.png)

IRS Form 4797 reports the sale or exchange of business property used in your trade or business, including buildings, equipment, and vehicles. The form calculates depreciation recapture (taxed as ordinary income) and determines whether remaining gains qualify as capital gains or ordinary income based on property type and holding period.

Marcus sold his construction company's equipment for $280,000 after claiming $120,000 in depreciation over five years.

He assumed the $80,000 gain would be capital gains taxed at 15%. His CPA filed Form 4797 and discovered $75,000 was depreciation recapture taxed at his 32% ordinary rate, costing him an extra $12,750 he hadn't budgeted.

Understanding Form 4797 prevents these surprises. Business owners selling property often overlook depreciation recapture rules, leading to unexpected tax bills.

Here's your complete guide: when to file, how to calculate gains correctly, and avoiding common mistakes.

Form 4797, "Sales of Business Property," reports gains and losses from selling property used in your trade or business. The IRS requires this form when you dispose of depreciable property, real property used for business, or assets subject to Section 179 or Section 1245 recapture.

The form separates property by holding period and type. Section 1231 property (held over one year) goes in Part I. Ordinary gains and losses from property held one year or less appear in Part II. Part III calculates depreciation recapture under Sections 1245 and 1250, while Part IV handles partner and S corporation shareholder dispositions.

Quick Facts:

File Form 4797 when selling:

Depreciable Business Property , Equipment, machinery, vehicles, computers, furniture. If you claimed depreciation or Section 179 deductions, Form 4797 captures recapture amounts.

Real Property Used in Business , Commercial buildings, warehouses, office space, manufacturing facilities, and business rental properties.

Section 1231 Property , Assets held over one year including timber, coal, livestock (cattle and horses for draft, breeding, dairy, or sporting held 24+ months), and unharvested crops sold with land.

Don't report: inventory, personal-use assets, investment property (use Schedule D), or property held one year or less unless it's Section 1231 property.

Follow this formula accounting for depreciation:

Step 1: Adjusted Basis , Original cost + improvements - depreciation claimed. Equipment bought for $100,000, with $20,000 upgrades and $40,000 depreciation = $80,000 basis.

Step 2: Gross Proceeds , Sales price - selling expenses. A $150,000 sale with $5,000 in fees = $145,000 net proceeds.

Step 3: Total Gain/Loss , Net proceeds - adjusted basis. $145,000 - $80,000 = $65,000 gain.

Step 4: Depreciation Recapture , The lesser of your gain or total depreciation becomes ordinary income. Here, $40,000 is recaptured at ordinary rates, with $25,000 remaining potentially qualifying for capital gains.

Part III of Form 4797 handles this calculation. Section 179 deductions add complexity requiring recapture if you dispose of property before its recovery period ends.

The IRS treats personal property and real property differently.

Section 1245 (Personal Property) , Equipment, machinery, vehicles, furniture. All depreciation is recaptured as ordinary income up to the full gain amount.

Section 1250 (Real Property) , Buildings and structural components. Only "excess" depreciation beyond straight-line is recaptured as ordinary income (rare with straight-line). Remaining gain gets "unrecaptured Section 1250" treatment, taxed at maximum 25% rate.

Example: Selling a rental building with $100,000 straight-line depreciation and $150,000 gain. The $100,000 depreciation is unrecaptured Section 1250 gain (25% rate), while the remaining $50,000 qualifies for capital gains rates (15-20%).

Most business property sales require both forms because gains and losses flow between them.

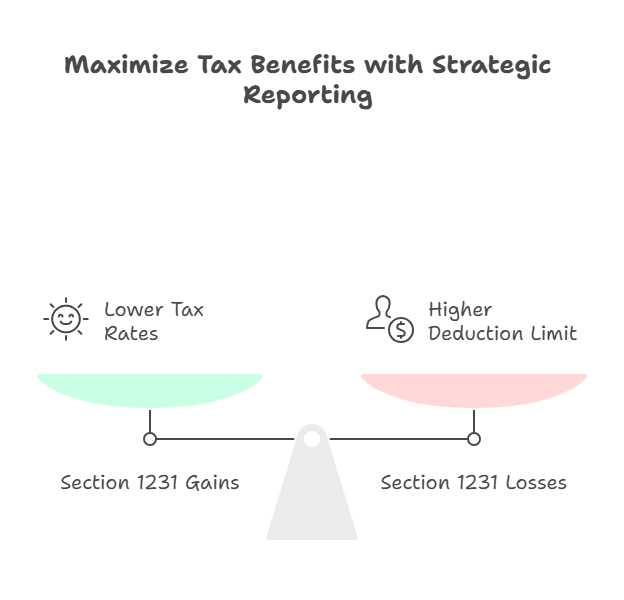

Form 4797 Part I reports Section 1231 gains and losses. Net Section 1231 gains flow to Schedule D as long-term capital gains. Net Section 1231 losses flow to Form 1040 as ordinary losses, better treatment than capital losses.

