.png)

Rental property tax deductions are expenses you can subtract from your rental income to reduce your taxable income and lower your tax bill. Property owners typically deduct mortgage interest, property taxes, repairs, depreciation, insurance, and operating expenses. These deductions can reduce your rental income taxes by 30-40% when properly documented and claimed on Schedule E of your tax return.

You bought a rental property expecting steady income. Then tax time arrives, and you're staring at rental income that gets taxed like regular wages. Most new landlords don't realize they're overpaying taxes by thousands because they're missing deductions hiding in plain sight.

The IRS allows property owners to deduct ordinary and necessary expenses for managing and maintaining rental properties. Yet 60% of landlords leave money on the table by not tracking expenses properly or confusing repairs with improvements. Here's what you can actually deduct, backed by IRS guidelines and real examples from property owners we work with.

A rental property deduction is any ordinary and necessary expense you pay to manage, maintain, or operate your rental real estate. The IRS defines "ordinary" as common in the rental business and "necessary" as helpful and appropriate for your rental activities.

You report rental income and expenses on Schedule E (Form 1040) of your tax return.

The key distinction: you can only deduct expenses in the year you pay them if you use cash-basis accounting, which most individual landlords do. Expenses must be directly related to your rental property and documented with receipts, invoices, or bank statements.

Property owners can't deduct personal expenses or costs for improvements that add value to the property, those get depreciated over time instead. The market value of the property doesn't matter for deduction purposes; what counts is the actual expense you paid.

Tax deductions directly reduce your taxable rental income, which lowers your tax bill. If you collect $30,000 in rental income annually and have $12,000 in deductible expenses, you only pay taxes on $18,000 of income.

For property owners in the 24% tax bracket, that $12,000 in deductions saves $2,880 in federal taxes alone. Add state taxes, and you're looking at $3,500+ in tax savings. Over three rental properties, that's more than $10,000 staying in your pocket instead of going to the IRS.

Beyond immediate tax savings, proper expense tracking creates documentation for IRS audits and helps you understand your rental property income and expenses clearly. Many landlords discover their property isn't as profitable as they thought once they account for all operating expenses.

The IRS allows landlords to deduct several categories of expenses related to their rental properties. Here are the deductions that deliver the biggest tax savings for owners of rental properties:

Mortgage interest is typically your largest deduction. If you pay $18,000 annually on your rental property mortgage and $12,000 goes toward interest, that entire $12,000 is deductible. Property taxes you pay to local governments are also fully deductible as an operating expense.

Unlike your personal home where mortgage interest is an itemized deduction, rental property mortgage interest gets reported on Schedule E and directly reduces your rental income. You'll receive Form 1098 from your lender showing the interest amount for the tax year.

Depreciation lets you deduct the cost of your rental property over 27.5 years for residential properties. If you bought a rental property for $275,000 (excluding land value), you can deduct $10,000 annually even though you didn't spend any money that year.

The basis in the property, what you paid plus improvements, gets divided by 27.5 years. You must take depreciation whether you claim it or not; the IRS assumes you did. This means maintaining accurate records from the day you buy your rental property is essential for tax planning purposes.

Personal property inside the rental (appliances, furniture in furnished rentals) depreciates faster, over 5-7 years. This accelerates your tax deductions in early years of ownership.

Repairs are fully deductible in the year you pay them. Fixing a leaky faucet, patching drywall, or repainting walls are repairs. You deduct the full cost immediately on your current tax year return.

Improvements add value or extend the useful life of the property, new roof, HVAC system, or kitchen remodel. These get added to your property basis and depreciated over 27.5 years instead of deducted immediately. Repairing the property differs dramatically from improving it for tax purposes.

The distinction trips up many property owners. Replacing three shingles is a repair; replacing the entire roof is an improvement. Our guide to preparing for tax audits covers exactly how to document repairs versus improvements.

Operating expenses are the day-to-day costs of managing your rental real estate. These include:

Insurance premiums for your rental property are fully deductible. Most landlords pay $1,000-2,000 annually for property insurance, and every dollar reduces taxable income.

Property management fees, typically 8-10% of monthly rent, are deductible. If you pay a property manager $400 monthly to handle tenant issues and collect rental income, that's $4,800 in annual deductions.

Utilities you pay (when not covered by tenants), HOA fees, pest control, lawn care, and snow removal are all deductible. Any expense for maintaining the property in good condition qualifies.

Advertising expenses for finding tenants, Zillow listings, Craigslist ads, signs, are deductible. The cost to market your rental and fill vacancies counts as a legitimate rental expense.

Travel expenses related to your rental activities are deductible. If you drive 30 miles to your rental property for repairs or tenant meetings, you can deduct either actual expenses (gas, maintenance) or the standard mileage rate (67 cents per mile in 2025).

For landlords with properties in different cities, airfare and hotel costs for property inspections or managing renovations are deductible. Keep detailed logs showing the business purpose of each trip.

