to file formation documents with the state, and there are no separate tax filings for the business. This makes it the easiest and least expensive structure to start with, but also the riskiest.

This setup works well for low-risk ventures or people testing an idea. Freelancers, consultants, tutors, and side hustlers often start when they operate their business as a sole proprietorship.

Sole proprietors don't file a separate business tax return. Instead:

Self-employment tax is currently 15.3% on net earnings. This is in addition to federal and state income taxes, which makes tax planning essential even at early stages.

This form of business makes sense when:

An S Corporation, or Subchapter S Corporation, is not a business entity itself; it's a tax classification you make with the Internal Revenue Service after forming a corporation or limited liability company (LLC). When you elect S Corp tax status (by filing Form 2553), your business avoids double taxation by passing income, losses, deductions, and credits directly to shareholders for federal tax purposes.

Unlike a sole proprietorship, an S Corp creates a separate legal and tax identity, offering liability protection and tax planning advantages, but also comes with more rules, paperwork, and scrutiny.

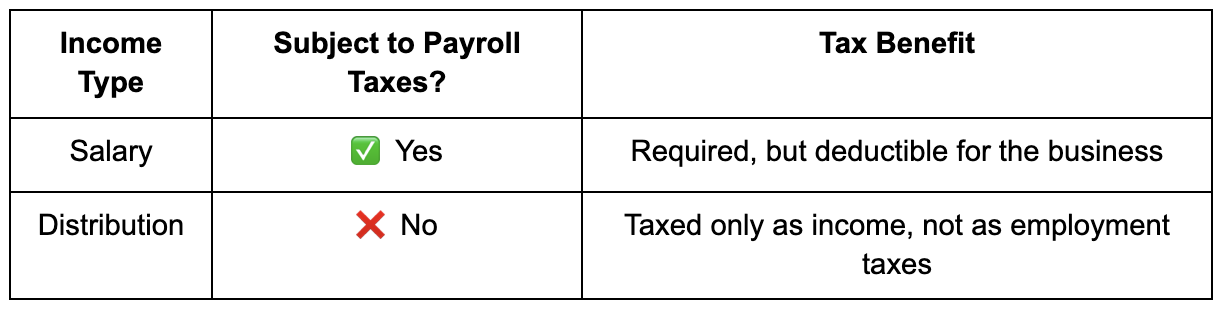

Here's where S Corps shine, tax efficiency for profitable businesses.

S Corp owners split their income into:

This allows substantial potential tax savings once your business is earning $80K+ in net profit.

⚠️ But: The Internal Revenue Service closely monitors this. You must pay a "reasonable" salary based on your role, industry, and revenue. Underpaying yourself just to avoid taxes = audit risk.

Operating as an s corporation isn't as simple as freelancing. You'll need to:

These add both cost (for payroll/bookkeeping software or accountants) and operational complexity.

When you choose a business structure, you're not just making a legal decision, you're making a tax decision. The Internal Revenue Code provides different tax treatments for different entity types, and understanding these differences is crucial for many business owners.

Here's how the main structures compare:

Each structure has unique tax implications:

A tax professional or tax specialist can help you understand which structure best fits your business needs and provides the most favorable tax treatment.

Let's say you earn $100,000 in net profit as a freelancer.

As a Sole Proprietor:

As an S Corp:

This demonstrates why transitioning to an s corporation can make financial sense despite the admin work, especially once net profits cross the $80K mark.

