.png)

The short-term rental tax loophole lets property investors treat rental income as non-passive, offsetting W-2 wages and business income with accelerated depreciation losses. Combined with cost segregation, investors generate $150,000-$200,000 in first-year deductions on a $500,000 property, cutting tax bills 40-80% in year one.

Sarah, a software engineer earning $180,000, bought a Tennessee vacation rental for $450,000. Her CPA ran a cost segregation study identifying $175,000 in accelerated depreciation. Meeting material participation requirements, she offset her salary with those losses, saving $61,000 in taxes her first year.

This legitimate IRS-recognized strategy works when structured correctly. But most investors miss the opportunity because they don't understand qualification rules or document involvement properly.

Here's everything about the short-term rental tax loophole: exact requirements, maximizing deductions, and avoiding audits.

The short-term rental tax loophole refers to IRS rules that classify certain rental properties as non-passive activities. Unlike traditional long-term rentals where losses can only offset passive income, qualified short-term rental losses offset any income source, including your salary, bonuses, and business profits.

Normally, rental real estate is passive income. But the IRS makes an exception for short-term rentals meeting two criteria: average guest stay of 7 days or less AND substantial services provided to guests. This transforms your rental to non-passive activity. Combined with cost segregation, you generate massive first-year losses that directly reduce taxable income from any source.

Key Statistics:

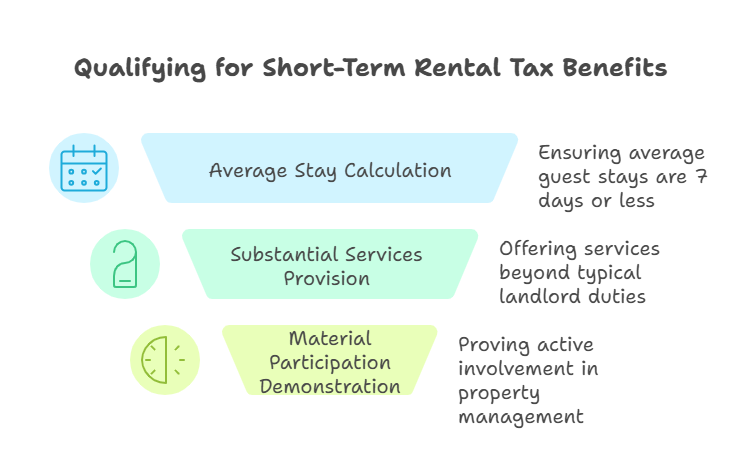

Three requirements must align for this strategy to work:

Requirement 1: Average Stay of 7 Days or Less

Calculate average guest stays across all bookings. Properties on Airbnb and Vrbo typically qualify because platforms favor shorter stays. The IRS looks at your weighted average, so you can have some 14-day bookings as long as the overall average stays below 7 days. Keep detailed booking records with check-in and check-out dates.

Requirement 2: Substantial Services

Provide services beyond typical landlords, daily housekeeping, concierge services, breakfast, or frequent linen changes. Most short-term rental owners meet this through regular cleaning between guests, restocking supplies, and maintaining hotel-like standards. Document every service with photos, receipts, and schedules.

Requirement 3: Material Participation

Spend 100+ hours per year on the rental AND more time than anyone else. Managing bookings, coordinating maintenance, purchasing furniture, responding to messages, all count. If you hire help, prove you're still more involved. Track time meticulously using calendars or detailed logs for audit protection.

Cost segregation accelerates depreciation by reclassifying building components into shorter recovery periods. Instead of depreciating your entire property over 27.5 years, you identify assets qualifying for 5-year, 7-year, or 15-year depreciation.

A $500,000 property breaks down as: $100,000 land (non-depreciable), $200,000 building structure (27.5 years), $120,000 in 5-year property (appliances, carpets, furniture), $50,000 in 7-year property (fixtures), and $30,000 in 15-year property (sidewalks, fencing).

Without cost segregation: $14,545 annual depreciation. With cost segregation and 40% bonus depreciation: $80,000+ in year one. Bonus depreciation lets you immediately write off 40% of shorter-life assets, with remaining basis depreciating normally.

Example for a $500,000 property:

Add operating expenses (mortgage interest, taxes, insurance, utilities, cleaning, supplies), and you generate $150,000-$200,000 in deductions. With $40,000 rental income, you create a $110,000-$160,000 loss offsetting other income.

Many confuse the short-term rental loophole with real estate professional status, they're completely different.

Real estate professional status requires 750+ hours annually in real estate AND more time in real estate than any other work. Difficult for W-2 employees, but unlocks unlimited passive loss deductions across all properties.

The short-term rental loophole needs only 100+ hours per property AND more involvement than anyone else for that property. You don't quit your day job. One well-managed short-term rental generates significant tax benefits while maintaining your career. Real estate professional status requires dedicating your career primarily to property management, a much higher bar.

