.png)

Estate planning isn't just about wills and trusts; it's about location. While the federal estate tax only applies to estates over $13.61 million (as of 2025), many states still impose their own state estate tax or inheritance taxes on much smaller estates. And that can quietly cost your heirs thousands, or even millions.

So here's the big question: What states have no estate tax? And which ones also avoid inheritance tax altogether?

This guide breaks it down clearly:

Whether you're planning a relocation, preparing for retirement, or optimizing your trust strategy, knowing your state's tax laws is essential.

Let's walk through the smart estate tax map.

When it comes to preserving generational wealth, understanding the difference between estate tax and inheritance tax isn't just semantics; it's a financial strategy. These two taxes operate differently, apply in different states, and impact different parties. Here's how they work, what triggers them, and why the distinction matters so much for high-net-worth families and estate planners.

Definition: The estate tax is a tax on the total value of the estate of a deceased person before any assets are passed on to heirs. It's paid by the decedent's estate itself, not the recipients.

How It Works:

Upon death, your estate is assessed for its gross value, including real estate, investments, cash, business holdings, retirement accounts, and even certain insurance policies.

Deductions (like debts, funeral expenses, charitable contributions) reduce the total to create the individual's taxable estate.

If the estate exceeds the tax threshold, estate taxes apply before distribution.

2025 Federal Threshold:

Key Point: Only about 0.1% of estates in the U.S. owe federal estate tax, but many more fall into the trap of state-level estate taxes, which often kick in at much lower thresholds.