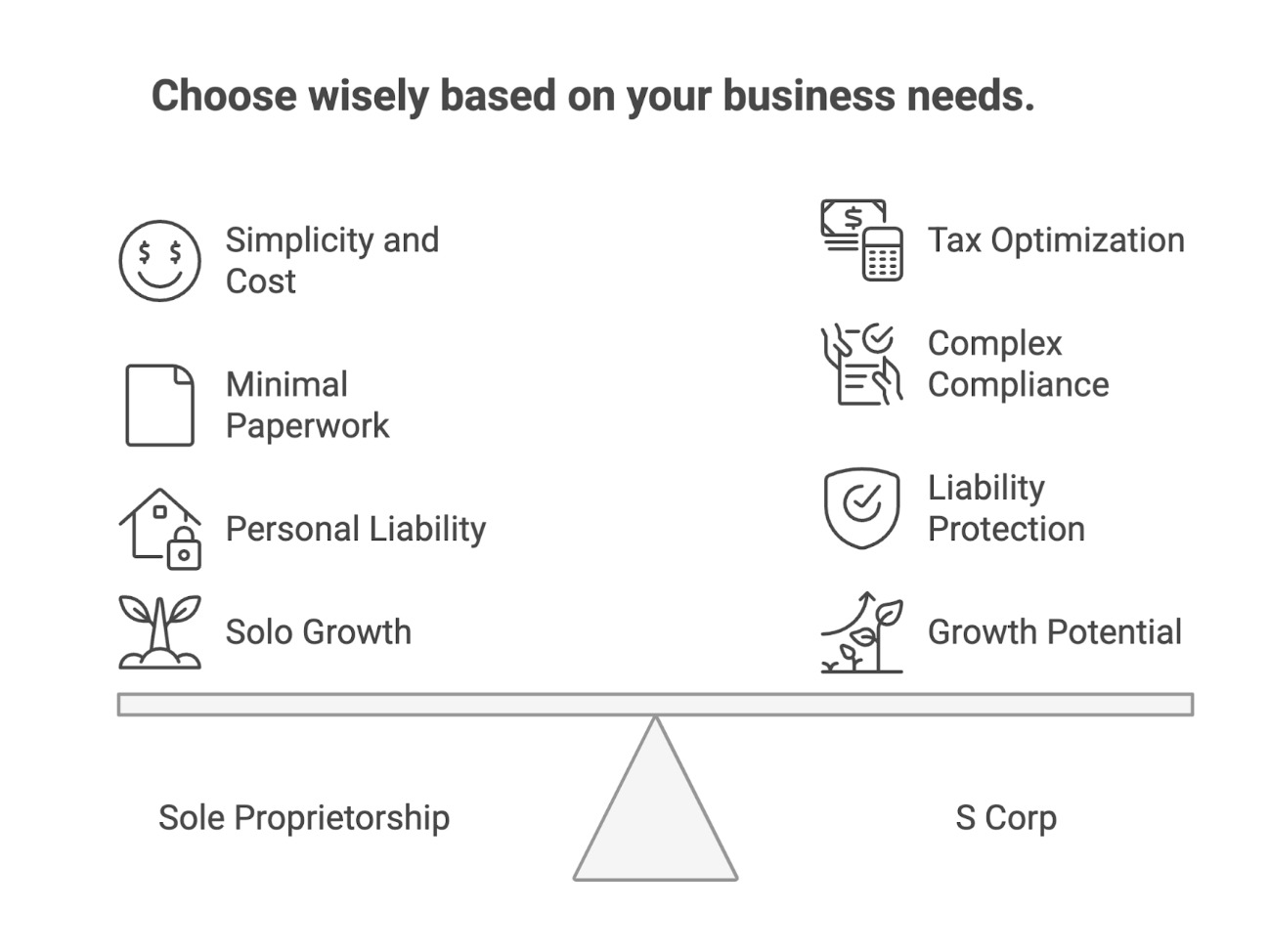

There's no one-size-fits-all answer here, and if you're running a business in the U.S., the structure you choose impacts how much tax you pay, how much risk you carry, and how much complexity you're signing up for.

So let's break it down using real decision factors that founders and freelancers face when selecting a business structure.

