.png)

The IRS tangible property regulations determine when business property expenditures must be capitalized (depreciated over time) versus immediately deducted as repairs. These final regulations provide safe harbors for de minimis expenses, routine maintenance, and small business taxpayers, helping property owners correctly classify expenditures and maximize current-year deductions while maintaining IRS compliance.

Jennifer owns three rental properties and spent $47,000 on improvements in 2024. Her accountant capitalized everything for 27.5-year depreciation. A new CPA found $22,000 qualified as deductible repairs under safe harbor provisions, saving Jennifer $7,040 in year-one taxes.

The tangible property regulations create clear rules distinguishing repairs from improvements. Property owners who understand these regulations can immediately deduct qualifying expenditures rather than waiting decades.

Here's your complete guide: what the regulations cover, how safe harbors work, and avoiding costly mistakes.

The final tangible property regulations are IRS rules governing how taxpayers treat expenditures for tangible property, real property (buildings, land improvements) and personal property (equipment, vehicles, furniture). Released in 2013 and effective for tax years beginning in 2014, these regulations replaced inconsistent guidance with clear standards.

They address three areas: when amounts paid must be capitalized versus deducted, what constitutes a unit of property, and rules for property dispositions. They apply to anyone owning or leasing business property.

Key Statistics:

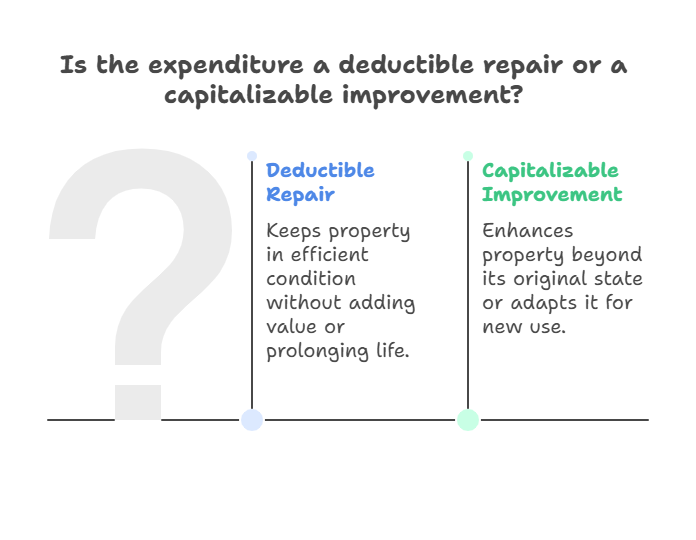

The regulations distinguish deductible repairs from capitalizable improvements based on what the expenditure accomplishes.

Deductible Repairs , Amounts keeping property in ordinarily efficient condition. These don't materially add value, prolong life, or adapt property for new use. Painting, fixing leaks, replacing windows, and routine servicing qualify.

Capitalizable Improvements , Expenditures must be capitalized if they better property, restore it to like-new condition, or adapt it to new use. Betterments improve property beyond its state when placed in service. Restorations return property to ordinarily efficient condition. Adaptations modify property for substantially different use.

Example: Replacing damaged roof shingles is deductible repair. Replacing the entire roof system is capitalizable improvement.

The de minimis safe harbor allows immediately deducting property acquisition costs if amounts per item don't exceed thresholds: $2,500 without financial statements, $5,000 with audited statements. Make the election annually by attaching a statement to your return.

This simplifies accounting for small purchases. Small businesses often miss this election, unnecessarily complicating bookkeeping and delaying deductions.

Critical requirement: Written accounting procedures must be in place at year-start treating amounts below the threshold as expenses. Simply making the election without procedures won't survive IRS scrutiny.

The routine maintenance safe harbor lets taxpayers deduct recurring activities keeping property in ordinarily efficient condition, even if work might otherwise qualify as improvement.

For buildings, activities performed more than once during 10 years qualify. For other property, activities performed more than once during class life (or 10 years) qualify. The key test is expectation when property is placed in service.

Example: HVAC inspections every three years qualify because you expect multiple performances during the system's life. Replacing the entire HVAC doesn't qualify.

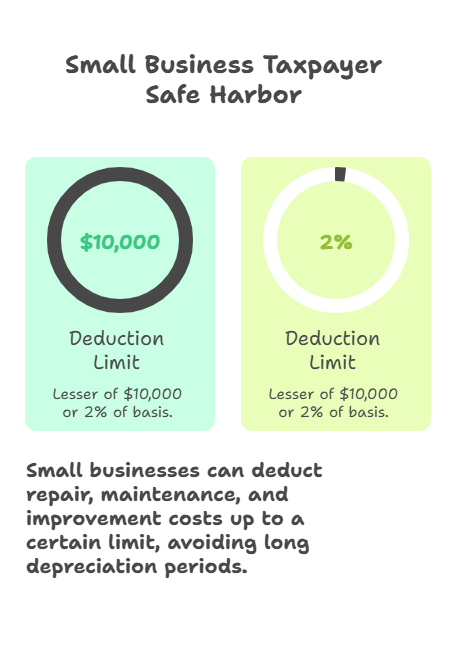

The regulations include a special safe harbor for small business taxpayers. Qualifying taxpayers can deduct amounts for repairs, maintenance, and improvements if totals don't exceed the lesser of $10,000 or 2% of building's unadjusted basis.

