.png)

You bought your first rental property aexpecting steady income and solid tax deductions. Then tax season arrives, and your CPA tells you those $15,000 in rental losses can't offset your W-2 income. Welcome to passive activity loss rules.

The IRS classifies most rental real estate as passive activities, which means losses from rental properties can only offset passive income, not your salary, business profits, or investment gains. However, there's a $25,000 special allowance for active participants, and real estate professionals can avoid these limits entirely. Understanding these rules determines whether you'll carry losses forward for years or use them immediately to reduce your tax bill.

This guide explains how passive activity loss rules work, who qualifies for exceptions, and practical strategies to maximize your rental property deductions in 2025.

Passive activity loss rules, established by the IRS in 1986, limit your ability to deduct losses from passive activities against active income. A passive activity is any rental activity or trade or business in which you don't materially participate. For most rental property owners, this means rental losses can only offset income from other passive sources, like dividends, interest, or gains from other rental properties.

The purpose behind these rules is to prevent high-income taxpayers from using paper losses from rental real estate to shelter their earned income.

Before 1986, investors could buy rental properties primarily for tax deductions, creating artificial losses through depreciation while building equity. The passive activity loss rules changed this landscape significantly.

Here's what matters most: if your rental property generates a $10,000 loss for the tax year, you generally cannot use that loss to reduce your W-2 income, business profits, or investment gains. Instead, that loss becomes suspended and carries forward to future years until you either generate passive income to offset it or dispose of the property in a fully taxable transaction.

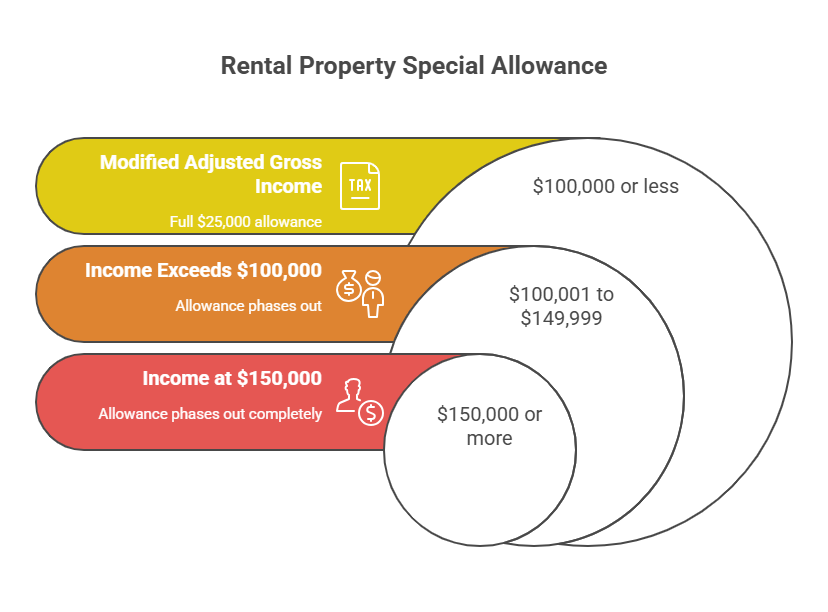

The $25,000 special allowance provides relief for active rental property owners with modified adjusted gross income below $100,000. If you actively participate in your rental real estate activities, you can deduct up to $25,000 in rental losses against your non-passive income each year, even your salary or business income.

Active participation requires meaningful involvement in management decisions, but it's a less stringent standard than material participation. You satisfy active participation if you make management decisions like approving tenants, setting rental terms, approving repairs, or making decisions about capital improvements. You can hire a property manager and still maintain active participation status as long as you retain final decision-making authority.

The income phase-out works like this: you get the full $25,000 allowance if your modified adjusted gross income is $100,000 or less. For every dollar your income exceeds $100,000, you lose 50 cents of the allowance. At $150,000 in modified adjusted gross income, the allowance phases out completely.

If you're filing separately while married, different rules apply, the allowance drops to $12,500 with a lower phase-out threshold.

Most rental property owners with day jobs fall into this category. If you earn $90,000 annually and your rental property shows a $20,000 loss, you can deduct the full loss against your salary. This special allowance can save you $4,000 to $7,000 annually depending on your tax bracket, making it one of the most valuable rental property tax benefits available.

