Most new business owners meet the chart of accounts for the first time when they open accounting software and see a long list of categories they did not create. Some look obviously relevant. Others feel like they belong to a completely different industry. It is tempting to leave the list as is and just start coding transactions.

That works for a while. Then you try to answer a simple question like, "How much did we really spend on marketing last quarter?" and realize half your ad spend is under "Office Expense" and the rest is split between three different miscellaneous accounts. The structure never matched your real world.

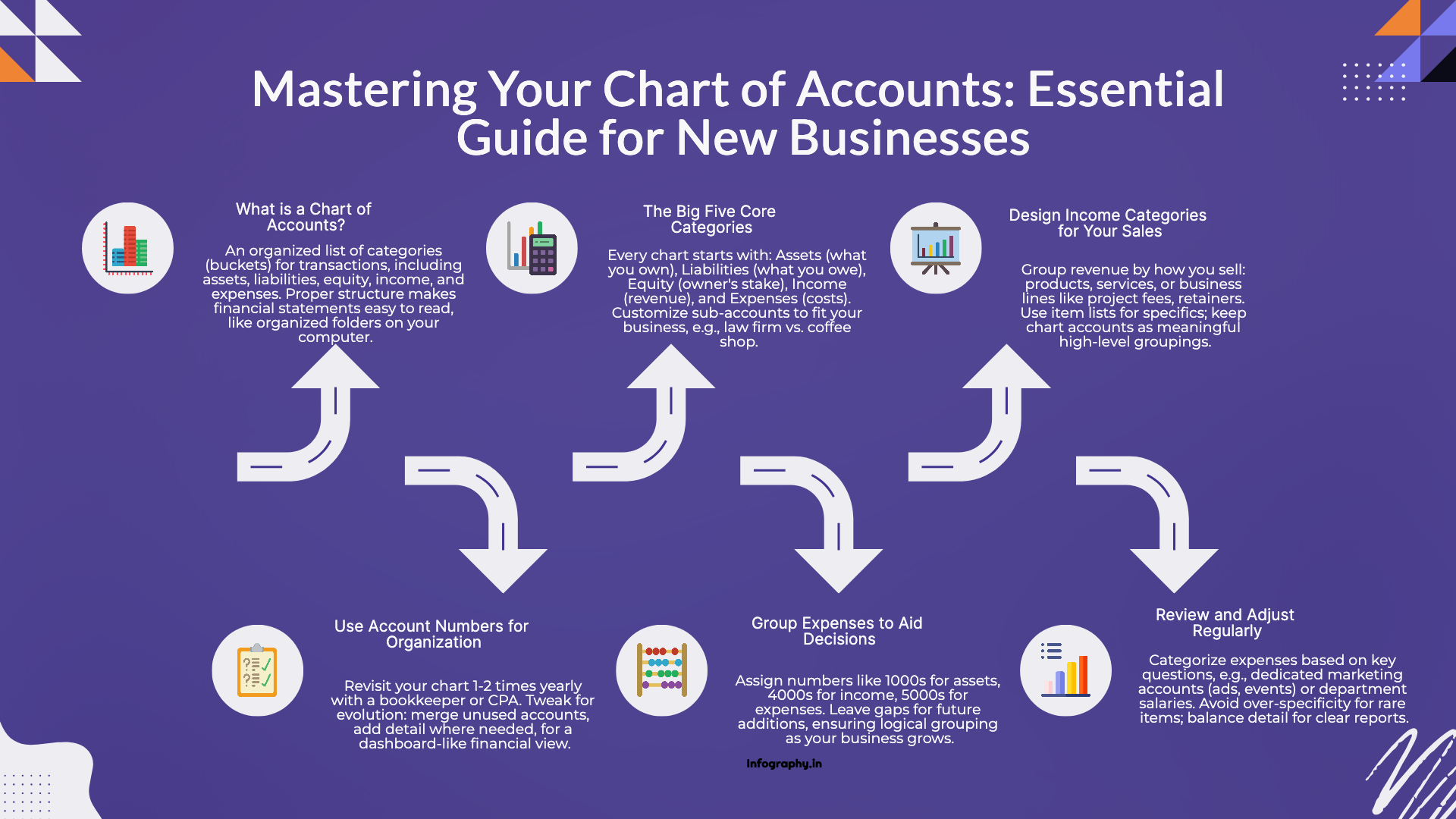

At its core, a chart of accounts is just an organized list of buckets where transactions live. Assets, liabilities, equity, income, and expenses each get their own section. The way you name and group those buckets determines how easy it is to read your financial statements later.

Think of it like the folders on your computer. If everything ends up in one folder called "Stuff," you will eventually waste time hunting for files. A thoughtful structure upfront saves hours down the road.

Every chart of accounts rests on the same basic pillars:

Your software will usually provide starter accounts under each. The key is to adjust the details so they reflect how your company actually works. A law firm needs different income and expense detail than a coffee shop.

For revenue, ask yourself how you naturally describe what you do. Do you sell products, services, or both? Do you have clearly separate lines of business that you want to track? For example, a consulting firm might want separate accounts for project fees, retainers, and training income.

Avoid the temptation to create a new income account for every single product. That is what item or product lists are for. Your chart of accounts should show meaningful groupings, not an endless catalog.

On the expense side, think about the questions you will ask later. If you care a lot about customer acquisition, it probably makes sense to have a dedicated group of marketing accounts: advertising, sponsorships, events, and so on. If payroll is your biggest cost, you might want separate salary accounts for different departments.

At the same time, resist the urge to create ultra specific accounts for one or two transactions a year. If you only buy office plants twice a year, "Office Supplies" is fine. Too much granularity makes reports harder to read, not easier.

Some owners ignore account numbers entirely, but they can be very helpful, especially as the business grows. A simple numbering scheme, such as 1000s for assets, 2000s for liabilities, 3000s for equity, 4000s for income, and 5000s and up for expenses, keeps everything grouped logically.

Within each range, you can leave gaps for future accounts. Maybe 5100 is "Rent," 5200 is "Utilities," 5300 is "Office Expenses." If you later add 5250 for "Internet and Phone," it still fits in the right neighborhood.

A chart of accounts is not carved in stone. As your business evolves, you might need more detail in some areas and less in others. The important thing is to make changes deliberately, not on the fly during a busy week.

A good habit is to review your accounts with your bookkeeper or CPA once or twice a year. Ask which accounts are rarely used, which ones seem overloaded, and whether the current structure still supports the kind of reporting you want. Make a few thoughtful tweaks rather than constant small edits.

When you design the chart of accounts to match how you actually think about your business, the financial statements stop feeling like homework and start feeling like a dashboard. That is the goal. For more insights on using your accounting data effectively, see our guide on data analytics in accounting.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.