.png)

You purchased a $3 million commercial property last month. Your accountant mentions you could deduct $1.2 million immediately through bonus depreciation instead of spreading it over 39 years. That's $444,000 in tax savings this year alone. Most real estate investors miss this opportunity because they don't understand how bonus depreciation works or assume it's too complicated to implement.

Bonus depreciation for real estate allows property owners to immediately deduct 100% of qualifying assets, fixtures, equipment, and building improvements, in the year they're placed in service. The One Big Beautiful Bill Act, signed July 4, 2025, permanently restored 100% bonus depreciation for property acquired after January 19, 2025. This guide explains what qualifies, how to claim it, and why cost segregation studies unlock the biggest savings.

Bonus depreciation is a tax provision that lets real estate investors immediately expense qualifying property components instead of depreciating them over their standard recovery period. Under Section 168(k) of the Internal Revenue Code, you can deduct 100% of eligible assets with a recovery period of 20 years or less in the year you place them in service.

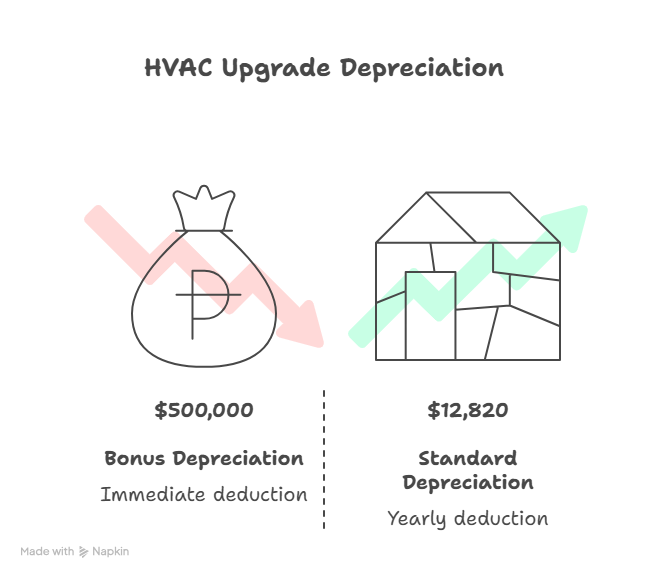

The difference from regular depreciation is timing. A commercial building normally depreciates over 39 years at roughly 2.5% annually. If you spend $500,000 on HVAC upgrades, standard depreciation gives you $12,820 yearly. Bonus depreciation lets you deduct the full $500,000 immediately, creating substantial tax savings when you need it most.

Key qualifying criteria exist: The property must be tangible personal property, qualified improvement property, or certain land improvements. It needs a MACRS recovery period of 20 years or less. Both new and used property qualify, as long as it's new to you and wasn't previously owned by a related party. The property must be acquired and placed in service after January 19, 2025, to qualify for the permanent 100% rate.

Buildings themselves don't qualify, they depreciate over 27.5 years (residential) or 39 years (commercial). However, many components inside and around buildings do qualify. This is where cost segregation studies become essential for maximizing your deduction.

The One Big Beautiful Bill Act fundamentally changed bonus depreciation from a phasing-out provision to a permanent tax benefit. Understanding this shift helps you plan investments strategically.

Prior to July 2025, bonus depreciation was declining rapidly. The Tax Cuts and Jobs Act created 100% bonus depreciation in 2017, but it began phasing down in 2023. Under the old schedule, 2025 would have offered only 40% bonus depreciation, dropping to 20% in 2026 and disappearing entirely by 2027. This created urgency around timing property acquisitions before the benefit vanished.

The new law permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. The previous phase-out schedule was eliminated. This permanence transforms real estate tax planning because you no longer need to rush acquisitions to beat a deadline.

The impact is substantial: A $5 million property with $2 million in qualifying components would have generated $800,000 in first-year deductions under the old 40% rule. Under permanent 100% bonus depreciation, the same property produces $2 million in immediate deductions. At a 37% tax rate, that's an additional $444,000 in tax savings, capital that stays in your business instead of going to the IRS.

Critical timing requirement: Property must be acquired after January 19, 2025. The acquisition date is when you execute a binding written contract, not when you close or take possession. If you signed a purchase agreement in December 2024, even if you closed in March 2025, you're locked into the old 40% rate. Properties acquired before January 20, 2025, remain subject to the phase-down schedule regardless of when they're placed in service.

Not all property components qualify for bonus depreciation. Knowing what qualifies prevents missed opportunities and compliance issues.

Qualifying property categories include:

Personal property: Removable fixtures, furniture, appliances, and equipment with recovery periods of 5 or 7 years. This includes carpeting, window treatments, free-standing shelving, decorative lighting, and specialized equipment for specific business uses.

Land improvements: Site work with a 15-year recovery period, such as parking lots, sidewalks, fencing, landscaping, outdoor lighting, drainage systems, and paved surfaces. These improvements must be outside the building footprint to qualify.