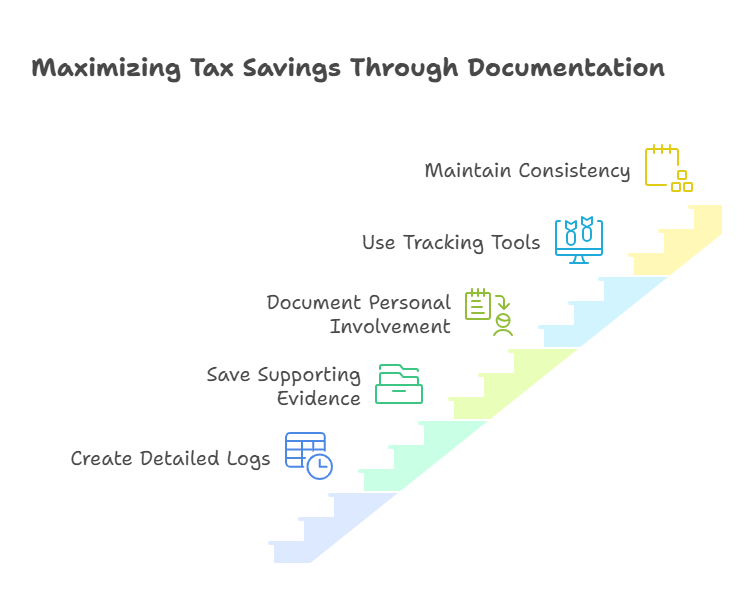

Documentation either proves your case during audits or costs thousands in disallowed deductions plus penalties.

Create detailed logs tracking every hour. Include dates, tasks, and time spent: booking management (inquiries, reservations, check-ins), property maintenance (repairs, inspections, supplies), financial management (bookkeeping, expenses, taxes), and marketing (listings, photos, pricing).

Save supporting evidence, calendar entries, email threads with guests and vendors, receipts, photos, bank statements. If you hire help, document why you're more involved. Show time logs proving you spend more hours than cleaners or managers. Detail tasks you handle personally.

Use Hostfully, Guesty, or spreadsheets for tracking. Consistency matters. Starting documentation after an audit notice is too late, gaps and missing records undermine your entire deduction.

Mistake 1: Claiming Non-Passive Without Meeting Requirements , Reporting losses as non-passive without proving average stay under 7 days or material participation. IRS reclassifies everything as passive and disallows losses against W-2 income.

Mistake 2: Poor Time Tracking , Claiming 100+ hours without real-time records. Reconstructing from memory after audit notices doesn't satisfy IRS standards.

Mistake 3: Aggressive Cost Segregation Without Studies , Estimating allocations without professionals. Professional studies from licensed engineers provide documentation to defend depreciation schedules.

Mistake 4: Mixing Personal and Rental Use , Using property personally for more than 14 days or 10% of rental days limits deductions to rental income only, eliminating loss creation ability.

Year one delivers maximum benefits through accelerated depreciation. Years two through five continue producing depreciation plus operating expenses, many investors still generate tax losses with positive cash flow.

At sale, depreciation recapture applies at 25%, with remaining gains at capital gains rates. Use 1031 exchanges to defer all taxes and continue the strategy indefinitely: acquire property, accelerate depreciation, hold 5-7 years, exchange into larger property. Each exchange resets depreciation while deferring previous taxes.

You need sufficient income to absorb losses. If you earn $60,000 annually, $150,000 in losses provides minimal benefit. The strategy works best for high earners in 32-37% brackets where deductions save $0.32-$0.37 per dollar.

You must genuinely commit to active management, faking participation invites IRS problems. Work with experienced tax professionals to structure involvement legitimately.

Consider long-term goals. Short-term rentals require ongoing effort, guest communication, frequent turnovers, constant marketing. Want passive income you ignore for decades? Traditional rentals suit you better despite smaller tax benefits.

A property qualifies when average guest stay is 7 days or less AND you provide substantial services like daily housekeeping or concierge. Airbnb or Vrbo properties typically meet this with active management and regular turnover.

Yes, with material participation, 100+ hours annually AND more time than anyone else. Qualified short-term rentals are non-passive, letting losses offset wages, bonuses, and business income.

A $500,000 property typically generates $150,000-$200,000 first-year depreciation through cost segregation, creating $40,000-$70,000 in tax savings depending on your bracket. This accelerates 27.5-year deductions into year one.

No. The loophole works WITHOUT real estate professional status. You only need material participation (100+ hours, more than anyone else) per property. Real estate professional status requires 750+ hours across all properties.

Qualifying activities: managing bookings, coordinating cleaning and maintenance, purchasing supplies and furniture, responding to inquiries, marketing, and financial record-keeping. Document with calendars, emails, and receipts.

Bonus depreciation is 40% in 2025 (down from 60% in 2024). After cost segregation identifies 5-year, 7-year, and 15-year assets, immediately deduct 40% of those components. Remaining basis depreciates normally.

Converting to long-term (stays over 30 days) changes the activity to passive. You lose ability to offset non-passive income with new losses, though you can carry forward unused losses for future passive income or property sale.

We've processed 50,000+ tax returns for real estate investors since 2015, including cost segregation, material participation documentation, and tax planning. Our CPAs partner with U.S. firms offshore, reducing costs while maintaining quality.

The short-term rental tax loophole delivers legitimate savings when structured correctly. Meet three requirements, average stay under 7 days, substantial services, and material participation, and offset high W-2 income with accelerated depreciation.

Document everything from day one. Track hours, save communications, and work with tax professionals who understand the nuances. The strategy works when you follow IRS requirements precisely.

About Madras Accountancy: Since 2015, we've served as offshore partners to U.S. CPA firms, processing 50,000+ tax returns with cost segregation analysis, tax planning, and compliance services for real estate investors.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.