Real estate professional status lets you treat rental losses as non-passive, allowing full deductions against any income type without the $25,000 cap. However, qualifying requires meeting strict IRS requirements that most rental property owners cannot satisfy.

To qualify as a real estate professional, you must spend more than 750 hours during the tax year in real property trades or businesses in which you materially participate. Additionally, more than half of your total working hours for the year must be in real estate activities. These real estate activities include property development, construction, management, leasing, brokerage, or similar fields, not just owning rental properties.

The 750-hour test sounds manageable until you realize it requires material participation. Material participation generally means more than 500 hours in the activity, or substantially all participation if multiple people are involved, or more than 100 hours if no one else participates more.

For rental properties specifically, you must also make a separate election to aggregate all rental properties as a single activity, otherwise the material participation test applies to each property individually.

Here's a real scenario: Sarah works full-time as a real estate agent (2,000 hours annually) and owns three rental properties where she spends 600 hours on management and maintenance. She meets the real estate professional requirements because more than half her work time (2,600 total hours) involves real estate, and she exceeds 750 hours in real estate activities. If she also materially participates in her rental activities, her rental losses become non-passive and can offset her commission income without limitation.

Most rental property owners don't qualify because they maintain other full-time careers. If you work 2,000 hours annually as an engineer, you'd need to spend more than 2,000 hours in real estate activities, essentially impossible unless real estate becomes your primary occupation. Our tax planning strategies for small businesses guide explores alternative approaches when real estate professional status isn't achievable.

When passive losses exceed your passive income and available allowances, those excess losses don't disappear, they become suspended losses that carry forward indefinitely. The IRS tracks these suspended losses year after year until you can use them against future passive income or when you dispose of the property.

Suspended losses accumulate on Form 8582, which calculates your passive activity loss limitation each year.

If your rental property generates a $15,000 loss but you only have $5,000 in passive income and don't qualify for the $25,000 allowance, you can use $5,000 immediately while $10,000 becomes suspended. Next year, if you generate $8,000 in passive income, you can use $8,000 of your prior-year suspended losses.

The key trigger for releasing all suspended losses is disposing of your entire interest in the passive activity in a fully taxable transaction. When you sell your rental property to an unrelated party, all suspended losses from that property become deductible in the year of sale, regardless of whether you have passive income.

This creates a significant tax benefit in the disposition year.

Consider this example: you bought a rental property in 2020 and accumulated $40,000 in suspended losses over five years because your income exceeded $150,000 and you had no other passive income. In 2025, you sell the property for a $100,000 gain. You can deduct all $40,000 in suspended losses against that gain, effectively paying tax on only $60,000 instead of the full $100,000. This is why keeping detailed records of suspended losses matters, the IRS requires you to track them, and they provide substantial value at disposition.

Death doesn't release suspended losses the same way. When you die owning rental properties, your heirs receive a stepped-up basis, but your suspended passive losses generally disappear. However, your estate may be able to deduct them on the final tax return under specific circumstances. The rules around death and suspended losses are complex enough that consulting with a tax professional experienced in estate planning becomes essential.

At-risk rules limit your deductible losses to the amount you have "at risk" in the activity, generally, your cash investment plus recourse debt for which you're personally liable. These rules apply before passive activity loss rules, creating an additional layer of limitation for rental property owners.

Your amount at-risk includes money you invested, amounts you borrowed for which you're personally liable, and your share of recourse debt if you own the property through a partnership or LLC. Non-recourse debt, loans where the lender can only take the property if you default, not pursue your other assets, generally doesn't increase your at-risk basis except for qualified non-recourse financing on real estate.

Here's why this matters: you buy a rental property for $300,000 with $50,000 down and a $250,000 non-recourse mortgage. In year one, the property generates a $60,000 loss from depreciation and operating expenses.

Your at-risk amount is only $50,000 (your cash investment), so you can only deduct $50,000 in losses. The remaining $10,000 becomes suspended under at-risk rules, separate from passive activity loss limitations.

The interaction between these rules creates a two-step limitation process. First, at-risk rules limit your losses to your economic investment. Second, passive activity rules limit your ability to use those losses against non-passive income. You must clear both hurdles to deduct rental losses against your salary or business income. Understanding how Section 179 and bonus depreciation interact with these limitations helps you plan deductions more strategically.

