.png)

Your firm just signed three new clients who need full bookkeeping services. Your team is already working 50-hour weeks, and you're wondering how to deliver quality work without burning out your staff or turning away growth opportunities.

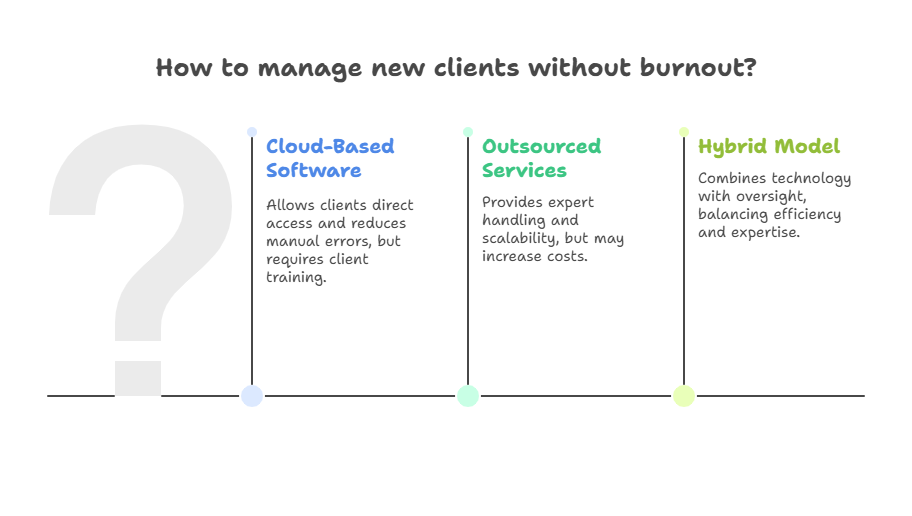

Client bookkeeping solutions are systems, software, and services that enable accounting firms to manage their clients' daily financial transactions, reporting, and compliance needs efficiently. These solutions range from cloud-based software platforms that clients can use directly, to outsourced bookkeeping services where specialist teams handle the work behind the scenes, to hybrid models that combine technology with expert oversight.

The right client bookkeeping solution lets CPA firms serve 30-50% more clients without adding proportional headcount, improves accuracy by reducing manual data entry errors by 80%, and creates recurring monthly revenue streams that stabilize cash flow. This guide covers everything from selecting software platforms to building scalable delivery models that support your firm's growth.

Client bookkeeping solutions encompass the tools, processes, and services that accounting firms use to deliver bookkeeping services to their clients at scale. This goes beyond simply tracking transactions, you're building a systematic approach to managing accounts payable, accounts receivable, bank reconciliations, financial reporting, and compliance across dozens or hundreds of client companies.

Modern client bookkeeping solutions typically involve three components working together. First, the technology layer includes accounting software (QuickBooks Online, Xero, NetSuite) that records transactions and generates reports. Second, the process layer defines how work flows through your firm, from client data collection to review cycles to report delivery. Third, the resource layer determines who does the work, your in-house team, offshore partners, automation tools, or a combination.

The evolution of client bookkeeping has accelerated dramatically since 2020. Firms that relied on desktop software and local file servers have shifted to cloud-based platforms. Those that required clients to mail paper receipts now accept digital uploads via mobile apps. Accounting firms that manually entered every transaction now use AI-powered tools that categorize 70-80% of transactions automatically.

This transformation means that client bookkeeping solutions now deliver results that were impossible five years ago. A single bookkeeper supported by modern tools can manage 25-35 clients effectively, compared to 12-15 clients using traditional methods. The quality often improves too, automated bank feeds and reconciliation tools catch errors that human reviewers miss.

Traditional bookkeeping delivery models don't scale. When your firm relies entirely on local staff entering data manually, every new client requires proportional increases in headcount. This creates a ceiling on growth that most firms hit around 50-75 bookkeeping clients.

Client expectations have shifted dramatically. Today's business owners expect real-time access to financial dashboards, mobile receipt capture, automated invoice reminders, and instant answers to questions. Firms that provide quarterly reports on paper face client churn to competitors offering cloud-based portals and monthly reporting.

The economics matter too. Bookkeeping services generate predictable monthly recurring revenue, but only if you deliver them profitably. When bookkeepers spend 60-70% of their time on data entry instead of analysis and advisory, you're subsidizing low-value work at the expense of high-value services. Better client bookkeeping solutions shift this ratio, your team spends 30-40% on data processing and 60-70% on value-added activities.

