If your UK entity files VAT, or your US HQ sells into the UK, 2025 tightens expectations on how VAT data flows, how invoices are exchanged, and how penalties apply when filings or payments slip. A clean setup now prevents rework during quarter-end.

Definition

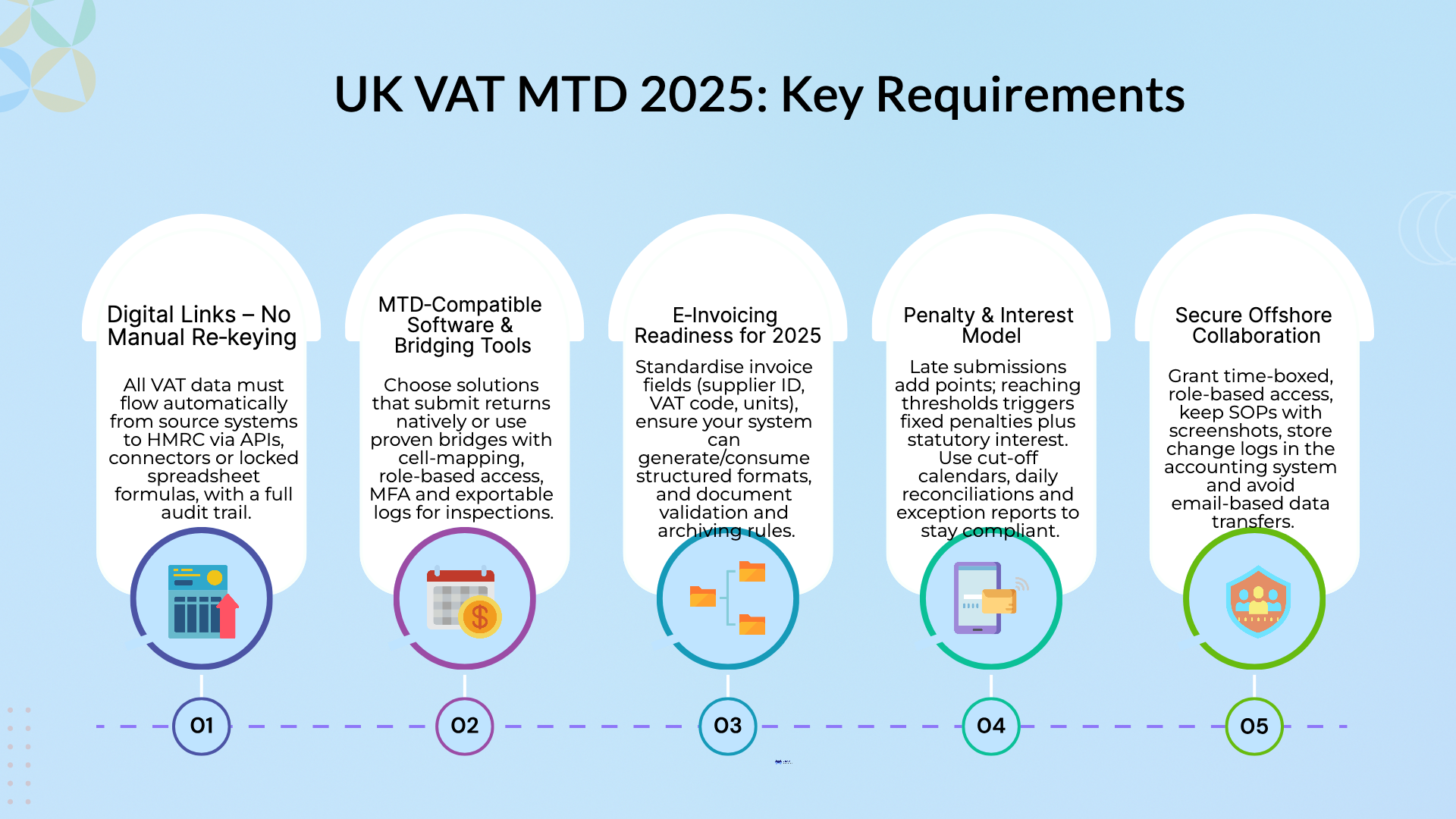

Under MTD for VAT, records must flow digitally from source systems into the return. Manual copy-paste, retyping totals, or editing CSVs breaks the chain.

What good looks like

Quick check

All VAT-registered businesses need MTD-compatible software to keep digital records and submit returns. You can use full accounting software with built-in submissions or a bridging tool that connects a structured spreadsheet to HMRC.

Selection criteria

The UK is consulting on broader e-invoicing adoption. There is interest in standard formats and potential real-time or near-real-time models, but no live mandate yet. Treat 2025 as a readiness year.

Readiness actions

What to document for pilots

Late submission uses a points-based system. Each missed return adds a point; reaching a threshold triggers a fixed penalty, with further penalties for additional late returns until you reset by staying compliant. Late payment penalties sit alongside this model, and statutory interest applies from the due date.

Operational guardrails

MTD in 2025 is about traceable data and steady discipline. Build end-to-end digital links, choose compatible software or a controlled bridge, prepare for e-invoicing by standardising data, and run VAT on a calendar that prevents points and penalties. Small fixes now protect cash and time at quarter-end.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.