.png)

You're buying $100,000 in equipment for your business. Your accountant mentions Section 179, but you're unsure if you should expense it now or depreciate it over years. Choosing wrong could cost thousands in delayed tax benefits.

IRS Section 179 lets businesses deduct the full purchase price of qualifying equipment placed in service during the tax year, instead of depreciating it over multiple years. For 2024, deduct up to $1,220,000 in equipment purchases (phase-out begins at $3,050,000 total purchases). This reduces taxable income immediately, lowering your current tax bill rather than spreading benefits over 5-27 years.

This guide explains what Section 179 is, what qualifies, limits, and how to claim it.

Section 179 of the Internal Revenue Code lets businesses expense (deduct immediately) qualifying property costs in the year placed in service, rather than depreciating over its useful life. A $50,000 equipment purchase reduces 2024 taxable income by $50,000, not $10,000 spread over five years.

Applies to tangible property used in your trade or business: machinery, equipment, vehicles, computers, furniture, and certain nonresidential real property improvements. Property must be purchased and placed in service (ready for use) during the tax year.

Section 179 is limited to your business's taxable income. If your business earned $80,000 and you bought $100,000 equipment, you can only deduct $80,000. The remaining $20,000 carries forward.

Unlike bonus depreciation (no income limitation), Section 179 requires business profit. This makes it ideal for profitable businesses investing in equipment. Understanding how Section 179 and bonus depreciation work together maximizes immediate tax savings.

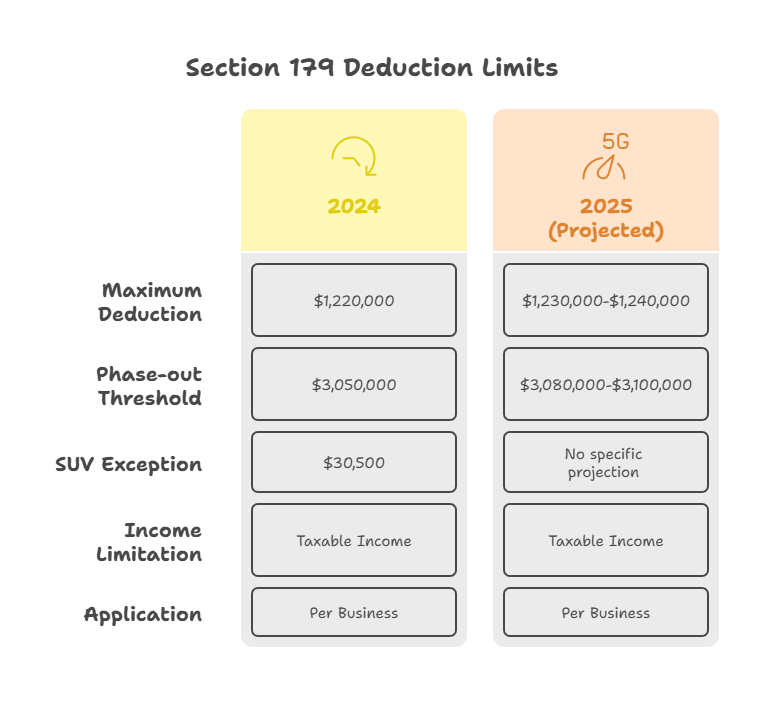

For 2024, maximum Section 179 deduction is $1,220,000 for all qualifying property placed in service.

Phase-out: Deduction phases out dollar-for-dollar once total purchases exceed $3,050,000. Buy $3,150,000 equipment = $1,120,000 max deduction ($1,220,000 minus $100,000 overage).

2025 projections: Limits increase with inflation. Expect $1,230,000-$1,240,000 deduction with $3,080,000-$3,100,000 phase-out threshold.

SUV exception: SUVs over 6,000 pounds have $30,500 Section 179 limit for 2024, preventing luxury vehicle full deductions.

Income limitation: Section 179 cannot exceed taxable income. $500,000 business income = $500,000 maximum Section 179 deduction.

Limits apply per business, not per taxpayer. Multiple businesses each calculate their own Section 179 based on income and purchases.

Qualifying property must be tangible, purchased (not inherited/gifted), used in your trade or business, and placed in service during the tax year.

Qualifies: Equipment, machinery, vehicles (trucks/vans over 6,000 lbs get full deduction; SUVs capped at $30,500), computers, office furniture, off-the-shelf software, qualified improvement property (interior improvements to nonresidential buildings: HVAC, fire protection, alarms, roofs added since 2018).

Doesn't qualify: Land, buildings (structure itself), property used outside U.S., property used 50% or less for business, inventory, investment property, pre-2018 AC/heating units.