Talent challenges compound the problem. Quality bookkeepers are difficult to hire and expensive to retain. When your growth depends on finding local talent in a competitive market, expansion becomes nearly impossible. Client bookkeeping solutions that incorporate offshore resources, automation, or outsourced components give firms flexibility that pure in-house models lack.

Compliance requirements continue to increase. Between sales tax nexus rules, 1099 reporting requirements, PPP loan documentation, and evolving state regulations, the compliance burden on bookkeeping has grown substantially. Solutions that automate compliance tracking reduce the risk of costly mistakes.

Software selection forms the foundation of any client bookkeeping solution. The platform you choose affects everything from data accuracy to client experience to your team's efficiency. Here's what accounting firms need to evaluate.

QuickBooks Online dominates the small business market with roughly 80% share among firms with under $5M revenue. This creates a network effect, most bookkeepers know QuickBooks, most apps integrate with QuickBooks, and most clients have heard of QuickBooks. For firms building client bookkeeping solutions that serve small businesses, QuickBooks Online Accountant provides free access to manage unlimited clients.

Xero has gained significant traction among firms that value user experience and work with international clients. The platform's approach to bank reconciliation and its clean interface reduce training time for both clients and staff. Xero's pricing structure also creates better margins for accounting firms compared to QuickBooks in many scenarios.

For clients with complex needs, multiple entities, inventory, manufacturing, or revenue over $10M, platforms like NetSuite or Sage Intacct become necessary. These solutions require specialized expertise, which creates opportunities for firms willing to develop that capability. Consider whether you want to invest in building specialized skills in-house or partner with firms that have that expertise.

Software selection should align with your target client profile. Firms that primarily serve restaurants need platforms with strong inventory and point-of-sale integrations. Those serving professional services need robust time tracking and project accounting. E-commerce clients require platforms that handle high transaction volumes and multi-channel sales.

Outsourcing components of client bookkeeping creates leverage that pure in-house models cannot match. When structured properly, outsourced bookkeeping partnerships let firms serve 3-4x more clients with the same local management team.

The key is understanding which functions to outsource versus which to keep in-house. Transaction processing, data entry, bank reconciliations, and routine month-end tasks are perfect candidates for outsourcing. These activities require attention to detail but don't demand deep knowledge of each client's business. Client communications, advisory conversations, tax planning, and exception handling typically remain with your local team.

Quality outsourcing partners provide more than just labor cost savings.

The best partners bring specialized technology, proven processes, and quality control systems that improve accuracy. When you outsource to firms with dedicated QA teams and multi-level review processes, error rates often drop below what in-house teams achieve.

Geographic arbitrage creates the cost advantage. By partnering with bookkeeping teams in regions with lower labor costs, firms reduce the cost per client by 40-60% while maintaining or improving quality. This margin expansion funds investment in advisory services, technology, or business development.

The staffing flexibility matters too. When you hire a local bookkeeper, you commit to their full salary whether you have 15 clients or 35 clients. Outsourced models scale up or down based on actual client count, eliminating the risk of overstaffing during slow periods or understaffing during growth phases. Our guide on deciding when to outsource versus hiring in-house provides a detailed framework for this decision.

Successful outsourcing requires clear processes. Document your workflow, create detailed SOPs for common scenarios, establish communication protocols, and define quality standards. Firms that treat outsourcing as "throwing work over the wall" fail. Those that invest in partnership development, training, and continuous improvement succeed.

AI and machine learning have moved from buzzwords to practical tools in bookkeeping. Modern platforms use AI for transaction categorization, receipt data extraction, anomaly detection, and predictive analytics. This automation eliminates 60-70% of manual data entry while improving accuracy.

AI-powered tools can review bank transactions and suggest appropriate categories based on historical patterns, vendor names, and transaction descriptions. After a learning period of 1-2 months, these tools achieve 85-90% accuracy on routine transactions. Your team reviews and approves suggestions rather than manually categorizing every transaction.

Receipt management has transformed through optical character recognition (OCR) technology. Clients snap photos of receipts with their phones, and software automatically extracts the date, vendor, amount, and purpose. This data flows directly into accounting systems without manual typing. The time saved per transaction is small, maybe 30 seconds, but multiplied across thousands of transactions annually, it becomes significant.

Bank feed automation has reached the point where many clients go weeks without their bookkeeper needing to access their books. Transactions flow automatically from bank accounts into accounting software, get categorized by AI, and reconcile automatically if they match invoices or bills. Your team focuses on reviewing exceptions and unusual items rather than processing routine transactions.

