When you sit in a planning meeting with auditors, you will hear certain words over and over. Two of the most important are "materiality" and "risk." To an owner, they can sound abstract, even a bit like jargon that belongs in a textbook.

Underneath the technical language, though, the ideas are fairly practical. They explain why auditors spend a lot of time on certain accounts and only a little on others, and why they ask deep questions about one area of your business while barely touching another.

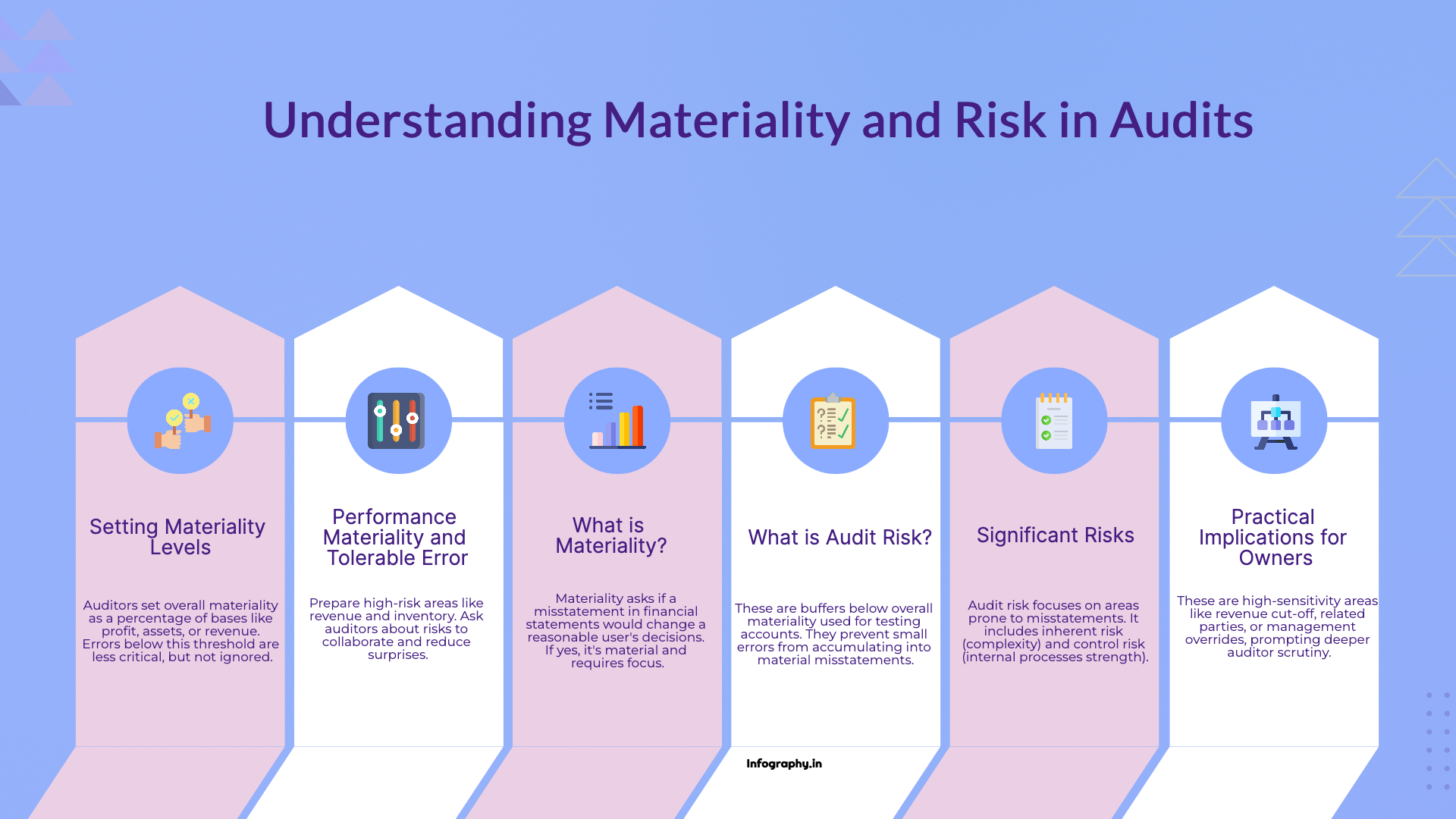

Materiality is the auditors way of asking, "Would a reasonable user of these financial statements change their decisions if this number were wrong?" If the answer is yes, then the amount is material. If not, it may still be an error, but it is less important in the context of the overall picture.

Auditors often start with a percentage of a base figure, such as profit before tax, total assets, or revenue, to set an overall materiality level. For example, they might say that misstatements under a certain threshold are unlikely to affect decisions, while those above it clearly could.

This does not mean smaller errors are ignored. It means the audit procedures are designed primarily to catch mistakes that cross that significance line, since time and budget are not infinite.

In practice, auditors do not wait until the exact threshold is crossed to care. They build in a buffer. Concepts like performance materiality and tolerable error come into play. These are lower levels used for testing individual account balances or classes of transactions, to reduce the chance that many small errors add up to something big.

For you as an owner, the key takeaway is that auditors are not aiming for absolute perfection. They are aiming for financial statements that are free of material misstatement. Tiny rounding differences will not derail an audit. Larger issues that could mislead readers will.

Risk in an audit context is about where misstatements are more likely to exist and not be caught. Auditors consider inherent risk (how complex or judgment heavy an area is) and control risk (how strong or weak your internal processes are) when deciding how much work to do on each section of the financial statements.

For example, cash in a simple bank account has relatively low inherent risk when reconciled properly. Complex revenue recognition arrangements, on the other hand, often carry higher risk because they involve estimates, multiple performance obligations, or unusual contract terms.

If your business relies heavily on inventory that is hard to count or easy to lose, auditors will see that as a higher risk area and plan more detailed procedures there. The goal is to focus effort where it matters most.

Sometimes auditors identify specific significant risks, areas where the combination of complexity, judgment, or past issues makes them particularly sensitive. Common examples include revenue cut off around year end, related party transactions, or management override of controls.

When you see auditors asking many questions about a particular transaction type while barely glancing at others, it is often because they have flagged that area as a significant risk. That is not necessarily an accusation. It is a reflection of how their standards tell them to allocate their attention.

Understanding materiality and risk can make audit conversations less mysterious. If you know that revenue and inventory are high risk areas in your industry, it makes sense to invest extra time keeping those records clean and well documented. If you realize that certain disclosures are particularly important to lenders or investors, you can review them carefully before the auditors arrive.

When you talk with the audit team, do not be afraid to ask, "Which areas have you identified as higher risk for us this year, and how can we help you get comfortable there?" That simple question can lead to more focused preparation and fewer surprises on both sides.

Materiality and risk are not just buzzwords. They are the lenses through which auditors view your numbers. Seeing your business through those lenses, even briefly, can help you strengthen your own financial processes along the way. For more on preparing for audits, see our guide on preparing for your first external audit.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.