Qualified Improvement Property (QIP): Interior improvements made to nonresidential property after the building was first placed in service. This includes interior walls, ceilings, doors, mechanical systems, electrical upgrades, plumbing modifications, and fire protection systems. QIP has a 15-year recovery period and qualifies for bonus depreciation.

Building systems: HVAC units, electrical distribution, plumbing systems, fire alarms, security systems, and specialized ventilation equipment typically qualify when installed in commercial property.

Property that does NOT qualify:

A retail store renovation illustrates these categories. The building shell (walls, foundation, roof structure) doesn't qualify. But the new flooring, interior partitions, upgraded electrical, HVAC system, storefront signage systems, and parking lot resurfacing all qualify for bonus depreciation. Strategic planning around small business tax law changes helps identify which improvements generate the largest immediate deductions.

Cost segregation studies are the key to maximizing bonus depreciation benefits. Without proper analysis, you'll miss substantial deductions hiding in your real estate acquisitions.

A cost segregation study is an engineering-based analysis that identifies and reclassifies building components into shorter depreciation categories. Instead of depreciating the entire property as 39-year real property, the study breaks it into components with 5-, 7-, 15-, and 20-year recovery periods. These shorter-lived assets qualify for bonus depreciation.

The process involves: Engineering professionals physically inspect your property and review construction documents. They identify components that qualify as personal property or land improvements rather than real property. Each component is valued and assigned to the appropriate tax classification. The study produces an IRS-compliant report documenting the methodology and allocations.

Real-world impact: A $4 million office building might allocate $3.5 million to the 39-year building structure and $500,000 to qualifying components. Without cost segregation, you'd depreciate everything over 39 years. With proper segregation, you immediately deduct $500,000 through bonus depreciation, creating $185,000 in tax savings (at 37% rate).

The study typically identifies 20-40% of a commercial property's cost as eligible for accelerated depreciation. Restaurants and retail properties often see higher percentages due to specialized equipment and extensive interior improvements. Medical facilities, hotels, and manufacturing buildings also produce substantial reclassifications.

Cost segregation works retroactively through Form 3115 (change in accounting method). If you purchased property in 2020-2024 but never performed cost segregation, you can still claim the accelerated depreciation and bonus rates that were in effect when you placed the property in service. This creates opportunities to generate immediate deductions from properties you've owned for years. For businesses managing multiple properties, professional tax planning and preparation services ensure you maximize these complex deduction strategies.

Claiming bonus depreciation requires proper calculation and documentation. The process is straightforward but mistakes can trigger IRS scrutiny.

Step 1: Determine your qualifying property basis. Calculate the total cost of assets eligible for bonus depreciation. This includes the purchase price allocation from cost segregation plus any improvements you made. Don't include land, building structure, or assets with recovery periods exceeding 20 years.

Step 2: Verify the placed-in-service date. Property must be acquired and operational. Simply ordering equipment isn't enough, it must be installed and available for use. For real estate, this typically means the closing date when you take legal ownership and the property is ready for its intended use.

Step 3: Calculate your deduction. Multiply the qualifying property basis by 100%. For property placed in service after January 19, 2025, you deduct the full amount. For property placed in service earlier in 2025 or in prior years, use the applicable percentage from the phase-down schedule.

Step 4: Complete IRS Form 4562. Part II is for bonus depreciation and Part III covers MACRS depreciation. List each asset class separately, 5-year property, 7-year property, and 15-year property. The form calculates your total depreciation deduction including bonus and regular depreciation.

Step 5: Maintain supporting documentation. Keep cost segregation reports, invoices, closing statements, and proof of placed-in-service dates. The IRS commonly examines large depreciation deductions, particularly when combined with bonus depreciation. Thorough documentation prevents problems during audits, which our guide on preparing for tax audits covers comprehensively.

Electing out of bonus depreciation: You can choose to opt out of bonus depreciation for specific asset classes. This makes sense when you want to spread deductions over multiple years to match income, preserve AMT considerations, or avoid creating large tax losses you can't currently use.

Real estate investors often confuse bonus depreciation with Section 179, but these are distinct tax provisions with different strategic applications.

Section 179 characteristics:

Bonus depreciation characteristics:

You typically use both together. Section 179 works well for equipment and personal property purchases. Bonus depreciation handles the larger building components identified through cost segregation. Our detailed guide on Section 179 and bonus depreciation strategies explains how to optimize both provisions together.

A real estate developer might use Section 179 for $100,000 in office equipment and computers, then apply bonus depreciation to $800,000 in building improvements and land enhancements. This combined approach maximizes current-year deductions while preserving flexibility for future tax planning.

Even sophisticated investors make errors that reduce deductions or create compliance problems. These mistakes cost thousands in lost tax benefits.