API integrations connect accounting platforms to payment processors, CRM systems, inventory software, and payroll providers. This creates a unified ecosystem where data flows automatically between systems without manual export/import processes. For example, when a client processes a credit card payment through Square, that transaction appears in QuickBooks within hours without anyone touching it.

Cloud-based platforms enable real-time collaboration. Your team in the US can review work completed by offshore partners in India overnight. Clients can access financial dashboards 24/7 without requesting reports. This eliminates the bottlenecks created by file-based accounting systems.

Building scalable client bookkeeping solutions requires more than good software, you need a systematic delivery model that produces consistent results regardless of which team member handles the work. This standardization is what separates firms that scale from those that hit capacity limits.

Start with client segmentation. Not all bookkeeping clients need the same level of service. A consultant with 20 monthly transactions needs basic bookkeeping. A retail store with inventory, multiple locations, and 2,000 monthly transactions needs comprehensive services. Create 2-4 service tiers with defined deliverables, pricing, and service levels.

Document every process in detail. Create step-by-step procedures for client onboarding, month-end close, accounts payable processing, accounts receivable management, payroll integration, and financial reporting. Include screenshots, examples, and quality checkpoints. This documentation becomes the training manual for new team members and the quality standard for review.

Implement tiered review structures. Junior bookkeepers handle data entry and routine processing. Senior bookkeepers review their work and handle complex transactions. Controllers perform final review and client communication. This pyramid structure lets you hire less experienced staff for routine work while maintaining quality through systematic review.

Use project management software to track all client work. Tools like Karbon, Financial Cents, or TaxDome let you create standardized workflows, assign tasks, track time, and monitor deadlines across your entire client portfolio. Without these systems, client work falls through the cracks as your firm grows.

Build measurement into your delivery model. Track metrics like transactions processed per hour, error rates, days to close, client satisfaction scores, and revenue per client. Review these metrics monthly and use them to identify training needs, process improvements, or staffing adjustments. For more guidance on optimizing your finance operations as you scale, explore our article on deciding when to outsource versus hire in-house at each growth stage.

Data quality issues create the most persistent problems in client bookkeeping. When clients provide incomplete information, fail to categorize transactions properly, or submit documentation weeks late, even the best systems struggle. The solution involves setting clear expectations during onboarding and implementing consequences for non-compliance, whether that's delayed reporting, additional fees, or client termination.

Technology resistance from clients can slow implementation. Some business owners resist cloud accounting because they're comfortable with desktop software. Others don't want to adopt mobile receipt scanning because they prefer paper. These clients require more hand-holding initially, but most adapt once they experience the benefits. Consider whether serving technology-resistant clients aligns with your firm's direction.

Scope creep damages profitability. Client bookkeeping engagements start with defined deliverables, but clients gradually request additional services without corresponding fee increases. "Can you just help with this one payroll question?" becomes weekly payroll support. Clear engagement letters and disciplined scope management prevent this drift.

Quality control becomes difficult at scale. When your firm manages 100+ bookkeeping clients, ensuring consistent quality across all clients requires systematic review processes. Random sampling, automated exception reports, and peer review systems help maintain standards. Without these controls, quality varies dramatically based on who's assigned to each client.

Staff retention challenges affect client bookkeeping more than most service lines. Bookkeeping roles can become repetitive, leading to burnout and turnover. Combat this through career development paths, exposure to advisory work, and using technology to eliminate tedious tasks. Investing in understanding common mistakes that affect retention helps prevent costly turnover.

Pricing strategies dramatically affect profitability in client bookkeeping. Traditional hourly billing creates the wrong incentives, you make more money by being inefficient. Fixed monthly pricing aligns better with client expectations and your firm's economics.

Value-based pricing tiers work well for most firms. Create packages based on transaction volume, complexity, and deliverables. A basic package might include 50 transactions monthly, bank reconciliations, and quarterly financial statements for $500/month. A premium package could handle 500 transactions, weekly reporting, and management advisory for $2,500/month.

Use transaction-based pricing as a foundation, then adjust for complexity factors. A construction company with 200 transactions requires more expertise than a consultant with 200 transactions because of job costing, contract accounting, and progress billing complexities. Build complexity multipliers into your pricing.

Annual prepayment discounts improve cash flow and reduce churn. Offer clients 10-15% discounts for paying annually upfront. This locks in revenue, reduces collections issues, and creates switching costs that improve retention.

Avoid underpricing to win clients. New firms often price bookkeeping services too low, creating unsustainable businesses. Calculate your fully loaded costs, including software, overhead, and team time, and ensure prices cover costs plus target margins. If that makes you more expensive than competitors, that's fine. You're selling quality, reliability, and expertise, not the cheapest option.