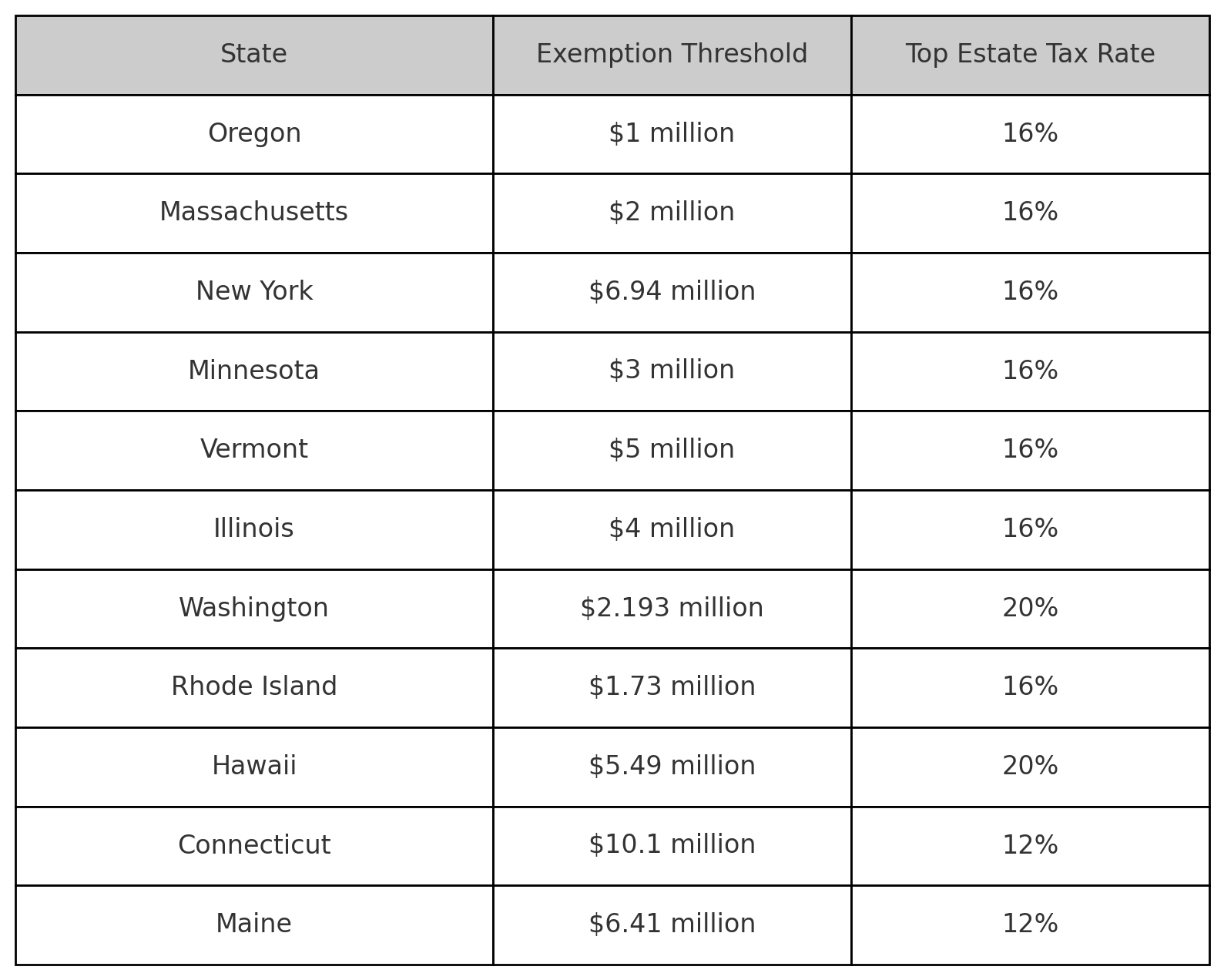

States that impose estate taxes: Twelve states + Washington, D.C., still impose their state estate tax in 2025, some starting at just $1 million. (We'll cover these states in the next section.)

Definition: Unlike the estate tax, the inheritance tax is levied on the person who receives the assets. That means your heirs, not your estate, are responsible for paying this tax. This is sometimes referred to as a "hidden tax" because many beneficiaries don't realize they may owe it.

How It Works:

After you die and your assets are distributed, the recipient may owe taxes depending on:

Progressive Rate Structure: State inheritance tax rates are typically graduated:

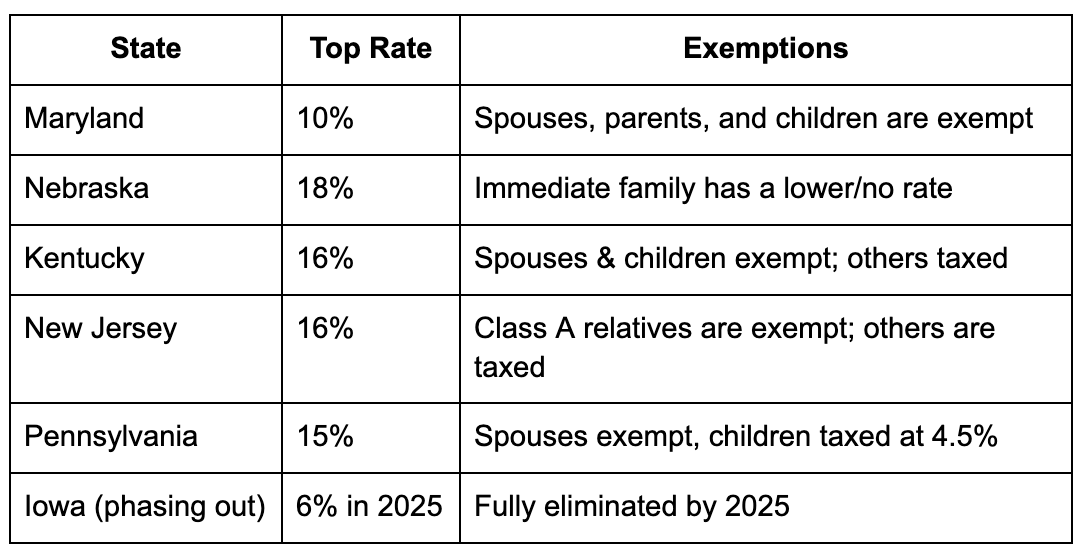

States with Inheritance Tax (2025): Only six states with inheritance tax currently levy inheritance tax: Iowa (phasing out its inheritance tax by 2025), Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania, each with its own exemption rules.

Both Taxes Can Apply: Yes, you can get hit with both. For example, Maryland is the only state that has both estate and inheritance tax, so your estate may be taxed first, and then your beneficiaries taxed again.

Your Residency Affects the Tax Outcome: Where you live and where your property is located can determine whether these taxes apply. A Florida resident (no estate or inheritance tax) with property in Oregon (an estate tax state) may still trigger estate tax liability in Oregon.

Relationship to the Deceased Matters: State and inheritance tax rates often favor immediate family. But if you're leaving assets to a niece, friend, or caregiver, they might owe a larger share to pay the state.

Gifting and Trusts Play a Role: Smart estate planning, including lifetime gifts, irrevocable trusts, and domicile planning, can help minimize or eliminate estate/inheritance taxes. But it requires knowing the rules early.

If you're planning your estate with an eye on long-term tax efficiency, location matters more than most people realize. In the U.S., both estate and inheritance taxes are imposed at the state level in addition to (or instead of) federal taxes. But not all states impose the tax, and some offer complete tax-free inheritance.

Here's a breakdown of where you're off the hook entirely in 2025:

As of 2025, 33 states with no inheritance tax or estate tax exist, meaning your assets can pass to heirs without any state-level tax consequences. These low taxes states are attractive options for estate planning.

These tax-free states include:

...and several more.

Pro tip: These states are popular not just for sunshine and retirement, but also for passing on wealth without erosion from state death taxes.