This creates "best of both worlds": gains taxed as capital gains (lower rates), losses deductible as ordinary losses (no $3,000 limitation). The IRS closely examines these transactions during audits because tax benefits are substantial.

Form 8949 may be required if you sell business property held for investment or have partial business use.

Mistake 1: Incorrect Basis , Forgetting to reduce basis by depreciation claimed (or allowable). The IRS reduces your basis even if you forgot to claim depreciation.

Mistake 2: Missing Recapture , Reporting entire gain as capital gains without calculating recapture triggers automatic IRS corrections and penalties.

Mistake 3: Wrong Form , Using Schedule D for business property or Form 4797 for investments. Qualified tax professionals prevent form selection errors that delay refunds.

Mistake 4: Poor Documentation , Missing purchase records, depreciation schedules, or improvement receipts makes audit reconstruction difficult.

Mistake 5: Ignoring 1031 History , If you acquired property through a like-kind exchange, your basis includes adjustments from the exchanged property.

Report each property separately on Form 4797 with its own calculation. The form includes space for multiple transactions, or attach additional statements.

Group by type: Section 1231 assets in Part I, ordinary gain/loss property in Part II, and calculate depreciation recapture in Part III for each. Net all Section 1231 gains and losses together, net gains become long-term capital gains on Schedule D.

Partners and S corporation shareholders receiving distributions use Part IV with Schedule K-1 coordination. Professional tax planning becomes essential when handling multiple simultaneous dispositions.

Maintain comprehensive documentation from purchase through sale:

Purchase Records , Original contract, closing statement, loan documents, inspection receipts, legal fees, title insurance. These establish initial basis.

Improvement Documentation , Receipts for capital improvements increasing basis (new roof, HVAC, major renovations). Regular repairs don't count.

Depreciation Schedules , Every tax return's depreciation schedule showing annual deductions. If missing, request IRS transcripts or reconstruct using purchase date and recovery periods.

Sale Documentation , Final contract, closing statement, broker commissions, legal fees, other selling expenses reducing gain.

Keep Form 4797 documentation for seven years after filing (IRS audits returns three years, six if you underreport 25%+).

Form 4797 reports sale or exchange of business property used in your trade or business. This includes depreciable property, real property for business operations, and property subject to Section 179 or 1245 recapture. The form calculates whether gains or losses are ordinary or capital.

File Form 4797 when selling property used in your business for over one year, buildings, equipment, vehicles, machinery. Personal property sales and investment capital assets use Schedule D or Form 8949.

Form 4797 reports business property sales and calculates depreciation recapture. Schedule D reports capital asset sales like stocks and investment property. Business property gains flow from Form 4797 to Schedule D for final calculation. Many transactions require both.

Depreciation recapture taxes the portion of gain equal to depreciation claimed at ordinary income rates (up to 25% for real property, your regular rate for personal property). Claiming $50,000 depreciation with a $100,000 gain means $50,000 is ordinary income.

Section 1231 property includes business real estate, depreciable assets, and certain livestock held over one year. Favorable tax treatment: gains taxed as capital gains (lower rates), losses deductible as ordinary losses (better). Report in Part I.

Yes. Business property losses are typically ordinary losses, deductible against any income without capital loss limitations. Investment property losses on Schedule D are limited to $3,000 annually against ordinary income.

You need original purchase price, purchase date, total depreciation claimed, sale price, sale date, and selling expenses. Gather depreciation schedules from prior returns, closing statements, and improvement receipts. Missing records require reconstructing basis.

We've processed 50,000+ tax returns since 2015, including complex Form 4797 calculations. Our offshore CPA team handles depreciation recapture, basis adjustments, and multi-property transactions while maintaining IRS compliance for U.S. firms.

Form 4797 requires precise calculations of depreciation recapture and basis adjustments. Mistakes create unexpected tax bills or IRS corrections.

Gather complete records, purchase documents, depreciation schedules, sale closing statements. Calculate adjusted basis correctly, identify which sections apply, and report recapture amounts accurately. For complex situations, professional help prevents costly errors.

About Madras Accountancy: Since 2015, we've served as offshore partners to U.S. CPA firms, processing 50,000+ tax returns including business property sales and complex Form 4797 situations.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.