Requirements: average annual gross receipts of $10 million or less for three years, and building unadjusted basis of $1 million or less.

Strategic tax planning using this safe harbor allows immediately deducting what would otherwise require decades-long depreciation. The election applies annually to all eligible building property you own or lease.

The unit of property concept determines the level where you decide whether expenditures must be capitalized or deducted. Defining units correctly affects whether you're repairing a component or replacing the entire unit.

For buildings, each building and its structural components constitute one unit. Structural components include walls, floors, HVAC, plumbing, electrical, and fire protection. Building systems can be treated as separate units if properly identified.

For personal property, functionally interdependent components form one unit. A computer system is one unit; delivery trucks are separate units.

Example: Replacing an HVAC compressor is repairing a component (deductible if it doesn't restore the system). Replacing the entire HVAC means replacing the unit, requiring capitalization.

The regulations provide rules for recognizing gain or loss when disposing of property. You generally recognize gain or loss when disposing of the entire unit through sale, exchange, retirement, or abandonment.

Partial disposition elections allow recognizing loss when disposing of a component, even if you replace it. Without this, replacing building components requires capitalizing the replacement without recognizing loss on removed components.

Documentation supporting these elections becomes critical during IRS audits because the IRS examines basis adjustments and loss recognition closely.

Mistake 1: Not Making Elections , Failing to attach required statements to returns means missing immediate deductions. Elections aren't automatic, you must make them annually.

Mistake 2: Incorrect Unit Identification , Misdefining units leads to wrong decisions. Treating each building system as separate without proper designation results in IRS adjustments.

Mistake 3: Missing De Minimis Procedures , Making the election without written accounting procedures at year-start invalidates it. The IRS requires contemporaneous procedures, not retroactive policies.

Mistake 4: Wrong Betterment Standards , The regulations require comparing property condition after expenditure to its condition when placed in service, not immediately before the work. Working with qualified CPAs familiar with these nuances prevents costly misclassifications.

Mistake 5: Ignoring Examples , The regulations include 83 detailed examples providing critical guidance for gray-area situations.

Review property expenditures and categorize them under the regulations' framework. Identify which qualify for safe harbors, which are repairs, and which require capitalization.

Establish written accounting procedures for de minimis safe harbor specifying your threshold and treating items below it as expenses. These must be in place at year-start.

Track units of property with records showing how you've defined building systems and basis allocated to each. Make elections timely by attaching statements to your return, missing deadlines means losing benefits.

The final regulations are IRS rules determining when expenditures for business property must be capitalized versus deducted as repairs. Released in 2013 and effective for 2014 tax years, these regulations define repairs, improvements, and disposal rules for business property.

The de minimis safe harbor lets taxpayers immediately deduct property costing $2,500 or less per item. With audited financial statements, taxpayers can elect a $5,000 threshold. The election must be made annually on your return.

An expenditure is deductible repair if it keeps property in ordinarily efficient condition without bettering, restoring, or adapting it. Improvements must be capitalized if they better the property, restore it to like-new condition, or adapt it for different use.

The routine maintenance safe harbor allows deducting recurring activities keeping property in ordinarily efficient condition. For buildings, activities performed more than once during 10 years qualify. For other property, activities performed more than once during class life or 10 years qualify.

Small business taxpayers have average annual gross receipts of $10 million or less for three preceding years. Qualifying taxpayers can deduct amounts paid for repairs, maintenance, and improvements to eligible building property costing $10,000 or less annually.

A unit of property is the level where taxpayers determine whether expenditures must be capitalized. For buildings, each building and its structural components form one unit. For personal property, functionally interdependent components comprise one unit.

Safe harbor elections are made annually by attaching a statement to your timely filed return. The statement must include your name, taxpayer ID, and declaration that you're making the specific election. Some require additional criteria like applicable financial statements.

We've processed 50,000+ tax returns since 2015, including complex tangible property determinations. Our offshore CPA team analyzes repair vs. capitalization decisions, prepares safe harbor elections, and ensures compliance while maximizing current-year deductions for U.S. firms.

The tangible property regulations provide clear rules for classifying expenditures while offering safe harbors maximizing current-year deductions. Understanding these provisions prevents over-capitalizing deductible repairs and ensures IRS compliance.

Review property expenditures annually using the regulations' framework. Make elections timely, establish necessary procedures, and maintain documentation. When situations fall into gray areas, the regulations' 83 examples provide guidance, or professional help ensures correct application.

About Madras Accountancy: Since 2015, we've served as offshore partners to U.S. CPA firms, processing 50,000+ tax returns including tangible property determinations, safe harbor elections, and compliance with final regulations.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.