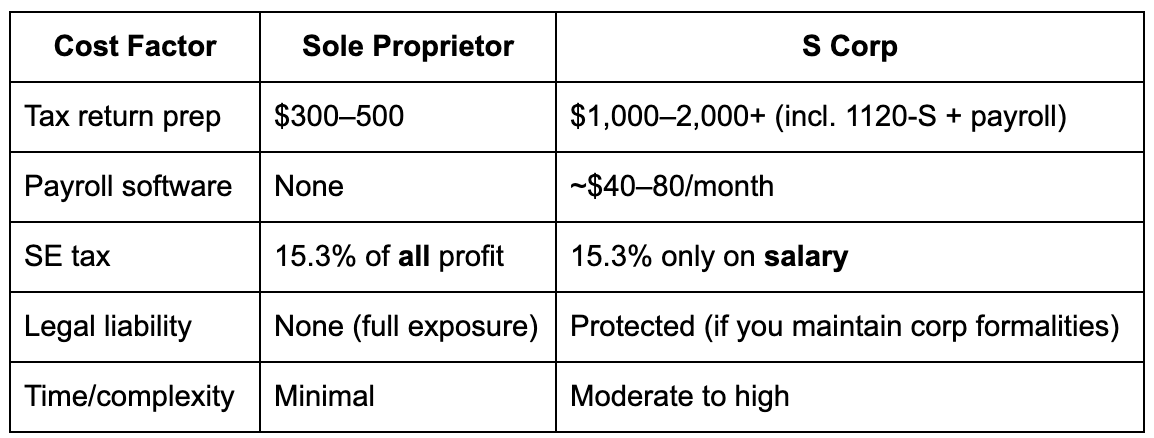

If you're earning under $60,000/year in net income, an S Corp probably isn't worth it. You'll add extra costs (payroll, bookkeeping, tax filings) that eat into any potential tax savings.

But if you're crossing $80,000+ in profit, it's time to seriously consider switching. That's the point where the S Corp election can reduce your self-employment taxes by thousands and provide lower tax benefits overall.

💡 Quick math: As a sole proprietor, you pay 15.3% SE tax on all profit. As an S Corp, you only pay that on your salary, not your distributions. Big difference once your profit grows.

Sole Proprietorship:

✅ Simple to run

✅ No separate tax return

✅ No payroll headaches

S Corp:

🚧 You must pay yourself a "reasonable salary" via payroll (which means using Gusto or similar)

🚧 You file a 1120-S corporate tax return

🚧 You need to keep basic records (minutes, bylaws , even if it's just you)

So if you want to keep things lean and spend less on accountants, the sole prop is your best friend. But if you're fine trading simplicity for tax optimization, an S Corp works.

This is where S Corp wins, liability protection.

Sole proprietorship = you are the business.

If you're sued, your house, savings, and car are fair game.

S Corp (via an LLC or corporation) = personal and business assets are separate.

Creditors and lawsuits can't touch your assets unless you've commingled funds or done something shady.

If you're offering services, handling client data, or shipping products, protecting yourself matters, even if you're small.

This is less about size and more about intent.

If you're freelancing, side hustling, or consulting solo, and don't expect major team growth, → Sole Proprietorship makes sense.

If you're hiring, building a real brand, or want to raise funding to grow your business → S Corp (via LLC or Inc) gives you credibility and legal structure to grow.

Choose Sole Proprietorship if:

→ You're just starting out

→ You want simplicity

→ Your net profit is under ~$70K/year

Switch to S Corp if:

→ Your profits are consistent and above ~$80K

→ You want liability protection

→ You're ready to deal with payroll and compliance

Understanding the sole proprietorship vs s corp decision is crucial for optimizing your tax strategy and protecting your business interests.

Whether you're just launching your business or restructuring for tax efficiency, understanding the formation process for both Sole Proprietorships and S Corporations is critical. Below is a step-by-step breakdown of how each is set up and what ongoing obligations come with them.