Several strategies help rental property owners work within passive activity loss rules to maximize current-year deductions and minimize suspended losses.

Generate passive income from other sources. If you have rental losses, creating passive income from other investments lets you use those losses immediately. Consider investing in a limited partnership, publicly traded partnership, or other passive investments that generate income. Some real estate investors intentionally diversify into passive income investments specifically to absorb rental losses.

Bunch deductions strategically. Since suspended losses carry forward indefinitely, timing major repairs or improvements can optimize your tax benefits. If you're nearing retirement when your income will drop below $100,000, deferring major repairs until then lets you take advantage of the $25,000 allowance. Conversely, if you expect income to rise, accelerating deductions into earlier years makes sense.

Convert short-term rentals to active businesses. Rental properties where the average guest stay is seven days or less aren't automatically classified as passive activities if you provide substantial services. Vacation rentals managed actively can qualify as non-passive businesses, though this requires significant involvement in guest services, cleaning, and property management. Our guide to small business tax compliance covers the documentation needed for this approach.

Consider cost segregation studies. Cost segregation accelerates depreciation by reclassifying building components into shorter recovery periods. While this increases early-year losses, it provides more value if you can use those losses currently rather than suspend them. This strategy works best if you qualify for the $25,000 allowance or have other passive income.

Make the grouping election carefully. You can elect to treat all rental real estate as a single activity, which helps you meet the material participation threshold. However, this election is binding and affects how you calculate gain or loss on disposition. Once made, you generally cannot change it without IRS consent. The election works best if you're close to qualifying as a real estate professional but need to aggregate activities to meet the hour requirements.

The most effective strategy depends on your specific situation, your income level, other investments, career trajectory, and long-term real estate plans.

Many rental property owners benefit from working with tax professionals who specialize in real estate because the rules are complex and the dollar amounts involved make professional guidance cost-effective.

Passive activity loss rules flow through to individual partners and S corporation shareholders, but the determination of whether activities are passive happens at the individual level, not the entity level.

When you own rental property through an LLC taxed as a partnership or through an S corporation, the entity reports income or losses on Schedule K-1, which flows to your personal return. The entity doesn't determine whether the activity is passive, that determination depends on your level of participation.

Two partners in the same LLC might treat the same rental activity differently: one as passive (because they don't participate) and another as non-passive (because they materially participate in management).

This creates planning opportunities. If you own rental properties with a spouse or business partner, you can structure participation to maximize one person's involvement to qualify as a real estate professional while the other maintains their career.

The real estate professional spouse can then deduct rental losses against the couple's combined income on a joint return.

However, special rules apply to limited partners. As a limited partner, the IRS presumes you don't materially participate unless you meet specific exceptions. You must prove you participated more than 500 hours, or substantially all participation, or meet other strict tests. This makes qualifying for real estate professional status much harder through limited partnership interests.

S corporation shareholders face similar challenges. Your activity in the corporation generally doesn't count toward material participation unless you perform services as an employee or in another capacity. Simply owning shares while the corporation manages rentals typically results in passive treatment. Understanding these considerations when structuring your business prevents costly classification mistakes.

The IRS requires detailed recordkeeping for passive activities, and inadequate documentation can result in disallowed deductions, penalties, and interest. Maintaining organized records protects your deductions and simplifies compliance.

Track time spent on rental activities.

If you claim active participation or real estate professional status, maintain contemporaneous time logs showing dates, activities performed, and hours spent. Calendar entries, time-tracking apps, or detailed logs work well. The IRS expects contemporaneous records, you can't recreate them years later during an audit. Record activities like tenant communications, property inspections, maintenance coordination, financial management, and time spent analyzing acquisitions or dispositions.

Document all suspended losses.

Create a spreadsheet tracking suspended losses by property and by year. Form 8582 calculates current-year limitations, but you need your own records to track cumulative suspended losses over multiple years. When you sell a property, you'll need this documentation to claim all suspended losses.

Maintain activity-level records.

Keep separate records for each rental property showing income, expenses, and time spent. If you own properties in different states or have properties with different operational characteristics, separate recordkeeping becomes even more critical. This organization also helps with state tax compliance and simplifies due diligence if you sell properties.