Fees you pay to tax professionals for preparing Schedule E and calculating rental property deductions are deductible. Legal fees for evictions, lease agreements, or property disputes related to your rental are also deductible.

Many property owners work with specialized tax planning services to maximize deductions and ensure compliance. Professional fees that save you thousands in taxes often pay for themselves several times over.

You report rental income on Schedule E (Supplemental Income and Loss) attached to Form 1040. The top section shows your rental properties by address, and you list rental income received during the tax year.

Below the income line, you deduct eligible expenses in specific categories: advertising, auto and travel, cleaning and maintenance, commissions, insurance, legal and professional fees, mortgage interest, repairs, taxes, utilities, and depreciation.

The result, your net rental income or loss, flows to your Form 1040. If expenses exceed income, you may have a rental loss, though passive activity rules limit how much loss you can deduct against other income unless you qualify for the $25,000 real estate professional exception.

Most residential rental property owners use cash-basis accounting, meaning you report income when received and deduct expenses when paid. This is simpler than accrual accounting and matches how most individuals manage their finances.

Not every expense related to your rental qualifies as a deduction. The IRS excludes several categories that property owners commonly misunderstand.

Your mortgage principal payments aren't deductible, only the interest portion. If your monthly payment is $1,800 and $1,200 is interest, you only deduct the $1,200.

Capital improvements that increase property value get depreciated, not deducted immediately. That $30,000 kitchen remodel doesn't generate a $30,000 deduction in year one; instead, you depreciate it over 27.5 years alongside the property.

Personal use of the property eliminates deductions proportionally. If you rent your property 10 months and use it personally for 2 months, you can only deduct 10/12 of expenses. The IRS watches short-term rental properties closely for this issue.

Expenses incurred before you place the property in service aren't immediately deductible. Costs for searching for rental property to buy, or expenses during the purchase process, get added to your basis instead of deducted as rental expenses.

Maximizing tax deductions starts with documenting every expense from day one. Use separate bank accounts for rental activities so your personal expenses don't mix with rental property expenses.

Track mileage religiously. Use apps like MileIQ or simple spreadsheets, but record the date, destination, miles driven, and business purpose for every trip to your rental property. This creates audit-proof documentation the IRS accepts.

Time major repairs strategically. If you're planning multiple repairs and it's late December, consider accelerating payments into the current tax year to maximize deductions you can claim now rather than waiting until next year.

Consider cost segregation studies for properties over $500,000. These identify personal property components you can depreciate over 5-7 years instead of 27.5 years, accelerating tax savings significantly. Our fractional CFO services include advanced tax planning strategies like this for real estate investors.

Review your rental business structure annually. Some landlords benefit from holding properties in LLCs or S-corps for liability protection and potential tax advantages, though this adds complexity you should evaluate with a tax professional.

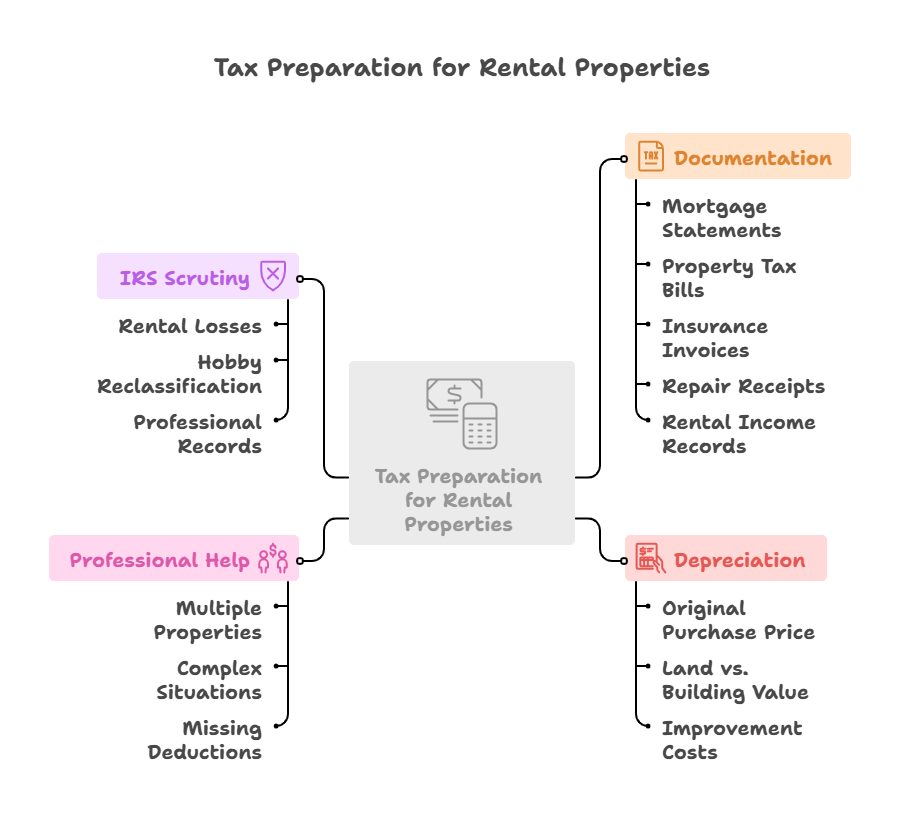

Tax preparation for rental properties requires gathering documentation: mortgage statements (Form 1098), property tax bills, insurance invoices, receipts for repairs, and records of rental income received.