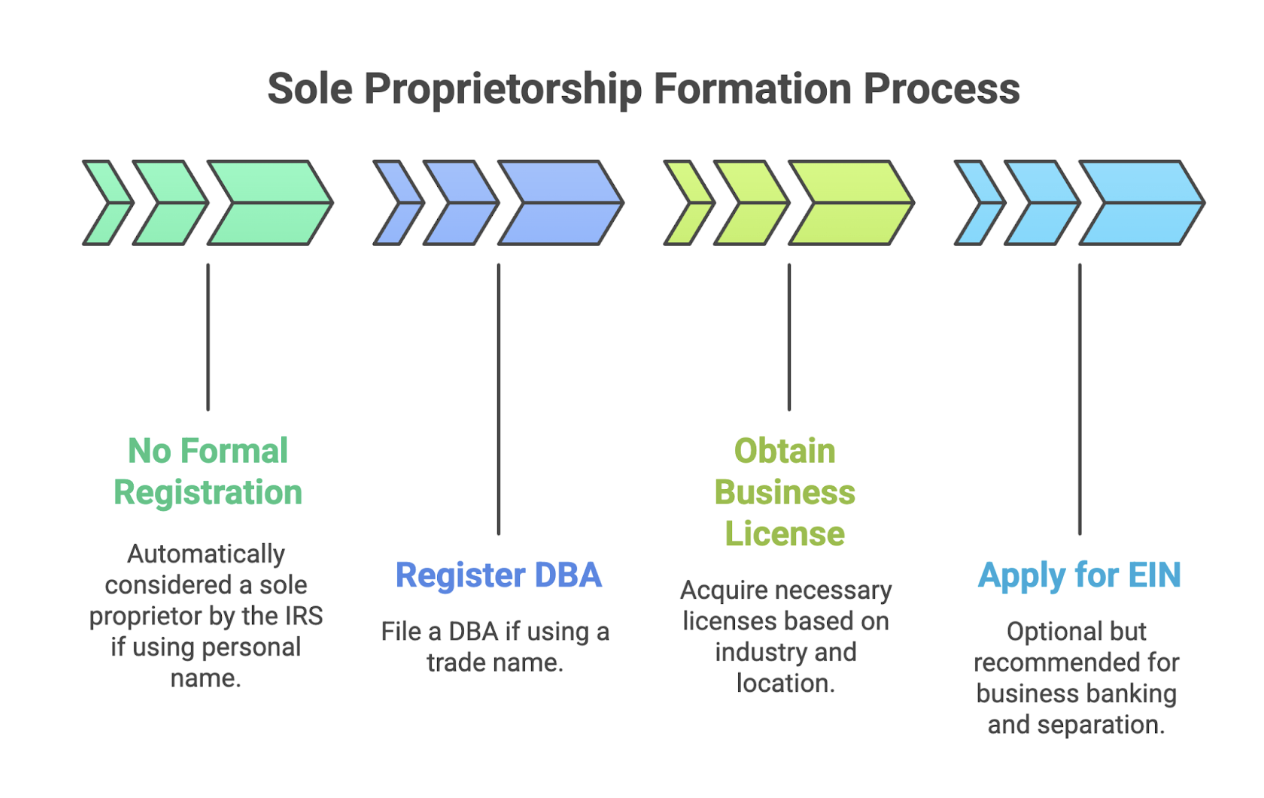

If you're doing business under your name, you're automatically considered a sole proprietor by the IRS. There's no paperwork required at the federal level.

If you're using a name other than your name, you'll likely need to file a DBA with your city, county, or state. Fees usually range from $10–$100.

Depending on your industry (e.g., food service, cosmetology, retail), local or state licenses may be needed. This varies widely by location.

You can use your SSN when you file your taxes, but applying for an Employer Identification Number (EIN) helps you open a business bank account and build separation between personal and business activities.

Setup Time: 1–5 business days

Cost: Often <$100 (plus any local license fees)

Ongoing Compliance: Minimal (no separate tax filings unless you hire employees)