Real property (buildings, land) generally doesn't qualify except specific qualified improvements. Understanding these distinctions prevents claiming ineligible property triggering IRS adjustments. Our guide to avoiding accounting mistakes covers proper asset classification.

File Form 4562 (Depreciation and Amortization) with your business tax return to elect Section 179.

Step 1: Identify qualifying property purchases made during the tax year.

Step 2: Calculate maximum deduction ($1,220,000 for 2024) minus any phase-out if purchases exceed $3,050,000.

Step 3: Apply income limitation—deduction cannot exceed business taxable income.

Step 4: Complete Form 4562 Part I. List property description, cost, elected amount. Total cannot exceed allowable deduction.

Step 5: Attach to Schedule C (sole proprietors), Form 1065 (partnerships), Form 1120S (S corps), or Form 1120 (C corps).

Partnership/S corp notes: Entity makes election, but income limits apply at entity and owner levels. Deduction passes through; owners apply their own income limitations.

Carryforward: Unused deductions carry forward indefinitely. Elected $200,000 but only deducted $150,000 due to income limits? $50,000 carries forward.

Many businesses benefit from professional tax preparation when claiming Section 179 because calculations, phase-outs, and depreciation interactions require precise handling.

Both accelerate equipment deductions but work differently:

Income limitation: Section 179 cannot exceed taxable income. Bonus depreciation has no limit—deduct even with losses.

Dollar limit: Section 179 caps at $1,220,000 (2024). Bonus depreciation has no cap (100% of unlimited purchases, though phasing to 80% for 2024, 60% for 2025).

Property types: Section 179 covers more types including real property improvements and SUVs. Bonus covers tangible property with 20-year or less recovery periods.

Used property: Section 179 allows used property if new to you. Bonus requires property be new (first use by any taxpayer).

Strategy: Use Section 179 first for items with specific limits (SUVs at $30,500), then apply bonus depreciation to remaining purchases.

Not placed in service - Buy equipment December 28, arrives January 3? Doesn't qualify for prior year—not placed in service until ready for use.

Exceeding income - Business earned $75,000 but elected $150,000 Section 179? Only deduct $75,000; $75,000 carries forward.

Forgetting SUV limits - $90,000 Range Rover for business? Section 179 caps SUVs at $30,500. Remaining $59,500 must be depreciated or use bonus depreciation.

Ineligible improvements - Not all building improvements qualify. Structural components (new floors, walls, expansion) don't qualify. Only specific qualified improvement property qualifies.

Missing Form 4562 - Section 179 isn't automatic. Must file Form 4562 and elect. Forget = depreciate instead, losing immediate benefit.

Personal use allocation - $50,000 vehicle 70% business, 30% personal? Section 179 limited to $35,000 (70% of cost). Property must be used 50%+ for business to qualify.

Yes, if new to your business. Section 179 allows used property as long as you're the first business user. A used truck purchased for your business qualifies, but property transferred from personal use typically doesn't.

You may face recapture—repaying some deduction as ordinary income. Sell a $40,000 vehicle three years after claiming Section 179? Report gain (possibly recapture) based on adjusted basis. Hold property longer than recovery period to avoid recapture.

Yes. Section 179 applies whether you paid cash or financed. Deduct full purchase price immediately, even with monthly payments. Key: property must be placed in service, not fully paid off.

Generally no. Section 179 requires purchase. Lease payments are ordinary business expenses deducted over the lease term. Some leases with purchase options might qualify if structured correctly.

Rarely. Section 179 requires trade or business use. Rental real estate is usually investment property unless you're a real estate professional or operate hotels/motels. However, equipment used in rentals (mowers, tools) might qualify.

Section 179 deducts full cost immediately in one year. Regular depreciation spreads deductions over useful life (5 years computers, 7 years furniture, 27.5 years residential rentals). Section 179 provides immediate tax savings.

Yes. Buy $100,000 equipment with $60,000 taxable income? Elect $60,000 Section 179, depreciate remaining $40,000. This optimizes current deduction while preserving basis.

Can't deduct Section 179 in loss years, but deduction carries forward indefinitely. Business loses $10,000 with $50,000 elected Section 179? Full $50,000 carries forward to next profitable year.

Section 179 provides immediate tax relief for businesses investing in equipment, reducing taxable income by up to $1,220,000 in 2024. Time purchases strategically, ensure property is placed in service before year-end, and complete Form 4562 correctly.

Plan equipment purchases with tax implications in mind. Buying in December versus January shifts thousands in tax savings between years. Most businesses save $10,000-$300,000+ annually through proper Section 179 planning.

Madras Accountancy helps businesses maximize Section 179 and bonus depreciation while maintaining compliance. We ensure you claim every eligible deduction, optimize timing, and document all elections. Contact us to optimize your 2024 equipment deductions and plan your 2025 strategy.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.