You'll need the property's original purchase price and the value of land versus building (usually from your property tax assessment) to calculate depreciation correctly. If you made improvements, add those costs to your depreciable basis.

Most tax software handles Schedule E, but landlords with multiple properties or complex situations benefit from working with tax professionals who specialize in rental real estate. Missing deductions costs more than professional tax preparation fees in most cases.

The IRS scrutinizes rental losses carefully. If you show rental losses year after year, they may reclassify your rental as a hobby, disallowing deductions and potentially triggering audits of previous tax returns. Maintaining professional records demonstrates you're running a legitimate rental business seeking profit.

You should consider working with a tax professional if you own three or more rental properties, have rental income over $100,000 annually, or experienced major changes like selling a rental or completing large renovations.

Tax professionals catch deductions you miss and structure your rental activities for maximum tax savings. They also provide audit support if the IRS questions your deductions, which gives most landlords significant peace of mind.

Madras Accountancy works with property owners and real estate professionals to prepare tax returns, implement tax planning strategies, and ensure you claim every deduction available under current IRS rules. We've helped landlords reduce tax bills by $5,000-15,000 annually through proper expense tracking and strategic deduction planning.

The cost of professional tax preparation typically ranges from $500-1,500 for rental property owners, depending on complexity. That investment often returns 3-5x in tax savings from deductions and strategies you wouldn't have identified independently. Understanding typical tax preparation costs helps you budget appropriately and evaluate the return on professional services.

Bottom Line: Rental property tax deductions reduce your taxable rental income by 30-40% when you properly track and claim mortgage interest, property taxes, depreciation, repairs, insurance, and operating expenses on Schedule E. Most landlords save $3,000-10,000 annually in federal taxes by documenting all deductible expenses from the day they acquire rental property.

Action Items:

Yes, you can deduct ordinary expenses like mortgage interest, property taxes, insurance, and utilities even during vacancy periods, as long as you're actively trying to rent the property. The IRS considers these legitimate costs of maintaining the property for rental purposes. Keep evidence of your marketing efforts, listing screenshots, ads, showing logs, to prove you intended to rent it.

Repairs maintain the property in its current condition and are fully deductible in the year you pay them, fixing a leak, repainting, replacing broken appliances. Improvements add value or extend the property's useful life and must be depreciated over 27.5 years, new roof, HVAC replacement, kitchen remodel. When in doubt, the IRS uses the "betterment, adaptation, or restoration" test to classify expenses.

Yes, the IRS requires you to claim depreciation whether you actually take the deduction or not. If you don't claim depreciation, the IRS still reduces your cost basis when you sell the property and calculates capital gains as if you had taken it. This means you'll owe more in taxes without receiving any benefit. Always claim depreciation to avoid being taxed twice on the same income.

It depends on your income level and participation. If you actively participate in managing your rental (approving tenants, making decisions) and your adjusted gross income is under $100,000, you can deduct up to $25,000 in rental losses. This phases out completely at $150,000 AGI. If you're a real estate professional spending 750+ hours annually and over 50% of your working time in real estate, you can deduct unlimited losses.

Yes, property management fees are fully deductible as an operating expense in the year you pay them. Whether you pay a property manager 8% of rent or a flat monthly fee, the entire amount reduces your taxable rental income on Schedule E. Keep invoices from your property management company as documentation for your records.

Travel expenses to view properties you already own are deductible, but travel to search for new rental properties to purchase is not immediately deductible. Those search costs get added to the purchase price of the property you eventually buy (increasing your basis) or become personal expenses if you don't purchase anything. Once you own a rental, all related travel becomes deductible.

Keep receipts, invoices, bank statements, and credit card statements for all rental expenses for at least three years after filing your return (seven years is safer). Document mileage with logs showing date, destination, miles, and purpose. Save your closing documents, improvement invoices, and depreciation schedules permanently, you'll need them when you sell the property to calculate capital gains.

Madras Accountancy provides comprehensive tax preparation and planning for property owners, identifying every eligible deduction and structuring your rental activities for maximum tax savings. We've processed returns for 200+ landlords since 2015, reducing tax bills by an average of $7,200 annually through proper expense categorization, depreciation optimization, and strategic tax planning. Our offshore accounting partnership model delivers CPA-quality service at 40% lower cost than traditional firms.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.