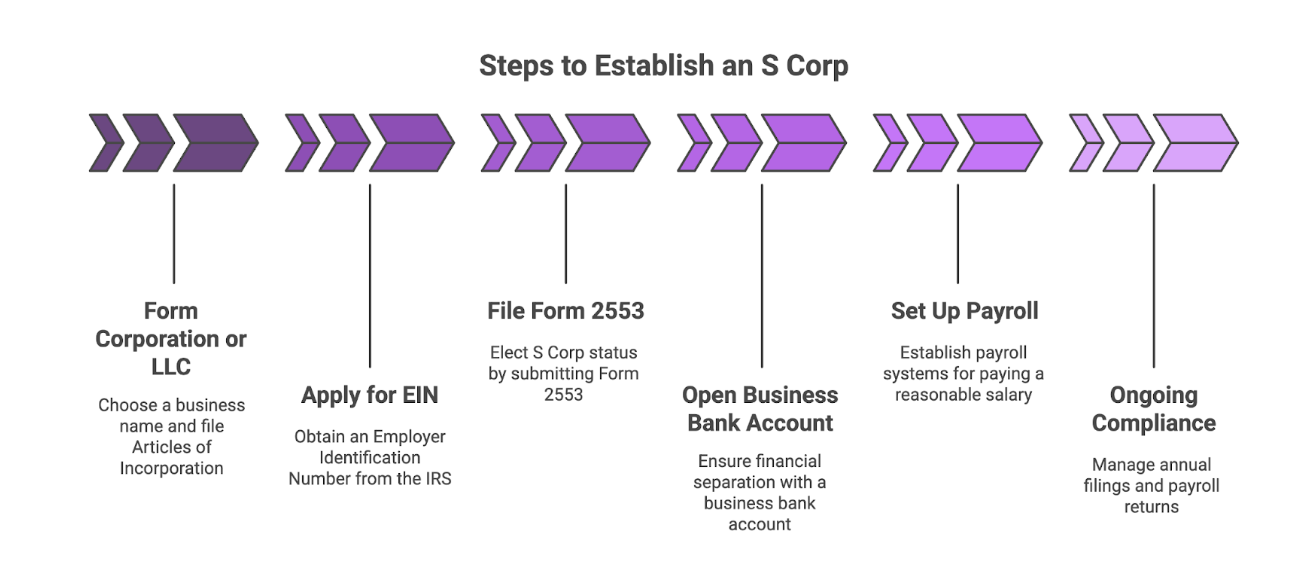

You can't elect S Corp tax status directly, you must first incorporate as a general corporation (Inc.) or an LLC at the state level.

All S Corps need an EIN, regardless of employee count.

This form must be submitted within 75 days of incorporation or the beginning of the tax year you want S Corp treatment. All corporation shareholders must consent.

This ensures financial separation, especially important for pass-through taxation.

S Corp owners must pay themselves a salary, subject to payroll tax, before taking distributions. That requires setting up payroll systems or using a payroll provider.

Setup Time: 1–3 weeks

Cost: $500–$1,500+ (if using legal help + payroll setup)

Ongoing Compliance:

