Nothing reminds you how small the world has become like getting paid from three different countries in the same week. The sales side feels exciting. Then you open your accounting software and realize everything is landing in different currencies, on different days, at different rates. That feeling? Mild panic, mixed with a little curiosity.

Multi-currency bookkeeping does not have to be chaos. It just punishes guesswork. A few clear rules, followed consistently, make the difference between reports you can trust and a spreadsheet that nobody fully believes.

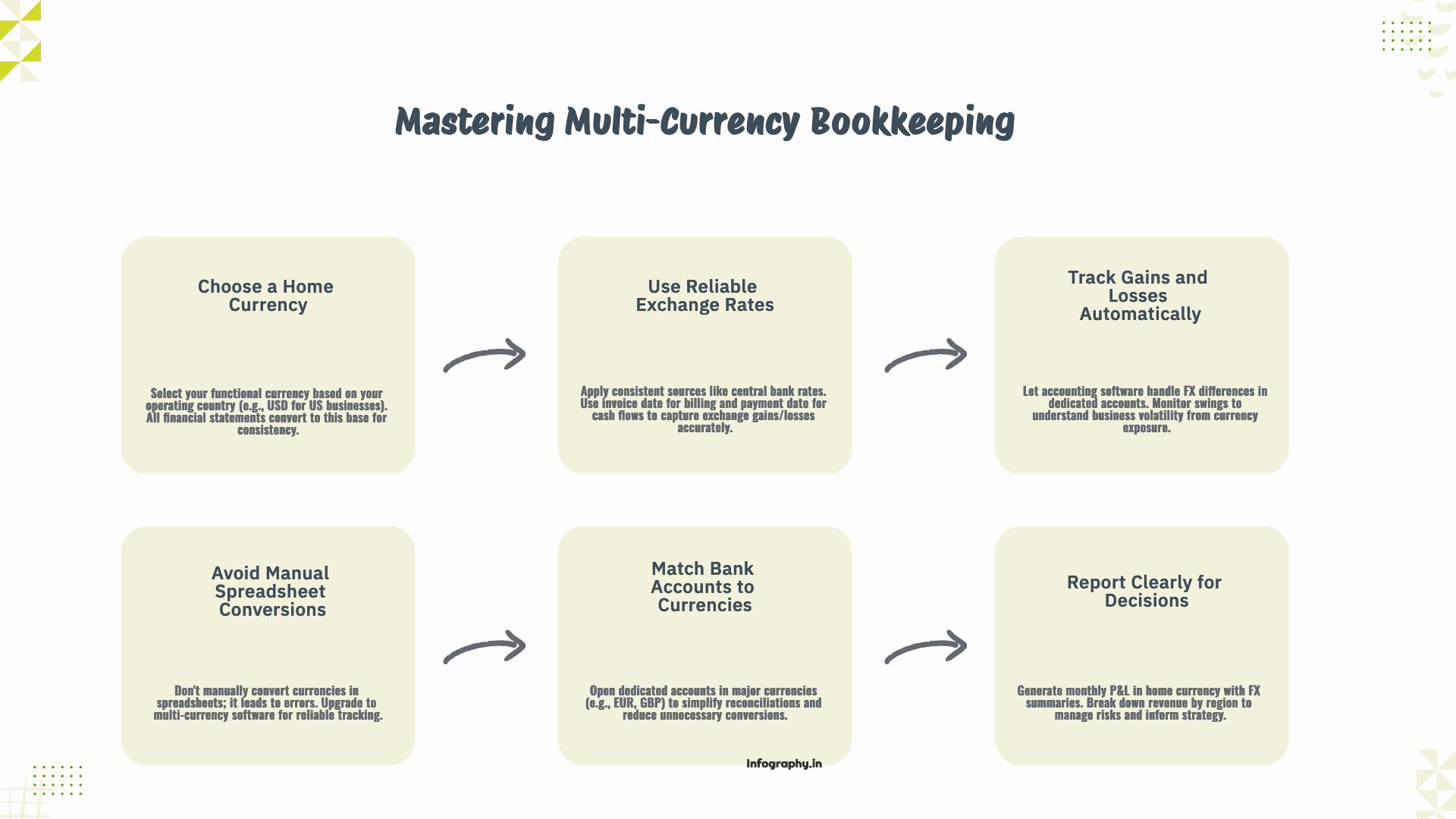

First, decide on your functional currency, also called the home or base currency. For most small businesses, that is simply the currency of the country where you operate and file taxes. If you are based in the United States, that is the dollar. If you are in the eurozone, it might be the euro, and so on.

All of your financial statements will ultimately be presented in that currency. The job of your accounting system is to translate foreign cash flows back into this home base on a consistent basis. Problems start when you flip between bases in your head. If your P and L is in dollars, but you are evaluating a contract in pounds using gut feel, you are asking for surprises.

Every time you record a foreign currency transaction, you need an exchange rate. Some systems pull daily rates automatically from a data feed. Others require you to input them manually. Whichever route you use, be consistent about the source. Central bank reference rates, major financial data providers, or your bank's posted rates all work, as long as you do not mix and match randomly.

For invoices, use the rate on the invoice date. For payments, use the rate on the date the cash actually moves. The gap between those two rates is where exchange gains and losses live. They are not mistakes. They are simply the cost of dealing with money that changes value over time.

Speaking of gains and losses, do not try to hide them in sales or expense accounts. Good accounting tools have specific accounts for realized and unrealized foreign exchange differences. When a foreign invoice is settled, the system should automatically calculate the difference between the original rate and the payment rate, and post that to an FX gain or loss account.

At first, seeing noisy numbers there can feel uncomfortable. Over time, you will learn what is normal for your business. A company with tight settlement cycles and few currencies will see smaller swings. One that holds large balances in foreign accounts will see more volatility. The point is to measure it clearly, not bury it.

One of the fastest ways to break your books is to export everything to a spreadsheet, convert currencies by hand with a few ad hoc formulas, and then reimport totals. I have watched this happen in real life, and it always ends with someone saying, "I am not sure which version is right anymore."

If your current accounting system does not support multi-currency at all, consider upgrading before the volume of foreign transactions grows. If that is not possible yet, at least keep a clear audit trail: document which rate you used for each batch of conversions and keep the underlying detail.

Another simple but powerful practice is to open separate bank accounts in your main operating currencies instead of forcing everything through one account. If you are routinely getting paid in euros and pounds, having dedicated euro and pound accounts lets you pay expenses in those currencies without constant conversions.

From a bookkeeping perspective, that also makes reconciliation cleaner. Each bank ledger is in its own currency, and the system handles translation into your home currency at the statement date. You are not guessing how much of a mixed currency account is exposed at any given time.

Finally, remember that multi-currency bookkeeping is not just about being technically correct. It is about telling a clear story. Internally, management might want to see revenue broken down by currency or region to understand where margins are strong or weak. Externally, your tax filings will require everything stated in your home currency.

Design a simple reporting rhythm. Maybe once a month, you review a home currency P and L plus a short schedule showing major foreign balances and any large FX gains or losses. That way, currency risk moves from a vague worry to a visible, trackable factor in your decisions.

You do not need to love exchange rates to get this right. You just need a set of rules and the discipline to follow them the same way every time a foreign invoice hits your inbox. For more on streamlining your accounting workflow, see our guide.

Related read: accounting software.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.