Missing the acquisition date requirement. Properties acquired before January 20, 2025, don't qualify for permanent 100% bonus depreciation even if placed in service later in 2025. The acquisition date is when you sign the binding contract, not the closing date. Timing matters significantly.

Failing to perform cost segregation. The largest mistake is treating the entire property as 39-year real property. Without cost segregation, you can't identify qualifying components eligible for bonus depreciation. This leaves hundreds of thousands in deductions unclaimed.

Misclassifying property categories. Not every interior improvement qualifies as QIP. Structural components, building enlargements, and elevators don't qualify. Understanding the technical definitions prevents disallowed deductions during IRS examinations.

Forgetting about depreciation recapture. When you sell property after claiming accelerated depreciation, you face recapture tax on the excess depreciation claimed. The recaptured amount is taxed as ordinary income up to 25%, not capital gains rates. Plan exit strategies considering this recapture impact.

Ignoring state conformity issues. Not all states follow federal bonus depreciation rules. California, for example, doesn't conform to 100% bonus depreciation. Properties in non-conforming states require separate state depreciation calculations. For businesses operating across state lines, understanding sales tax compliance requirements by state becomes equally important for comprehensive tax planning.

Poor documentation practices. The IRS scrutinizes large depreciation deductions. Without proper cost segregation reports, placed-in-service evidence, and allocation documentation, you can't defend your deductions. Invest in professional studies rather than unsupported estimates.

Does bonus depreciation apply to residential rental properties?

Yes, residential rental properties qualify for bonus depreciation on components with recovery periods of 20 years or less. Cost segregation studies identify personal property, land improvements, and certain building systems that qualify. The residential structure itself (27.5-year property) doesn't qualify, but many components do, creating substantial first-year deductions.

Can I use bonus depreciation if I inherited the property?

No, inherited property doesn't qualify for bonus depreciation. The property must be newly acquired through purchase, construction, or manufacture. The "first-use" requirement means inherited assets don't meet the acquisition criteria even though they're new to you.

What happens if I sell property within a few years of claiming bonus depreciation?

You'll face depreciation recapture on the accelerated depreciation you claimed. The recaptured amount is taxed as ordinary income (up to 25% rate) rather than capital gains rates. This doesn't eliminate the benefit, you still received tax savings upfront, but you need to plan for recapture tax when selling.

Can I claim bonus depreciation on property purchased before 2025 if I renovate it now?

Yes, new improvements and renovations placed in service after January 19, 2025, qualify for 100% bonus depreciation. The original building follows its existing depreciation schedule, but new QIP and improvements you make qualify for immediate expensing under the new permanent rules.

Is cost segregation worth it for smaller properties?

Cost segregation typically makes financial sense for properties over $500,000. The study costs $5,000-$15,000 depending on complexity. If the accelerated depreciation generates $50,000+ in additional deductions, creating $15,000-$20,000 in tax savings, the ROI justifies the cost. Smaller properties may not produce sufficient reclassifications to warrant the expense.

Does bonus depreciation work with 1031 exchanges?

Yes, but it's complex. In a 1031 exchange, you defer gain by rolling your basis into replacement property. Any bonus depreciation claimed reduces your basis, affecting future exchange calculations. The replacement property qualifies for bonus depreciation on qualifying components. Consult tax advisors before combining these strategies.

Can partnerships and LLCs use bonus depreciation?

Yes, pass-through entities like partnerships, LLCs, and S corporations can claim bonus depreciation. The deduction flows through to individual partners or shareholders based on their ownership percentage. Individual owners may face additional limitations based on their passive activity status and at-risk rules.

How do accounting firms help maximize bonus depreciation benefits?

Professional accounting firms coordinate cost segregation studies, ensure proper tax form completion, model different depreciation scenarios, handle state conformity issues, and maintain compliance documentation. They also integrate bonus depreciation into comprehensive tax strategies considering AMT, NOLs, and multi-year income optimization.

Bonus depreciation is now permanent, eliminating the urgency that existed under the phase-down schedule. However, you still need to act deliberately. Properties acquired after January 19, 2025, qualify for 100% bonus depreciation, but only if you properly identify qualifying components through cost segregation.

Schedule a cost segregation study for any property purchased or improved in 2025. The sooner you complete the analysis, the sooner you can capture tax savings. Even properties acquired in previous years can benefit from look-back studies using Form 3115 to claim missed depreciation.

Work with tax professionals who understand real estate depreciation strategies. The interaction between bonus depreciation, cost segregation, passive activity rules, and state tax conformity requires specialized knowledge that general practitioners may lack.

About Madras Accountancy

Madras Accountancy provides comprehensive tax planning, real estate accounting, and cost segregation coordination services for real estate investors and CPA firms nationwide. Since 2015, we've helped over 200 firms optimize their clients' tax strategies while maintaining full IRS compliance. Our team specializes in depreciation strategies, multi-property portfolio management, and preparing investors for successful tax examinations. Learn more at madrasaccountancy.com.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.