Twelve states + Washington, D.C. impose a state-level estate tax (but not inheritance tax):

The estate tax exemption threshold in these states is often much lower than the federal limit, as low as $1 million in MA and OR.

6 states impose an inheritance tax in 2025:

Inheritance tax rates in these states depend on:

Only Maryland has both types of taxes in 2025, making it one of the most aggressive states and the district in terms of taxing intergenerational wealth transfer.

The federal estate tax exemption amount for 2025 is $13.61 million per individual. This means that most estates won't pay estate taxes at the federal level. However, the Internal Revenue Service has scheduled this exemption to sunset after 2025, potentially reverting to around $6-7 million per person.

State estate tax exemption amounts vary significantly. While some states with no inheritance tax or estate tax offer complete exemption, others have much lower thresholds. For example:

Some states offer tax credits that can reduce your overall tax burden. Understanding both federal and state estate tax implications, as well as available tax credits, can help minimize the total tax liability.

While estate and inheritance taxes are separate from income tax, beneficiaries should understand that inherited assets may affect their income tax rates in the tax year they receive them. Consulting with an estate planning attorney can help navigate these complexities.

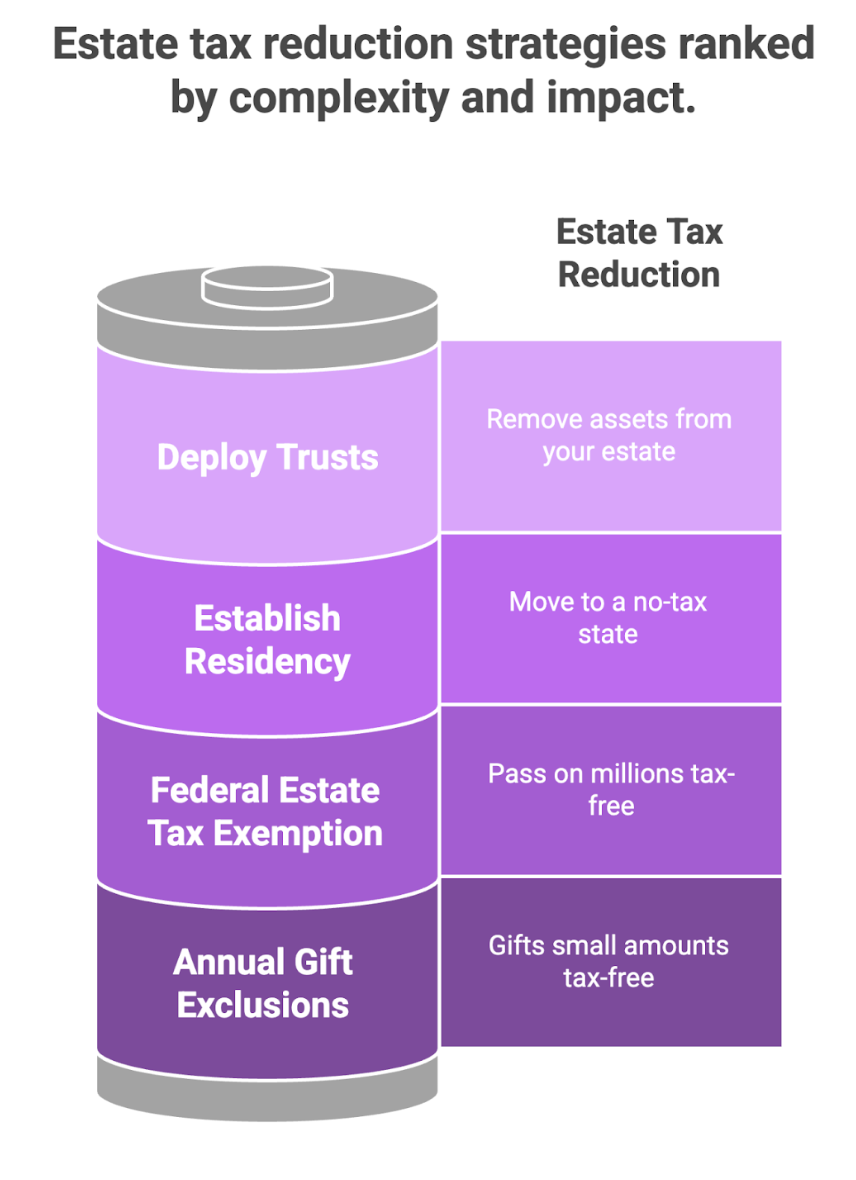

If you're building generational wealth, estate taxes can feel like a penalty for doing the right thing. But with smart planning, you can minimize or even eliminate these taxes. Here's how high-net-worth families, founders, and even upper-middle-class households are legally reducing estate and inheritance tax exposure in 2025.