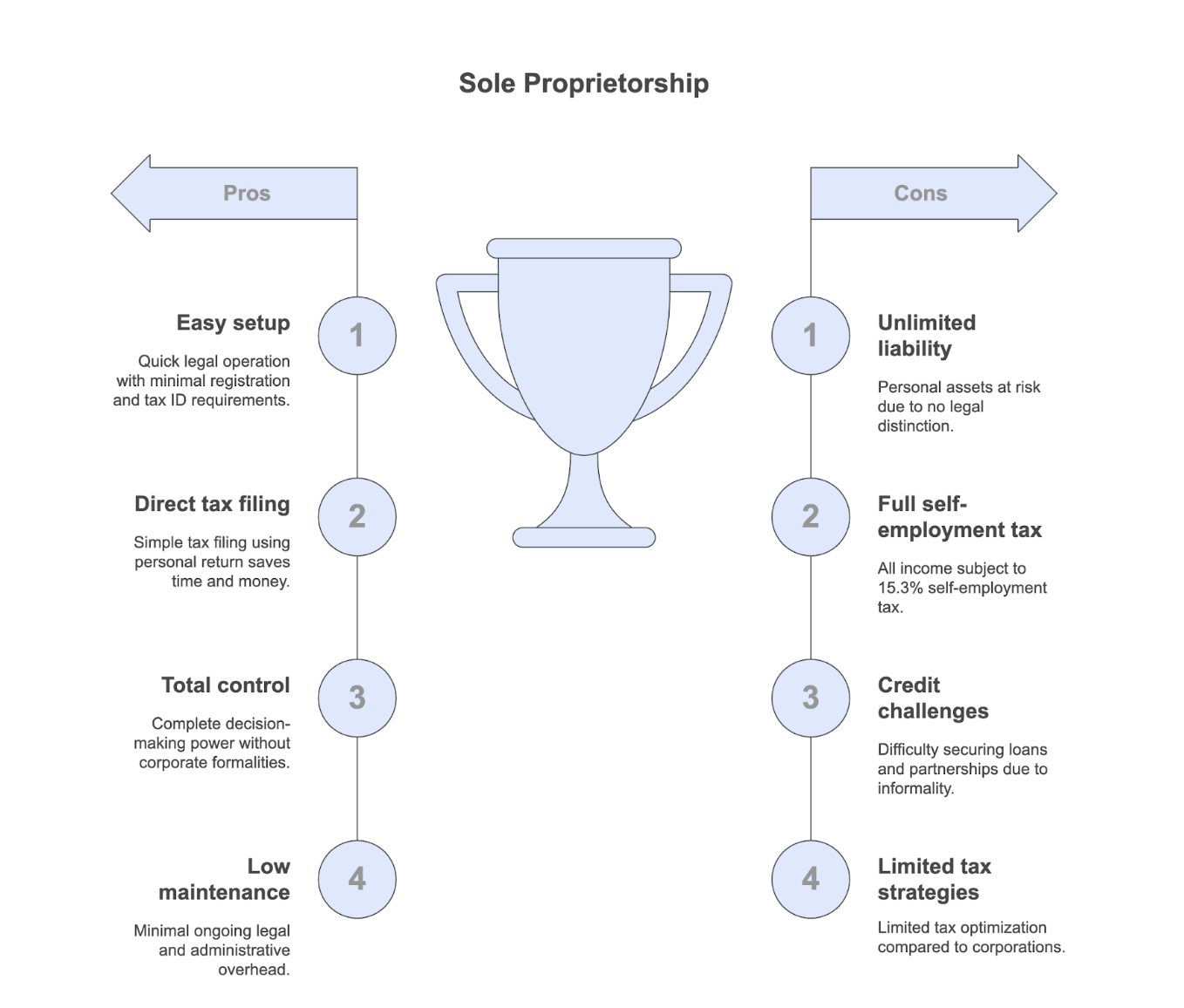

Starting a sole proprietorship is straightforward, no state-level registration (unless using a fictitious name), no separate business tax ID needed. For freelancers, consultants, and solo service providers, it's the quickest path to operating legally.

You report business profits or losses on your Form 1040 using Schedule C. There's no separate business return, which saves time and money during tax season.

As the sole owner, you make all decisions. There are no corporate formalities or shareholder obligations to manage.

No need to file annual reports or hold board meetings. It's simple to run and requires minimal legal or administrative overhead.

There's no legal distinction between you and your business. If your business is sued or goes into debt, your assets (like your home or savings) are at risk.

All net income is subject to 15.3% self-employment tax, covering both Social Security and Medicare. There's no option to classify any part of your income as distributions.

Banks and investors often view sole proprietorships as informal, which can make it harder to secure loans, lines of credit, or partnerships.

You can't separate your salary from business profits or leverage tax deferral strategies available to corporations. All profits are taxed as personal income.

S Corp owners only pay self-employment taxes on their "reasonable salary." The remaining profit, taken as distributions, isn't subject to these taxes, offering significant savings as income scales.

Your personal assets are generally shielded from business-related lawsuits or debts, assuming corporate formalities are properly maintained.

Incorporating can help build trust with clients, vendors, and financial institutions. It signals that you're operating a formal business, growth-oriented business.

With an S Corp, you can explore retirement plan contributions through the business, health reimbursement arrangements, and other tax-efficient strategies.

You'll need to file incorporation documents, draft bylaws, issue shares, and file annual reports. Corporate compliance isn't optional, it's mandatory.

Even as an owner, you must pay yourself a reasonable W-2 salary, which means setting up payroll systems and filing quarterly employment tax returns.

S Corps must file Form 1120-S and issue Schedule K-1s to shareholders. This adds complexity and usually requires professional tax help.

An S Corp can't have more than 100 shareholders, and all must be U.S. citizens or residents. You also can't issue multiple classes of stock.

Choosing between an S Corporation and a Sole Proprietorship isn't just about paperwork, it's about how you want to operate, grow, and protect your business.

If you're testing a side hustle, freelancing casually, or just want to get started with minimal hassle, a sole proprietorship keeps things simple.

But if you're earning steady profits, want to optimize for taxes, and plan to grow with limited liability, an S Corp offers more long-term benefits, despite the extra admin.

There's no one-size-fits-all answer. Your business model, income level, risk tolerance, and plans for scaling all matter when you choose a business structure.

Understanding the tax implications and working with a tax professional can help ensure you make the right decision for your specific situation. Whether you're comparing sole proprietorship and s corp options or considering other business structures, getting expert guidance can save you money and protect your interests long-term.

Madras Accountancy offers tailored entity structuring, tax planning, and ongoing compliance support, built specifically for small businesses and independent professionals across the U.S.

📞 Get in touch for a free consultation, and let's figure out what's best for your business future.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.