On the surface, both long-term leases and short-term stays bring in rent. For tax purposes, the IRS treats them as distinct activities. That difference shapes how you report income, which deductions you can use, and whether losses are trapped as passive or can offset other earnings.

If you are considering converting a traditional rental into a short-term listing—or adding a vacation rental to a portfolio of longer leases—understanding these distinctions ahead of time can prevent unpleasant surprises later.

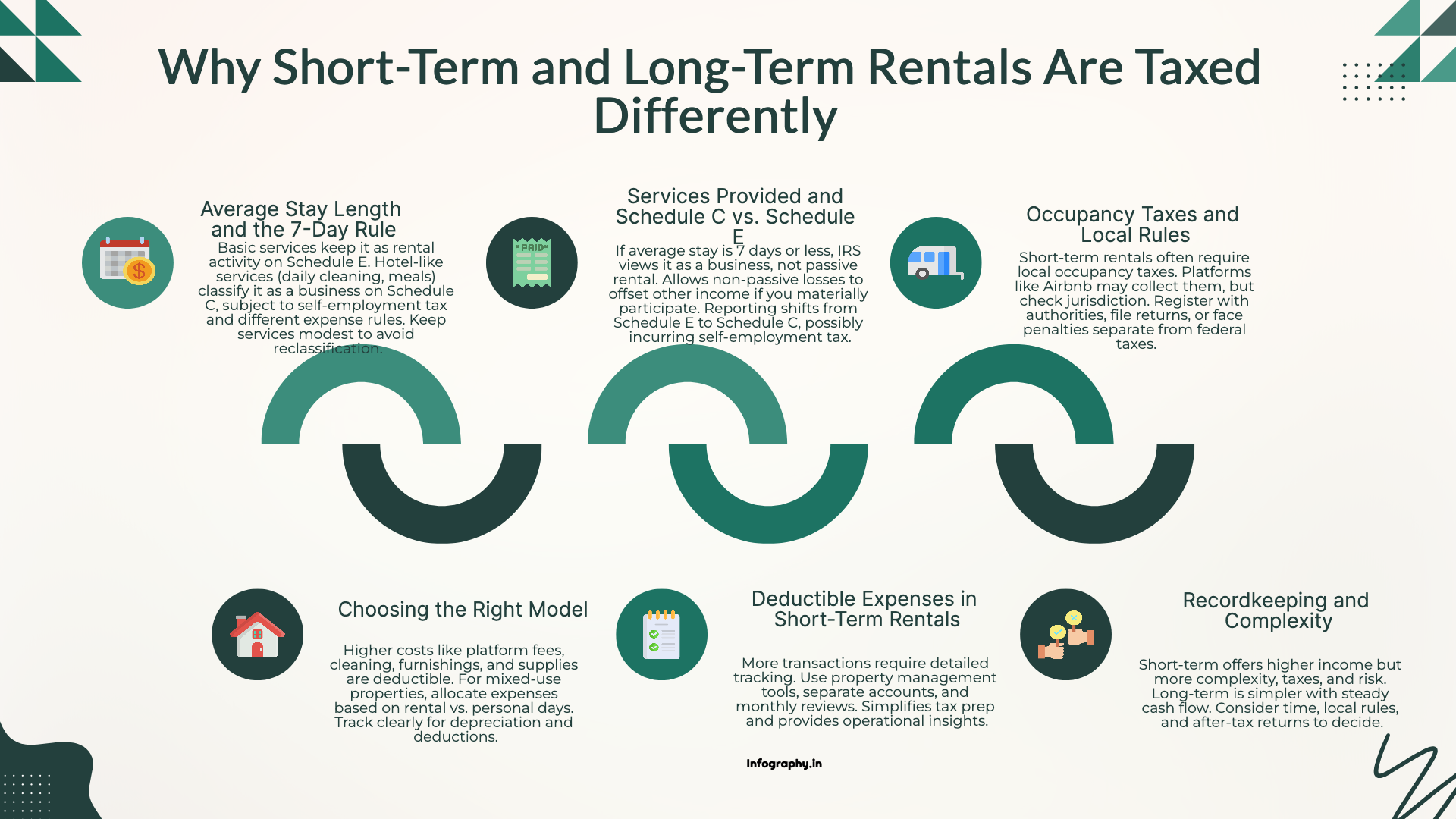

One of the most important dividing lines is how long guests stay on average. Under the passive activity rules, an activity is generally not treated as a rental if the average period of customer use is seven days or less.

When your average stay is very short:

Longer average stays tend to keep the activity squarely in the passive rental category, with income and losses reported on Schedule E.

Beyond length of stay, the level of services you provide also matters. Basic items like utilities, furnishings, and simple check-in processes usually align with rental activity. More hotel-like services—such as daily cleaning, meals, or concierge offerings—push the activity toward being a trade or business.

When an activity crosses that line:

Many hosts aim to keep services modest and standardized to avoid unintentionally turning a rental into something that looks like hospitality income in the eyes of the tax code.

Short-term rentals frequently trigger local occupancy or lodging taxes in addition to income tax. These taxes are often collected at the city or county level and can apply even when you do not think of your property as a "hotel."

Key points include:

Checking the rules where your property sits—and confirming exactly what your booking platform does or does not handle—is an early, important step.

Short-term rentals often involve higher operating costs than long-term leases. Frequent turnovers, higher furnishing standards, and platform fees add up. Many of these costs are deductible, but you need to track them clearly.

Common categories include:

For mixed-use properties—where you use the property personally part of the year and rent it out at other times—allocation rules for expenses and depreciation require special attention. Personal days and rental days affect how much of each cost is deductible.

Short-term rentals typically generate more individual transactions than long-term leases. A single guest stay might involve nightly charges, cleaning fees, platform fees, and taxes—all for a few days' use. Over a year, that creates a dense trail of entries.

Trying to manage this on spreadsheets or with bank statements alone can quickly become unmanageable. Many hosts benefit from:

Clean records make tax preparation smoother and provide useful insight into what is and is not working operationally.

Short-term rentals can produce higher gross income and offer unique tax planning opportunities, but they also bring additional taxes, administrative work, and sometimes higher risk. Long-term rentals tend to be simpler to manage and report, with steadier cash flows and fewer moving parts.

When deciding between models—or considering a mix in your portfolio—ask:

There is no universal best choice. The better path is the one that fits your time, your tolerance for variability, and your overall financial plan. Understanding the tax differences up front lets you make that choice with more clarity and fewer surprises. For more on real estate bookkeeping and outsourcing real estate bookkeeping, see our guides.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.