What's the difference between client bookkeeping solutions and accounting services?

Client bookkeeping solutions focus on recording daily transactions, reconciling accounts, and producing basic financial statements. Accounting services encompass broader activities including financial analysis, tax planning, audit preparation, and strategic advisory.

Bookkeeping is the foundation that captures transaction data, while accounting interprets that data to provide insights. Most firms offer both services, with bookkeeping creating recurring monthly revenue and accounting services generating project-based fees.

How much should accounting firms charge for client bookkeeping services?

Pricing varies based on transaction volume, complexity, and service level. Small businesses with 50-100 monthly transactions typically pay $400-800 monthly. Mid-sized companies with 200-500 transactions pay $1,200-2,500 monthly. Complex businesses with inventory, multiple entities, or 500+ transactions often pay $3,000-5,000+ monthly. Calculate your costs including software, labor, overhead, and review time, then add your target margin to determine sustainable pricing.

Can AI replace human bookkeepers in client accounting?

AI excels at automating routine tasks like transaction categorization, receipt data extraction, and bank reconciliation, reducing manual work by 60-80%. However, AI cannot replace human judgment for complex decisions, client communication, exception handling, or advisory services. The future involves AI handling repetitive processing while bookkeepers focus on analysis, problem-solving, and advisory work. Firms that embrace AI augmentation gain competitive advantages over those resisting technology.

What software do most CPA firms use for client bookkeeping?

QuickBooks Online dominates with roughly 80% market share among small business clients. Xero has grown to 10-15% market share, particularly among firms serving international clients. Specialized platforms like NetSuite or Sage Intacct serve mid-market and complex businesses. Most CPA firms become proficient in 2-3 platforms to serve their client mix, with QuickBooks Online typically forming the foundation and specialized platforms handling edge cases.

How do you handle clients who resist moving to cloud-based bookkeeping?

Start by understanding their concerns, usually security, learning curve, or internet reliability. Address security by explaining that cloud platforms use bank-level encryption and automatic backups, often more secure than local servers. Reduce learning curve anxiety with personalized training and hands-on support. For internet concerns, note that most platforms work offline with data syncing when connection resumes. Ultimately, some clients will insist on desktop software, and you need to decide whether serving them aligns with your firm's direction.

Should accounting firms build in-house bookkeeping teams or outsource?

The answer depends on your scale and expertise. Firms with under 20 bookkeeping clients often handle work in-house to maintain control and client relationships. Those serving 30-50+ clients benefit from hybrid models combining local oversight with outsourced processing. Pure outsourcing works when you partner with specialized providers who understand your standards and processes.

Calculate the total cost including salaries, benefits, training, and turnover before deciding. Most growing firms eventually adopt hybrid models that combine in-house management with outsourced processing capacity.

What metrics should firms track for client bookkeeping operations?

Track revenue per client, cost per client, gross margin per client, transactions processed per hour, days to close books, error rates requiring corrections, client satisfaction scores, and client churn rate. These metrics identify profitable versus unprofitable clients, efficiency improvements, quality issues, and retention problems. Review monthly with your team and use insights to adjust pricing, improve processes, or make staffing decisions.

How can small CPA firms compete with large firms offering client bookkeeping?

Small firms compete through specialization, personal service, and technology adoption. Choose an industry niche and become the expert in that vertical's bookkeeping needs. Provide responsive, personalized service that large firms cannot match. Adopt technology aggressively to match large firms' efficiency advantages. Consider outsourcing partnerships to access the scale benefits that large firms achieve through internal teams. Many clients prefer working with smaller firms despite slightly higher prices because of the relationship and responsiveness.

Client bookkeeping solutions have evolved from manual data entry to technology-enabled services that combine cloud software, AI automation, and strategic outsourcing. Accounting firms that embrace this evolution serve more clients profitably while delivering better service than traditional approaches allowed.

Start by selecting software that matches your target client profile, then build systematic processes that produce consistent results regardless of team size. Consider hybrid delivery models that combine local oversight with offshore processing to achieve scale without compromising quality. Most importantly, measure what matters and continuously refine your approach based on data.

At Madras Accountancy, we partner with CPA firms and accounting practices across the US as their offshore bookkeeping team. Our specialized staff handles transaction processing, reconciliations, and month-end close procedures under your firm's oversight, letting you serve 30-50% more clients without adding local headcount. We've supported 200+ accounting firms since 2015, processing bookkeeping for their clients while they maintain relationships and advisory services.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.