Qualified Opportunity Zones (QOZs) were introduced as one of the headline incentives in the Tax Cuts and Jobs Act. For investors with large capital gains from stock sales, business exits, or property dispositions, the promise was simple: roll those gains into a QOZ fund and defer the tax bill while potentially earning tax-free growth on the new investment.

The deferral, however, was never permanent. A hard date was written into the law, and that date—December 31, 2026—is now close enough that planning can no longer be postponed. Understanding what happens on that date, and how to prepare, is essential for anyone who moved gains into a QOZ structure.

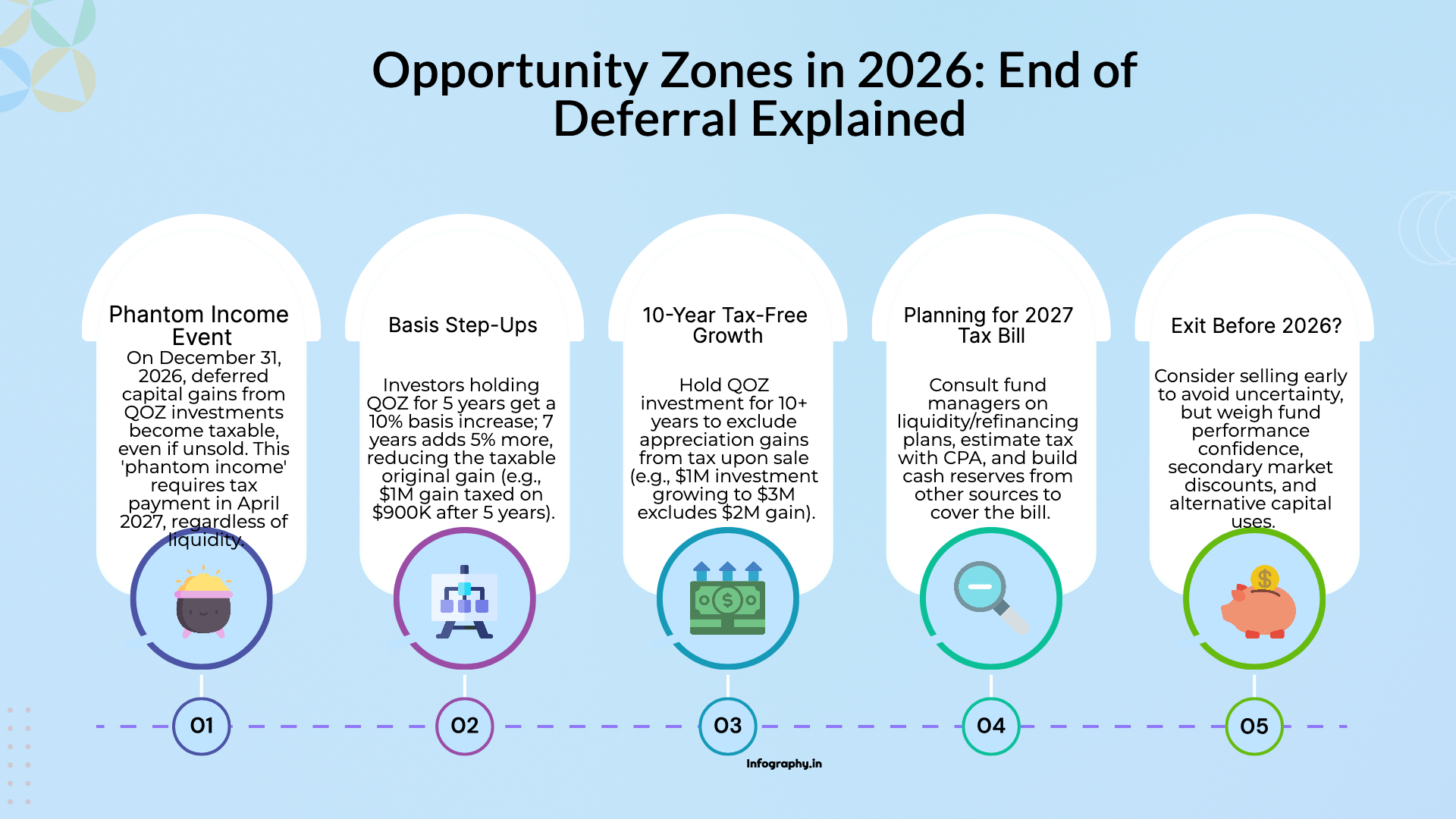

When you rolled an eligible capital gain into a QOZ fund within the required window, you postponed paying tax on that original gain. The law states that this deferment lasts until the earlier of two events: when you dispose of the QOZ investment, or December 31, 2026.

On that date, the deferred gain becomes taxable, even if you have not sold your QOZ investment and have not received any cash. In practical terms:

This is why the event is often called "phantom income." You owe tax on something you do not see as current cash in hand.

For early QOZ investors, the law provided basis increases to soften the 2026 impact. If you held your QOZ investment long enough before the deferral end date, a portion of the original gain is effectively forgiven.

The key thresholds were:

In simple terms, an investor who rolled a $1 million gain into a QOZ fund and met the five-year test might only pay tax on $900,000 of that gain. The remaining $100,000 becomes tax-free. That does not eliminate the 2026 tax bill, but it reduces it meaningfully.

The often more powerful aspect of QOZ investing is separate from the 2026 deferral. If you hold your QOZ investment for at least ten years, you can generally exit the investment without paying tax on the appreciation that occurred inside the fund.

Using the same example, if a $1 million QOZ investment grows to $3 million over a decade, the $2 million of internal gain can be excluded from tax when you dispose of the investment after the required holding period. That benefit is not tied to the 2026 date and remains even after you pay tax on the original deferred gain.

Understanding this distinction matters. The 2026 event affects the gain you brought in. The ten-year rule affects the gain you build going forward.

For many investors, the most immediate concern is simple: how to pay a sizable tax bill in April 2027 when capital is tied up in illiquid projects. Waiting and hoping that the fund will distribute cash in time is not a strategy.

Practical steps include:

Creating a plan reduces the risk of being forced into hasty asset sales or unfavorable borrowing just to cover tax obligations.

Some investors are considering selling their QOZ interests before the deferral deadline. Doing so accelerates recognition of the original deferred gain, plus any gain on the QOZ investment itself. In exchange, you eliminate uncertainty about future regulations, fund performance, or refinancing risk.

Questions to weigh include:

There is no universal right answer. The deferral and ten-year exclusion rules are tools; whether to continue using them depends on current facts and future plans.

The 2026 event does not occur in isolation. It lands in a tax year that will also include your other income, deductions, and transactions. That means:

Running scenarios with your advisors over the next few filing seasons can help you decide when to realize other gains and losses so that the required QOZ recognition fits as smoothly as possible.

Opportunity Zones were designed to encourage long-term, patient investment. The upcoming deferral end date does not erase their benefits, but it does change the shape of the conversation. Instead of treating the deadline as a distant footnote, it now belongs at the center of your planning.

If you hold QOZ investments, the most helpful steps now are straightforward: understand your numbers, clarify your fund's plans, and coordinate the 2026 recognition with the rest of your tax and cash flow picture. With those pieces in place, the program can still deliver what it promised—a bridge from a past gain into a better-structured, longer-term investment—without turning 2027 into an unwelcome surprise. For more on opportunity zone tax benefits, see our comprehensive guide.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.