Where you live (and more importantly, die) matters. States like Florida, Texas, and Nevada don't pay estate taxes, so if your estate is under the federal exemption, you could avoid all estate taxes completely.

But simply owning a home isn't enough.

To shift tax residency, you need to prove domicile:

States like New York and California often audit high-net-worth exits, so the paperwork and timing need to be airtight.

In 2025, you can pass on $13.61 million per person (or $27.22 million for couples) without federal estate tax. But this is temporary.

The exemption is scheduled to sunset after 2025, likely reverting to around $6–7 million per person, meaning estates that are tax-free today could face a 40% hit in 2026.

What wealthy families are doing now:

The annual gift tax exemption is $18,000 per person in 2025.

That means:

For larger estates, advanced trusts aren't just a tool; they're essential.

Here are 3 widely used ones:

These trusts work best when combined with legal and financial guidance; they're not DIY.

Estate law is state-specific, complex, and always changing.

What a good CPA or estate planning attorney does:

If your estate is likely to exceed $7 million per person after 2025, now is the time to act. You don't need to be ultra-wealthy to benefit; just be proactive.

If you live in one of these states or even own property there, your estate could be taxed twice: once by the state and again by the federal government (if it exceeds the federal threshold). Understanding state estate tax rates and inheritance tax implications is crucial for proper planning.

Here's a breakdown of the highest state estate and inheritance tax rates in 2025:

(Estate tax is levied on the total value of the deceased person's estate before it's passed on.)

Important: Some states have "cliff" rules—go $1 over the exemption, and your entire estate gets taxed.

(This is taxed on the recipient, based on how closely related they are to the deceased.)

✅ Only one state, Maryland, has both estate and inheritance tax.

If you're:

...then understanding where your assets are located and how they'll be taxed can save your heirs hundreds of thousands of dollars in state death taxes.

When evaluating states for estate planning purposes, consider the full tax picture. Some states may have no estate tax but high property tax or sales taxes. Others may have favorable income tax rates that benefit you during your lifetime.

When an estate tax return must be filed depends on the value of the estate and applicable exemption amounts. The Internal Revenue Service requires federal estate tax returns for estates exceeding the federal exemption, while states have their own filing requirements.

Tax laws continue to evolve. What constitutes a flat estate tax structure in one state may change, and new estate tax legislation can affect planning strategies. Staying informed about these changes is crucial for effective estate planning.

Estate and inheritance taxes are two of the most misunderstood parts of the U.S. tax system. While they both deal with wealth transfer after someone dies, they are fundamentally different, and confusing them can lead to costly planning mistakes. Let's clear up the most common misconceptions.

Wrong. Estate tax is paid by the estate before assets are distributed to heirs. Inheritance tax is paid by the individual receiving the inheritance.

In other words:

Some states have one, some have both, and many have neither, which is why understanding your state's rules is crucial.

Half-true. While the federal estate tax exemption is over $13 million in 2025, state-level estate taxes often kick in at much lower thresholds. For example:

If you live in a state that levied the tax and own a home, retirement accounts, and life insurance, your estate could be subject to tax even if it doesn't seem "ultra-wealthy."

Not necessarily. Even if your state doesn't impose an inheritance tax, you might inherit money from someone who lived in a state that does.

Example: You live in Florida (no inheritance tax), but inherit from someone in Pennsylvania—you may still owe inheritance tax to Pennsylvania.

False. Estate planning isn't just about taxes; it's about:

Even modest estates can benefit from trusts, beneficiary designations, and smart tax moves. And if you own property in multiple states, things get even more complex.

Not at all. Each state has the power to levy its taxes, and state laws can coexist with or stack on top of federal law.

That means:

A comprehensive tax chart showing estate tax rates and state inheritance tax rates can help you understand the full scope of potential tax liability across different jurisdictions.

Estate and inheritance taxes aren't just for the ultra-wealthy. Even modest estates can trigger tax obligations in certain states, and without the right plan, your family could end up with more questions than answers.

By understanding where these taxes apply and how to structure your assets, you can safeguard your legacy and ensure the people you care about receive the full benefit of what you've built. Whether you need to pay income tax during your lifetime or your heirs will pay a state inheritance tax, proper planning makes all the difference.

At Madras Accountancy, we go beyond tax filing. Our team helps you take control of your finances with personalized strategies that span estate planning, tax optimization, and proactive business accounting, so you're never caught off guard by a state inheritance law or federal change.

Whether you're thinking ahead for your family or preparing your business for succession, we make sure your numbers work for your future.

👉 Start a conversation with us at MadrasAccountancy.com, and get clear, human advice that helps you plan with confidence.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.