Preserve acquisition and improvement documentation.

Keep purchase documents, closing statements, improvement receipts, and depreciation schedules for each property. These documents establish your basis, support depreciation deductions, and prove capital improvements that increase basis and reduce gain on sale.

Document material participation tests.

If you claim to materially participate in rental activities, document how you meet one of the seven IRS tests. The most common tests are the 500-hour test and the substantially-all-participation test. Your records should clearly demonstrate which test you satisfy and provide supporting evidence.

Regular recordkeeping throughout the year is far easier than scrambling to reconstruct records during tax preparation or an IRS audit. Consider setting up a simple system, even just 30 minutes monthly updating spreadsheets and organizing receipts. This minimal investment saves hours later and protects deductions worth thousands of dollars.

Yes, if you actively participate in managing your rental property and your modified adjusted gross income is below $100,000, you can deduct up to $25,000 in rental losses against your salary. The deduction phases out between $100,000 and $150,000 in income.

If your income exceeds these thresholds, your losses become suspended and carry forward to future years when you have passive income or sell the property.

Active participation is a less stringent standard requiring meaningful involvement in management decisions like approving tenants, setting rental terms, and approving repairs. Material participation requires significantly more involvement, generally more than 500 hours annually in the activity. Active participation qualifies you for the $25,000 special allowance, while material participation (combined with real estate professional status) lets you treat rental losses as non-passive without dollar limitations.

No, suspended passive losses carry forward indefinitely until you can use them. You can use suspended losses when you generate passive income in future years or when you dispose of your entire interest in the property in a fully taxable transaction. The losses don't expire after a certain number of years, but you must track them carefully because the IRS doesn't track them for you.

Yes, but the allowance drops significantly. Each spouse can claim up to $12,500 in deductions (not $25,000), and the phase-out begins immediately, there's no $100,000 threshold. If either spouse actively participates in rental real estate, they must report all passive income and losses separately. This makes filing separately much less advantageous for rental property owners compared to filing jointly.

Maintain detailed contemporaneous time logs showing all time spent in real property trades or businesses, including property management, leasing, repairs, tenant communications, and related activities. You need to prove you spent more than 750 hours in these activities and that real estate work comprised more than half your total working hours for the year. Calendar entries, time-tracking software, or detailed logs with dates and descriptions provide the best documentation.

When you sell your rental property in a fully taxable transaction to an unrelated party, all suspended passive losses from that property become deductible in the year of sale. These losses offset the gain on sale, potentially reducing your taxable gain significantly. This is one of the most valuable aspects of suspended losses, they're not wasted, just deferred until disposition.

Yes, you can elect to treat all your rental real estate as a single activity, which helps you meet the material participation threshold more easily. However, this election is binding and affects how you calculate gain or loss when you sell individual properties. You should make this election carefully, preferably with guidance from a tax professional, because it cannot be easily changed once made.

Not always. If the average guest stay is seven days or less and you provide substantial services (like cleaning, concierge services, or meals), the IRS may classify your vacation rental as a non-passive business activity rather than rental real estate.

This classification lets you deduct losses against other income without passive activity limitations, but it requires significant personal involvement in providing services to guests and proper documentation of your activities.

Passive activity loss rules significantly impact rental property tax benefits, but understanding the exceptions and planning strategies lets you maximize deductions.

Most rental property owners with income below $100,000 can deduct $25,000 in rental losses annually through active participation. Those who can't use losses immediately still benefit from suspended losses at disposition, often decades later when they sell properties.

The key is maintaining detailed records, understanding your qualification for various exceptions, and planning strategically around income thresholds. If you're approaching $100,000 in income, small adjustments, like timing bonuses or maximizing retirement contributions, can preserve your $25,000 allowance. If you're considering making real estate your primary business, documenting your path to real estate professional status from day one protects your ability to deduct losses fully.

At Madras Accountancy, we help real estate investors and CPA firms navigate these complex rules, optimize tax positions, and maintain the detailed documentation the IRS requires. Whether you're buying your first rental property or managing a portfolio, working with experienced tax professionals ensures you maximize deductions while remaining compliant. Contact us to discuss how passive activity loss rules affect your specific situation and strategies to minimize your tax liability.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.